Notice of Meeting:

I hereby give notice that an ordinary meeting of the Audit

and Risk Subcommittee will be held on:

Date: Monday

10 March 2025

Time: 12.30

pm

Venue: Council

Chamber, Dunedin Public Art Gallery, The Octagon, Dunedin

Sandy Graham

Audit and Risk Subcommittee

PUBLIC AGENDA

|

Chairperson

|

Mr Warren Allen

|

|

|

Deputy Chairperson

|

Ms Janet Copeland

|

|

|

Members

|

Cr Christine Garey

|

Cr Cherry Lucas

|

|

|

Mayor Jules Radich

|

Cr Lee Vandervis

|

Senior Officer Carolyn

Allan, Chief Financial Officer

Governance Support Officer Wendy

Collard

Wendy Collard

Governance Support Officer

Telephone: 03 477 4000

Wendy.Collard@dcc.govt.nz

www.dunedin.govt.nz

Note: Reports

and recommendations contained in this agenda are not to be considered as

Council policy until adopted.

|

|

Audit and Risk Subcommittee

10 March 2025

|

ITEM TABLE OF CONTENTS PAGE

1 Apologies 4

2 Confirmation

of Agenda 4

3 Declaration

of Interest 5

4 Confirmation

of Minutes 10

4.1 Audit and Risk

Subcommittee meeting - 4 December 2024 10

Part

A Reports (Committee has power to decide these matters)

5 Audit

and Risk Subcommittee Work Plan 2025 21

6 Audit

and Risk Subcommittee Updates Report 25

7 Health

and Safety Monthly Reporting for December 2024 and January 2025 86

8 Financial

Report - Period ended 31 December 2024 110

9 Waipori

Fund - Quarter ending 31 December 2024 139

Resolution to Exclude the Public 146

|

|

Audit and Risk Subcommittee

10 March 2025

|

1 Apologies

An apology has been received from

Ms Janet Copeland.

That the Subcommittee:

Accepts the apology from Ms

Janet Copeland.

2 Confirmation

of agenda

Note:

Any additions must be approved by resolution with an explanation as to why they

cannot be delayed until a future meeting.

|

|

Audit and Risk Subcommittee

10 March 2025

|

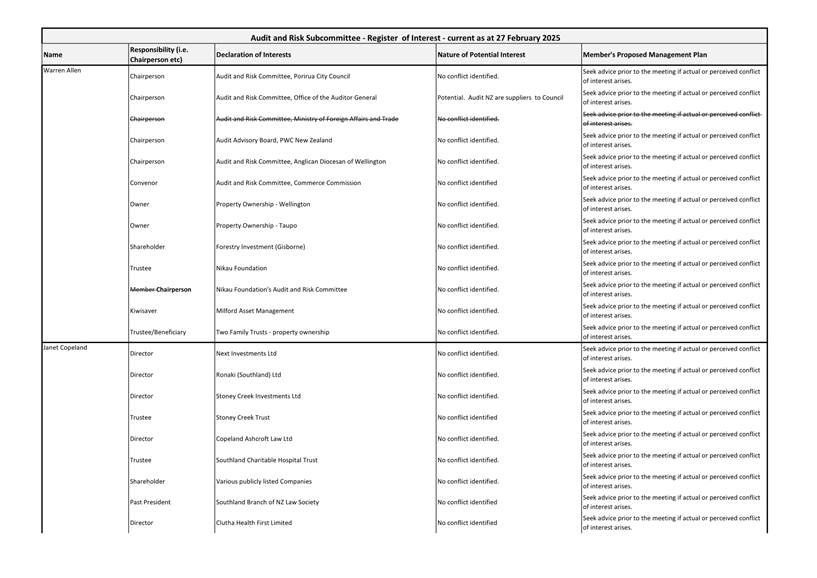

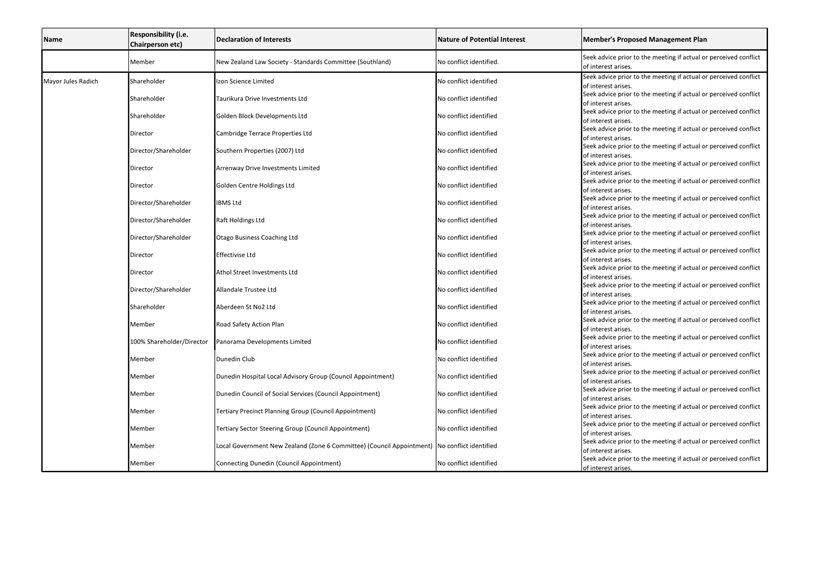

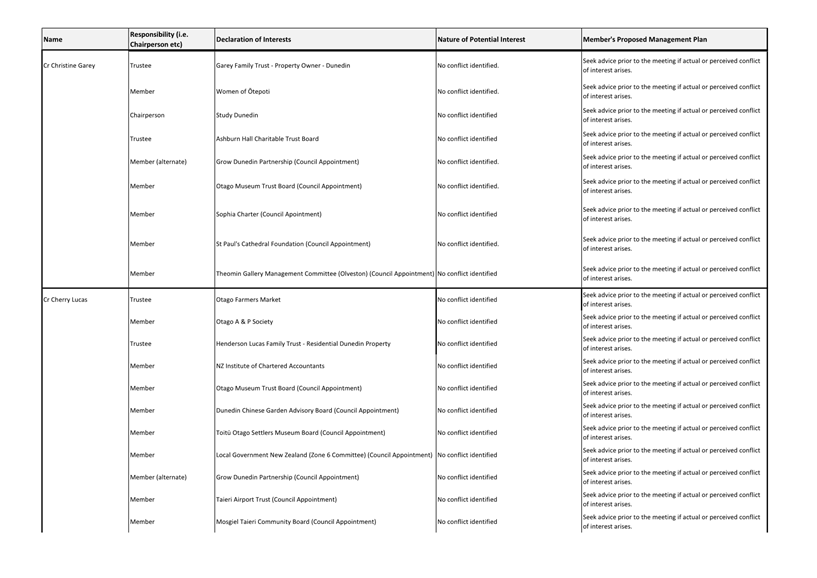

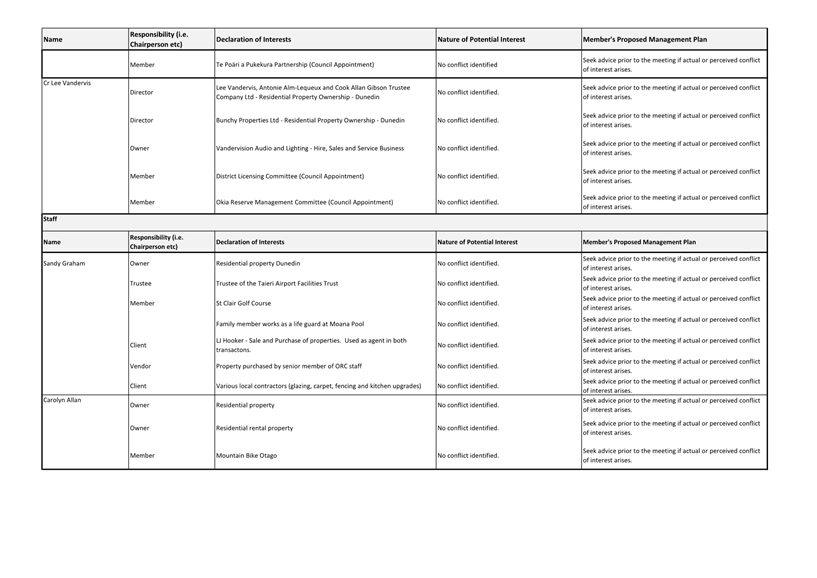

Declaration of Interest

EXECUTIVE SUMMARY

1. Members

are reminded of the need to stand aside from decision-making when a conflict

arises between their role as an elected representative or independent member and

any private or other external interest they might have.

2. Elected

and Independent members are reminded to update their register

of interests as soon as practicable, including amending the register at this

meeting if necessary.

RECOMMENDATIONS

That the Subcommittee:

a) Notes/Amends if

necessary the Elected or Independent Members' Interest Register attached as

Attachment A; and

b) Confirms/Amends the

proposed management plan for Elected or Independent Members' Interests.

Attachments

|

|

Title

|

Page

|

|

⇩a

|

Register of Interests

|

6

|

|

|

Audit and Risk Subcommittee

10 March 2025

|

|

|

Audit and Risk Subcommittee

10 March 2025

|

Confirmation

of Minutes

Audit

and Risk Subcommittee meeting - 4 December 2024

RECOMMENDATIONS

That the Subcommittee:

a) Confirms the public

part of the minutes of the Audit and Risk Subcommittee meeting held on 04

December 2024 as a correct record.

Attachments

|

|

Title

|

Page

|

|

A⇩

|

Minutes of Audit and

Risk Subcommittee meeting held on 4 December 2024

|

11

|

|

|

Audit and Risk

Subcommittee

10 March 2025

|

Audit and Risk Subcommittee

MINUTES

Minutes of

an ordinary meeting of the Audit and Risk Subcommittee held in the Council

Chamber, Dunedin Public Art Gallery, The Octagon, Dunedin on Wednesday 04

December 2024, commencing at 2.00 pm

PRESENT

|

Chairperson

|

Warren

Allen

|

|

|

Deputy Chairperson

|

Janet

Copeland

|

|

|

Members

|

Cr

Christine Garey

|

Cr

Cherry Lucas

|

|

|

Cr Lee

Vandervis

|

|

|

IN ATTENDANCE

|

Sandy Graham

(Chief Executive Officer), Carolyn Allan (Chief Financial Officer), Scott

MacLean (General Manager, Climate and City Growth), Jinty MacTavish (Manager,

Zero Carbon), Jonathan Rowe (Programme Manager, South Dunedin Future), Jane

Pearce (Health and Safety Manager) Richard Davey (Treasurer, Dunedin City

Holdings Ltd), Hayley Knight (Assurance Manager) and Cr Sophie Barker

|

Governance Support Officer Wendy Collard

|

1 Apologies

|

|

An apology has been received from Mayor Jules Radich

|

|

|

Moved (Warren Allen/Cr Christine Garey):

That the

Subcommittee:

Accepts the apology from Mayor Jules Radich

Motion carried (AR/2024/034)

|

|

2 Confirmation

of agenda

|

|

|

Moved (Warren Allen/Cr Cherry Lucas):

That the

Subcommittee:

Confirms the agenda without addition or alteration.

Motion carried (AR/2024/035)

|

3 Declarations

of interest

Members were reminded of the need to stand aside from

decision-making when a conflict arose between their role as an elected

representative and any private or other external interest they might have.

Warren Allen

provided an update to his register of interests.

|

|

Moved (Warren Allen/Cr Cherry Lucas):

That the

Subcommittee:

a) Amends the Elected and Independent Members' Interest

Register; and

b) Confirms the proposed management plan for Elected

or Independent Members' Interests.

Motion carried (AR/2024/036)

|

4 Confirmation

of Minutes

|

4.1 Audit

and Risk Subcommittee meeting - 7 October 2024

|

|

|

Moved (Warren Allen/Cr Christine Garey):

That the

Subcommittee:

a) Confirms the public part of the minutes of the

Audit and Risk Subcommittee meeting held on 07 October 2024 as a correct

record.

Motion carried (AR/2024/037)

|

|

4.2 Audit

and Risk Subcommittee meeting - 25 October 2024

|

|

|

Moved (Warren Allen/Cr Cherry Lucas):

That the

Subcommittee:

a) Confirms the public part of the minutes of the

Audit and Risk Subcommittee meeting held on 25 October 2024 as a correct

record.

Motion carried (AR/2024/038)

|

Part

A Reports

|

5 Audit

and Risk Subcommittee Work Plan 2024/2025

|

|

|

A report

from Civic provided a copy of the Audit and Risk Subcommittee Work Plan

2024/2025 which has been aligned with work programme scheduling and decision

making.

The

Chief Financial Officer (Carolyn Allan) responded to questions.

Following

discussion it was agreed that the Financial Strategy and Risks would be added

to the work plan along with regular reporting on the Climate Change

Adaptation and Mitigation Risk and 2030 Zero Carbon Policy.

|

|

|

Moved (Mr Warren Allen/Cr Christine Garey):

That the

Subcommittee:

a) Notes the Audit and Risk Subcommittee Work Plan for 2024/2025

Motion carried (AR/2024/039)

|

|

6 Audit

and Risk Subcommittee Updates Report

|

|

|

A report

from Finance provided updates on the progress of various sundry matters that

had been noted by the Subcommittee.

The Chief

Financial Officer (Carolyn Allan) spoke to the report and responded to

questions.

|

|

|

Moved (Warren Allen/Cr Cherry Lucas):

That the

Subcommittee:

a) Notes the Audit and Risk Subcommittee

Updates Report.

b) Notes the Timeline for Water

Services Delivery Plan.

Motion carried (AR/2024/040)

|

|

7 DCC

Policy Update Report

|

|

|

A report

from Finance provided an update on DCC policies as identified in the Audit

and Risk Subcommittee (ARS) Workplan and ongoing audit and business

improvement activities.

The Chief

Financial Officer (Carolyn Allan) and the Assurance Manager (Hayley Knight)

spoke to the report and responded to questions.

Following

discussion on the Fraud, Bribery and Corruption Prevention Policy, it was

agreed that the following minor amendments be made:

1.1 d) to now read: Outline clear

roles and responsibilities of the DCC for investing and responding to

allegations of fraud, bribery, or corruption.

4.8 to now read: Where fraud is

established………………………………..

4.12 h) to now read: robust due

diligence enquiry of new suppliers.

|

|

|

Moved (Warren Allen/Cr Cherry Lucas):

That the

Committee:

a) Notes the Policy Update Report – December 2024.

b) Endorses approval of the Treasury Risk Management Policy.

c) Approves the Fraud, Bribery and Corruption

Prevention Policy.

d) Notes the Fraud, Bribery and Corruption Investigation

procedures.

Motion carried (AR/2024/041)

|

|

|

Moved (Warren Allen/Cr Cherry Lucas):

That the

Subcommittee:

Pursuant to the provisions of the Local Government Official

Information and Meetings Act 1987, exclude the public from the following part

of the proceedings of this meeting namely:

|

General subject of the matter to be considered

|

Reasons

for passing this resolution in relation to each matter

|

Ground(s)

under section 48(1) for the passing of this resolution

|

Reason

for Confidentiality

|

|

C4 DCC Risk 'Deep Dive' - Climate Change Mitigation and

Adaptation

|

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or

could be compelled to provide under the authority of any enactment, where

the making available of the information would be likely to prejudice the

supply of similar information or information from the same source and it is

in the public interest that such information should continue to be

supplied.

|

S48(1)(a)

The

public conduct of the part of the meeting would be likely to result in the

disclosure of information for which good reason for withholding exists

under section 7.

|

|

Motion carried (AR/2024/042)

|

|

|

The meeting moved into non public at 2.34

pm and reconvened in public at 3.12 pm

|

|

7 DCC

POLICY UPDATE REPORT (continued)

|

|

|

Following discussion on the Gifts and

Hospitality Policy, , it was agreed that the

following minor amendments be made:

2.2 to now read: This Policy does not

apply to volunteers and those people who provide honorary or unpaid employee

of the DCC.

4.1 to now read: The offer of gifts

and/or hospitality .from third parties can constitute a personal thank you or

be appropriate for relationship management because of the nature of the

work. Gifts and/or hospitality ……………..

4.4 to now read: The following is a

list of gifts that should not be accepted.

|

|

|

Moved (Warren Allen/Cr Cherry Lucas):

That the

Subcommittee:

e) Provide feedback on the Gifts and Hospitality Policy.

f) Notes the Gifts and Hospitality Procedures.

g) Approve the Policy Review Schedule .

h) Notes the Policy Review Process for the Audit and Risk

Subcommittee.

Motion carried (AR/2024/043)

|

|

8 Health

and Safety Monthly Reporting for October 2024

|

|

|

A report

from Health and Safety provided the monthly Health, Safety and Wellbeing

report for October 2024 for the Subcommittee’s information.

The Health and Safety Manager (Jane

Pearce) spoke to the report and responded to questions.

|

|

|

Moved (Warren Allen/Cr Christine Garey):

That the

Subcommittee:

a) Notes the monthly Health, Safety and Wellbeing report for

October 2024.

Motion carried (AR/2024/044)

|

|

9 Financial

Report - Period Ended 30 September 2024

|

|

|

A report

from Finance provided the financial results for the period ended 30 September

2024 and the financial position as at that date which was presented to the

Finance and Council Controlled Organisation Committee meeting held on 14

November 2024.

The

Chief Financial Officer (Carolyn Allan) spoke to the report and responded to

questions.

|

|

|

Moved (Cr Lee Vandervis/Warren Allen):

That the

Subcommittee:

a) Notes the Financial Performance for the period ended 30

September 2024 and the Financial Position as at that date.

Motion carried (AR/2024/045)

|

|

10 Waipori

Fund - Quarter ending 30 September 2024

|

|

|

A report

from Dunedin Treasury Limited provided information on the results of the

Waipori Fund for the quarter ended 30 September 2024 which was presented to

the Finance and Council Controlled Organisation Committee meeting held on 14

November 2024.

The Treasurer, Dunedin City Holdings Ltd

(Richard Davey) spoke to the report and responded to questions.

|

|

|

Moved (Mr Warren Allen/Cr Cherry Lucas):

That the

Committee:

a) Notes the report from Dunedin City Treasury Limited on the

Waipori Fund for the quarter ended 30 September 2024.

Motion carried (AR/2024/046)

|

Cr Garey left the meeting at 3.57 pm.

|

Resolution to Exclude the Public

|

|

Moved (Mr Warren Allen/Cr Cherry Lucas):

That the

Committee:

Pursuant to the provisions of the Local Government Official

Information and Meetings Act 1987, exclude the public from the following part

of the proceedings of this meeting namely:

|

General subject of the matter to be considered

|

Reasons

for passing this resolution in relation to each matter

|

Ground(s)

under section 48(1) for the passing of this resolution

|

Reason

for Confidentiality

|

|

C1 Audit and Risk Subcommittee meeting - 7 October 2024 -

Public Excluded

|

S7(2)(h)

The withholding

of the information is necessary to enable the local authority to carry out,

without prejudice or disadvantage, commercial activities.

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or

could be compelled to provide under the authority of any enactment, where

the making available of the information would be likely to prejudice the

supply of similar information or information from the same source and it is

in the public interest that such information should continue to be

supplied.

S7(2)(b)(ii)

The

withholding of the information is necessary to protect information where

the making available of the information would be likely unreasonably to

prejudice the commercial position of the person who supplied or who is the

subject of the information.

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of

natural persons, including that of a deceased person.

|

.

|

|

|

C2 Audit and Risk Subcommittee meeting - 25 October 2024 -

Public Excluded

|

S7(2)(b)(i)

The

withholding of the information is necessary to protect information where

the making available of the information would disclose a trade secret.

|

.

|

|

|

C3 Treasury Risk Management Compliance Report

|

S7(2)(h)

The

withholding of the information is necessary to enable the local authority

to carry out, without prejudice or disadvantage, commercial activities.

|

S48(1)(a)

The

public conduct of the part of the meeting would be likely to result in the

disclosure of information for which good reason for withholding exists

under section 7.

|

|

|

C5 Internal Audit Workplan Update

|

S7(2)(b)(i)

The

withholding of the information is necessary to protect information where

the making available of the information would disclose a trade secret.

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or

could be compelled to provide under the authority of any enactment, where

the making available of the information would be likely to prejudice the

supply of similar information or information from the same source and it is

in the public interest that such information should continue to be

supplied.

S7(2)(h)

The

withholding of the information is necessary to enable the local authority

to carry out, without prejudice or disadvantage, commercial activities.

|

S48(1)(a)

The

public conduct of the part of the meeting would be likely to result in the

disclosure of information for which good reason for withholding exists

under section 7.

|

|

|

C6 DCC External Audit Actions Update - November 2024

|

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or

could be compelled to provide under the authority of any enactment, where

the making available of the information would be likely to prejudice the

supply of similar information or information from the same source and it is

in the public interest that such information should continue to be

supplied.

|

S48(1)(a)

The

public conduct of the part of the meeting would be likely to result in the

disclosure of information for which good reason for withholding exists

under section 7.

|

|

|

C7 Audit Engagement Letter (Draft)

|

S7(2)(i)

The

withholding of the information is necessary to enable the local authority

to carry on, without prejudice or disadvantage, negotiations (including

commercial and industrial negotiations).

|

S48(1)(a)

The

public conduct of the part of the meeting would be likely to result in the

disclosure of information for which good reason for withholding exists

under section 7.

|

|

|

C8 Dunedin City Holdings Ltd - Update on Audit and Risk Activity

|

S7(2)(b)(ii)

The

withholding of the information is necessary to protect information where

the making available of the information would be likely unreasonably to

prejudice the commercial position of the person who supplied or who is the

subject of the information.

|

S48(1)(a)

The

public conduct of the part of the meeting would be likely to result in the

disclosure of information for which good reason for withholding exists

under section 7.

|

|

|

C9 DCC Risk 'Deep Dive' - Fraud Risk Management

|

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or

could be compelled to provide under the authority of any enactment, where

the making available of the information would be likely to prejudice the

supply of similar information or information from the same source and it is

in the public interest that such information should continue to be

supplied.

|

S48(1)(a)

The

public conduct of the part of the meeting would be likely to result in the

disclosure of information for which good reason for withholding exists

under section 7.

|

|

This resolution

is made in reliance on Section 48(1)(a) of the Local Government Official

Information and Meetings Act 1987, and the particular interest or interests

protected by Section 6 or Section 7 of that Act, or Section 6 or Section 7 or

Section 9 of the Official Information Act 1982, as the case may require,

which would be prejudiced by the holding of the whole or the relevant part of

the proceedings of the meeting in public are as shown above after each item.

That Mark

Cervantes (Crowe) be permitted to attend the meeting, after the public has

been excluded, because of their knowledge of Items C5. This knowledge,

which would been of assistance in relation to the matters discussed, was

relevant because they would be reporting on the item under consideration.

Motion carried (AR/2024/047)

|

The meeting moved into non-public at 3.58

pm and concluded at 5.12 pm.

..............................................

CHAIRPERSON

|

|

Audit and Risk Subcommittee

10 March 2025

|

Part

A Reports

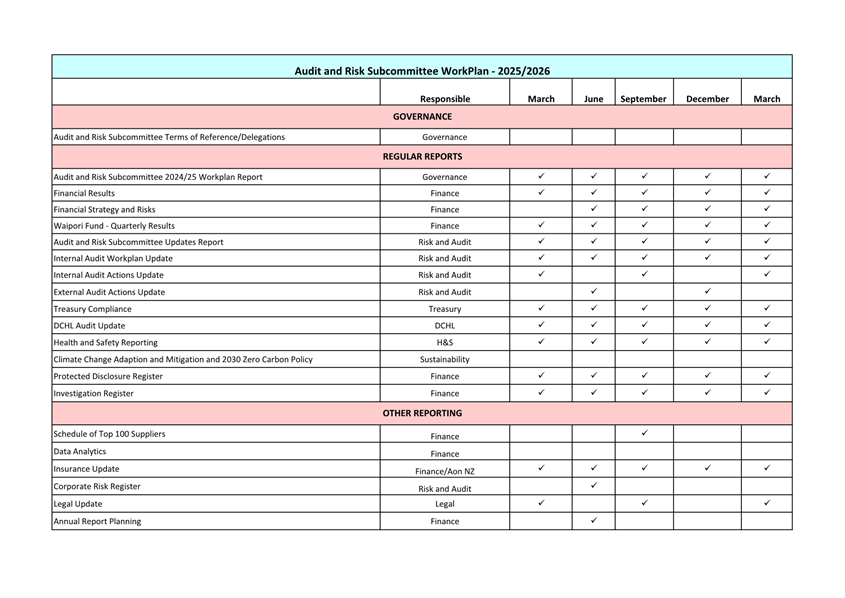

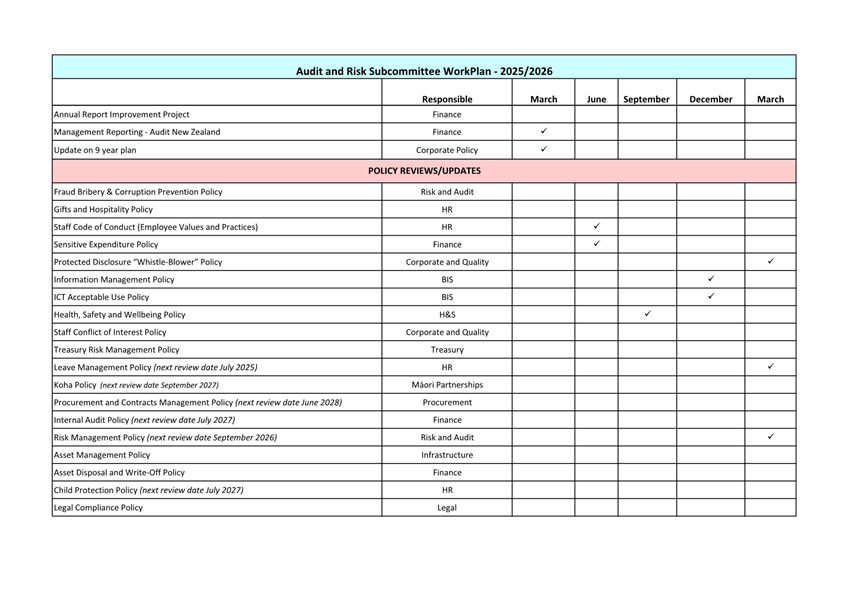

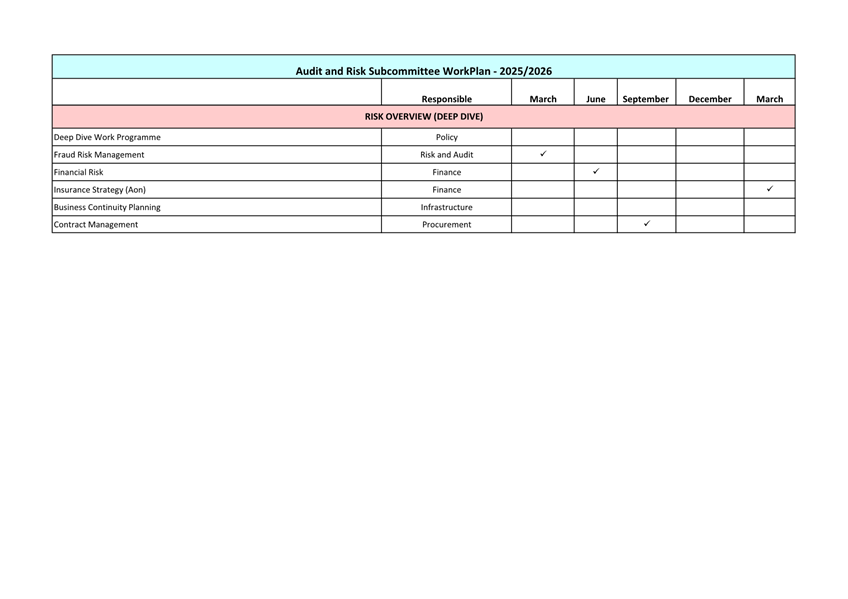

Audit and Risk Subcommittee Work Plan 2025

Department: Civic

EXECUTIVE SUMMARY

1 This

report provides a copy of the Audit and Risk Subcommittee Work Plan 2025 which

has been aligned with work programme scheduling and decision making.

2 It

should be noted that the items without ticks shown have not been scheduled for

action. A Deep Dive work programme will be developed after the Corporate Risk

Register has been reviewed. Deep dive topics will reflect the high or emerging

risks.

3 As

this is an administrative report only, the Summary of Consideration is not

required.

RECOMMENDATIONS

That the Subcommittee:

a) Notes the Audit and

Risk Subcommittee Work Plan for 2025

Signatories

|

Author:

|

Wendy Collard - Governance Support Officer

|

|

Authoriser:

|

Carolyn Allan - Chief Financial Officer

|

Attachments

|

|

Title

|

Page

|

|

⇩a

|

Audit and Risk

Subcommittee Work Plan

|

22

|

|

|

Audit and Risk Subcommittee

10 March 2025

|

|

|

Audit and Risk Subcommittee

10 March 2025

|

Audit and Risk Subcommittee Updates Report

Department: Finance

EXECUTIVE SUMMARY

1 This

report provides updates on the progress of various sundry matters that have

been noted by the Subcommittee.

RECOMMENDATIONS

That the Subcommittee:

a) Notes the Audit and

Risk Subcommittee Updates Report

b) Notes the OAG Report: Observations from 2024-34 long term plans

(Attachment A)

c) Notes the WEF Global Risks Report 2025: Key Findings (Attachment B)

DISCUSSION

1

Insurance

2 Following

the update to the National Seismic Hazard Model, Council commissioned work to

model and understand earthquake loss for below-ground assets to inform

insurance loss limits. This modelling has been completed and a draft report has

been received. Results from the modelling indicate that no significant

changes are required.

3 The

Business Interruption review is yet to be completed. This work is expected to

inform the 1 July 2025 renewal process which commences later this month.

2

9 Year Plan

4 A 9-year plan Council meeting was held on 28 - 30 January

2025, where activities and budgets were presented to Council for its consideration.

Following this, the first version of the draft consultation document was

provided to Audit NZ on 3 February 2025.

5 The

audit of the consultation document is in progress. A “hot

review” of the consultation document is scheduled to be undertaken by the

Office of the Auditor General during the week commencing 10 March 2025.

Adoption of the consultation document is scheduled for the 26 March 2025

Council meeting.

6 Alongside

the development of this 9-year plan, is the development of the “Local

Water Done Well – Ōtepoti” consultation document that

discusses potential models for delivering water services. Both

consultations will be undertaken at the same time, along with a joint hearing

in early May.

7 A decision on the delivery model to be used for Dunedin

will be made in late May, and the final 9-year plan document will reflect that

decision. Further discussion on Local Water Done Well is provided below.

8 A

high-level timetable for the remainder of the 9-year plan project is as

follows:

|

Timing

|

Task

|

|

March 2025

|

Audit “Hot

review”, completion of audit

Adoption of the 9-year

plan consultation document.

|

|

31 March to 30 April

2025

|

Engagement and

submission period

|

|

5 – 8 May 2025

26 – 29 May 2025

|

Hearings

Deliberations

|

|

30 June 2025

|

Adoption of the 9-year

plan

|

3

4

Local Water Done Well

9 The

Government is now in the final stage of their three-stage process implementing

its “Local Water Done Well” (LWDW) reform programme.

10 The first

stage of LWDW saw the repeal of legislation relating to large water services

entities. This was in February 2024.

11 The second

stage of LWDW was implemented with the passing of the Local Government (Water

Services Preliminary Arrangements) Act 2024 (Preliminary Act) on 2 September

2024. As a result, Council is required to prepare and submit a WSDP to the

Secretary for Local Government by 3 September 2025.

12 The third

stage of LWDW is now underway with the introduction of the Local Government

(Water Services) Bill (the December Bill) on 10 December 2024. The December

Bill provides the enduring settings for LWDW including the framework for

economic regulation as well as the more detailed powers and duties for service

delivery models. Council has made a submission on the Bill which is expected to

be enacted in mid-2025. The Bill provides for:

i. Structural

arrangements for water service delivery including establishment, ownership, and

governance of water organisations.

ii. Operational

matters such as arrangements for charging, bylaws, and management of stormwater

networks.

iii. Planning,

reporting, and financial management.

iv. A

new economic regulation and consumer protection regime.

v. Changes

to the water quality regulatory framework and the water services regulator.

13 Guidance on

the future water services delivery system was released by the DIA on 8 August

2024, and further on the WSDP on 3 September 2024. The Guidance was

subsequently updated in December 2024.

14 At the

Council meeting on 26 February 2025, Council was considered a report

“Local Water Done Well – Decision on Water Models for

Consultation”. The Council decided, for the purposes of consultation, on:

a) its

preferred water services delivery model (Preferred Option); and

b) what other

option(s) it will consult on (Alternative Option(s))

5

(together, referred to as “the Water Consultation Options”).

15 Council

selected the in-house delivery option as the preferred option for DCC’s

future water services delivery model, and the single CCO (asset owning) option

as an alternative option.

16 Staff

are preparing the LWDW consultation document accordingly. As discussed above,

the LWDW consultation document is being developed alongside the development of

the 9-year plan consultation document. Both consultations will be

undertaken at the same time, along with a joint hearing in early May.

17 A decision on the delivery model to be used for Dunedin will

be made as soon as possible after the Hearings. A decision on the WSDM

would need to be made in mid-May so that staff can update the 9-year plan to reflect

the WSDM, as required, and to allow time for the Audit Report on the 9-year

plan.

18 Council

will adopt its 9-year plan on 30 June 2025, and will submit its WSDP to the

Secretary for Local Government before 3 September 2025.

19 At the

Council meeting on 26 February 2025, Council also considered a report on

“Memorandum of Understanding with Christchurch City Council –

Potential for Shared Services”. This report provided Council with

information regarding a proposed process with Christchurch City Council (CCC)

to investigate whether there are opportunities for certain shared water

services (Shared Services) between the DCC and CCC.

20 The aim of

Shared Services would be to reduce costs and enhance water services for each

council’s communities. This aligns with the objectives of the LWDW

reforms. A memorandum of understanding (MOU) has been prepared to record the

proposed process for investigating the possibility of Shared Services.

21 Shared

Services would not affect the underlying ownership of each council’s

existing water assets as the services would be managed through contracts.

6

Policy Updates

22 There are

no updated policies presented at this meeting. The following policies are

undergoing review:

a) Asset

Management Policy

b) Asset

Disposal and Write-Off Policy

c) ICT

Acceptable Use Policy

d) Information

Management Policy

e) Purchase

Card Policy

f) Staff

Code of Conduct

g) Sensitive

Expenditure Policy

23 After

the review process, updated copies of DCC policies will be provided to the

Subcommittee for either feedback or noting.

7

OAG Report: Observations from audits of

council’s 2024-34 long term plans

24 The Office

of the Auditor General (OAG) have release a report outlining the observations

from audits conducted on council’s 2024-34 long term plans.

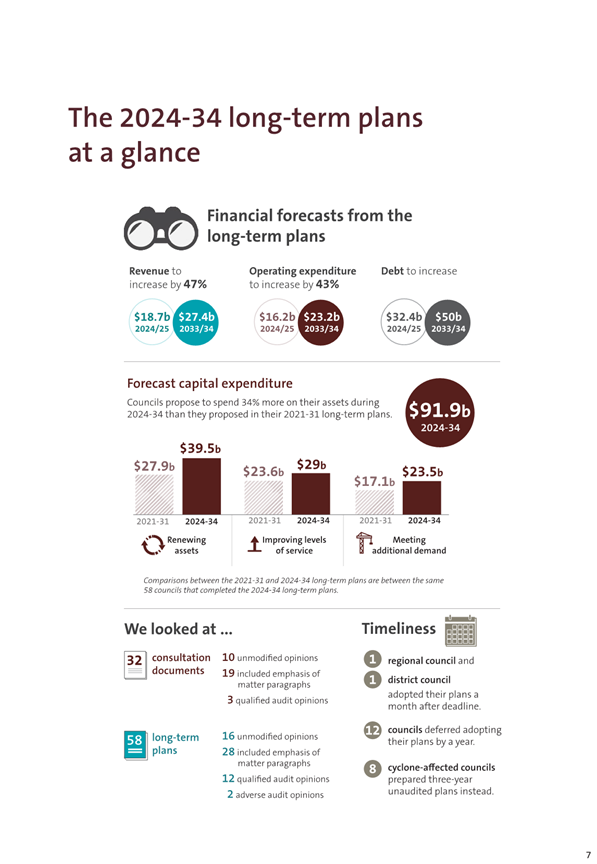

25 The Dunedin City Council is not in this audit report as it was one

of 12 council’s that opted to defer and carry out a 9-year plan. The

report is included as Attachment A for noting.

8

World Economic Forum – Global Risk Report

26 The World

Economic Forum (WEF) has produced insights report on the global risk landscape.

This report is based on findings from the Global Risks Perception Survey, which

is conducted with over 900 experts across academic, business, government, the

international community, and civil society.

27 This

information can be useful in understanding the global risk trends and possible

impacts for the Dunedin City Council (DCC).

28 The

summary section has been attached to this report for noting (Attachment B). The

full report can be found via the following link: https://reports.weforum.org/docs/WEF_Global_Risks_Report_2025.pdf

29 The main

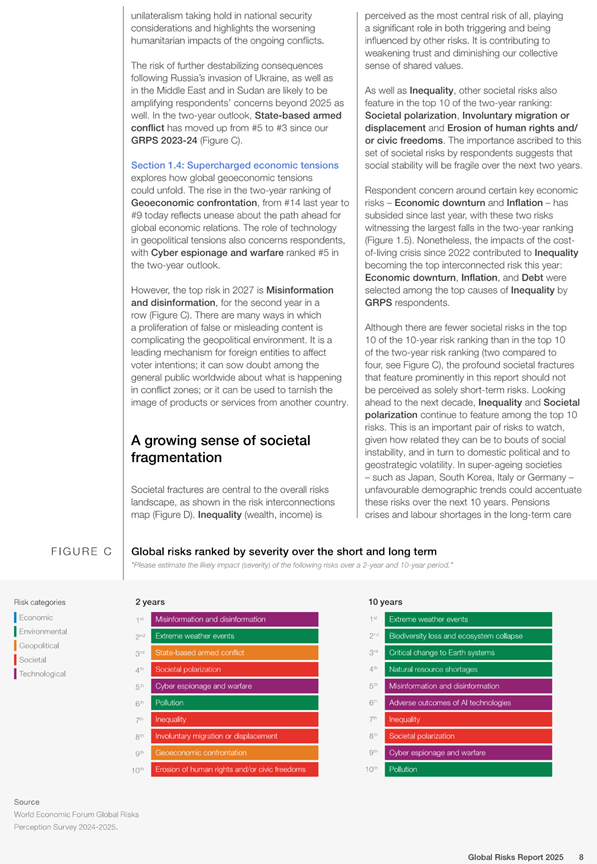

global findings from the 2025 report are:

a) The

perception on the global state now and into the future is ‘bleak’

with many expecting unsettled times in the next 2 years and turbulent in the

next 10 years (see Figure 1)

b) Geopolitical

concerns have risen to now be the number 1 and 3 top risks for the current

global risk landscape (see Figure 2).

c) The

top risk for the two-year horizon is misinformation and disinformation (see Figure

3). This is important to highlight for the DCC environment with both the

9-year plan consultation process and the local government elections coming up.

Care needs to be taken to support effective and accurate communication between

the DCC and the community to support trust in the Council.

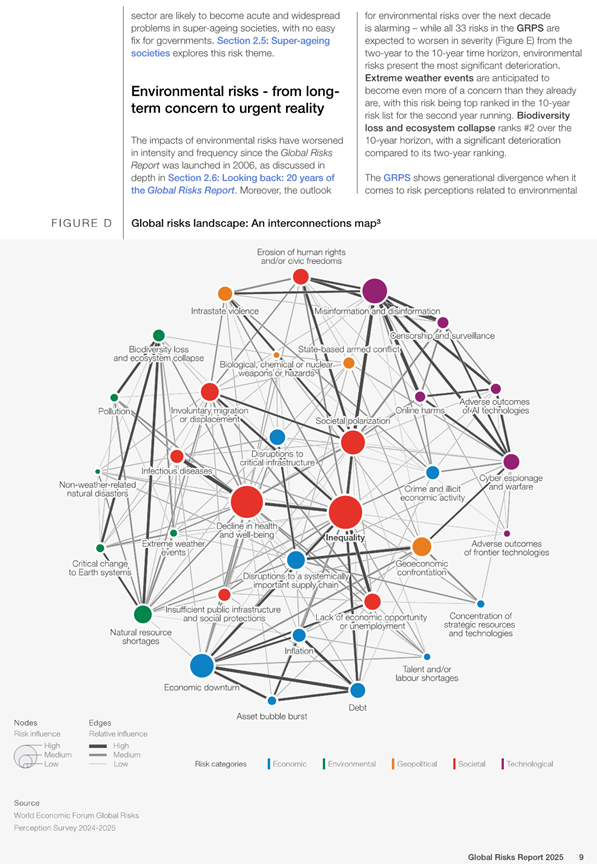

d) “Inequality”

has come out as the top interconnected risk this year, suggesting perceived

fragility to social stability over the next two years. This has come about

through challenges in the economic environment, social polarisation and

misinformation and disinformation as well as other risks.

e) Environmental

risks still feature prominently in the 10-year horizon (see Figure 3)

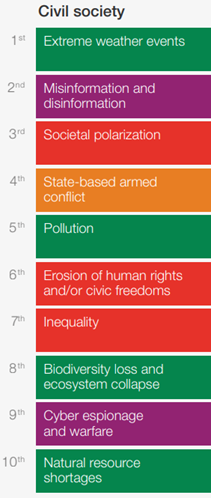

and is the top ranked risk in the civil sector for the next 2 years (see Figure

4).

f) The

use of AI has continued to grow, but the risk of adverse effects of AI

technologies is not featured in the top 10 for the 2-year outlook but is on the

10-year outlook.

30 From a New

Zealand perspective, the top 5 risks (see Figure 5) are mostly economic

based, alongside extreme weather, and poverty and inequality.

31 The

information provided from the WEF Global Risk Report will be used to analyse

the DCC corporate risk register and the potential impacts to the DCC.

9

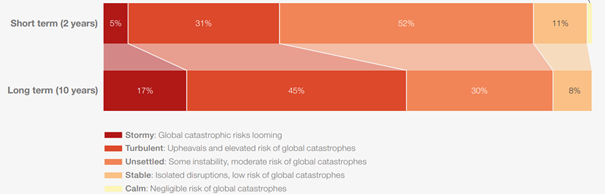

Figure 1: Short- and long-term global outlook.

10

11

Figure 2: The top five risks in the current global risk

landscape.

12

13

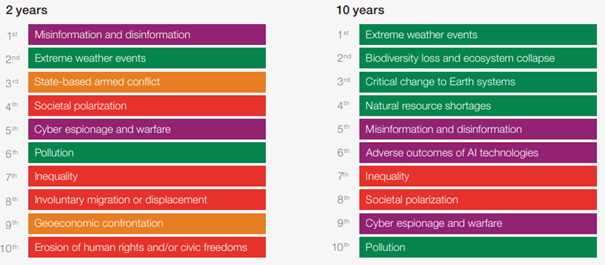

Figure 3: The top ten risks predicted globally for the next 2

years and 10 years.

14

Figure 4: The top ten risks predicted for the Civil Society for

the next 2 years.

15

16

Figure 5: The top five risks identified by risk professionals in

New Zealand.

OPTIONS

17

This is a noting report so there are no options.

Signatories

|

Author:

|

Hayley Knight - Assurance Manager

|

|

Authoriser:

|

Carolyn Allan - Chief Financial Officer

|

Attachments

|

|

Title

|

Page

|

|

⇩a

|

OAG Report:

Observations from 2024-34 long term plans

|

34

|

|

⇩b

|

WEF Global Risks Report

2025: Key Findings

|

74

|

|

SUMMARY OF CONSIDERATIONS

|

|

Fit with purpose of Local Government

This report provides an update on the DCC

Internal Audit Workplan, which is a regulatory function and is considered

good quality and cost effective.

|

|

Fit with strategic framework This report provides an update on the progress made

by Council to deliver upon the activities identified by the Audit and Risk

Subcommittee, which is a regulatory function and considered good quality and

cost effective

|

|

Contributes

|

Detracts

|

Not applicable

|

|

Social Wellbeing Strategy

|

✔

|

☐

|

☐

|

|

Economic Development Strategy

|

✔

|

☐

|

☐

|

|

Environment Strategy

|

✔

|

☐

|

☐

|

|

Arts and Culture Strategy

|

✔

|

☐

|

☐

|

|

3 Waters Strategy

|

✔

|

☐

|

☐

|

|

Future Development Strategy

|

✔

|

☐

|

☐

|

|

Integrated Transport Strategy

|

✔

|

☐

|

☐

|

|

Parks and Recreation Strategy

|

✔

|

☐

|

☐

|

|

Other strategic projects/policies/plans

|

☐

|

☐

|

✔

|

This report provides an update on the progress made by

Council to deliver upon the activities identified by the Audit and Risk

Subcommittee, which is a regulatory function and considered good quality and

cost effective

|

|

Māori Impact Statement

There are no known impacts for mana whenua.

|

|

Sustainability

There are no implications for sustainability

|

|

Zero carbon

There are no implications for zero carbon.

|

|

LTP/Annual Plan / Financial Strategy /Infrastructure

Strategy

There are no known implications.

|

|

Financial considerations

No financial implications have been identified

|

|

Significance

This report is rated low under the Council’s

Significance and Engagement Policy.

|

|

Engagement – external

No external engagement has been undertaken.

|

|

Engagement - internal

Activities noted herein include cross Council engagement

and collaboration.

|

|

Risks: Legal / Health and Safety etc.

No risks have been identified.

|

|

Conflict of Interest

There are no conflict of interest identified.

|

|

Community Boards

There have been no implications for Community Boards

identified.

|

|

|

Audit and Risk Subcommittee

10 March 2025

|

|

|

Audit and Risk Subcommittee

10 March 2025

|

|

|

Audit and Risk Subcommittee

10 March 2025

|

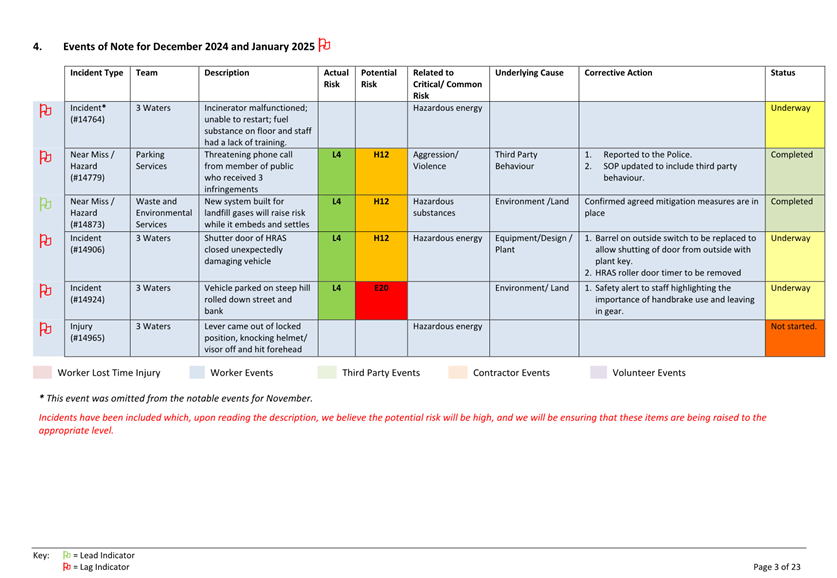

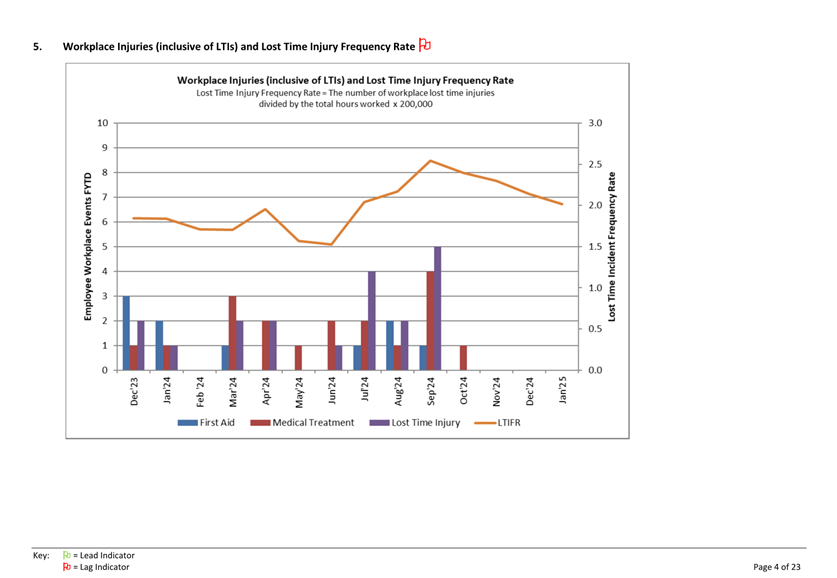

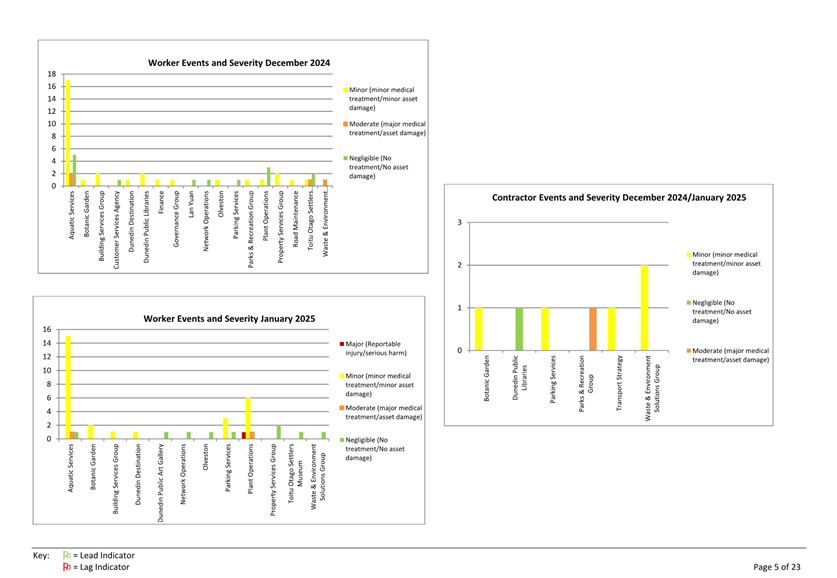

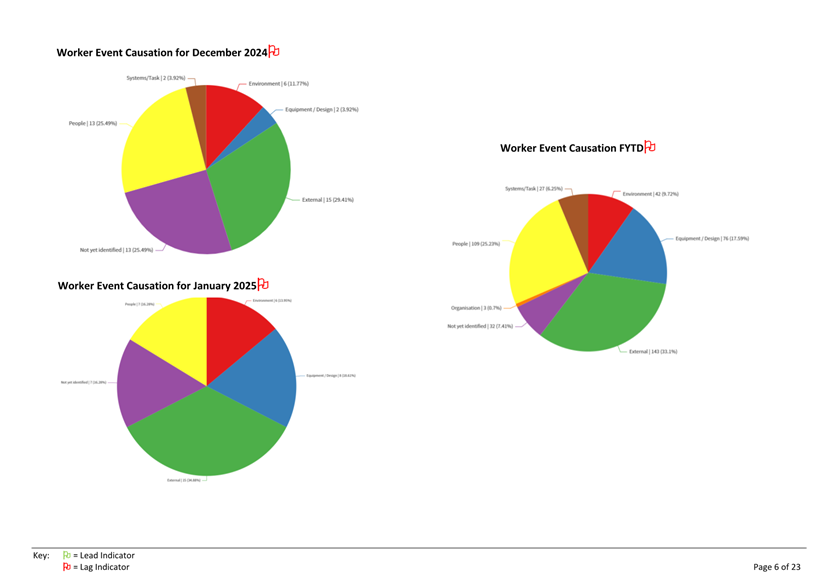

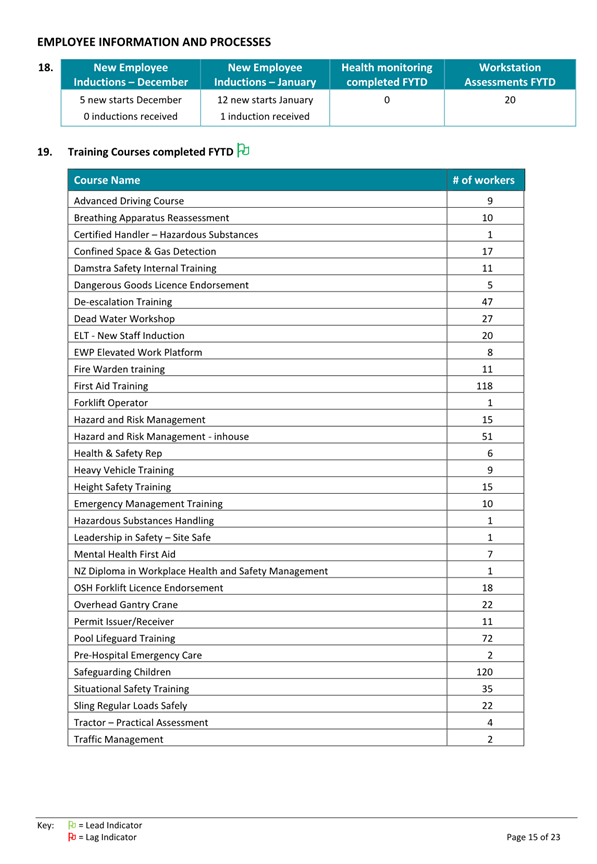

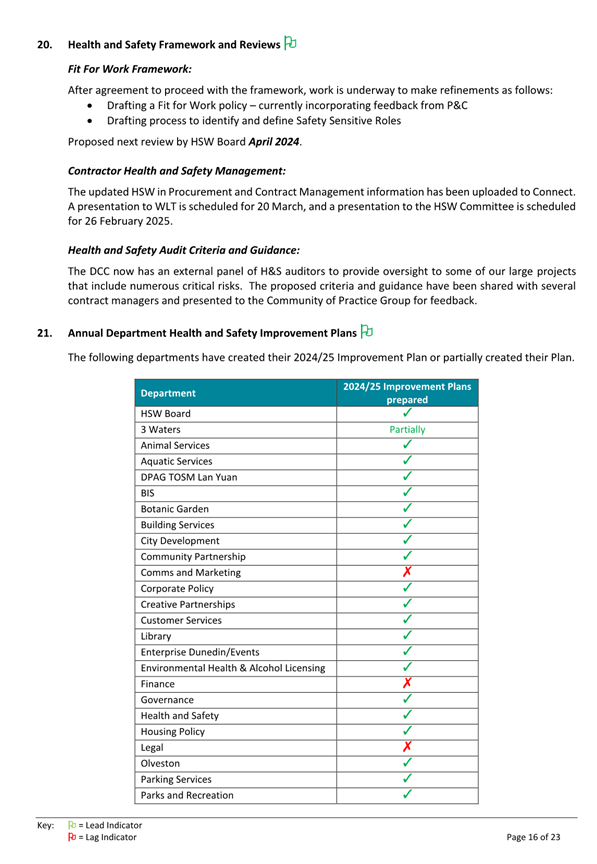

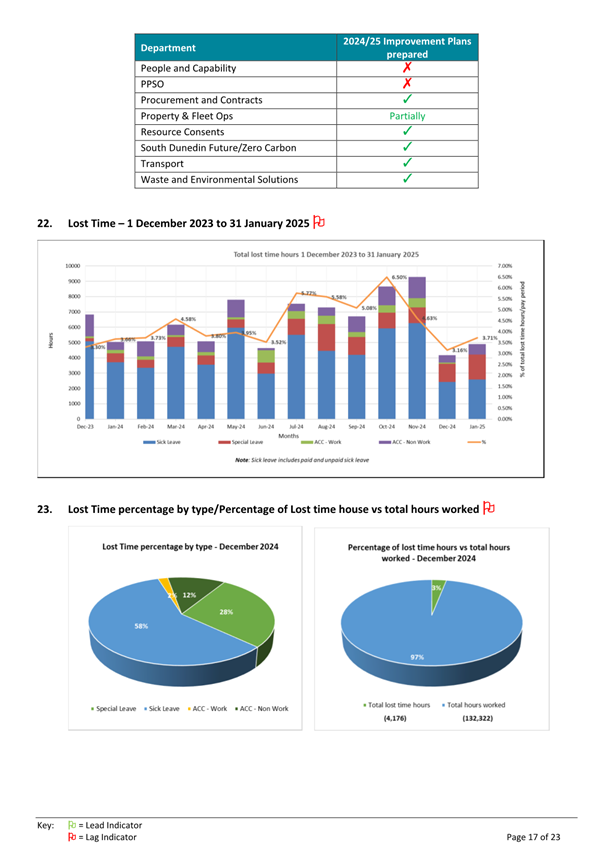

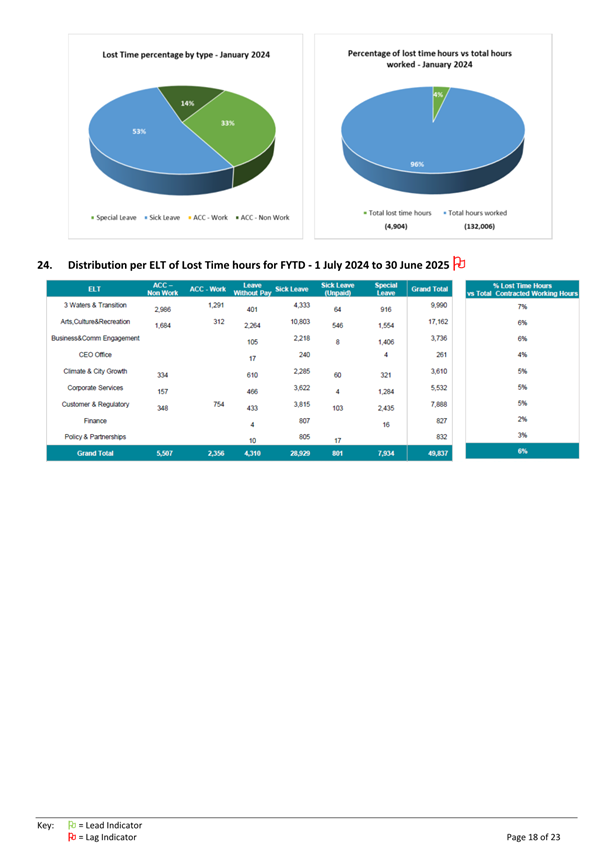

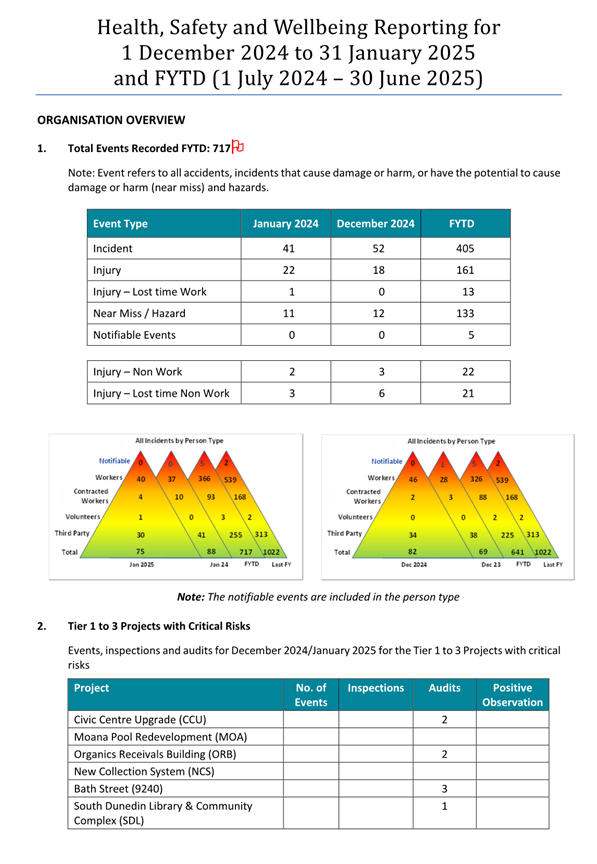

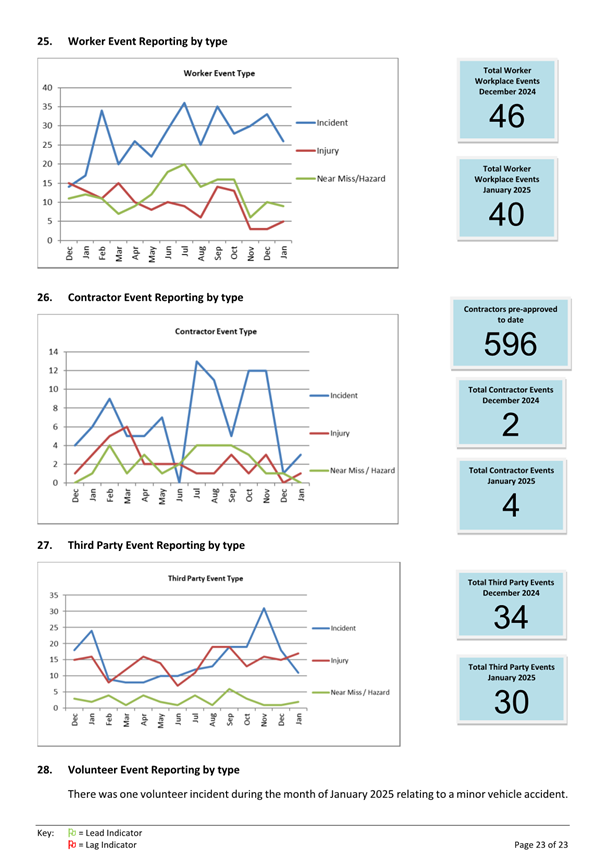

Health and Safety Monthly Reporting for December 2024 and

January 2025

Department: Health and Safety

EXECUTIVE SUMMARY

1 The

monthly Health, Safety and Wellbeing report for December 2024 and January 2025

is attached for consideration.

RECOMMENDATIONS

That the Subcommittee:

a) Notes the monthly

Health, Safety and Wellbeing report for December 2024 and January 2025.

Signatories

|

Author:

|

Jane Pearce - Health and Safety Manager

|

|

Authoriser:

|

Mike Cartwright – Acting General Manager Corporate

Services

|

Attachments

|

|

Title

|

Page

|

|

⇩a

|

HSW report for December

2024 and January 2025

|

87

|

|

|

Audit and Risk Subcommittee

10 March 2025

|

|

|

Audit and Risk Subcommittee

10 March 2025

|

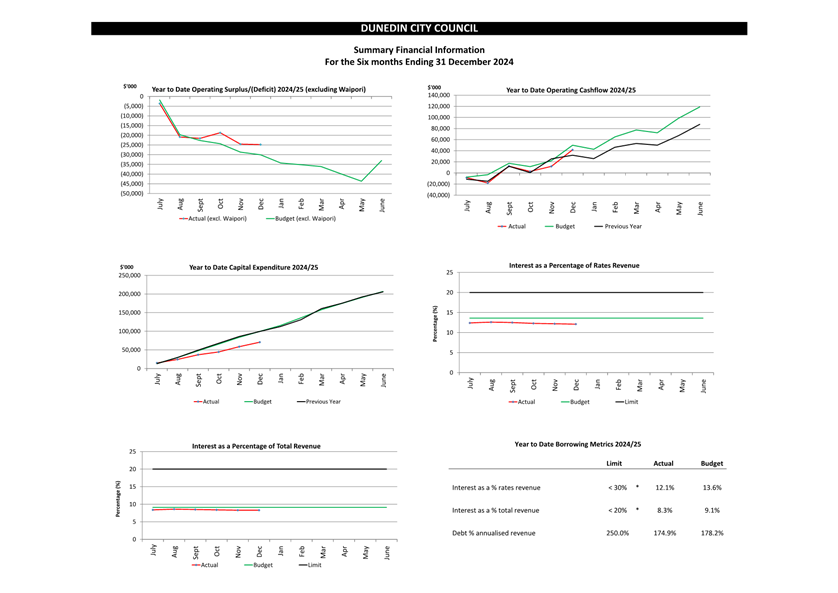

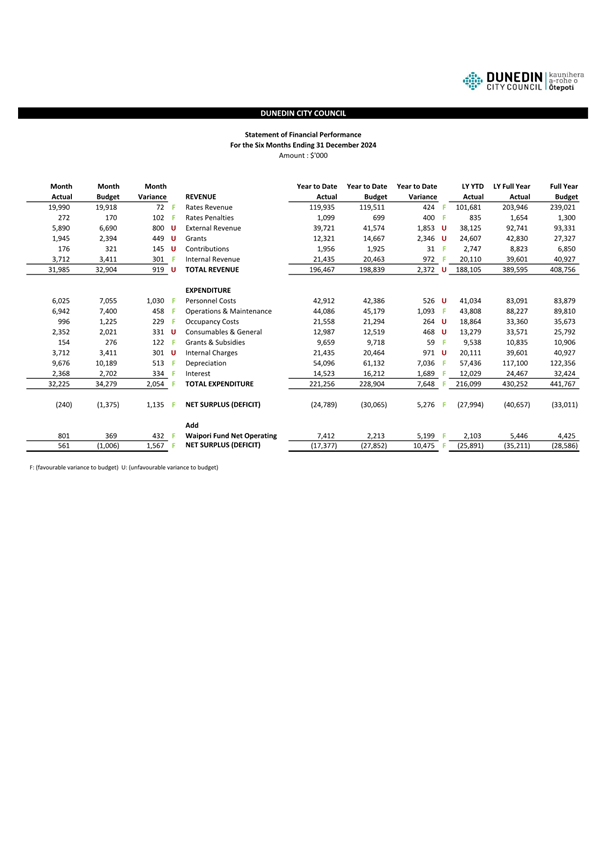

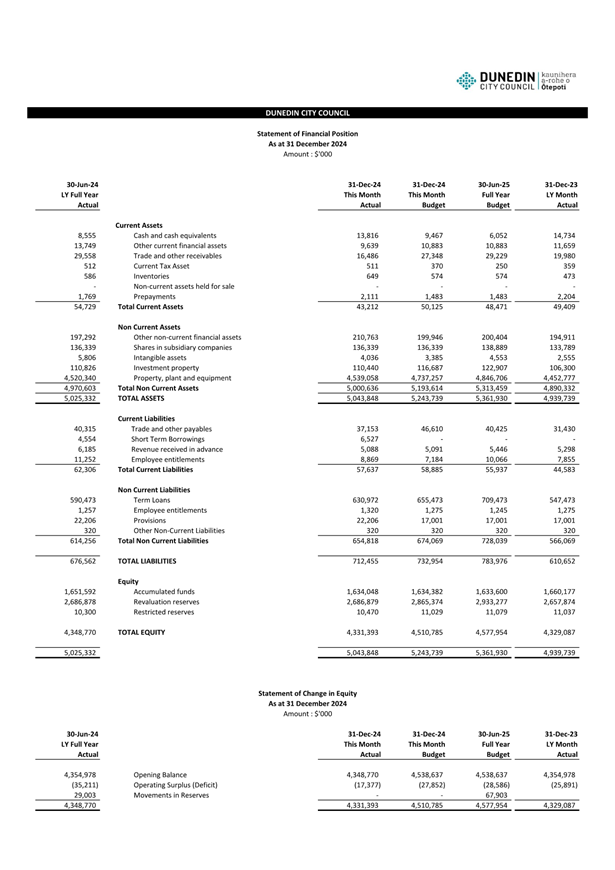

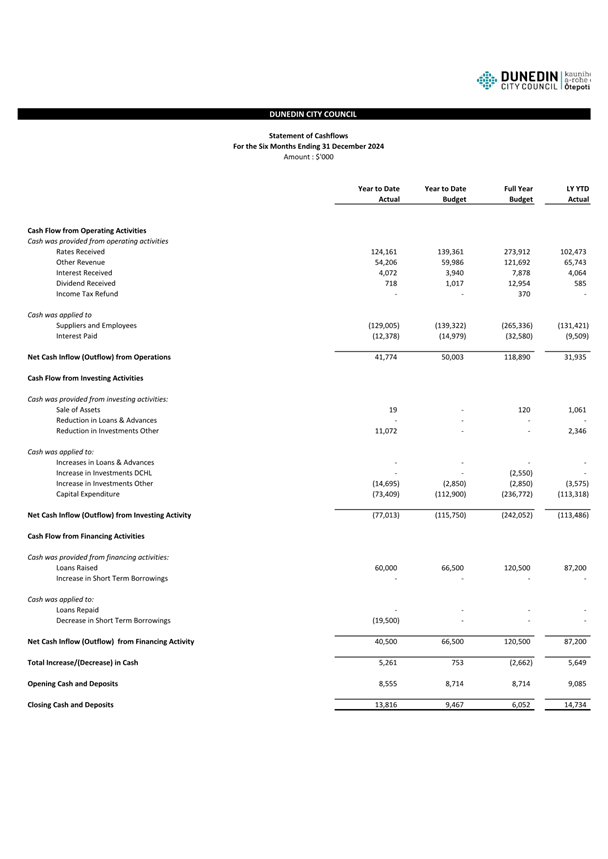

Financial Report - Period ended 31 December 2024

Department: Finance

EXECUTIVE SUMMARY

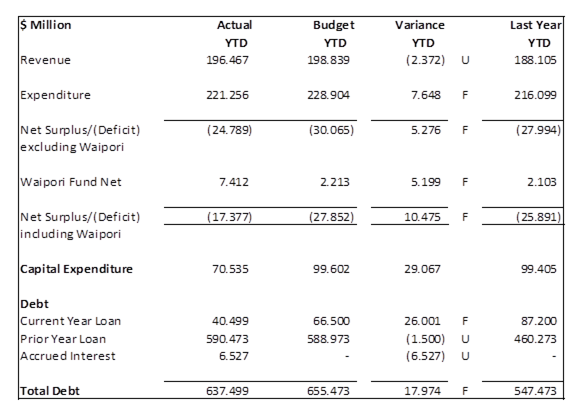

1 This

report provides the financial results for the period ended 31 December 2024 and

the financial position as at that date. This report was presented to the

Council meeting held on 26 February 2025.

2 As this is an administrative report only, there are no options or

Summary of Considerations.

Financial Overview

For the period ended 31

December 2024

RECOMMENDATIONS

That the Committee:

a) Notes the Financial

Performance for the period ended 31 December 2024 and the Financial Position as

at that date.

BACKGROUND

3 This

report provides the financial statements for the period ended 31 December

2024. It includes reports on financial performance,

financial position, cashflows and capital expenditure. Summary information

is provided in the body of this report with detailed results attached. The

operating result is also shown by group, including analysis by revenue and

expenditure type.

DISCUSSION

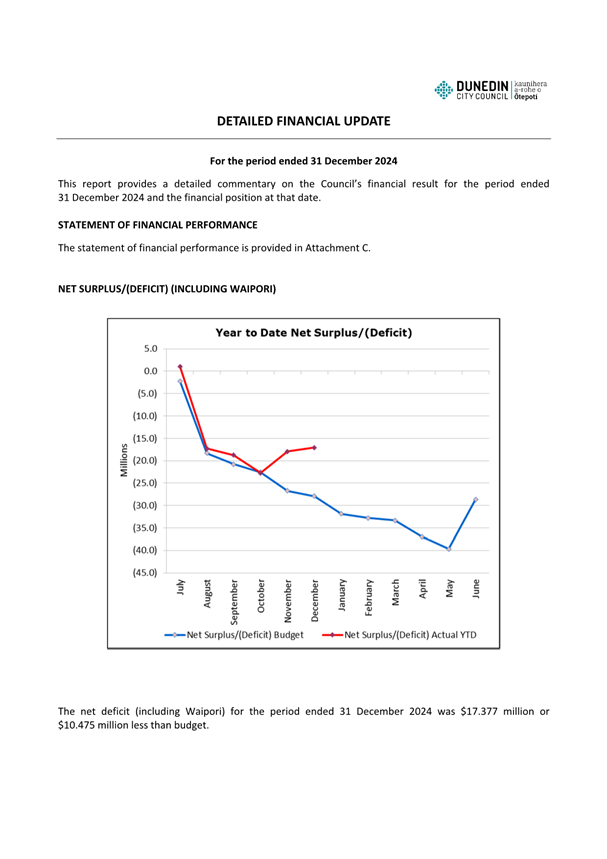

4 This

report includes a high-level summary of the financial information

to 31 December 2024. Please refer to Attachment I

for the detailed financial update.

Statement of

Financial Performance

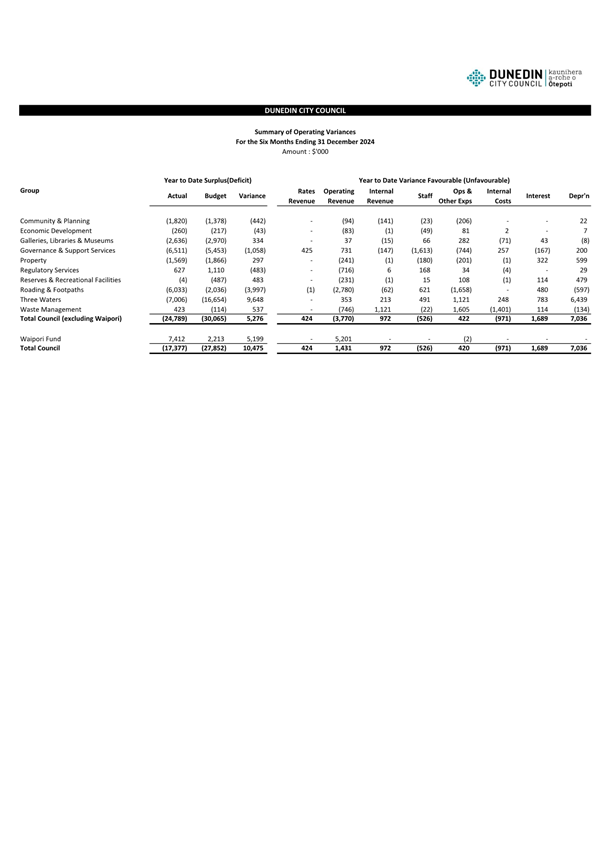

5 Revenue was $196.467 million for the period or $2.372 million less than

budget.

6 Operating revenue (external and internal combined) was unfavourable

$881k mainly due to lower-than-expected revenue from the Parking Services and

Aquatic Services activities.

7 Grants revenue was unfavourable $2.346 million reflecting funding

decisions by NZTA under the National Land Transport Programme, and timing of

the transport contractor work programme.

8 Expenditure

was $221.256 million for the period, or $7.648 million less than budget.

9 Personnel costs was unfavourable $526k, reflecting overtime payments

for 3 waters and union negotiated contract increases, which is being managed

with vacancy management. The month of December showed a favourable variance of

$1.030 million, primarily driven by changes in the annual leave provision as a

result of staff taking leave during the Christmas holiday period.

10 Operations

and maintenance expenditure was favourable $1.093 million; however, this

favourable variance was offset by an unfavourable $971k variance in internal

costs, due largely to landfill disposal costs for kerbside collections now

recorded as internal costs. Unfavourable Transport maintenance costs are more

than offset by under expenditure in other activities, including Three Waters

and Waste and Environmental Services. Transport costs included emergency

works totalling $1.718 million associated with the October rain event.

11 Depreciation

costs were favourable $7.036 million, mainly due to the revaluation of Three

Waters assets, and to a lesser extent Property and Parks assets.

12 Interest

costs were favourable $1.689 million, reflecting a lower interest rate than

budgeted and the timing of new loan advances.

13 Year to

date the Waipori Fund has reported a net operating surplus of $7.412 million,

$5.199 million more than budget. New Zealand and international equities saw

continued increases in value during December, largely offset however by a

reduction in value for Australian equities. Fixed term investment saw an

increase in value for the month, maintaining favourable results for the year to

date.

Statement of

Financial Position

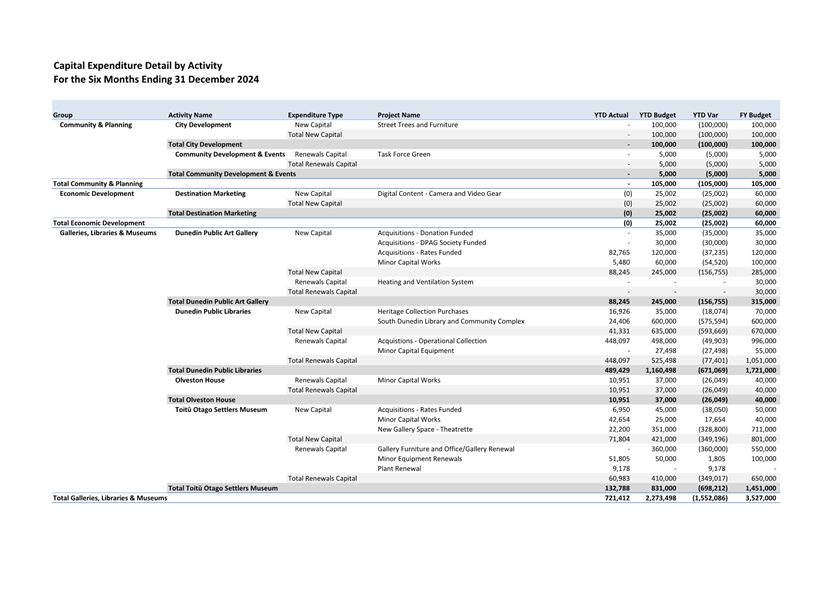

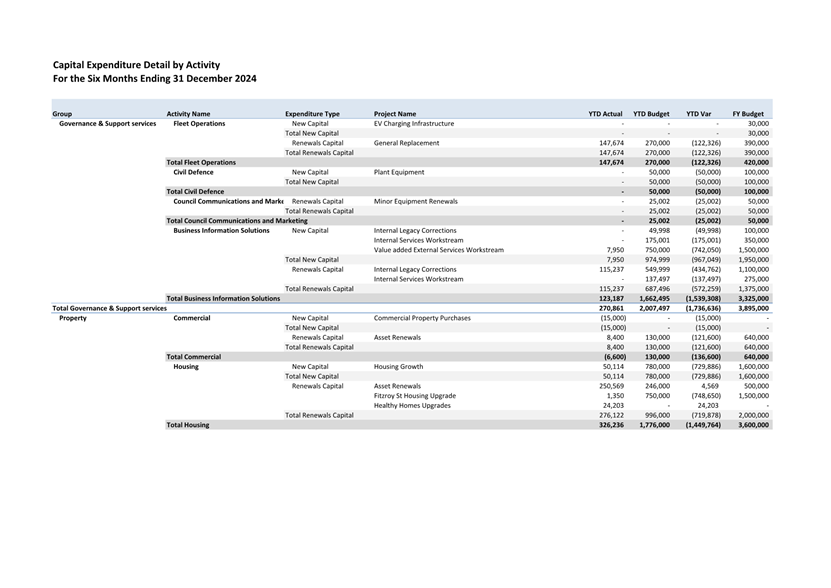

14 Capital

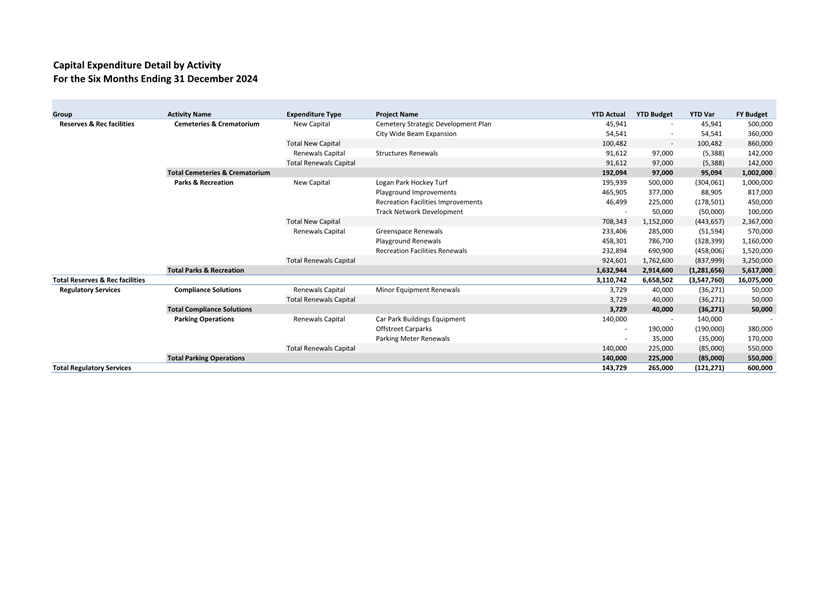

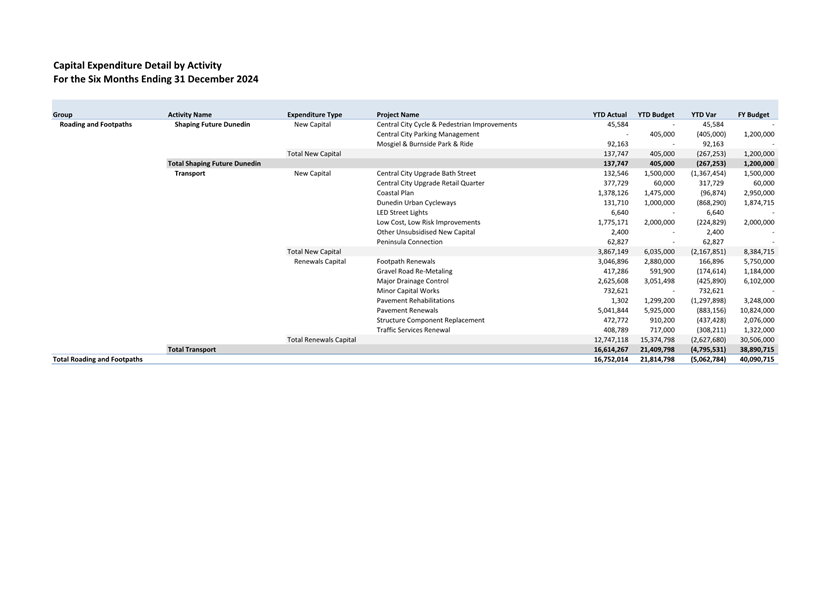

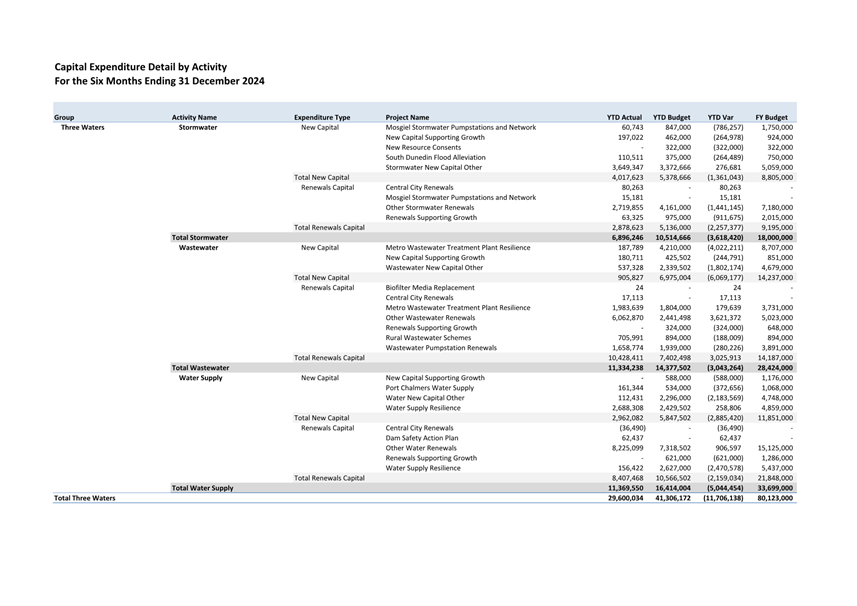

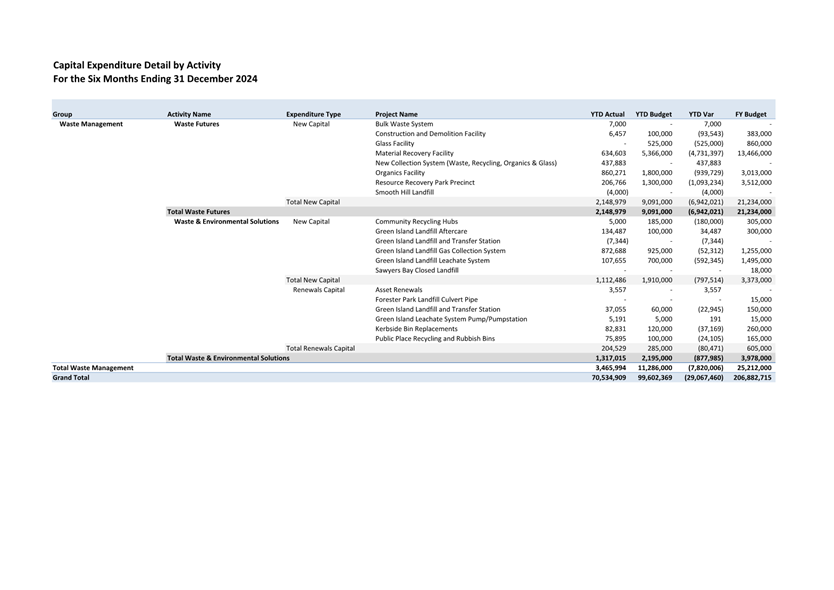

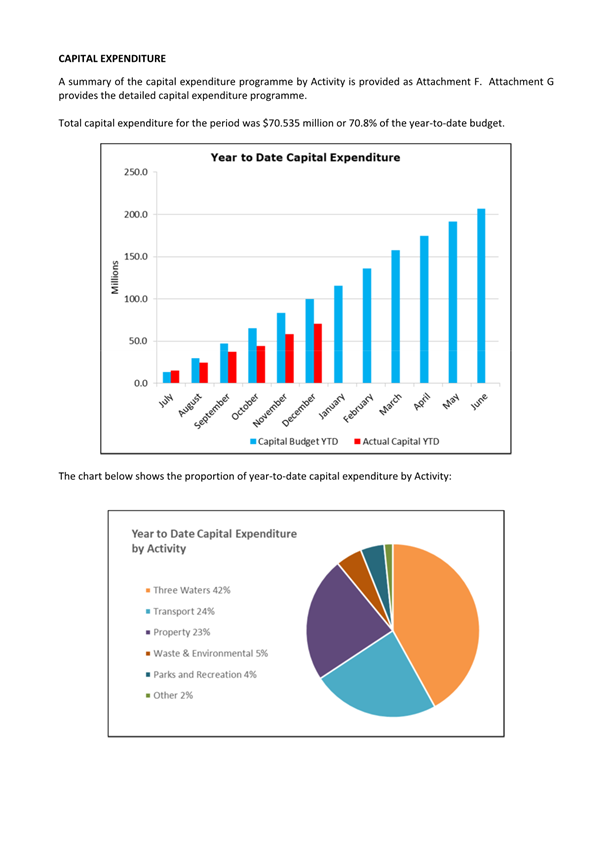

expenditure was $70.535 million or 70.8% of the year-to-date budget. Capital

expenditure in most activities was generally within budget for the period.

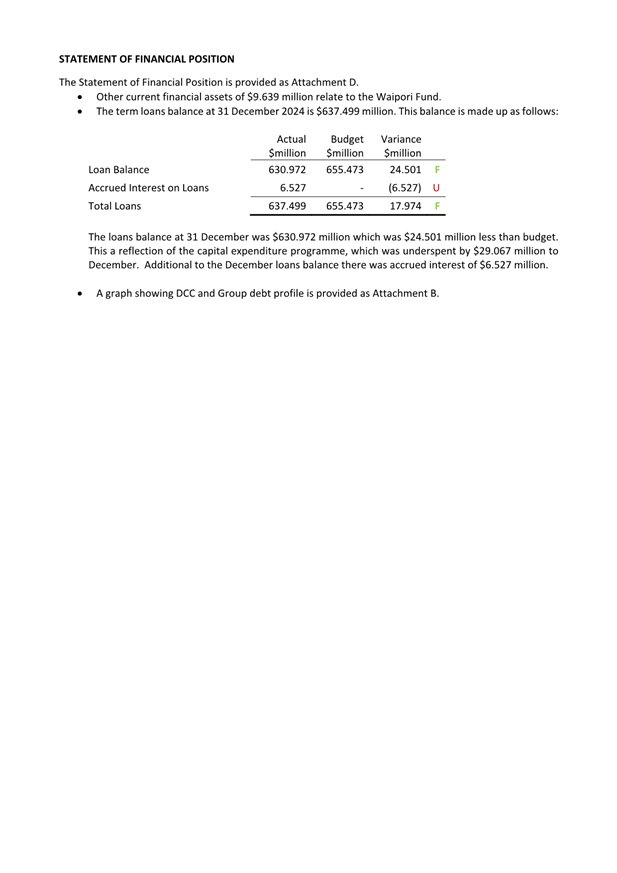

15 The loans

balance at 31 December was $630.972 million which was $24.501 million less than

budget. This a reflection of the capital expenditure programme, which was

underspent by $29.067 million to December. Additional to the December

loans balance there was accrued interest of $6.527 million.

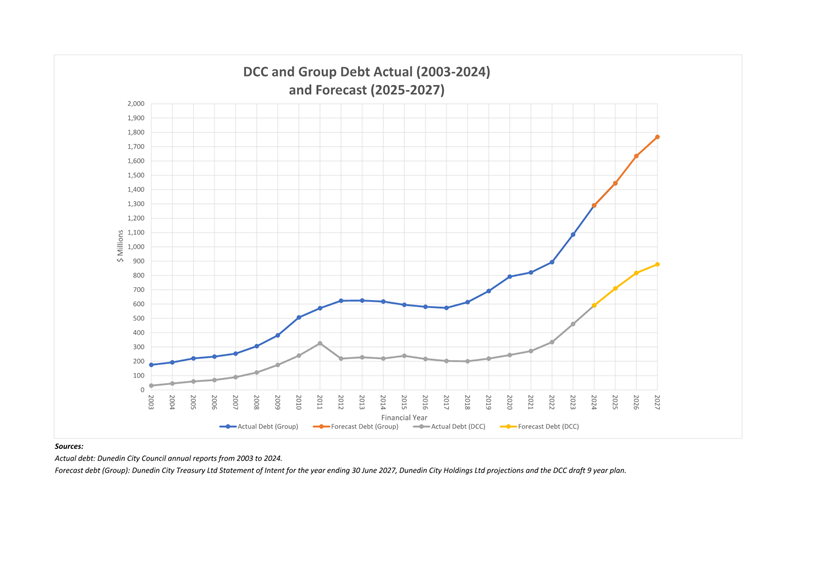

16 Attachment

A includes a chart showing actual group and DCC debt for the years ending June

2003-2024. It provides forecast information for the years ending June 2024-2027

based on the current Statements of Intent (SOI), and the first two years of the

draft 9 year plan.

OPTIONS

17 As this is an administrative report only, there are no options

provided.

NEXT STEPS

18 Financial

Result Reports continue be presented to future meetings of either the Finance

and Council Controlled Organisation Committee or Council.

Signatories

|

Author:

|

Hayden McAuliffe – Financial Services Manager

|

|

Authoriser:

|

Carolyn Allan – Chief Financial Officer

|

Attachments

|

|

Title

|

Page

|

|

⇩a

|

Dashboard Summary

Financial Information

|

113

|

|

⇩b

|

Debt Graph

|

114

|

|

⇩c

|

Statement of Financial

Performance

|

115

|

|

⇩d

|

Statement of Financial

Position

|

116

|

|

⇩e

|

Statement of Cashflow

|

117

|

|

⇩f

|

Capital Expenditure

Summary

|

118

|

|

⇩g

|

Capital Expenditure

Detailed Programme

|

119

|

|

⇩h

|

Operating Variances

|

126

|

|

⇩i

|

Detailed Financial

Update

|

127

|

|

|

Audit and Risk Subcommittee

10 March 2025

|

|

|

Audit and Risk Subcommittee

10 March 2025

|

|

|

Audit and Risk Subcommittee

10 March 2025

|

|

|

Audit and Risk Subcommittee

10 March 2025

|

|

|

Audit and Risk Subcommittee

10 March 2025

|

|

|

Audit and Risk Subcommittee

10 March 2025

|

|

|

Audit and Risk Subcommittee

10 March 2025

|

|

|

Audit and Risk Subcommittee

10 March 2025

|

|

|

Audit and Risk Subcommittee

10 March 2025

|

|

|

Audit and Risk Subcommittee

10 March 2025

|

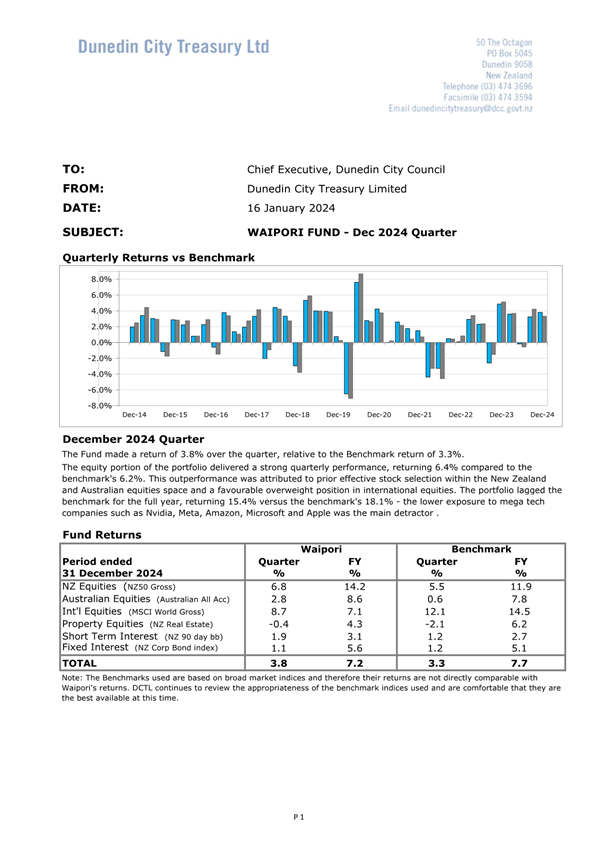

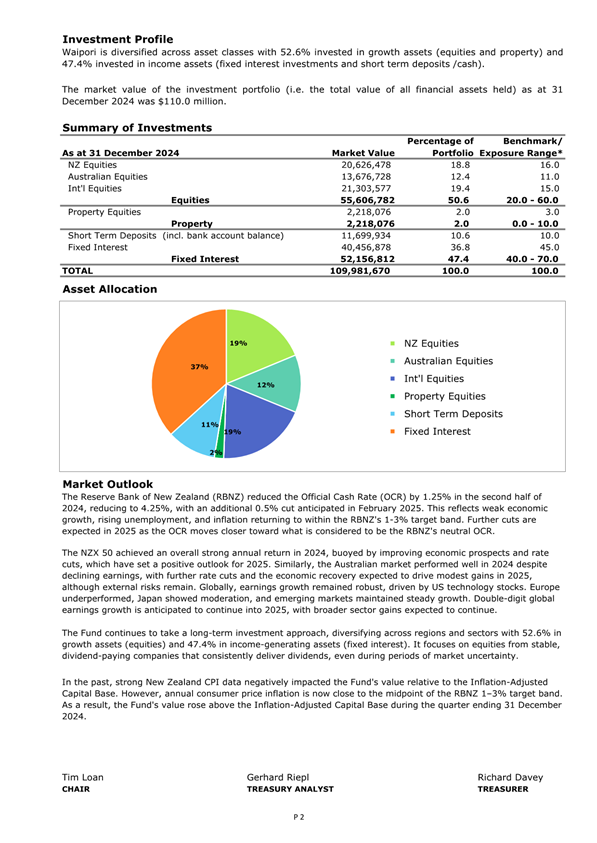

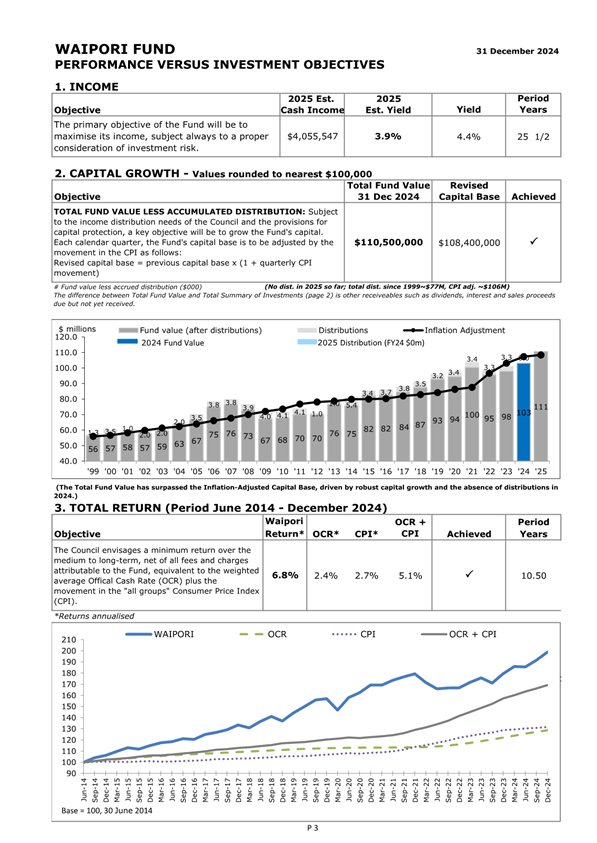

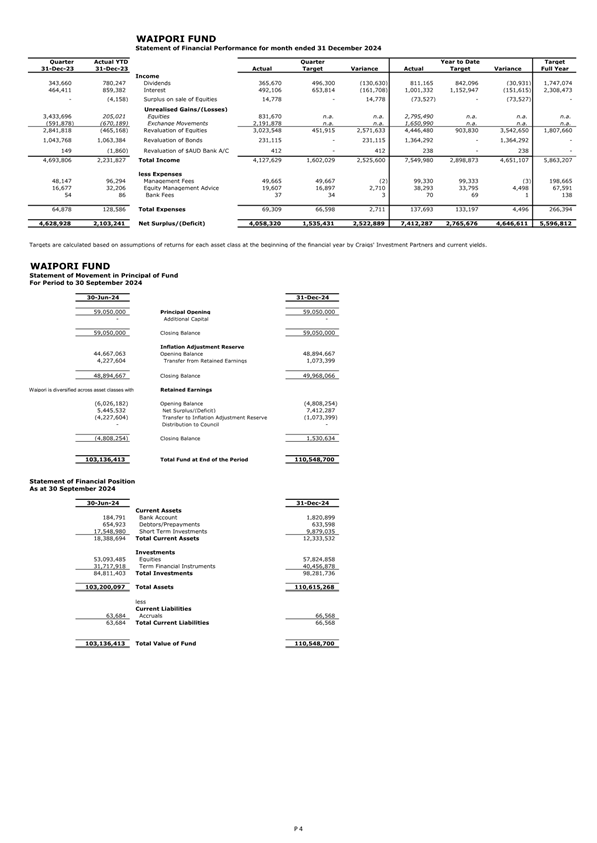

Waipori Fund - Quarter ending 31 December 2024

Department: Finance

EXECUTIVE SUMMARY

1 The

attached report from Dunedin City Treasury Limited provides information on the

results of the Waipori Fund for the quarter ended 31 December 2024.

RECOMMENDATIONS

That the Subcommittee:

a) Notes the report from

Dunedin City Treasury Limited on the Waipori Fund for the quarter ended 31

December 2024.

DISCUSSION

2 The

Waipori Fund Statement of Investment Policy and Objectives (SIPO) requires

quarterly reporting on the performance and financial position of the fund.

3 Dunedin

City Treasury Limited has provided the Waipori Fund report for the December

2024 quarter. The report is provided as Attachment A.

OPTIONS

4 As

this is a noting report, no options are provided.

NEXT STEPS

5 Quarterly

reporting on the performance and financial position of the fund will be

provided to future meetings of either the Financial and Council Controlled

Organisations Committee or Council.

Signatories

|

Authoriser:

|

Carolyn Allan - Chief Financial Officer

|

Attachments

|

|

Title

|

Page

|

|

⇩a

|

Waipori Fund - December

2024 Quarter

|

142

|

|

SUMMARY OF CONSIDERATIONS

|

|

Fit with purpose of Local Government

This decision enables democratic local

decision making and action by, and on behalf of communities.

|

|

Fit with strategic framework

|

|

Contributes

|

Detracts

|

Not applicable

|

|

Social Wellbeing Strategy

|

☐

|

☐

|

✔

|

|

Economic Development Strategy

|

☐

|

☐

|

✔

|

|

Environment Strategy

|

☐

|

☐

|

✔

|

|

Arts and Culture Strategy

|

☐

|

☐

|

✔

|

|

3 Waters Strategy

|

☐

|

☐

|

✔

|

|

Spatial Plan

|

☐

|

☐

|

✔

|

|

Integrated Transport Strategy

|

☐

|

☐

|

✔

|

|

Parks and Recreation Strategy

|

☐

|

☐

|

✔

|

|

Other strategic projects/policies/plans

|

☐

|

☐

|

✔

|

Reporting on the performance of the Waipori Fund does not

contribute directly to the Strategic Framework.

|

|

Māori Impact Statement

Investment returns from the Waipori Fund impact on the

level of rates payable, and therefore impact across all Dunedin communities

including Māori.

|

|

Sustainability

There are no impacts for sustainability.

|

|

LTP/Annual Plan / Financial Strategy /Infrastructure

Strategy

A review of the SIPO for the Waipori Fund will be taken

into account when developing a Financial Strategy for the 9 year plan

2025-34.

|

|

Financial considerations

Financial considerations are presented in the Waipori Fund

report for the March 2024 quarter.

|

|

Significance

This report is considered to be of low significance in

terms of the Council’s Significance and Engagement Policy.

|

|

Engagement – external

There has been no external engagement.

|

|

Engagement - internal

There has been no internal engagement.

|

|

Risks: Legal / Health and Safety etc.

There are no identified risks.

|

|

Conflict of Interest

There are no known conflicts of interest.

|

|

Community Boards

There are no implications for Community Boards.

|

|

|

Audit and Risk Subcommittee

10 March 2025

|

|

|

Audit and Risk Subcommittee

10 March 2025

|

Resolution to Exclude the

Public

That the Audit and Risk

Subcommittee:

Pursuant to the provisions of the

Local Government Official Information and Meetings Act 1987, exclude the public

from the following part of the proceedings of this meeting namely:

|

General subject of the matter to be considered

|

Reasons

for passing this resolution in relation to each matter

|

Ground(s) under

section 48(1) for the passing of this resolution

|

Reason for

Confidentiality

|

|

C1

Confirmation of the Confidential Minutes of Audit and Risk Subcommittee

meeting - 4 December 2024 - Public Excluded

|

S7(2)(h)

The

withholding of the information is necessary to enable the local authority to

carry out, without prejudice or disadvantage, commercial activities.

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to prejudice the supply

of similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

S7(2)(b)(i)

The

withholding of the information is necessary to protect information where the

making available of the information would disclose a trade secret.

S7(2)(i)

The

withholding of the information is necessary to enable the local authority to

carry on, without prejudice or disadvantage, negotiations (including

commercial and industrial negotiations).

S7(2)(b)(ii)

The

withholding of the information is necessary to protect information where the

making available of the information would be likely unreasonably to prejudice

the commercial position of the person who supplied or who is the subject of

the information.

|

.

|

|

|

C2

Treasury Risk Management Compliance Report

|

S7(2)(h)

The

withholding of the information is necessary to enable the local authority to

carry out, without prejudice or disadvantage, commercial activities.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C3

Report to the Council on the Audit of Dunedin City Council for the year end

30 June 2024

|

S7(2)(b)(ii)

The

withholding of the information is necessary to protect information where the

making available of the information would be likely unreasonably to prejudice

the commercial position of the person who supplied or who is the subject of

the information.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C4

9 Year Plan Audit - Update

|

S7(2)(b)(i)

The

withholding of the information is necessary to protect information where the

making available of the information would disclose a trade secret.

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to prejudice the supply

of similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

S7(2)(h)

The

withholding of the information is necessary to enable the local authority to

carry out, without prejudice or disadvantage, commercial activities.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C5

Dunedin City Holdings Ltd - Update on Audit and Risk Activity

|

S7(2)(b)(ii)

The

withholding of the information is necessary to protect information where the

making available of the information would be likely unreasonably to prejudice

the commercial position of the person who supplied or who is the subject of

the information.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C6

Internal Audit Workplan Update

|

S7(2)(b)(i)

The

withholding of the information is necessary to protect information where the

making available of the information would disclose a trade secret.

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to prejudice the supply

of similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

S7(2)(h)

The

withholding of the information is necessary to enable the local authority to

carry out, without prejudice or disadvantage, commercial activities.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C7

DCC Internal Audit Actions Update

|

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to prejudice the supply

of similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C8

DCC Risk 'Deep Dive' - Fraud Risk Management

|

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to prejudice the supply

of similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C9

Gifts and Hospitality Register

|

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of natural

persons, including that of a deceased person.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C10

Chairperson's Report

|

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of natural

persons, including that of a deceased person.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C11

Legal Matters

|

S7(2)(g)

The

withholding of the information is necessary to maintain legal professional privilege.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C12

Protected Disclosure Register - February 2025

|

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of natural

persons, including that of a deceased person.

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to prejudice the supply

of similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C13

Investigation Register - February 2025

|

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of natural

persons, including that of a deceased person.

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to prejudice the supply

of similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

This resolution is made in

reliance on Section 48(1)(a) of the Local Government Official Information and

Meetings Act 1987, and the particular interest or interests protected by

Section 6 or Section 7 of that Act, or Section 6 or Section 7 or Section 9 of

the Official Information Act 1982, as the case may require, which would be

prejudiced by the holding of the whole or the relevant part of the proceedings

of the meeting in public are as shown above after each item.

That Rudie Tomlinson (Director,

Audit New Zealand) be permitted to attend the meeting, after the public has

been excluded, because of his knowledge of Items C3. This knowledge,

which would been of assistance in relation to the matters discussed, was

relevant because they would be reporting on the item under consideration.