Notice of Meeting:

I hereby give notice that an ordinary meeting of the Audit

and Risk Subcommittee will be held on:

Date: Thursday

18 April 2019

Time: 1.30

pm

Venue: Otaru

Room, Civic Centre, The Octagon, Dunedin

Sue Bidrose

Audit and Risk Subcommittee

PUBLIC AGENDA

|

Chairperson

|

Susie Johnstone

|

|

|

Deputy Chairperson

|

|

|

|

Members

|

Janet Copeland

|

Mayor Dave Cull

|

|

|

Cr Doug Hall

|

Cr Mike Lord

|

|

|

Cr Chris Staynes

|

|

Senior Officer Dave

Tombs, General Manager Finance and Commercial

Governance Support Officer Wendy

Collard

Wendy Collard

Governance Support Officer

Telephone: 03 477 4000

Wendy.Collard@dcc.govt.nz

www.dunedin.govt.nz

Note: Reports

and recommendations contained in this agenda are not to be considered as

Council policy until adopted.

|

Audit and Risk Subcommittee

18 April 2019

|

|

ITEM TABLE OF CONTENTS PAGE

1 Apologies 4

2 Confirmation

of Agenda 4

3 Declaration

of Interest 5

4 Confirmation

of Minutes 11

4.1 Audit and Risk Subcommittee meeting - 21

February 2019 11

Part

A Reports (Committee has power to decide these matters)

5 Audit

and Risk Subcommittee Work Plan 2019 21

6 Annual

Report Timetable for Year Ended 30 June 2019 26

Resolution to Exclude the Public 27

|

Audit and Risk Subcommittee

18 April 2019

|

|

1 Apologies

An apology has been received from

Cr Chris Staynes.

That the Committee:

Accepts the apology from Cr

Chris Staynes.

2 Confirmation

of agenda

Note:

Any additions must be approved by resolution with an explanation as to why they

cannot be delayed until a future meeting.

|

Audit and Risk Subcommittee

18 April 2019

|

|

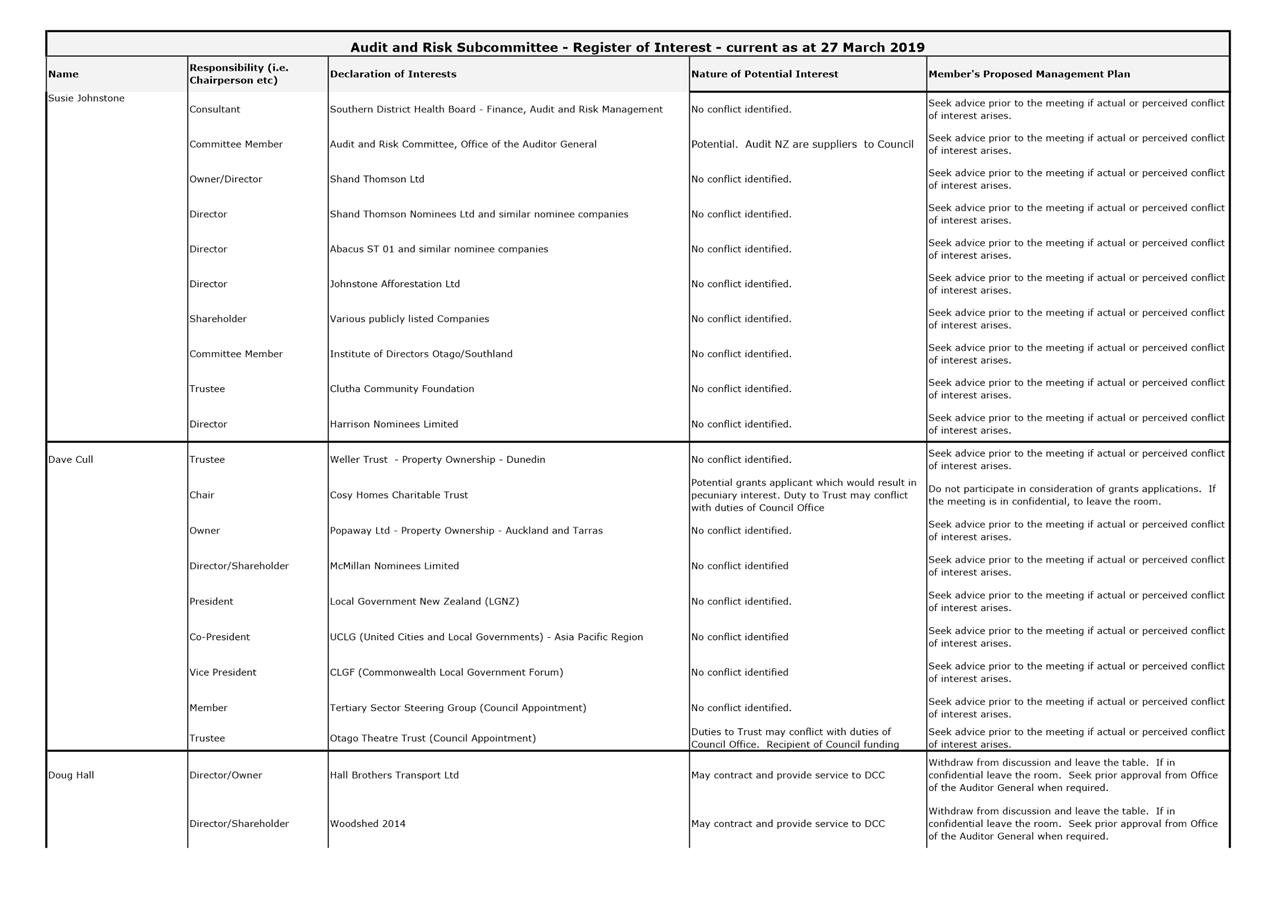

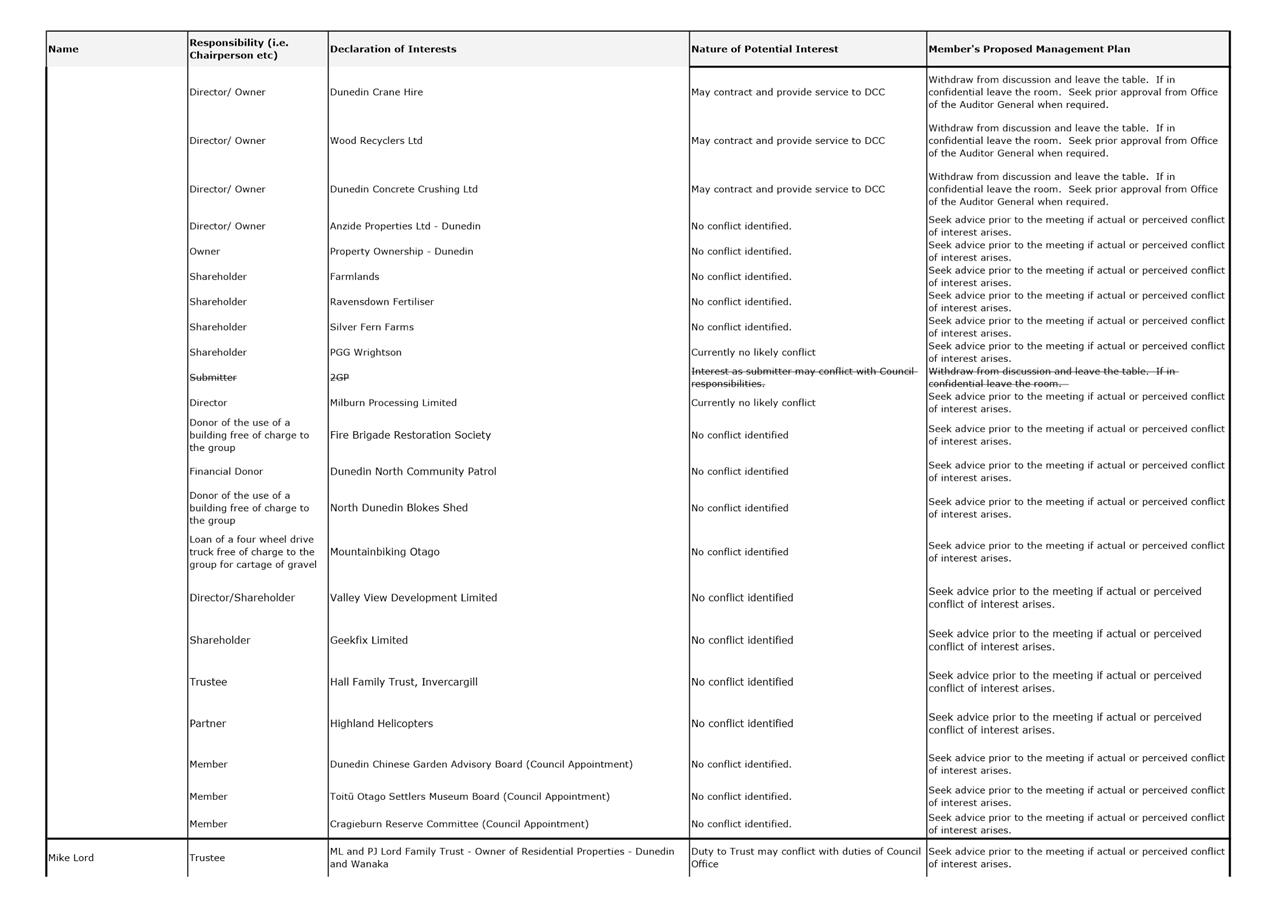

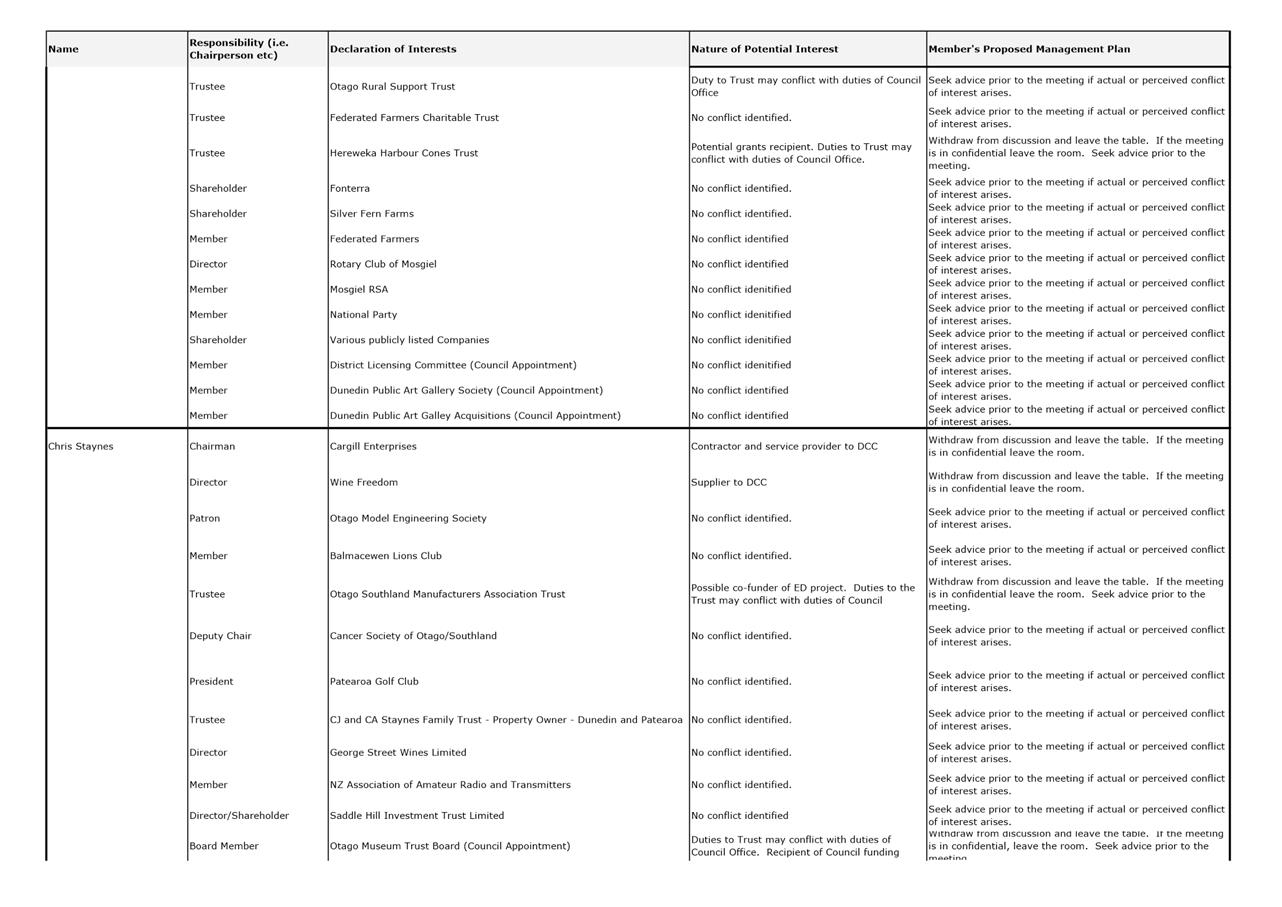

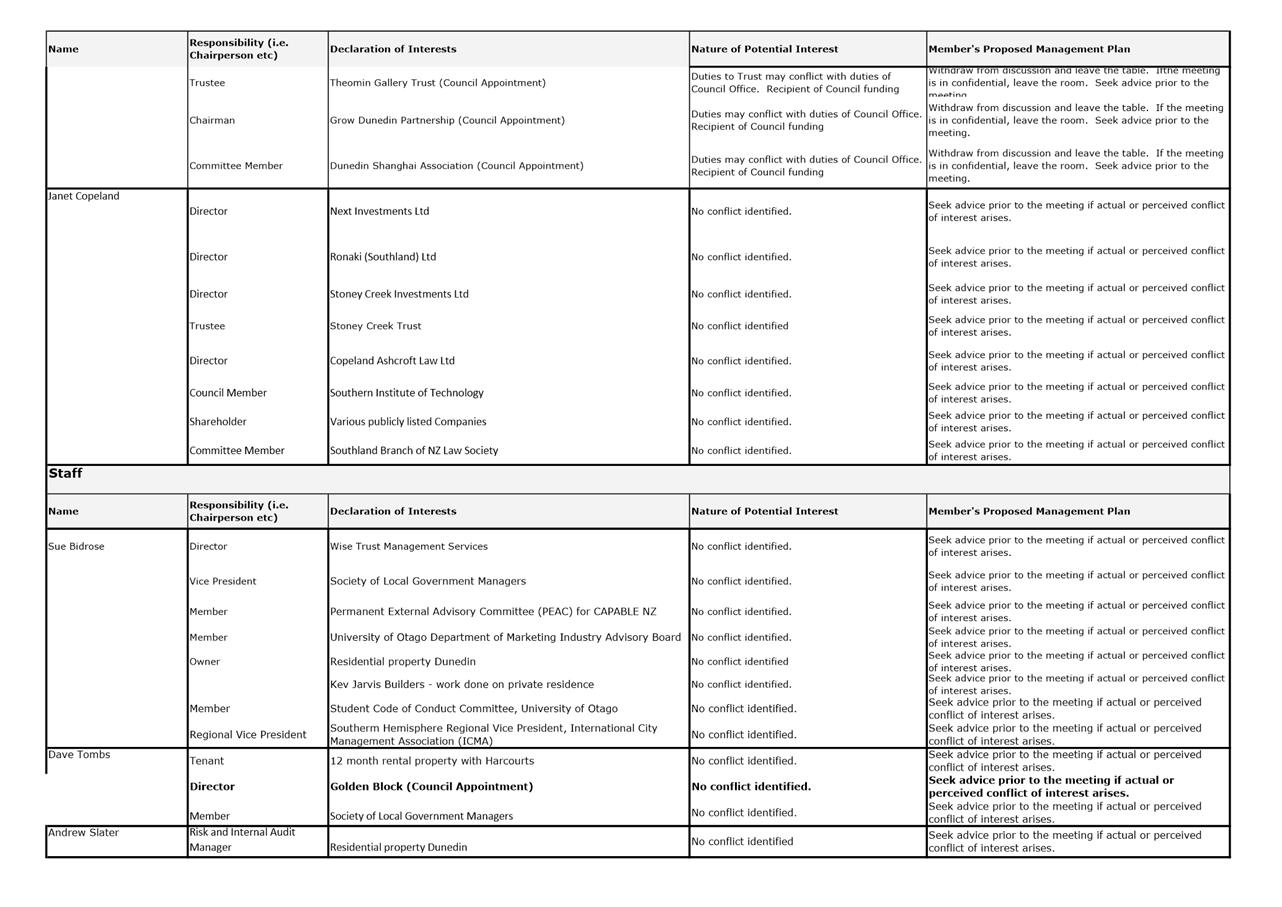

Declaration of Interest

EXECUTIVE SUMMARY

1. Members are reminded of the need

to stand aside from decision-making when a conflict arises between their role

as an elected representative and independent member and any private or other

external interest they might have.

2. Elected members and Independent

Members are reminded to update their register of interests as

soon as practicable, including amending the register at this meeting if

necessary.

|

RECOMMENDATIONS

That the Committee:

a) Notes/Amends

if necessary the Elected or Independent Members' Interest Register attached

as Attachment A; and

b) Confirms/Amends the proposed management plan for Elected or Independent Members'

Interests.

|

Attachments

|

|

Title

|

Page

|

|

⇩a

|

Elected and Independent

Members' Register of Interest

|

7

|

|

Audit and Risk Subcommittee

18 April 2019

|

|

|

Audit and Risk Subcommittee

18 April 2019

|

|

Confirmation

of Minutes

Audit and Risk Subcommittee meeting - 21 February 2019

|

RECOMMENDATIONS

That the Subcommittee:

Confirms the public part of the minutes of

the Audit and Risk Subcommittee meeting held on 21 February 2019 as a correct

record.

|

Attachments

|

|

Title

|

Page

|

|

A⇩

|

Minutes of Audit and

Risk Subcommittee meeting held on 21 February 2019

|

12

|

Audit and Risk Subcommittee

MINUTES

Minutes of an ordinary

meeting of the Audit and Risk Subcommittee held in the Mayor's Lounge, Civic

Centre, The Octagon, Dunedin on Thursday 21 February 2019, commencing at 1.00

pm

PRESENT

|

Chairperson

|

Susie Johnstone

|

|

|

|

|

|

|

Members

|

Mayor Dave Cull

|

Cr Doug Hall

|

|

|

Cr Mike Lord

|

Cr Chris Staynes

|

|

IN ATTENDANCE

|

Sue Bidrose (Chief Executive

Officer), Dave Tombs (General Manager Finance and Commercial), Andrew Slater

(Risk and Internal Audit Manager), Martyn Solomon (Crowe Horwath) and Phil

Sinclair (Crowe Horwath)

|

Governance Support Officer Wendy

Collard

|

1 Apologies

|

|

|

Moved (Susie Johnstone/Cr Chris Staynes):

That the Subcommittee:

Accepts the apology from

Ms Janet Copeland.

Motion

carried (AR/2019/001)

|

|

2 Confirmation

of agenda

|

|

|

Moved (Susie Johnstone/Cr Chris Staynes):

That the Committee:

Confirms the agenda

without addition or alteration

Motion

carried (AR/2019/002)

|

3 Declarations

of interest

Members were

reminded of the need to stand aside from decision-making when a conflict arose

between their role as an elected representative and any private or other

external interest they might have.

|

|

Moved (Susie Johnstone/Cr Doug Hall):

That the Subcommittee:

a) Notes the

Elected or Independent Members' Interest; and

b) Confirms

the proposed management plan for Elected or Independent Members' Interests.

Motion

carried (AR/2019/003)

|

4 Confirmation

of Minutes

|

4.1 Audit and Risk

Subcommittee meeting - 6 December 2018

|

|

|

Moved (Susie Johnstone/Cr Chris Staynes):

That the Subcommittee:

Confirms

the public part of the minutes of the Audit and Risk Subcommittee meeting

held on 6 December 2018 as a correct record.

Motion

carried (AR/2019/004)

|

Part

A Reports

|

5 Audit

and Risk Subcommittee Work Plan 2019

|

|

|

A report from Civic provided

a copy of the updated Audit and Risk Subcommittee Work Plan 2019.

|

|

|

Moved (Susie Johnstone/Cr Mike Lord):

That the Subommittee:

a) Notes

the Audit and Risk Subcommittee Work Plan.

Motion

carried (AR/2019/005)

|

|

Resolution to exclude the public

|

|

Moved (Cr Mike Lord/Cr Doug Hall):

That the Committee:

Pursuant

to the provisions of the Local Government Official Information and Meetings

Act 1987, exclude the public from the following part of the proceedings of

this meeting namely:

|

General

subject of the matter to be considered

|

Reasons

for passing this resolution in relation to each matter

|

Ground(s) under

section 48(1) for the passing of this resolution

|

Reason for

Confidentiality

|

|

C1

Audit and Risk Subcommittee meeting - 6 December 2018 - Public Excluded

|

S7(2)(c)(ii)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or

could be compelled to provide under the authority of any enactment, where

the making available of the information would be likely to damage the

public interest.

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or

could be compelled to provide under the authority of any enactment, where

the making available of the information would be likely to prejudice the

supply of similar information or information from the same source and it is

in the public interest that such information should continue to be

supplied.

S7(2)(b)(ii)

The

withholding of the information is necessary to protect information where

the making available of the information would be likely unreasonably to

prejudice the commercial position of the person who supplied or who is the

subject of the information.

S7(2)(h)

The

withholding of the information is necessary to enable the local authority

to carry out, without prejudice or disadvantage, commercial activities.

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of

natural persons, including that of a deceased person.

S6(b)

The

making available of the information would be likely to endanger the safety

of a person.

|

.

|

|

|

C2

Audit and Risk Subcommittee Action List Report

|

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or

could be compelled to provide under the authority of any enactment, where

the making available of the information would be likely to prejudice the

supply of similar information or information from the same source and it is

in the public interest that such information should continue to be

supplied.

|

S48(1)(a)

The public conduct of the part of the meeting

would be likely to result in the disclosure of information for which good

reason for withholding exists under section 7.

|

|

|

C3

Internal Audit WorkPlan Update - February 2019

|

S7(2)(b)(ii)

The

withholding of the information is necessary to protect information where

the making available of the information would be likely unreasonably to

prejudice the commercial position of the person who supplied or who is the

subject of the information.

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or

could be compelled to provide under the authority of any enactment, where

the making available of the information would be likely to prejudice the

supply of similar information or information from the same source and it is

in the public interest that such information should continue to be supplied.

S7(2)(h)

The

withholding of the information is necessary to enable the local authority

to carry out, without prejudice or disadvantage, commercial activities.

|

S48(1)(a)

The public conduct of the part of the meeting

would be likely to result in the disclosure of information for which good

reason for withholding exists under section 7.

|

|

|

C4

Update on the DCC Internal Audit Actions Register - February 2019

|

S7(2)(c)(ii)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or

could be compelled to provide under the authority of any enactment, where

the making available of the information would be likely to damage the

public interest.

|

S48(1)(a)

The public conduct of the part of the meeting

would be likely to result in the disclosure of information for which good

reason for withholding exists under section 7.

|

|

|

C5

Update on the DCC External Audit Actions Register - February 2019

|

S7(2)(c)(ii)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or

could be compelled to provide under the authority of any enactment, where

the making available of the information would be likely to damage the

public interest.

|

S48(1)(a)

The public conduct of the part of the meeting

would be likely to result in the disclosure of information for which good

reason for withholding exists under section 7.

|

|

|

C6

Strategic Risk Register - Update February 2019

|

S7(2)(c)(ii)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or

could be compelled to provide under the authority of any enactment, where

the making available of the information would be likely to damage the

public interest.

|

S48(1)(a)

The public conduct of the part of the meeting

would be likely to result in the disclosure of information for which good

reason for withholding exists under section 7.

|

|

|

C7

Audit and Risk Subcommittee Policy Update Report

|

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or

could be compelled to provide under the authority of any enactment, where

the making available of the information would be likely to prejudice the

supply of similar information or information from the same source and it is

in the public interest that such information should continue to be

supplied.

|

S48(1)(a)

The public conduct of the part of the meeting

would be likely to result in the disclosure of information for which good

reason for withholding exists under section 7.

|

|

|

C8

Purchase Card Report

|

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of

natural persons, including that of a deceased person.

|

S48(1)(a)

The public conduct of the part of the meeting

would be likely to result in the disclosure of information for which good

reason for withholding exists under section 7.

|

This report is

confidential because it refers and impacts Council staff positions where

those staff have not had the opportunity to respond or comment on the

report..

|

|

C9

Health and Safety Monthly Report for December 2018

|

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of

natural persons, including that of a deceased person.

|

S48(1)(a)

The public conduct of the part of the meeting

would be likely to result in the disclosure of information for which good

reason for withholding exists under section 7.

|

The information

relates to the actions of individual staff who could be identified.

This would breach their privacy and potentially prejudice any processes

which may need to be managed..

|

|

C10

Dunedin City Holdings Ltd - Update on Audit and Risk Activity

|

S7(2)(b)(ii)

The

withholding of the information is necessary to protect information where

the making available of the information would be likely unreasonably to

prejudice the commercial position of the person who supplied or who is the

subject of the information.

|

S48(1)(a)

The public conduct of the part of the meeting

would be likely to result in the disclosure of information for which good

reason for withholding exists under section 7.

|

|

|

C11

Treasury Risk Management Compliance Report

|

S7(2)(h)

The

withholding of the information is necessary to enable the local authority

to carry out, without prejudice or disadvantage, commercial activities.

|

S48(1)(a)

The public conduct of the part of the meeting

would be likely to result in the disclosure of information for which good

reason for withholding exists under section 7.

|

|

|

C12

Investigation Report 1

|

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of

natural persons, including that of a deceased person.

S7(2)(c)(ii)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or

could be compelled to provide under the authority of any enactment, where

the making available of the information would be likely to damage the

public interest.

S7(2)(f)(ii)

The

withholding of the information is necessary to maintain the effective

conduct of public affairs through the protection of such members, officers,

employees and persons from improper pressure or harassment.

|

S48(1)(a)

The public conduct of the part of the meeting

would be likely to result in the disclosure of information for which good

reason for withholding exists under section 7.

|

|

|

C13

Investigation Register

|

S6(b)

The

making available of the information would be likely to endanger the safety

of a person.

|

S48(1)(a)

The public conduct of the part of the meeting

would be likely to result in the disclosure of information for which good

reason for withholding exists under section 6.

|

The matters detailed

in this report are subject to investigation and information should remain

confidential so as not to prejudice the investigation and any possible

outcomes of the investigation..

|

|

C14

Protected Disclosure Register

|

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of

natural persons, including that of a deceased person.

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or

could be compelled to provide under the authority of any enactment, where

the making available of the information would be likely to prejudice the

supply of similar information or information from the same source and it is

in the public interest that such information should continue to be

supplied.

|

S48(1)(a)

The public conduct of the part of the meeting

would be likely to result in the disclosure of information for which good

reason for withholding exists under section 7.

|

|

This resolution is made in

reliance on Section 48(1)(a) of the Local Government Official Information and

Meetings Act 1987, and the particular interest or interests protected by

Section 6 or Section 7 of that Act, or Section 6 or Section 7 or Section 9 of

the Official Information Act 1982, as the case may require, which would be

prejudiced by the holding of the whole or the relevant part of the

proceedings of the meeting in public are as shown above after each item.

That Martyn Solomon (Crowe Horwath) and Phil

Sinclair (Crowe Horwath) be permitted to remain at the meeting, after the

public has been excluded, because of their knowledge of Items C3 and

C4. This knowledge, which would be of assistance in relation to the

matters discussed, was relevant because they would be reporting on the item

under consideration.

Motion

carried (AR/2019/006)

|

The meeting moved into confidential at 1.06 pm and concluded

at 2.51 pm.

..............................................

CHAIRPERSON

|

Audit and Risk Subcommittee

18 April 2019

|

|

Part

A Reports

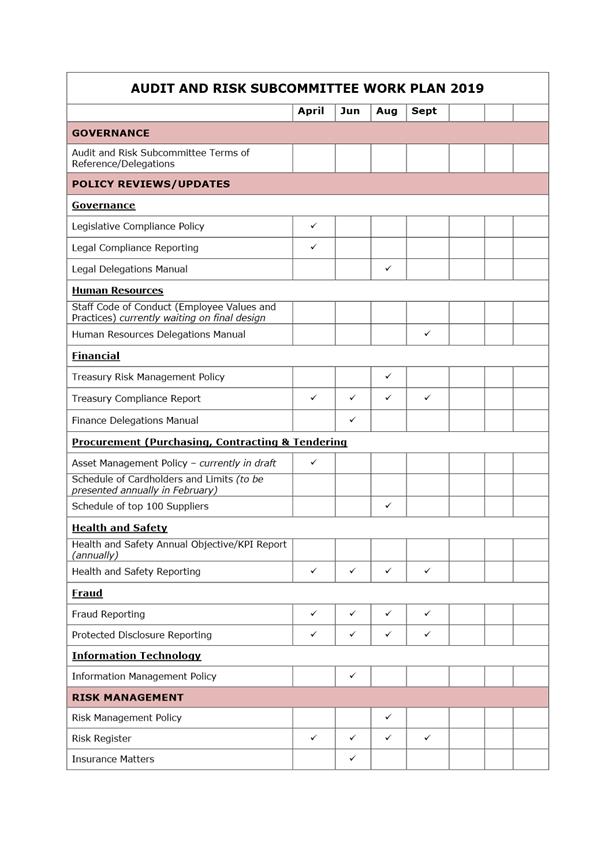

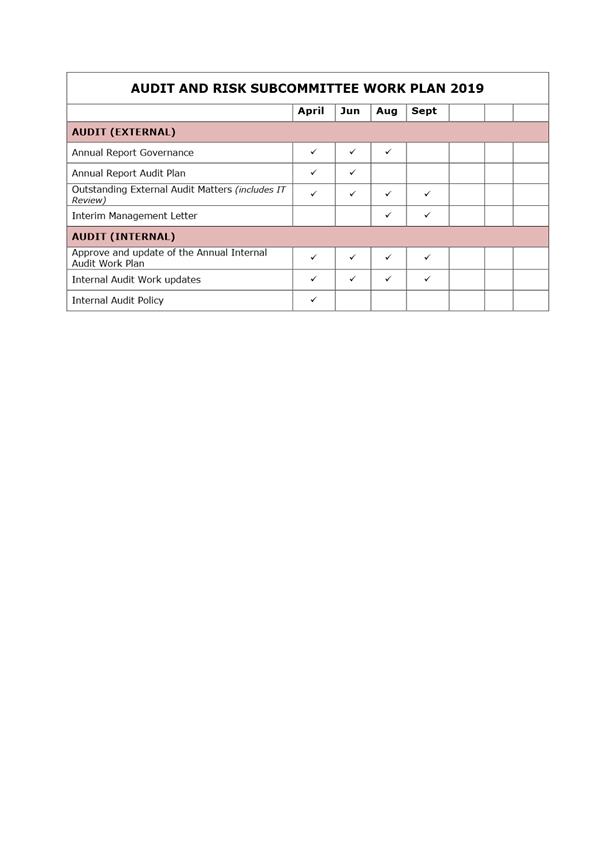

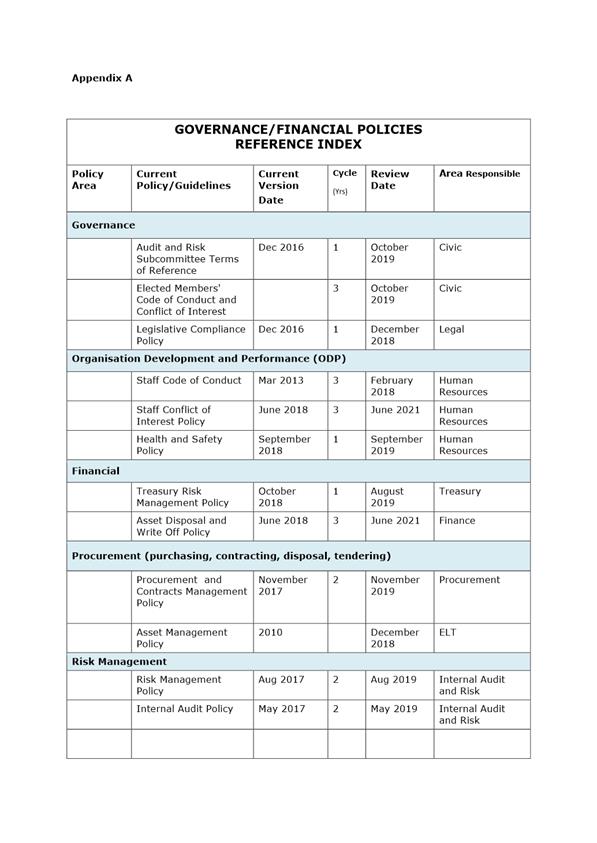

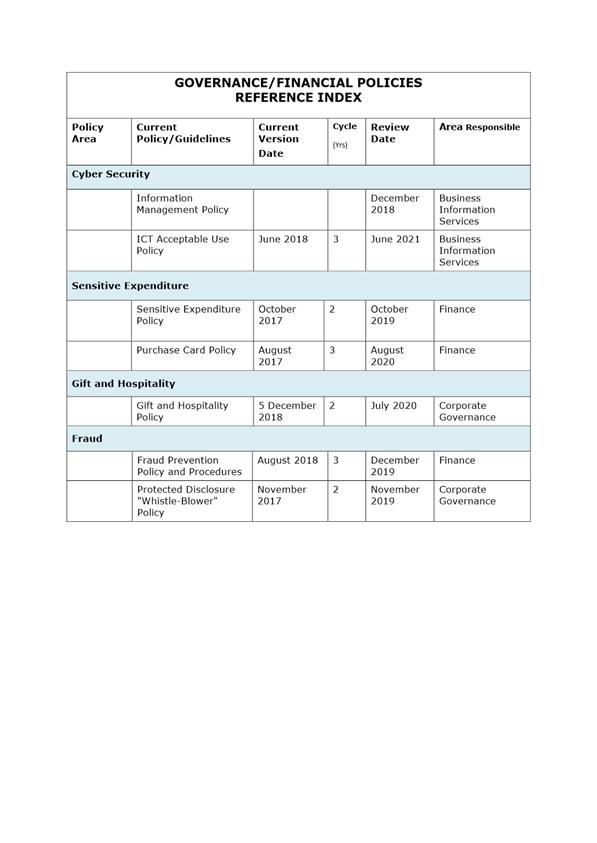

Audit and Risk Subcommittee Work Plan 2019

Department: Civic

EXECUTIVE SUMMARY

1 This

report provides a copy of the updated Audit and Risk Subcommittee Work Plan

2019. Please note that the Governance and Financial Policies are included

as an appendix to the Work Plan.

2 It should

be noted that the items without ticks shown have not been scheduled for action

before the end of the triennium.

3 As this

is an administrative report only, the Summary of Considerations is not

required.

|

RECOMMENDATIONS

That the Subcommittee:

a) Notes the

Audit and Risk Subcommittee Work Plan.

|

Signatories

|

Author:

|

Wendy Collard - Governance Support Officer

|

|

Authoriser:

|

Sharon Bodeker - Team Leader Civic

|

Attachments

|

|

Title

|

Page

|

|

⇩a

|

Audit and Risk

Subcommittee workplan

|

22

|

|

Audit and Risk Subcommittee

18 April 2019

|

|

|

Audit and Risk Subcommittee

18 April 2019

|

|

Annual Report Timetable for Year Ended 30 June

2019

Department: Finance

EXECUTIVE SUMMARY

1 This

report documents the timetable in relation to the preparation and approval of

the Dunedin City Council Annual Report for the year ended 30 June 2019.

2 It also

considers new accounting standards applicable to the reporting period.

|

RECOMMENDATIONS

That the Committee:

a) Notes the

report as presented.

|

BACKGROUND

3 Following

a request from the Audit and Risk Subcommittee, staff have prepared a high

level timetable associated with the annual report process for the year ended 30

June 2019.

DISCUSSION

4 The

following draft timetable relates to the preparation and approval of the annual

report for the year ended 30 June 2019.

5 The dates

are currently indicative pending receipt of the Audit Plan letter from Audit

New Zealand. The primary driver of the proposed dates is to have the

annual report approved by the outgoing Council – last meeting scheduled

for 8 October 2019.

6 This

report also includes a summary of the ‘significant considerations’

relevant to the 30 June 2019 financial statements. These have been

discussed with the DCHL Financial Accountant who has provided to the group

financial officers in these matters.

|

Date

|

|

Task

|

|

|

|

|

|

18-Apr-19

|

|

Audit Plan

Letter - Audit NZ

|

|

|

|

|

|

29-Apr-19

|

|

Interim

Audit Commences

|

|

|

|

|

|

28-Jun-19

|

|

Draft

Interim Audit management report issued to management

|

|

|

|

|

|

19-Jul-19

|

|

Management

feedback on Interim Audit Management report to

|

|

|

|

Audit NZ

|

|

|

|

|

|

8-Aug-19

|

|

Interim

Audit management report to Audit & Risk

|

|

|

|

|

|

19-Aug-19

|

|

Draft

parent financial statement available for audit

|

|

|

|

|

|

TBC

|

|

Parent

audit commences

|

|

|

|

|

|

2-Sep-19

|

|

DCHL Group

financial statements available for audit

|

|

|

|

|

|

9-Sep-19

|

|

Draft DCC

Group financial statements available for audit

|

|

|

|

|

|

12-Sep-19

|

|

Verbal

Audit clearance for DCHL Group from Audit NZ

|

|

|

|

|

|

19-Sep-19

|

|

DCHL

Annual Report approved by the DCHL Board

|

|

|

|

|

|

23-Sep-19

|

|

DCC Annual

Report available for audit (including commentary Mayor

|

|

|

|

and Chief

Executive)

|

|

|

|

|

|

27-Sep-19

|

|

Verbal

audit clearance from Audit NZ

|

|

|

|

|

|

30-Sep-19

|

*

|

Annual

report presented to Audit and Risk for confirmation and

|

|

|

|

endorsement

|

|

|

|

|

|

8-Oct-19

|

|

Annual

Report presented to Council for approval.

|

|

|

|

Letters of

Representation signed (Governance and Management)

|

|

|

|

|

|

8-Oct-19

|

|

Audit

Opinion Issued

|

|

|

|

|

|

28-Oct-19

|

|

Summary

annual report available for audit

|

|

|

|

|

|

31-Oct-19

|

|

Draft

Final Audit management report issued to management

|

|

|

|

|

|

TBA

|

|

Final

Audit management report to Audit & Risk

|

|

|

|

|

|

|

|

|

|

|

|

* Date to

be confirmed

|

NZ IFRS 9 Financial Instruments

7 Effective

date 30 June 2019 for the for-profit entities in the DCHL Group.

8 PBE’s

effective date is 30 June 2022; however the DCC will early adopt, noting that

the external hedging activity is held within Dunedin City Treasury Limited.

9 Changes

include how we classify and measure financial assets as well as how we assess

them for impairment. The new IFRS 9 impairment model is forward-looking, being

based on expected credit losses (ECLs) rather than actual losses incurred.

10 IFRS 9’s new

hedge accounting model is more closely aligned with an entity’s risk

management strategies and offers some simplifications to hedge accounting.

11 New disclosure

requirements will apply – systems and control changes may be necessary to

capture the data required noting again that these changes will be reflected in

the DCHL Group report presented for consolidation with the DCC.

NZ IFRS 15 Revenue from

Contracts with Customers

12 Effective date 30

June 2019 for the for-profit entities in the DCHL Group.

13 PBE’s have

already adopted their equivalent standard.

14 Many revenue

transactions are straightforward, but some can be highly complex. It might be

difficult to determine what the entity has committed to deliver, how much and

when revenue should be recognised.

15 This revenue

standard provides principles that an entity applies to report useful

information about the amount, timing, and uncertainty of revenue and cash flows

arising from its contracts to provide goods or services to customers. The core

principle requires an entity to recognise revenue to depict the transfer of

goods or services to customers in an amount that reflects the consideration

that it expects to be entitled to in exchange for those goods or services

(focus on control).

16 There is no material

impact anticipated from the introduction of this standard on the DCHL Group

activities.

OPTIONS

17 Not applicable.

NEXT STEPS

18 The timetable to be

confirmed following receipt of the Audit Plan letter from Audit NZ.

Signatories

|

Author:

|

Gavin Logie - Financial Controller

|

|

Authoriser:

|

Dave Tombs - General Manager Finance and Commercial

|

Attachments

There are no attachments for

this report.

|

SUMMARY OF CONSIDERATIONS

|

|

Fit with purpose of Local Government

This report provides a guideline of processes and

procedures for the Subcommittee.

|

|

Fit with strategic framework

|

|

Contributes

|

Detracts

|

Not applicable

|

|

Social Wellbeing Strategy

|

☐

|

☐

|

☒

|

|

Economic Development Strategy

|

☐

|

☐

|

☒

|

|

Environment Strategy

|

☐

|

☐

|

☒

|

|

Arts and Culture Strategy

|

☐

|

☐

|

☒

|

|

3 Waters Strategy

|

☐

|

☐

|

☒

|

|

Spatial Plan

|

☐

|

☐

|

☒

|

|

Integrated Transport Strategy

|

☐

|

☐

|

☒

|

|

Parks and Recreation Strategy

|

☐

|

☐

|

☒

|

|

Other strategic projects/policies/plans

|

☐

|

☐

|

☒

|

This report provides a guideline of processes and procedures

for the Subcommittee.

|

|

Māori Impact Statement

There are no known impacts for tangata whenua.

|

|

Sustainability

There are no implications for sustainability.

|

|

LTP/Annual Plan / Financial Strategy /Infrastructure

Strategy

This report provides a guideline of processes and

procedures for the Subcommittee.

|

|

Financial considerations

Not applicable – reporting only.

|

|

Significance

Not applicable – reporting only.

|

|

Engagement – external

The timetable has been prepared in conjunction with Audit

New Zealand.

|

|

Engagement - internal

Not applicable – reporting only.

|

|

Risks: Legal / Health and Safety etc.

This report provides a guideline of processes and

procedures for the Subcommittee.

|

|

Conflict of Interest

Not applicable – reporting only.

|

|

Community Boards

There are no known implications for Community Boards.

|

|

Audit and Risk Subcommittee

18 April 2019

|

|

Resolution to Exclude the

Public

That the Audit and Risk

Subcommittee:

Pursuant to the provisions of the

Local Government Official Information and Meetings Act 1987, exclude the public

from the following part of the proceedings of this meeting namely:

|

General subject of the matter to be considered

|

Reasons

for passing this resolution in relation to each matter

|

Ground(s) under

section 48(1) for the passing of this resolution

|

Reason for

Confidentiality

|

|

C1

Confirmation of the Confidential Minutes of Audit and Risk Subcommittee

meeting - 21 February 2019 - Public Excluded

|

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to prejudice the supply

of similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

S7(2)(b)(ii)

The

withholding of the information is necessary to protect information where the

making available of the information would be likely unreasonably to prejudice

the commercial position of the person who supplied or who is the subject of

the information.

S7(2)(h)

The

withholding of the information is necessary to enable the local authority to

carry out, without prejudice or disadvantage, commercial activities.

S7(2)(c)(ii)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to damage the public

interest.

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of natural

persons, including that of a deceased person.

S7(2)(f)(ii)

The

withholding of the information is necessary to maintain the effective conduct

of public affairs through the protection of such members, officers, employees

and persons from improper pressure or harassment.

S6(b)

The

making available of the information would be likely to endanger the safety of

a person.

|

.

|

|

|

C2

Report to the Council on the annual audit of Dunedin City Council for the

year ended 30 June 2018

|

S7(2)(b)(ii)

The

withholding of the information is necessary to protect information where the

making available of the information would be likely unreasonably to prejudice

the commercial position of the person who supplied or who is the subject of

the information.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C3

Dunedin City Holdings Ltd - Update on Audit and Risk Activity

|

S7(2)(b)(ii)

The

withholding of the information is necessary to protect information where the

making available of the information would be likely unreasonably to prejudice

the commercial position of the person who supplied or who is the subject of

the information.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C4

Audit and Risk Subcommittee Action List Report

|

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to prejudice the supply

of similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C5

Internal Audit WorkPlan Update - April 2019

|

S7(2)(b)(ii)

The

withholding of the information is necessary to protect information where the

making available of the information would be likely unreasonably to prejudice

the commercial position of the person who supplied or who is the subject of

the information.

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to prejudice the supply

of similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

S7(2)(h)

The

withholding of the information is necessary to enable the local authority to

carry out, without prejudice or disadvantage, commercial activities.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of information

for which good reason for withholding exists under section 7.

|

|

|

C6

Internal Audit - 2018 Data Analytics

|

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of natural

persons, including that of a deceased person.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

The report is

considered confidential because it refers to Council staff positions where

those staff may not have had the opportunity to respond or comment on the

report..

|

|

C7

Update on the DCC Internal Audit Actions Register - April 2019

|

S7(2)(c)(ii)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to damage the public

interest.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C8

Update on the DCC External Audit Actions Register - April 2019

|

S7(2)(c)(ii)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to damage the public

interest.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C9

ComplyWith Legal Compliance Survey (Jan - Dec 2018)

|

S7(2)(c)(ii)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to damage the public

interest.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C10

Strategic Risk Register - Update April 2019

|

S7(2)(c)(ii)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to damage the public

interest.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C11

Health and Safety Monthly Report for February 2019

|

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of natural

persons, including that of a deceased person.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

The information relates

to the actions of individual staff who could be identified. This would

breach their privacy and potentially prejudice any processes which may need

to be managed..

|

|

C12

Treasury Risk Management Compliance Report

|

S7(2)(h)

The

withholding of the information is necessary to enable the local authority to

carry out, without prejudice or disadvantage, commercial activities.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C13

Investigation Register

|

S6(b)

The

making available of the information would be likely to endanger the safety of

a person.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 6.

|

The matters detailed in

this report are subject to investigation and information should remain

confidential so as not to prejudice the investigation and any possible

outcomes of the investigation..

|

|

C14

Investigation Close Out Report - Awarding of Contracts

|

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of natural

persons, including that of a deceased person.

S7(2)(b)(ii)

The

withholding of the information is necessary to protect information where the

making available of the information would be likely unreasonably to prejudice

the commercial position of the person who supplied or who is the subject of

the information.

S7(2)(f)(ii)

The

withholding of the information is necessary to maintain the effective conduct

of public affairs through the protection of such members, officers, employees

and persons from improper pressure or harassment.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C15

Protected Disclosure Register

|

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of natural

persons, including that of a deceased person.

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to prejudice the supply

of similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

This resolution is made in

reliance on Section 48(1)(a) of the Local Government Official Information and

Meetings Act 1987, and the particular interest or interests protected by

Section 6 or Section 7 of that Act, or Section 6 or Section 7 or Section 9 of

the Official Information Act 1982, as the case may require, which would be

prejudiced by the holding of the whole or the relevant part of the proceedings

of the meeting in public are as shown above after each item.

That Julian Tan (Audit NZ) be permitted to remain at

the meeting, after the public has been excluded, because of his knowledge of

Items C2 and C3. This knowledge, which would be of assistance in relation

to the matters discussed, was relevant because they would be reporting on the

item under consideration.