Notice of Meeting:

I hereby give notice that an ordinary meeting of the Audit

and Risk Subcommittee will be held on:

Date: Tuesday

6 June 2017

Time: 2.00

pm

Venue: Otaru

Room, Civic Centre, The Octagon, Dunedin

Sue Bidrose

Audit and Risk Subcommittee

PUBLIC AGENDA

|

Chairperson

|

Susie Johnstone

|

|

|

|

|

|

|

Members

|

Janet Copeland

|

Mayor Dave Cull (ex

officio)

|

|

|

Cr Doug Hall

|

Cr Mike Lord

|

|

|

Cr Chris Staynes

|

|

Senior Officer Sandy

Graham, General Manager Strategy and Governance

Governance Support Officer Wendy

Collard

Wendy Collard

Governance Support Officer

Telephone: 03 477 4000

Wendy.Collard@dcc.govt.nz

www.dunedin.govt.nz

Note: Reports

and recommendations contained in this agenda are not to be considered as

Council policy until adopted.

|

Audit and Risk Subcommittee

6 June 2017

|

|

ITEM TABLE OF CONTENTS PAGE

1 Apologies 4

2 Confirmation

of Agenda 4

3 Declaration

of Interest 5

4 Confirmation

of Minutes 11

4.1 Audit and Risk Subcommittee meeting - 7

February 2017 11

Part

A Reports (Committee has power to decide these matters)

5 Audit

and Risk Subcommittee Work Plan 2016/17 19

6 Schedule

of Governance/Financial Policies 24

7 Conflict

of Interest Matters 27

8 Long

Term Plan Update - May 2017 30

9 Internal

Audit Policy - Review May 2017 37

Resolution to Exclude the Public 46

|

Audit and Risk Subcommittee

6 June 2017

|

|

1 Apologies

At the close of the agenda no

apologies had been received.

2 Confirmation

of agenda

Note:

Any additions must be approved by resolution with an explanation as to why they

cannot be delayed until a future meeting.

|

Audit and Risk Subcommittee

6 June 2017

|

|

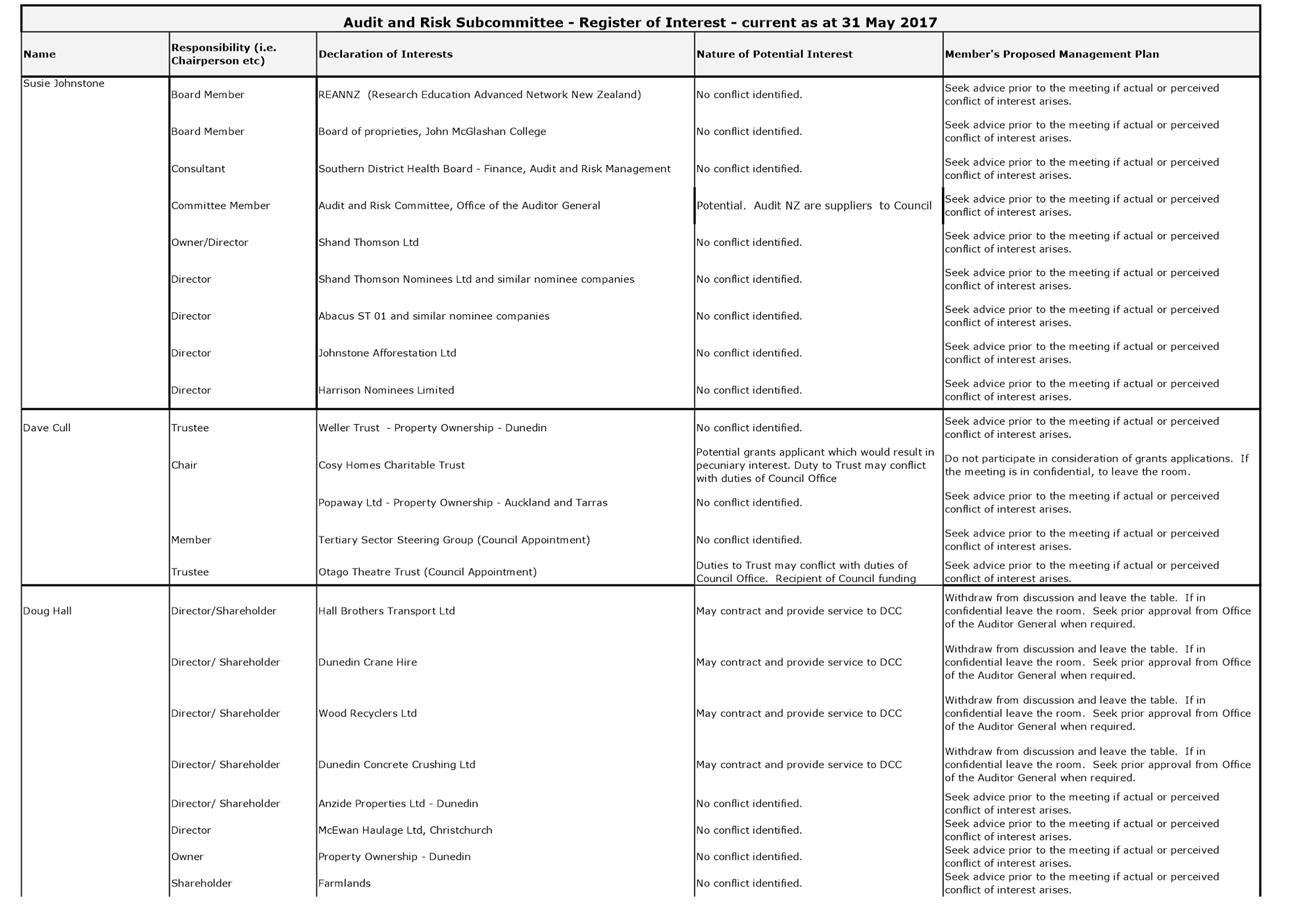

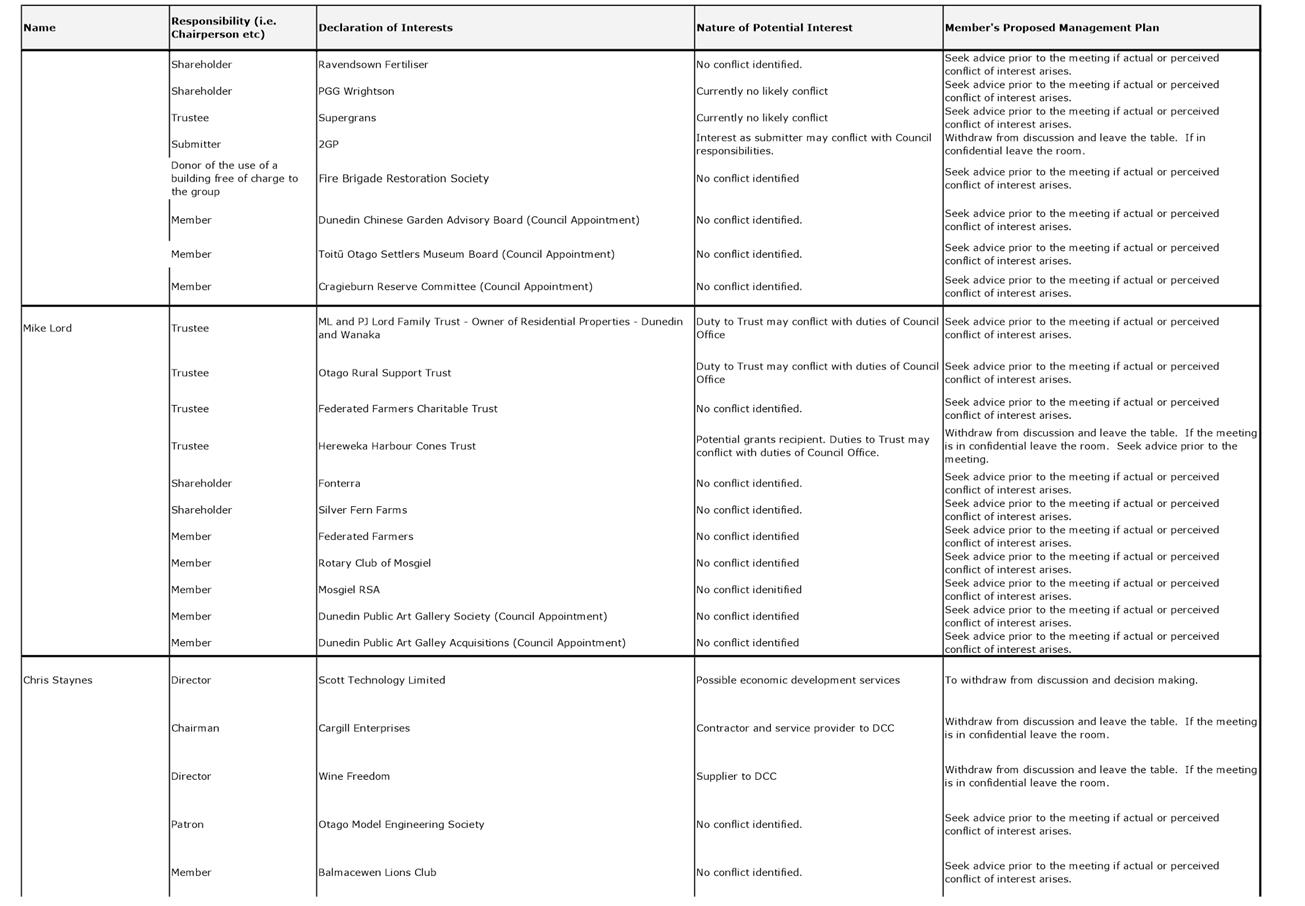

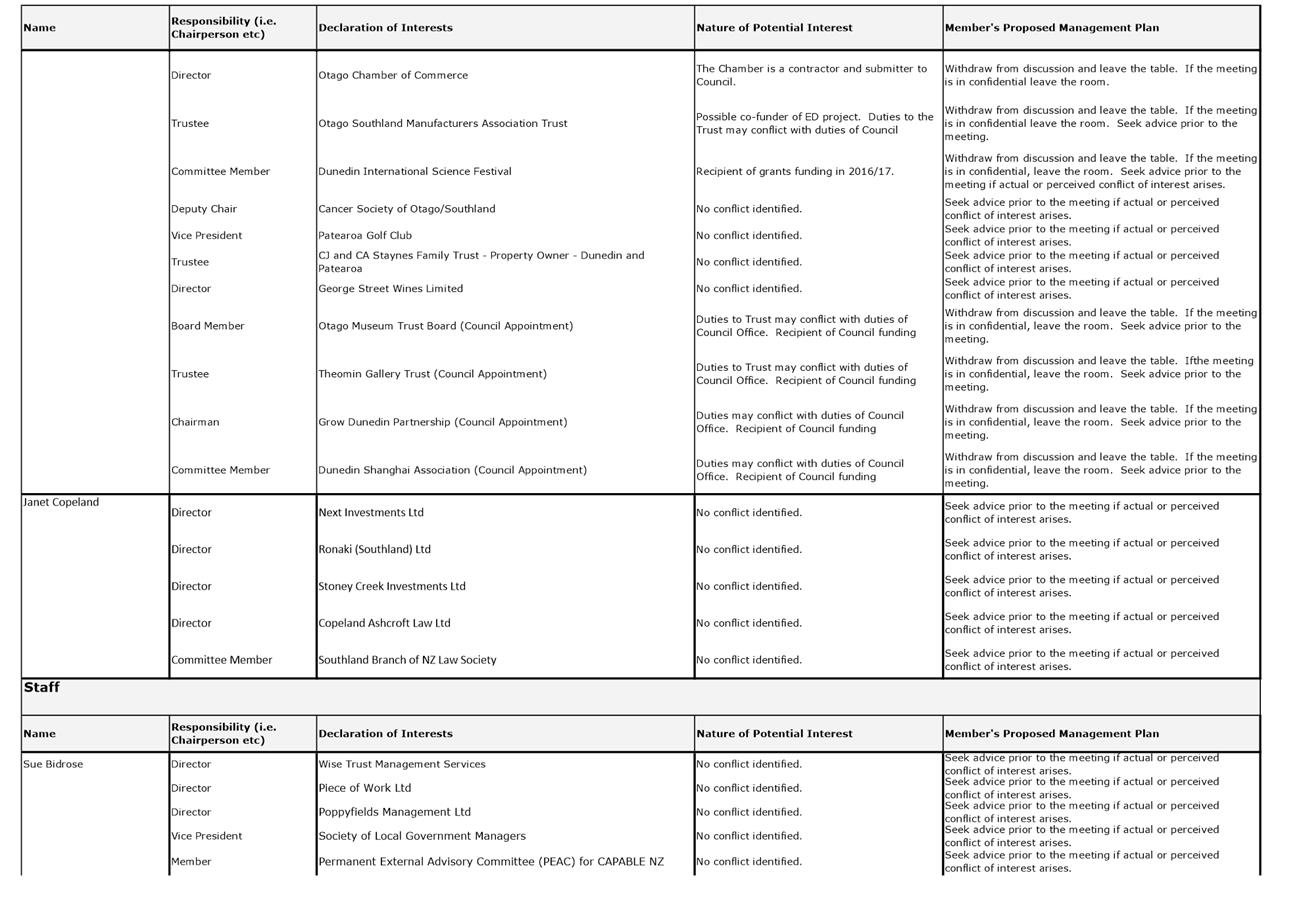

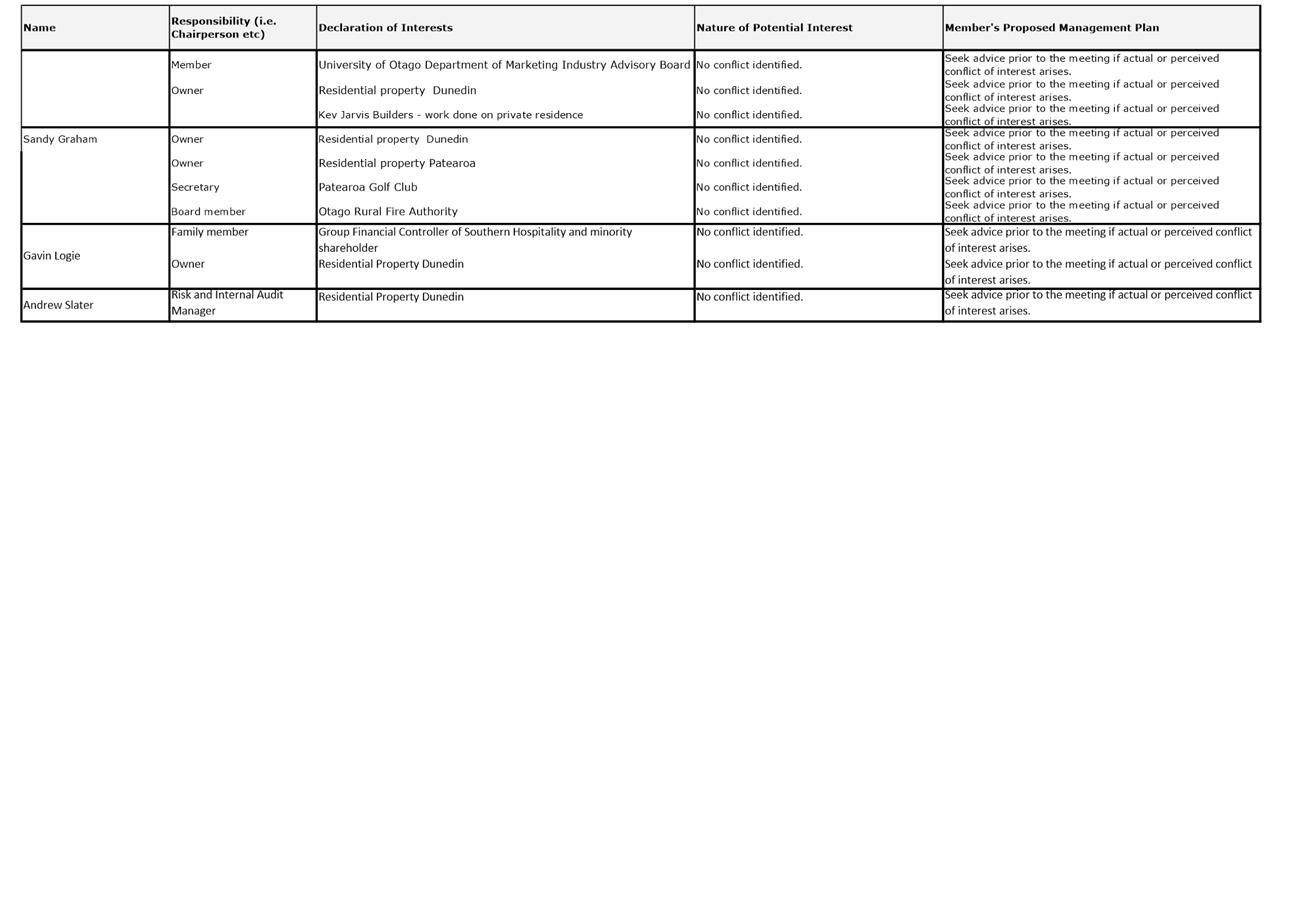

Declaration of Interest

EXECUTIVE SUMMARY

1. Members are reminded of the need

to stand aside from decision-making when a conflict arises between their role

as an elected representative or independent member and any private or other

external interest they might have.

2. Elected

members and independent members are reminded to update their

register of interests as soon as practicable, including amending the register

at this meeting if necessary.

|

RECOMMENDATIONS

That the Committee:

a) Notes/Amends

if necessary the Elected or Independent Members' Interest Register attached

as Attachment A; and

b) Confirms/Amends the proposed management plan for Elected or Independent Members'

Interests.

|

Attachments

|

|

Title

|

Page

|

|

a

|

Members' Register of

Interest

|

7

|

|

Audit and Risk Subcommittee

6 June 2017

|

|

|

Audit and Risk Subcommittee

6 June 2017

|

|

|

Audit and Risk Subcommittee

6 June 2017

|

|

|

Audit and Risk Subcommittee

6 June 2017

|

|

|

Audit and Risk Subcommittee

6 June 2017

|

|

Confirmation

of Minutes

Audit and Risk Subcommittee meeting - 7 February 2017

|

RECOMMENDATIONS

That the Committee:

Confirms the public part of the minutes of

the Audit and Risk Subcommittee meeting held on 7 February 2017 as a correct

record.

|

Attachments

|

|

Title

|

Page

|

|

A

|

Minutes of Audit and

Risk Subcommittee meeting held on 7 February 2017

|

12

|

Audit and Risk Subcommittee

UNCONFIRMED MINUTES

Unconfirmed minutes of an

ordinary meeting of the Audit and Risk Subcommittee held in the Otaru Room,

Civic Centre, The Octagon, Dunedin on Tuesday 07 February 2017, commencing at

2.07 pm

PRESENT

|

Chairperson

|

Susie Johnstone

|

|

|

Members

|

Cr Doug Hall

|

Cr Mike Lord

|

|

|

Cr Chris Staynes

|

|

|

IN ATTENDANCE

|

Sandy Graham (General Manager,

Strategy and Governance), Gavin Logie (Acting Chief Financial Officer),

Andrew Slater (Risk and Internal Audit Manager) and Martyn Solomon (Senior

Client Manager – Audit and Assurance, Crowe Horwath)

|

Governance Support Officer Wendy

Collard

|

1 Apologies

|

|

|

Moved (Cr Chris Staynes/Cr Mike Lord):

That the Committee:

Accepts the apologies

from Janet Copeland and Mayor Dave Cull.

Motion

carried (AR/2017/001)

|

|

2 Confirmation

of agenda

|

|

|

Moved (Susie Johnstone/Cr Chris Staynes):

That the Subcommittee:

Confirms the agenda with

the following alterations:

1 That

Item C8 - Update on the DCC Internal Audit Workplan – January 2017 be

taken before Item C3 due to the availability of staff from Crowe Horwath

2 That

part of Item C7 - Internal Audit Outcomes Report, January 2017 be taken

before Item C3 due to the availability of staff from Crowe Horwath.

Motion

carried (AR/2017/002)

|

3 Declarations

of interest

Members were

reminded of the need to stand aside from decision-making when a conflict arose

between their role as an elected representative and any private or other

external interest they might have.

There were no

declarations of interest made or conflicts of interest declared.

|

|

Moved (Susie Johnstone/Cr Mike Lord):

That the Subcommittee:

a) Notes the

Members' Interest Register attached as Attachment A; and

b) Confirms the

proposed management plan for members’ interests.

Motion

carried (AR/2017/003)

|

Minutes

of Committees

|

4 Audit

and Risk Subcommittee - 14 December 2016

|

|

|

Moved (Cr Mike Lord/Cr Doug Hall):

That the Committee:

a) Confirms

the public part of the minutes of the Audit and Risk Subcommittee meeting

held on 14 December 2016 as a correct record.

Motion

carried (AR/2017/004)

|

|

|

It was agreed that training on Standing Orders would be provided

to Susie Johnstone and Janet Copeland.

|

|

|

|

Part

A Reports

|

5 Audit

and Risk Subcommittee Work Plan 2016/17

|

|

|

A report from Civic provided a copy of the updated Audit

and Risk Subcommittee Work Plan 2016/17. There was discussion on the

work plan and it was agreed that the Chairperson and the General Manager

Strategy and Governance (Sandy Graham) would give consideration to the

prioritisation for future meetings.

|

|

|

Moved (Cr Mike Lord/Cr Chris Staynes):

That the Subcommittee:

a) Notes the

Audit and Risk Subcommittee Work Plan 2016/17.

Motion

carried (AR/2017/005)

|

|

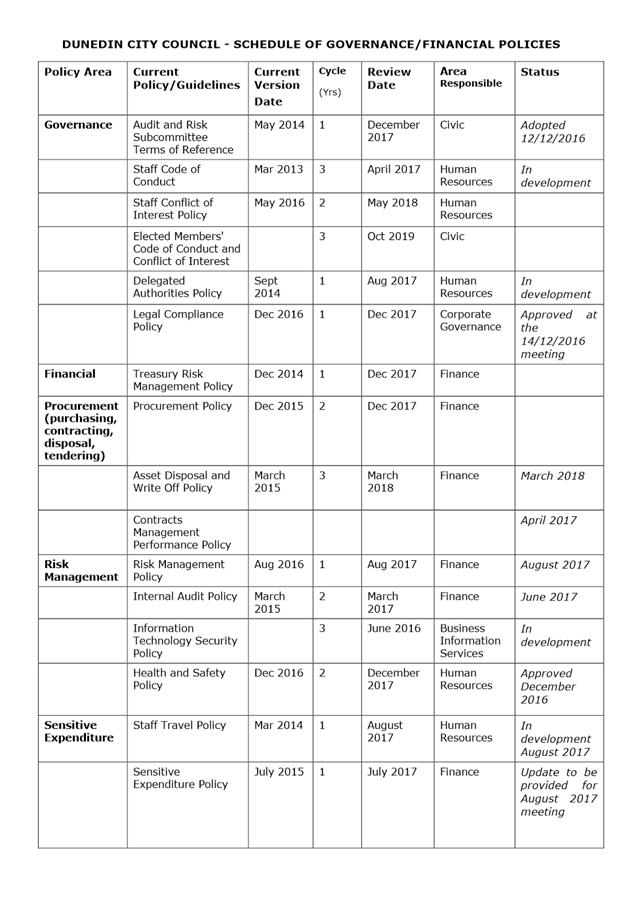

6 Schedule

of Governance/Financial Policies

|

|

|

The report

from Civic provided a copy of the updated Schedule of Governance/Financial

Policies.

There was

discussion on the review dates and cycle of policies and the Audit and Risk

Subcommittee recommended that the review date for some policies on an annual

or biannual cycle could be amended to a longer term.

|

|

|

|

|

|

Moved (Chairperson Susie Johnstone/Cr Chris Staynes):

That the Subcommittee:

a) Notes the

Schedule of Governance/Financial Policies

Motion

carried (AR/2017/006)

|

|

7 Long

Term Plan update - January 2017

|

|

|

A report from Community and Planning provided an update

and high level timetable on the development of the Long Term Plan. It

noted that the timetable had been approved by the Executive Leadership Team

on 30 January 2017.

The General Manager Strategy and Governance (Sandy Graham)

commented that the Long Term Plan (LTP) Core Project Team had developed the

LTP approach; work stream responsibilities; draft LTP timetable; Councillor

engagement; and staff engagement. Ms Graham noted that the LTP Project

planning was six months ahead of schedule and advised that the touch points

with Audit NZ and the Audit and Risk Subcommittee would be added.

Following discussion it was agreed that regular reporting

on the Long Term Plan would be presented to the Audit and Risk Subcommittee.

|

|

|

Moved (Chairperson Susie Johnstone/Cr Mike Lord):

That the Subcommittee:

a) Notes the

Long Term Plan Update – January 2017 report.

Motion

carried (AR/2017/007)

|

|

Resolution

to exclude the public

|

|

Moved (Cr Chris Staynes/Cr Doug Hall):

That the Subcommittee:

Pursuant

to the provisions of the Local Government Official Information and Meetings

Act 1987, exclude the public from the following part of the proceedings of

this meeting namely:

|

General

subject of the matter to be considered

|

Reasons

for passing this resolution in relation to each matter

|

Ground(s) under

section 48(1) for the passing of this resolution

|

Reason for

Confidentiality

|

|

C1

Audit and Risk Subcommittee - 14 December 2016 - Public Excluded

|

S7(2)(j)

The

withholding of the information is necessary to prevent the disclosure or

use of official information for improper gain or improper advantage.

|

S48(1)(a)

The public conduct of the part of the meeting

would be likely to result in the disclosure of information for which good

reason for withholding exists under section 7.

|

|

|

C2

Audit and Risk Subcommittee Action List Report

|

S7(2)(c)(ii)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or

could be compelled to provide under the authority of any enactment, where

the making available of the information would be likely to damage the

public interest.

|

S48(1)(a)

The public conduct of the part of the meeting

would be likely to result in the disclosure of information for which good

reason for withholding exists under section 7.

|

|

|

C3

Compliance with the Treasury Risk Management Policy

|

S7(2)(b)(ii)

The

withholding of the information is necessary to protect information where

the making available of the information would be likely unreasonably to

prejudice the commercial position of the person who supplied or who is the

subject of the information.

S7(2)(h)

The

withholding of the information is necessary to enable the local authority

to carry out, without prejudice or disadvantage, commercial activities.

|

S48(1)(a)

The public conduct of the part of the meeting

would be likely to result in the disclosure of information for which good

reason for withholding exists under section 7.

|

|

|

C4

Health and Safety Monthly Report for November 2016

|

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of

natural persons, including that of a deceased person.

|

S48(1)(a)

The public conduct of the part of the meeting

would be likely to result in the disclosure of information for which good

reason for withholding exists under section 7.

|

|

|

C5

Fraud Prevention Policy and Procedure

|

S7(2)(h)

The

withholding of the information is necessary to enable the local authority

to carry out, without prejudice or disadvantage, commercial activities.

|

S48(1)(a)

The public conduct of the part of the meeting

would be likely to result in the disclosure of information for which good

reason for withholding exists under section 7.

|

|

|

C6

DCC Strategic Risk Register Update - January 2017

|

S7(2)(c)(ii)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or

could be compelled to provide under the authority of any enactment, where

the making available of the information would be likely to damage the

public interest.

|

S48(1)(a)

The public conduct of the part of the meeting

would be likely to result in the disclosure of information for which good

reason for withholding exists under section 7.

|

|

|

C7

Internal Audit Outcomes Report - January 2017

|

S7(2)(c)(ii)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or

could be compelled to provide under the authority of any enactment, where

the making available of the information would be likely to damage the

public interest.

|

S48(1)(a)

The public conduct of the part of the meeting

would be likely to result in the disclosure of information for which good

reason for withholding exists under section 7.

|

|

|

C8

Update on the DCC Internal Audit Workplan - January 2017

|

S7(2)(b)(ii)

The

withholding of the information is necessary to protect information where

the making available of the information would be likely unreasonably to

prejudice the commercial position of the person who supplied or who is the

subject of the information.

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or

could be compelled to provide under the authority of any enactment, where

the making available of the information would be likely to prejudice the

supply of similar information or information from the same source and it is

in the public interest that such information should continue to be

supplied.

S7(2)(h)

The

withholding of the information is necessary to enable the local authority

to carry out, without prejudice or disadvantage, commercial activities.

|

S48(1)(a)

The public conduct of the part of the meeting

would be likely to result in the disclosure of information for which good

reason for withholding exists under section 7.

|

|

|

C9

Protected Disclosure Register

|

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of

natural persons, including that of a deceased person.

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or

could be compelled to provide under the authority of any enactment, where

the making available of the information would be likely to prejudice the

supply of similar information or information from the same source and it is

in the public interest that such information should continue to be

supplied.

|

S48(1)(a)

The public conduct of the part of the meeting

would be likely to result in the disclosure of information for which good

reason for withholding exists under section 7.

|

|

|

C10

Investigation Register

|

S6(b)

The

making available of the information would be likely to endanger the safety

of a person.

|

S48(1)(a)

The public conduct of the part of the meeting

would be likely to result in the disclosure of information for which good

reason for withholding exists under section 6.

|

The matters detailed

in this report are subject to investigation and information should remain

confidential so as not to prejudice the investigation and any possible

outcomes of the investigation..

|

|

C11

Purchase Card Report

|

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of

natural persons, including that of a deceased person.

|

S48(1)(a)

The public conduct of the part of the meeting

would be likely to result in the disclosure of information for which good

reason for withholding exists under section 7.

|

This report is

confidential because it refers and impacts Council staff positions where

those staff have not had the opportunity to respond or comment on the

report..

|

This resolution is made in

reliance on Section 48(1)(a) of the Local Government Official Information and

Meetings Act 1987, and the particular interest or interests protected by

Section 6 or Section 7 of that Act, or Section 6 or Section 7 or Section 9 of

the Official Information Act 1982, as the case may require, which would be

prejudiced by the holding of the whole or the relevant part of the

proceedings of the meeting in public are as shown above after each item.

That Martyn Solomon (Senior Client Manager – Audit

and Assurance) be permitted to attend the meeting, after the public has been

excluded, because of his knowledge of Items C8. This knowledge, which

will be of assistance in relation to the matters to be discussed, is relevant

because he will be reporting on the items under consideration.

Motion

carried (AR/2017/008)

|

The meeting moved into

non public at 2.25pm.

..............................................

CHAIRPERSON

|

Audit and Risk Subcommittee

6 June 2017

|

|

Part

A Reports

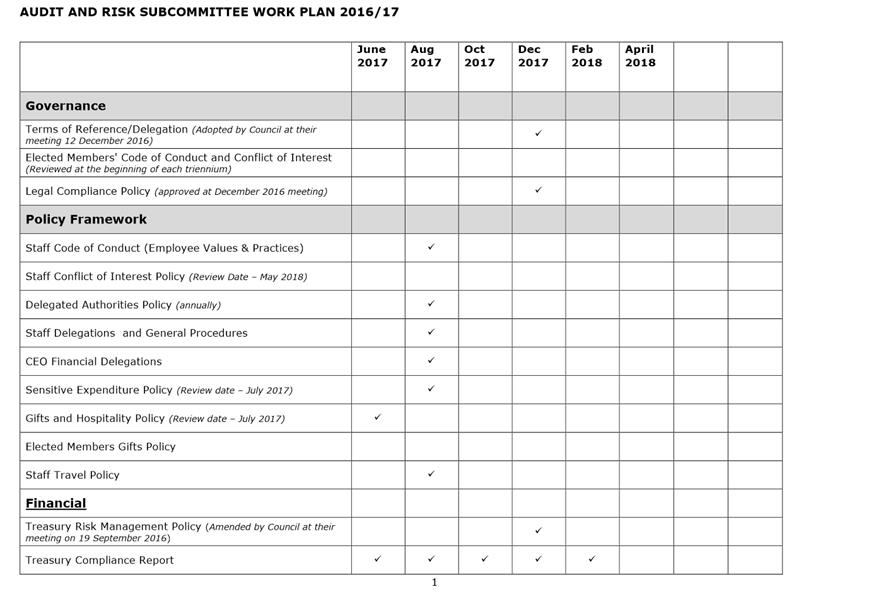

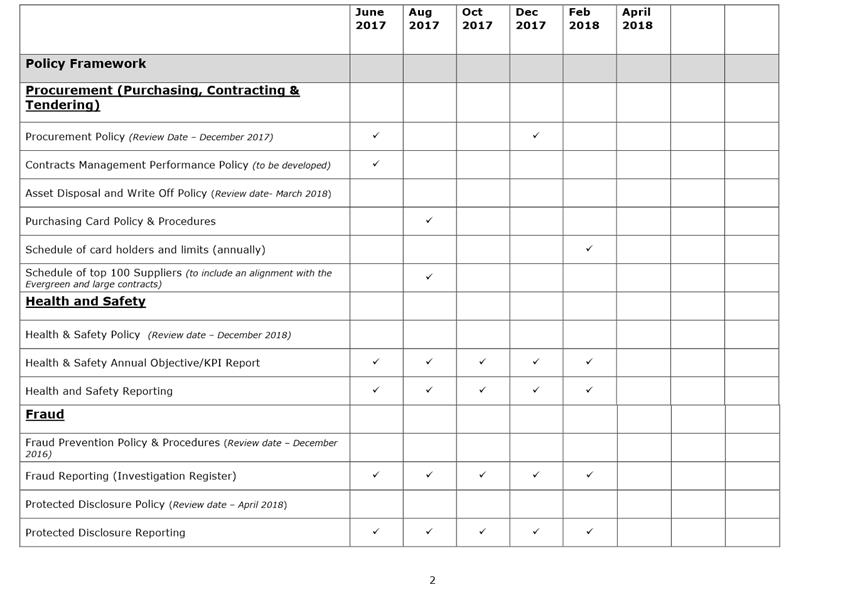

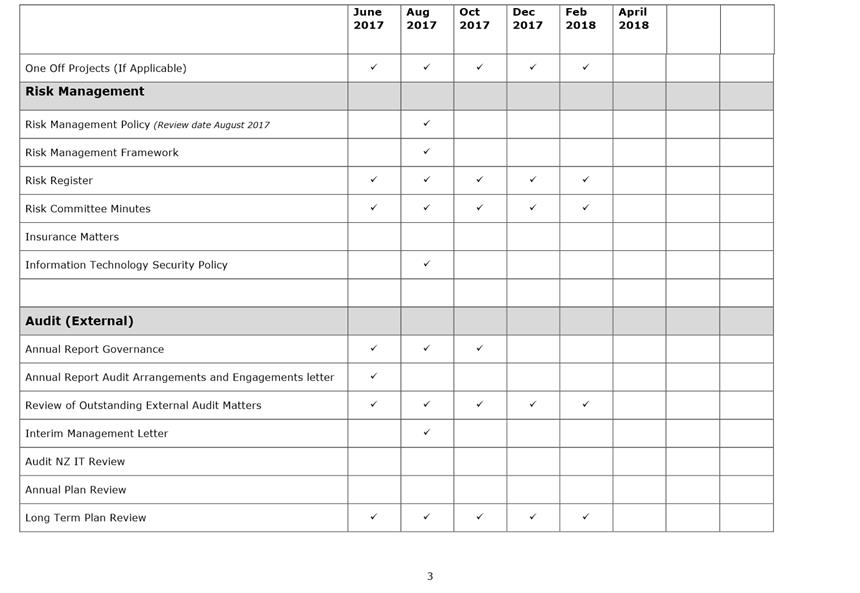

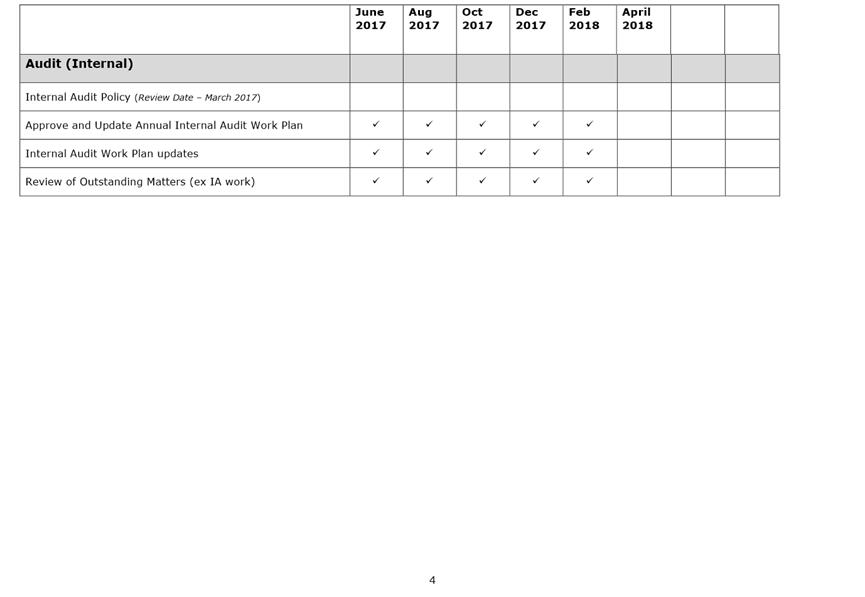

Audit and Risk Subcommittee Work Plan 2016/17

Department: Civic and Legal

EXECUTIVE SUMMARY

1 This

report provides a copy of the updated Audit and Risk Subcommittee Work Plan

2016/17. As this is an administrative report only, the Summary of

Considerations is not required.

2 It should

be noted that the items without ticks shown have not been scheduled for action

in the 2016/17 year.

|

RECOMMENDATIONS

That the Committee:

a) Notes the

Audit and Risk Subcommittee Work Plan 2016/17.

|

Signatories

|

Author:

|

Wendy Collard - Governance Support Officer

|

|

Authoriser:

|

Kristy Rusher - Manager Civic and Legal

|

Attachments

|

|

Title

|

Page

|

|

a

|

Audit and Risk

Subcommittee workplan

|

20

|

|

Audit and Risk Subcommittee

6 June 2017

|

|

|

Audit and Risk Subcommittee

6 June 2017

|

|

Schedule of Governance/Financial Policies

Department: Civic and Legal

EXECUTIVE SUMMARY

1 This

report provides a copy of the updated Schedule of Governance/Financial

Policies. As this is an administrative report only, the Summary of

Considerations is not required.

|

RECOMMENDATIONS

That the Committee:

a) Notes the

Schedule of Governance/Financial Policies

|

Signatories

|

Author:

|

Wendy Collard - Governance Support Officer

|

|

Authoriser:

|

Kristy Rusher - Manager Civic and Legal

|

Attachments

|

|

Title

|

Page

|

|

a

|

Schedule of

Governance/Financial Policies

|

25

|

|

Audit and Risk Subcommittee

6 June 2017

|

|

|

Audit and Risk Subcommittee

6 June 2017

|

|

Conflict of Interest Matters

Department: Office of the Chief Executive

EXECUTIVE SUMMARY

1 This

report provides information on how Interest Registers are dealt with in other

authorities and also provides guidance on best practice from the Office of the

Auditor General.

|

RECOMMENDATIONS

That the Committee:

a) Confirms that

the complete Register of Interests should be part of the agenda for all

Council and Committee meetings in line with best practice.

b) Recommends that

changes to the Register of Interest are highlighted by way of “bold”

for additions or “strikethrough” for deletions.

|

BACKGROUND

2 Since the

beginning of the new triennium, all Council and Committee agendas include a

copy of the Elected Members’ Interest Register and are accompanied by an

administrative report that notes and confirms that there are management plans

in place for any interests that may arise in the course of the meeting.

DISCUSSION

3 At the

Council meeting on 28 March 2017, there was discussion about the need and/or

desirability for the Interest Register to be attached to all agendas.

4 Advice

was provided at the meeting that the Dunedin City Council approach represented

best practice in the sector and aligned with the approach taken by the Office

of the Auditor General.

5 Following

that discussion, it was agreed that the matter would be considered by the Audit

and Risk Subcommittee at its next meeting.

6 Since the

Council meeting, governance staff have made contact with other local authorities

to determine what approaches are taken to this matter. Many Councils spoken to

publish the register on their websites (as does Dunedin City Council) but they

do not include it with agendas.

7 Nelson

City Council publishes the full register as an administrative report every

second Council meeting.

8 When

spoken to some of the larger metropolitan councils indicated they were

reviewing how they managed and reported elected member interests and many are

considering the approach being taken by the Dunedin City Council.

9 In

discussions with other Councils various management techniques were identified

that made the collation and review of the register more efficient.

10 When publishing

registers to their websites, some Councils highlight or bold any interests that

have been added to the register since it was last published. They also

“strikethrough” any items that have been deleted.

11 This approach could

be applied to the Dunedin City Council register whereby the register as

published on each Council agenda would show any changes made since the previous

Council meeting. This would address the concern of some members that it was

very difficult to know what had changed while still providing the information

in a fully transparent way.

OPTIONS

Option

One – Continue to publish the full Register on all agendas but with

changes highlighted - Recommended Option

12 This option

continues the current best practice while providing an easy visual reference to

those interests that have been changed. There are no identified disadvantages

with this option.

Option

Two – Change the frequency that the Register is published on agendas

13 This option is not

recommended as it does not align with the Office of the Auditor General’s

views on best practice and would mean a decrease in transparency around the

management of conflicts of interest.

NEXT STEPS

14 If the recommended

option is approved, governance staff will highlight changes to the registers in

future. Councillors will be advised of the new approach.

Signatories

|

Author:

|

Sandy Graham - General Manager Strategy and Governance

|

|

Authoriser:

|

Sue Bidrose - Chief Executive Officer

|

Attachments

There are no attachments for

this report.

|

SUMMARY OF CONSIDERATIONS

|

|

Fit with purpose

of Local Government

This report enables democratic local decision making and

action by, and on behalf of communities.

|

|

Fit with strategic

framework

|

|

Contributes

|

Detracts

|

Not applicable

|

|

Social Wellbeing Strategy

|

☐

|

☐

|

☐

|

|

Economic Development Strategy

|

☐

|

☐

|

☐

|

|

Environment Strategy

|

☐

|

☐

|

☐

|

|

Arts and Culture Strategy

|

☐

|

☐

|

☐

|

|

3 Waters Strategy

|

☐

|

☐

|

☐

|

|

Spatial Plan

|

☐

|

☐

|

☐

|

|

Integrated Transport Strategy

|

☐

|

☐

|

☐

|

|

Parks and Recreation Strategy

|

☐

|

☐

|

☐

|

|

Other strategic projects/policies/plans

|

☐

|

☐

|

☐

|

This report is administrative

|

|

Māori Impact

Statement

There are no known impacts for tangata whenua

|

|

Sustainability

There are no implications for sustainability.

|

|

LTP/Annual Plan /

Financial Strategy /Infrastructure Strategy

There are no implications.

|

|

Financial

considerations

This report is administrative and has no financial

implications.

|

|

Significance

This matter is of low significance in terms of the

Significance and Engagement Policy.

|

|

Engagement –

external

There has been external engagement with a range of other

local authorities.

|

|

Engagement -

internal

The in-house legal team were consulted.

|

|

Risks: Legal /

Health and Safety etc.

None identified.

|

|

Conflict of

Interest

This report deals specifically with managing potential

conflicts of interest.

|

|

Community Boards

Any changes made as a result of the report will apply to

Community Boards.

|

|

Audit and Risk Subcommittee

6 June 2017

|

|

Long Term Plan Update - May 2017

Department: Strategy and Governance

EXECUTIVE SUMMARY

1 This

report provides the Audit and Risk Subcommittee with an update on the

development of the Long Term Plan 2018 (LTP), as at 30 May 2017.

2 The LTP

project is currently on track. The Council considered a “Long Term Plan

update and first round of supporting documents” report on 30 May 2017.

This included information on the draft community outcomes and strategic

forecasting assumptions (e.g. population and dwelling growth; climate change

variables).

3 Council

has asked for more work to be undertaken to develop the proposed Community

Headline Indicators.

4 Over the

last three months, the LTP project has been focussed on establishing LTP

project management, process and structure; LTP workstreams; staff engagement;

and initiating work on some of the LTP deliverables. Of note:

5 LTP

health check and quality assurance: The LTP project team has utilised the

SOLGM 'health check' and quality assurance tools to assess the effectiveness

and readiness of our systems and processes for the LTP delivery. SOLGM quality

assurance checks have been scheduled in the LTP Project Plan – to be

undertaken every three months.

6 LTP

audit working group: To ensure the project and delivery documents benefit

fully from the audit process, an LTP audit staff working group, led by the DCC

Internal Audit and Risk Manager has been established to facilitate the

relationship with Audit New Zealand and support quality assurance. LTP

Project staff will attend an Audit NZ update on 7 June 2017,

following which key audit/ assurance milestones will be embedded within the LTP

Timetable.

7 It is

anticipated that Audit NZ will undertake a review of Council documentation

prior to being tabled at the Council meeting (December 2017), and then again

following that meeting (anticipated late 2017/ early 2018). This will then be

followed by a final review of Council's LTP prior to completion (May/ June

2018).

8 Relevant

comments and recommendations from the Office of the Auditor General regarding

the 2015/16 Long Term Plans have also been disseminated with Councillors and

key project staff and managers for their consideration in the development and

delivery of the LTP.

9 Group

management plans: Group Managers are developing Group Management Plans

(GMPs) as an alternative to Activity Management Plans. The GMPs will

include mandatory LTP components (e.g. service rationale, contribution to

community outcomes, service levels, and significant negative effects); asset

management summaries; major projects and programmes summary; and key

performance measures.

10 The GMPs will also

include a risk profile for each Group that maps the range of risks, controls

and residual exposure levels to core Group activities, and to the delivery of

Council’s strategic objectives.

11 Councillor

engagement: A series of five LTP workshops have been included to facilitate

and enable Councillor involvement in the development of the LTP. The first two

LTP workshops were convened in May focussed on strategic direction setting for

the LTP; and the capital expenditure programme.

12 Staff engagement:

Workshops were convened in February for staff to learn about some of the

critical parts of the LTP and understand how their work feeds into, and builds

on the LTP. A focus group was convened on 16 March 2017 to seek feedback on

some early LTP-related work.

|

RECOMMENDATIONS

That the Committee:

a) Notes the

Long Term Plan – Project Plan, as at 30 May 2017.

|

Signatories

|

Author:

|

Andrew Slater - Risk and Internal Audit Manager

|

|

Authoriser:

|

Sandy Graham - General Manager Strategy and Governance

|

Attachments

|

|

Title

|

Page

|

|

a

|

LTP Project Plan - May

2017

|

35

|

|

SUMMARY OF CONSIDERATIONS

|

|

Fit with purpose

of Local Government

The

development of the LTP enables democratic local decision making and action

by, and on behalf of communities; and meets the current and future needs of

the Dunedin communities for good quality public services in a way that is

most cost effective for households and businesses.

|

|

Fit with strategic

framework

|

|

Contributes

|

Detracts

|

Not applicable

|

|

Social Wellbeing Strategy

|

☒

|

☐

|

☐

|

|

Economic Development Strategy

|

☒

|

☐

|

☐

|

|

Environment Strategy

|

☒

|

☐

|

☐

|

|

Arts and Culture Strategy

|

☒

|

☐

|

☐

|

|

3 Waters Strategy

|

☒

|

☐

|

☐

|

|

Spatial Plan

|

☒

|

☐

|

☐

|

|

Integrated Transport Strategy

|

☒

|

☐

|

☐

|

|

Parks and Recreation Strategy

|

☒

|

☐

|

☐

|

|

Other strategic projects/policies/plans

|

☒

|

☐

|

☐

|

The

LTP contributes to all of the objectives and priorities of the strategic

framework as it describes the Council’s activities; the community

outcomes; and provides a long term focus for decision making and coordination

of the Council’s resources, as well as a basis for community

accountability.

|

|

Māori Impact

Statement

The

LTP provides a mechanism for Māori to contribute to local

decision-making.

|

|

Sustainability

The

LTP contains content regarding the Council’s approach to

sustainability. Major issues and implications for sustainability are

discussed in the 30 year Infrastructure Strategy and financial resilience is

discussed in the Financial Strategy.

|

|

LTP/Annual Plan /

Financial Strategy /Infrastructure Strategy

This

report provides an update on the development of the LTP 2018-2028.

|

|

Financial

considerations

There

are no financial implications.

|

|

Significance

This

report is considered low significance in terms of the Council’s

Significance and Engagement Policy.

|

|

Engagement –

external

There

will be extensive community engagement throughout the development of the LTP

2018-2028. Advice has been sought from AECOM and Rationale in the development

of the strategic significant forecasting assumptions.

|

|

Engagement -

internal

Staff

and managers from across the Council are involved in the development of the

LTP 2018-2028.

|

|

Risks: Legal /

Health and Safety etc.

There

is some degree of strategic risk exposure, arising from a potential failure

to meet Council statutory obligations pertaining to the delivery of the LTP.

This report provides an update on the LTP project activities underway to

manage and mitigate this risk.

|

|

Conflict of

Interest

There

are no known conflicts of interest.

|

|

Community Boards

Community

Boards will be involved in the development of the LTP 2018-2028.

|

|

Audit and Risk Subcommittee

6 June 2017

|

|

|

Audit and Risk Subcommittee

6 June 2017

|

|

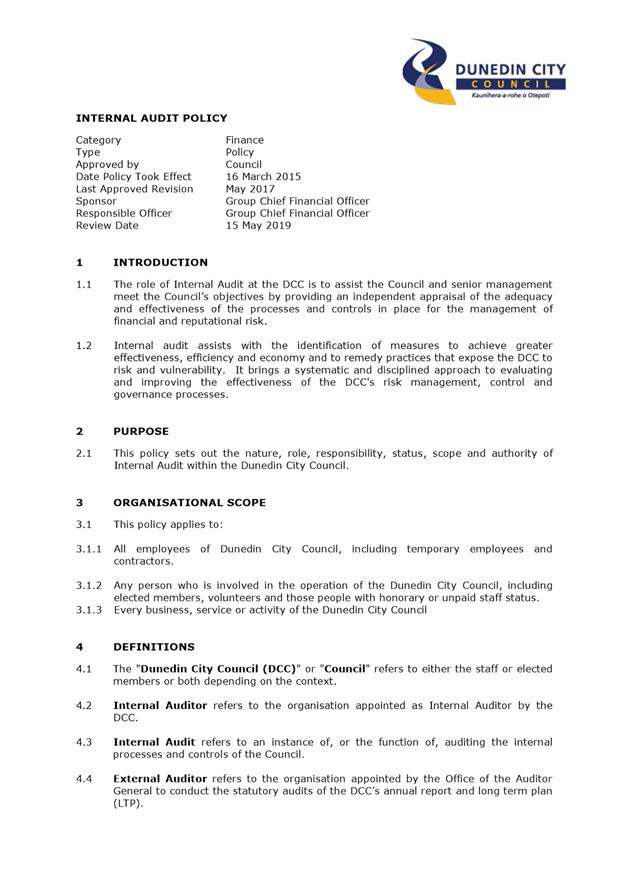

Internal Audit Policy - Review May 2017

Department: Strategy and Governance

EXECUTIVE SUMMARY

1 The

Internal Audit Policy was tabled and approved by Council on 16 March 2015, and

assigned a review date of March 2017.

2 The

Internal Audit Policy has been reviewed by ELT in May 2017, with only minor

amendments made to include reference to the position and role of the Risk and

Internal Audit Manager.

3 No other

changes were made to the text of the Policy.

4 It is

proposed that the Internal Audit Policy will be reviewed again not later than

May 2019.

|

RECOMMENDATIONS

That the Committee:

a) Notes the

revised Internal Audit Policy.

|

Signatories

|

Author:

|

Andrew Slater - Risk and Internal Audit Manager

|

|

Authoriser:

|

Sandy Graham - General Manager Strategy and Governance

|

Attachments

|

|

Title

|

Page

|

|

a

|

Internal Audit Policy -

reviewed May 2017

|

40

|

|

SUMMARY OF CONSIDERATIONS

|

|

Fit with purpose

of Local Government

The Internal Audit Policy relates to providing a

regulatory function and is considered good-quality and cost-effective

|

|

Fit with strategic

framework

|

|

Contributes

|

Detracts

|

Not applicable

|

|

Social Wellbeing Strategy

|

☒

|

☐

|

☐

|

|

Economic Development Strategy

|

☒

|

☐

|

☐

|

|

Environment Strategy

|

☒

|

☐

|

☐

|

|

Arts and Culture Strategy

|

☒

|

☐

|

☐

|

|

3 Waters Strategy

|

☒

|

☐

|

☐

|

|

Spatial Plan

|

☒

|

☐

|

☐

|

|

Integrated Transport Strategy

|

☒

|

☐

|

☐

|

|

Parks and Recreation Strategy

|

☒

|

☐

|

☐

|

|

Other strategic projects/policies/plans

|

☐

|

☐

|

☐

|

As a mechanism for strengthening Council governance and

performance assurance, robust internal audit practices will support the

delivery of all Council strategies and objectives.

|

|

Māori Impact

Statement

As a mechanism for strengthening Council governance,

operations and performance, robust internal audit practices will support

effective and collaborative partnerships with all community stakeholders,

including Kai Tahu.

|

|

Sustainability

As a mechanism for strengthening Council business

activities and performance, transparency, due diligence and informed,

sustainable growth, effective internal audit functions will support the

long-term sustainability of the DCC.

|

|

LTP/Annual Plan /

Financial Strategy /Infrastructure Strategy

As a mechanism for strengthening Council business

activities and performance, transparency, due diligence and informed,

sustainable growth, effective internal audit functions will support the

delivery of the Annual Plan/ LTP and other business strategies and

obligations.

|

|

Financial

considerations

No financial implications are identified

|

|

Significance

This is not deemed significant in terms of the Council's

Significance and Engagement Policy.

|

|

Engagement –

external

No external engagement has been conducted.

|

|

Engagement -

internal

Internal engagement included review by the General Manager

Strategy and Governance, (acting) Chief Financial Officer, and the Risk and

Internal Audit Manager.

|

|

Risks: Legal /

Health and Safety etc.

The absence of an effective Internal Audit Policy exposes

Council to significant potential strategic and operational risk, arising from

sub-optimal business performance controls, governance and decision-making

mechanisms.

|

|

Conflict of

Interest

No Conflicts of Interest have been identified.

|

|

Community Boards

No implications for Community Boards have been identified.

|

|

Audit and Risk Subcommittee

6 June 2017

|

|

|

Audit and Risk Subcommittee

6 June 2017

|

|

Resolution to Exclude the

Public

That the Audit and Risk

Subcommittee:

Pursuant to the provisions of the

Local Government Official Information and Meetings Act 1987, exclude the public

from the following part of the proceedings of this meeting namely:

|

General subject of the matter to be considered

|

Reasons

for passing this resolution in relation to each matter

|

Ground(s) under

section 48(1) for the passing of this resolution

|

Reason for

Confidentiality

|

|

C1

Confirmation of the Confidential Minutes of Audit and Risk

Subcommittee meeting - 7 February 2017 - Public Excluded

|

S7(2)(j)

The

withholding of the information is necessary to prevent the disclosure or use

of official information for improper gain or improper advantage.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C2

Audit and Risk Subcommittee Action List Report

|

S7(2)(c)(ii)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to damage the public

interest.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C3

Audit New Zealand

|

S7(2)(h)

The

withholding of the information is necessary to enable the local authority to

carry out, without prejudice or disadvantage, commercial activities.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C4

Treasury Risk Management Compliance

|

S7(2)(h)

The

withholding of the information is necessary to enable the local authority to

carry out, without prejudice or disadvantage, commercial activities.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C5

Dunedin City Holdings Limited Update

|

S7(2)(b)(ii)

The

withholding of the information is necessary to protect information where the

making available of the information would be likely unreasonably to

prejudice the commercial position of the person who supplied or who is the

subject of the information.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C6

Health and Safety Monthly Report for March 2017

|

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of

natural persons, including that of a deceased person.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C7

Strategic Risk Register Update - May 2017

|

S7(2)(c)(ii)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to damage the public

interest.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C8

Update on the DCC Internal Workplan - May 2017

|

S7(2)(b)(ii)

The

withholding of the information is necessary to protect information where the

making available of the information would be likely unreasonably to

prejudice the commercial position of the person who supplied or who is the

subject of the information.

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to prejudice the supply

of similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

S7(2)(h)

The

withholding of the information is necessary to enable the local authority to

carry out, without prejudice or disadvantage, commercial activities.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C9

Internal Audit Outcomes Report - May 2017

|

S7(2)(c)(ii)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to damage the public

interest.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C10

External Audit Outcomes Report - May 2017

|

S7(2)(c)(ii)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to damage the public

interest.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C11

Risk Management Committee Minutes - December 2016 and February 2017

|

S7(2)(b)(ii)

The

withholding of the information is necessary to protect information where the

making available of the information would be likely unreasonably to

prejudice the commercial position of the person who supplied or who is the

subject of the information.

S7(2)(h)

The

withholding of the information is necessary to enable the local authority to

carry out, without prejudice or disadvantage, commercial activities.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C12

Protected Disclosure Register

|

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of

natural persons, including that of a deceased person.

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to prejudice the supply

of similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C13

Investigation Register

|

S6(b)

The

making available of the information would be likely to endanger the safety

of a person.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 6.

|

The matters detailed

in this report are subject to investigation and information should remain

confidential so as not to prejudice the investigation and any possible

outcomes of the investigation..

|

This resolution is made in

reliance on Section 48(1)(a) of the Local Government Official Information and

Meetings Act 1987, and the particular interest or interests protected by

Section 6 or Section 7 of that Act, or Section 6 or Section 7 or Section 9 of

the Official Information Act 1982, as the case may require, which would be

prejudiced by the holding of the whole or the relevant part of the proceedings

of the meeting in public are as shown above after each item.

That Julian Tan (Audit Director, Audit NZ) and Amanda

Nicholls (Audit Manager, Audit NZ) be permitted to remain at the meeting, after

the public has been excluded, because of their knowledge of Item C3. This

knowledge, which would be of assistance in relation to the matters discussed,

was relevant because they would be reporting on the item under consideration.