Notice of Meeting:

I hereby give notice that an ordinary meeting of the Audit

and Risk Subcommittee will be held on:

Date: Thursday

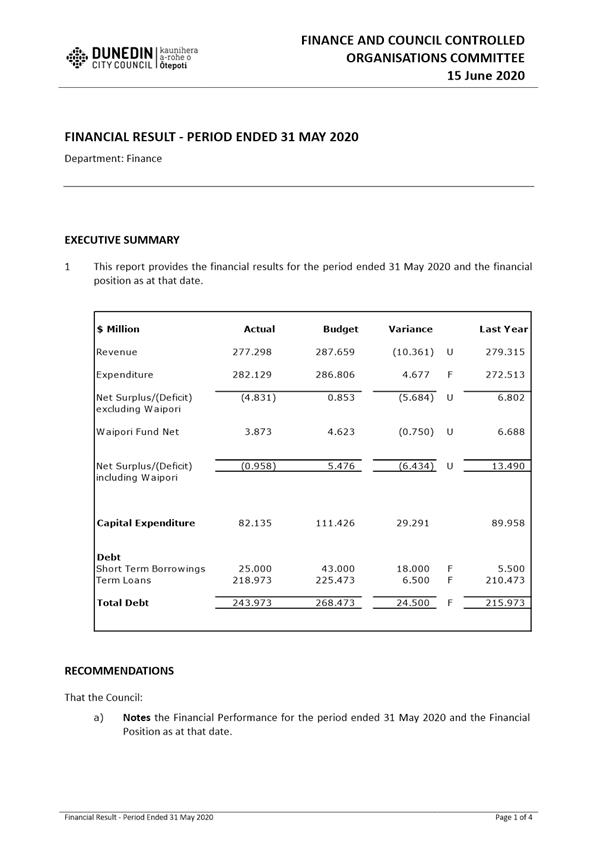

2 July 2020

Time: 2.00

pm

Venue: Otaru

Room, Civic Centre, The Octagon, Dunedin

Sue Bidrose

Audit and Risk Subcommittee

PUBLIC AGENDA

|

Chairperson

|

Susie Johnstone

|

|

|

Deputy Chairperson

|

Janet Copeland

|

|

|

Members

|

Cr Christine Garey

|

Cr Doug Hall

|

|

|

Mayor Aaron Hawkins

|

Cr Mike Lord

|

Senior Officer Dave

Tombs, General Manager Finance and Commercial

Governance Support Officer Wendy

Collard

Wendy Collard

Governance Support Officer

Telephone: 03 477 4000

Wendy.Collard@dcc.govt.nz

www.dunedin.govt.nz

Note: Reports

and recommendations contained in this agenda are not to be considered as

Council policy until adopted.

|

|

Audit and Risk Subcommittee

2 July 2020

|

ITEM TABLE OF CONTENTS PAGE

1 Apologies 4

2 Confirmation

of Agenda 4

3 Declaration

of Interest 5

4 Confirmation

of Minutes 13

4.1 Audit and Risk

Subcommittee meeting - 20 May 2020 13

Part

A Reports (Committee has power to decide these matters)

5 Audit

and Risk Subcommittee Work Plan 2020 22

6 Financial

Results 27

7 Annual

Report Timetable for Year Ended 30 June 2020 39

Resolution to Exclude the Public 65

|

|

Audit and Risk Subcommittee

2 July 2020

|

1 Apologies

An apology has been received from

Cr Mike Lord.

That the Subcommittee:

Accepts the apology from Cr

Mike Lord.

2 Confirmation

of agenda

Note:

Any additions must be approved by resolution with an explanation as to why they

cannot be delayed until a future meeting.

|

|

Audit and Risk Subcommittee

2 July 2020

|

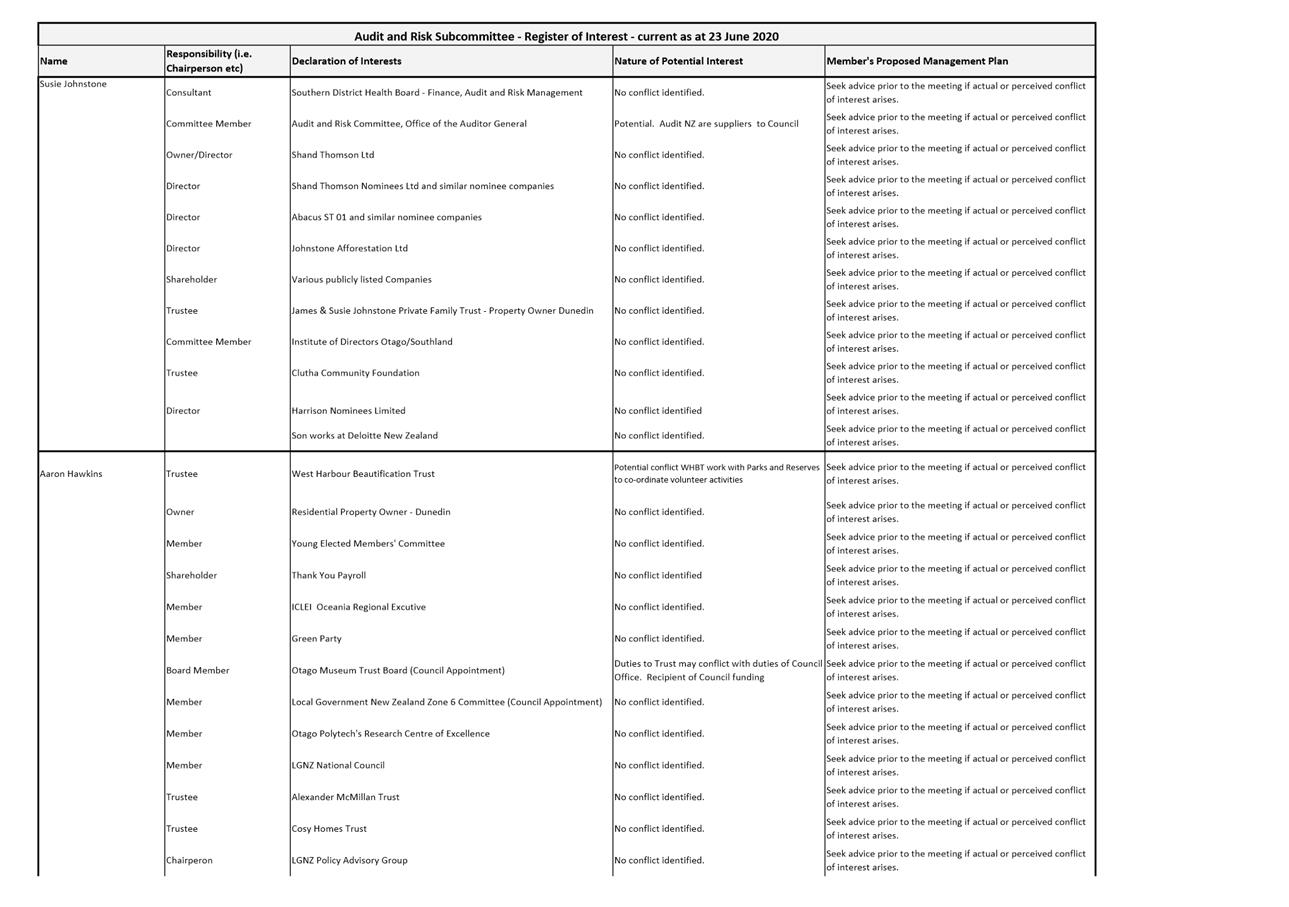

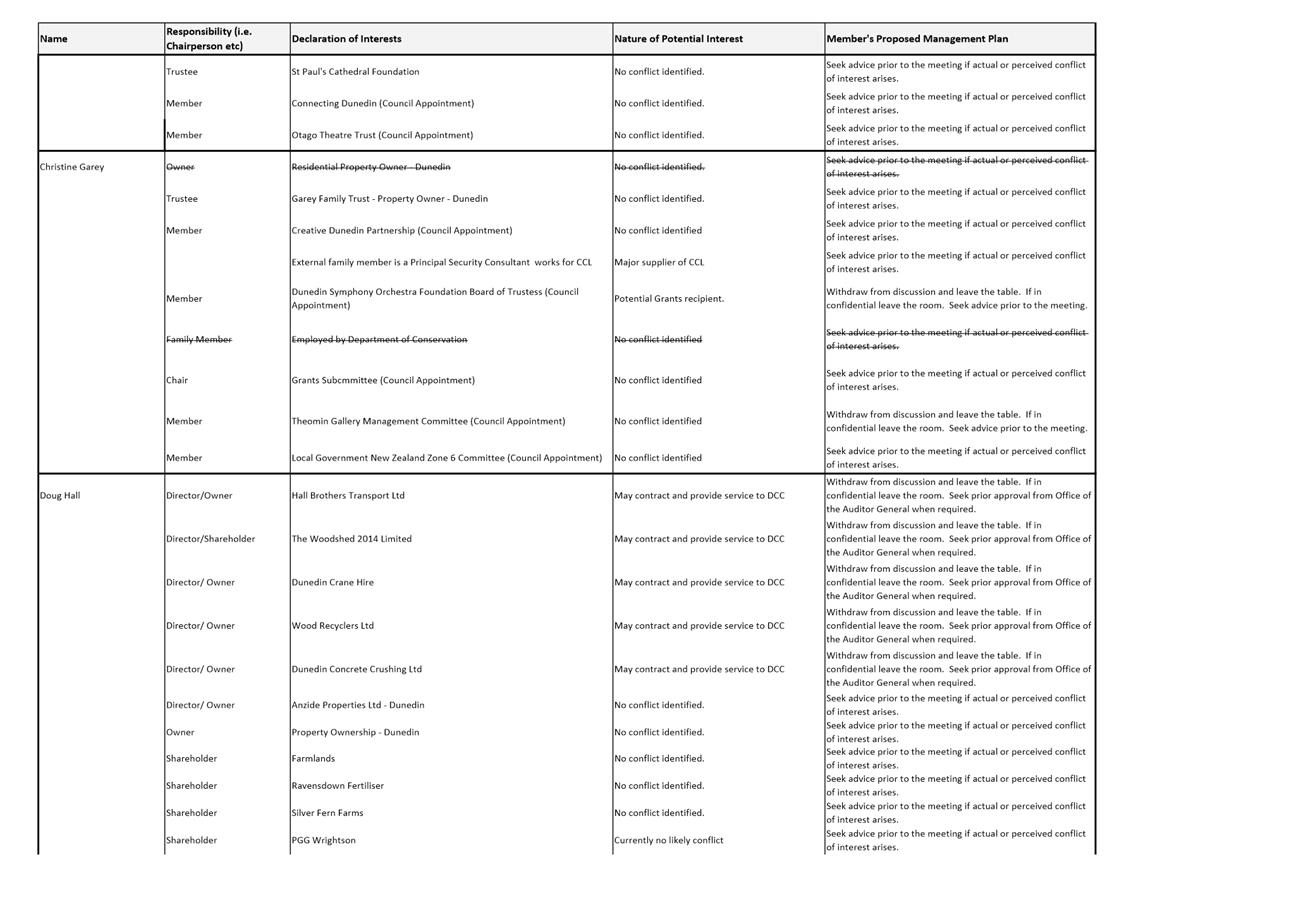

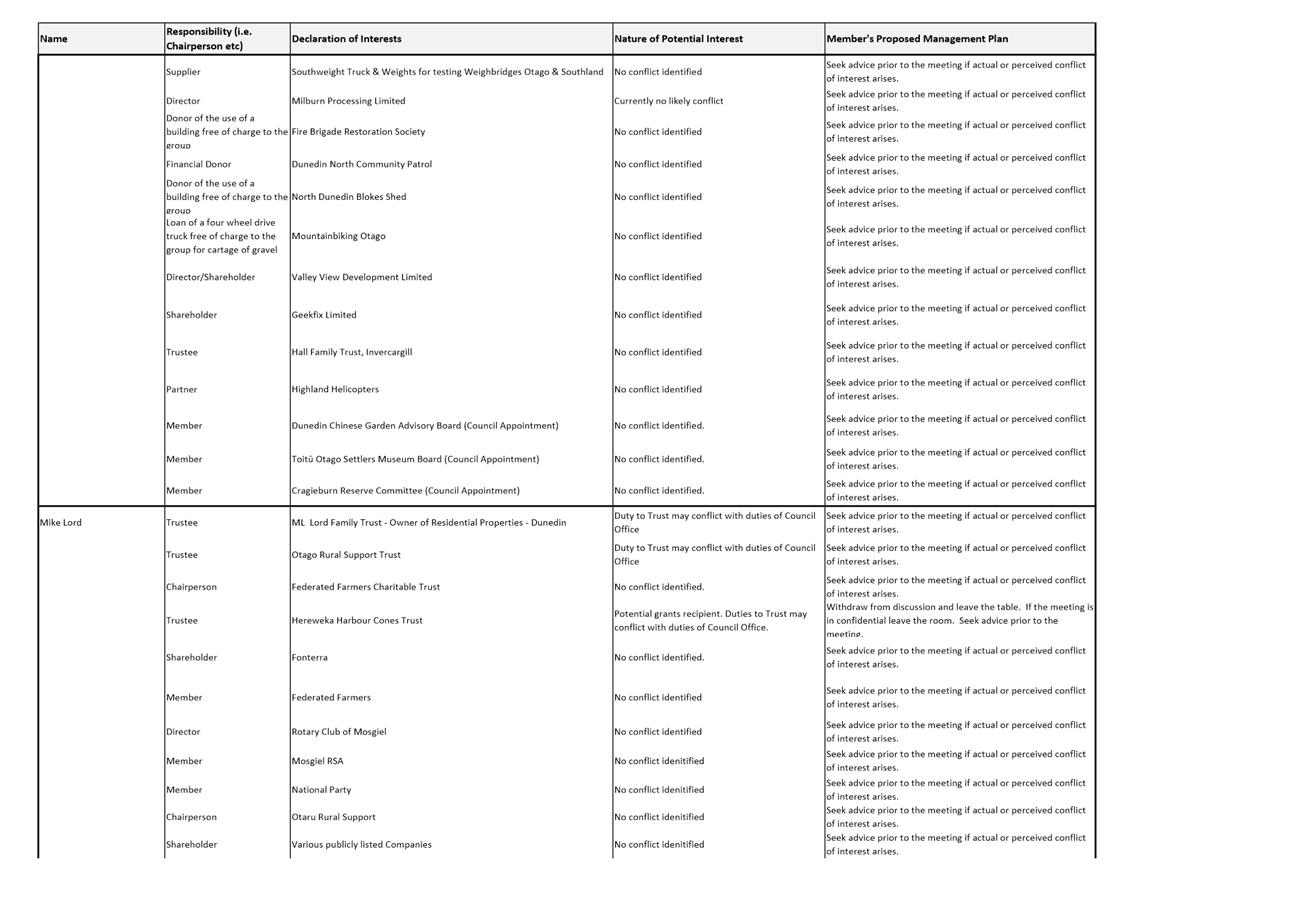

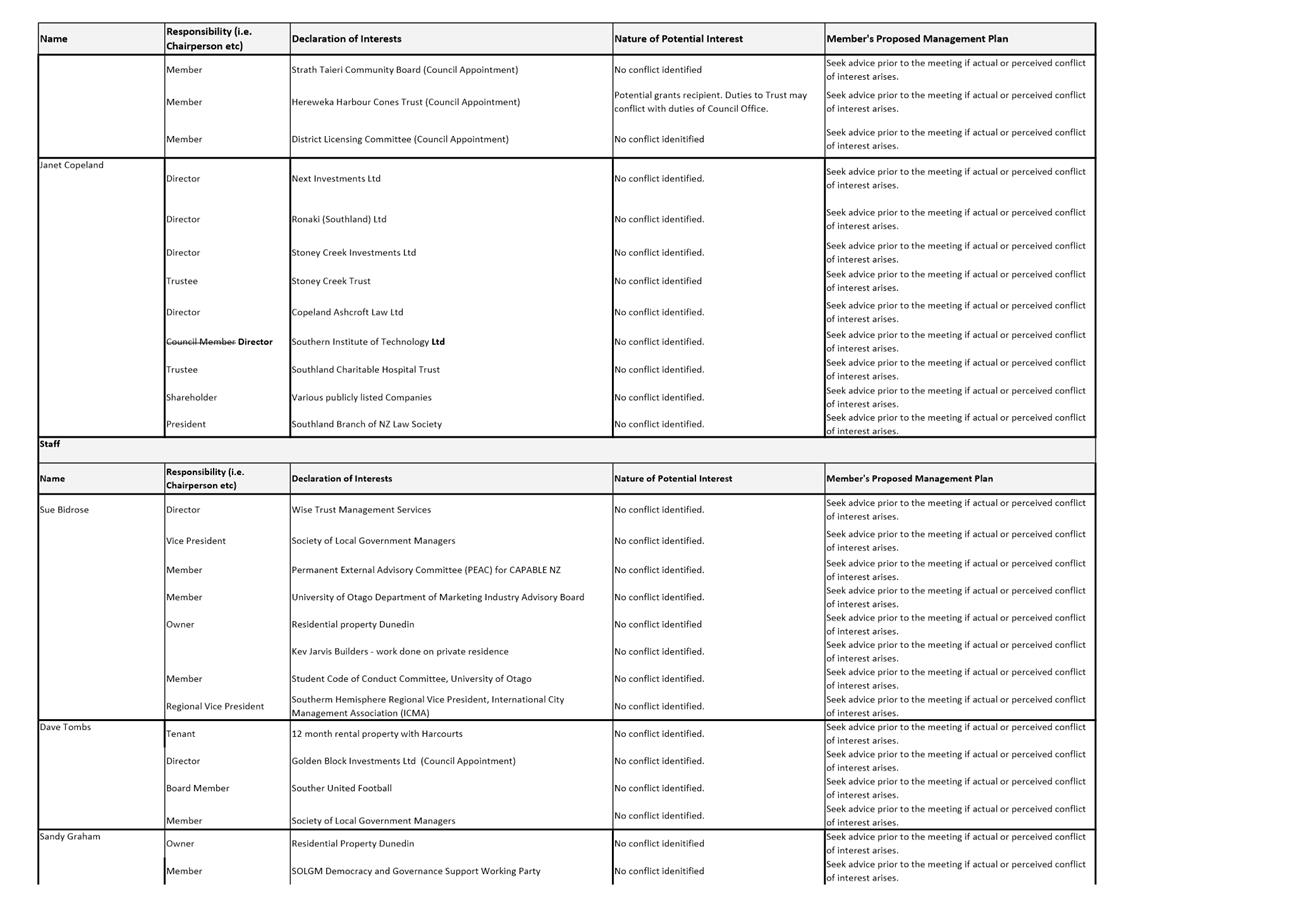

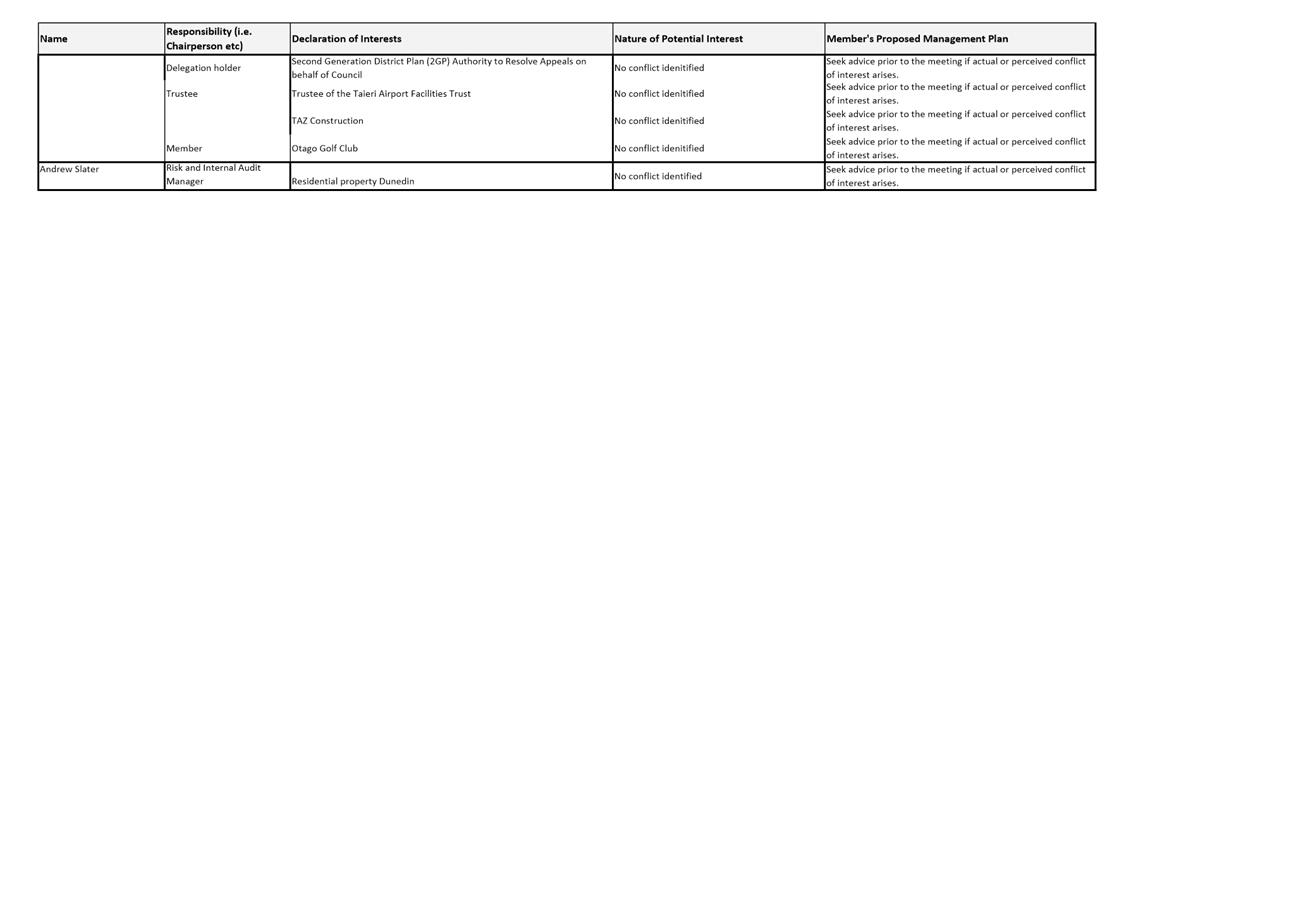

Declaration of Interest

EXECUTIVE SUMMARY

1.

Members are reminded of the need to stand aside from decision-making

when a conflict arises between their role as an elected representative and

independent members and any private or other external interest they might have.

2. Elected

members and independent members are reminded to update their

register of interests as soon as practicable, including amending the register

at this meeting if necessary.

|

RECOMMENDATIONS

That the Subcommittee:

a) Notes/Amends

if necessary the Elected or Independent Members' Interest Register attached

as Attachment A; and

b) Confirms/Amends the proposed management plan for Elected or Independent Members'

Interests.

|

Attachments

|

|

Title

|

Page

|

|

⇩a

|

Members' Register of

Interests

|

7

|

|

|

Audit and Risk Subcommittee

2 July 2020

|

|

|

Audit and Risk Subcommittee

2 July 2020

|

Confirmation

of Minutes

Audit and Risk Subcommittee meeting - 20 May 2020

|

RECOMMENDATIONS

That the Subcommittee:

Confirms the public part of the minutes of

the Audit and Risk Subcommittee meeting held on 20 May 2020 as a correct

record.

|

Attachments

|

|

Title

|

Page

|

|

A⇩

|

Minutes of Audit and

Risk Subcommittee meeting held on 20 May 2020

|

14

|

|

|

Audit and Risk Subcommittee

2 July 2020

|

Audit and Risk Subcommittee

MINUTES

Minutes of an ordinary

meeting of the Audit and Risk Subcommittee held in the Via Audio Visual Link on

Wednesday 20 May 2020, commencing at 2.04 pm

PRESENT

|

Chairperson

|

Susie Johnstone

|

|

|

Deputy Chairperson

|

Janet Copeland

|

|

|

Members

|

Cr Christine Garey

|

Mayor Aaron Hawkins

|

|

|

Cr Mike Lord

|

|

|

IN ATTENDANCE

|

Sue Bidrose (Chief Executive

Officer), Dave Tombs (General Manager, Finance and Commercial) and Andrew

Slater (Risk and Internal Audit Manager)

|

Governance Support Officer Wendy

Collard

|

1 Apologies

|

|

There were no apologies.

|

|

2 Confirmation

of agenda

|

|

|

Moved (Susie Johnstone/Cr Mike Lord):

That the Subcommittee:

Confirms the agenda

without addition or alteration

Motion

carried (AR/2020/015)

|

3 Declarations

of interest

Members were

reminded of the need to stand aside from decision-making when a conflict arose

between their role as an elected representative and any private or other

external interest they might have.

Mayor Aaron Hawkins and Ms

Copeland provided an update to their register of interests.

|

|

Moved (Susie Johnstone/Mayor Aaron Hawkins):

That the Subcommittee:

a) Amends the

Elected or Independent Members' Interest Register; and

b) Confirms

the proposed management plan for Elected or Independent Members' Interests.

Motion

carried (AR/2020/016)

Janet Copeland entered

the meeting at 2.10 pm

|

4 Confirmation

of Minutes

|

4.1 Audit

and Risk Subcommittee meeting meeting - 13 February 2020

|

|

|

Moved (Cr Mike Lord/Cr Christine Garey):

That the Subcommittee:

Confirms the public part of the minutes of the Audit

and Risk Subcommittee meeting held on 13 February 2020 as a correct

record.

Motion

carried (AR/2020/017)

|

Part

A Reports

|

5 Audit

and Risk Subcommittee Work Plan 2020

|

|

|

A report from Civic provided

the updated Audit and Risk Subcommittee Work Plan 2020 and the Governance and

Financial Policies.

|

|

|

Moved (Mayor Aaron Hawkins/Janet Copeland):

That the Subcommittee:

a) Notes the

Audit and Risk Subcommittee Work Plan.

Motion

carried (AR/2020/018)

|

|

Resolution

to exclude the public

|

|

Moved (Janet Copeland/Cr Mike Lord):

That the Subcommittee:

Pursuant

to the provisions of the Local Government Official Information and Meetings

Act 1987, exclude the public from the following part of the proceedings of this

meeting namely:

|

General

subject of the matter to be considered

|

Reasons

for passing this resolution in relation to each matter

|

Ground(s) under

section 48(1) for the passing of this resolution

|

Reason for

Confidentiality

|

|

C1

Audit and Risk Subcommittee meeting - 13 February 2020 - Public Excluded

|

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or

could be compelled to provide under the authority of any enactment, where

the making available of the information would be likely to prejudice the

supply of similar information or information from the same source and it is

in the public interest that such information should continue to be supplied.

S7(2)(b)(i)

The

withholding of the information is necessary to protect information where

the making available of the information would disclose a trade secret.

S7(2)(h)

The

withholding of the information is necessary to enable the local authority

to carry out, without prejudice or disadvantage, commercial activities.

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of

natural persons, including that of a deceased person.

S7(2)(b)(ii)

The

withholding of the information is necessary to protect information where

the making available of the information would be likely unreasonably to

prejudice the commercial position of the person who supplied or who is the

subject of the information.

S6(b)

The

making available of the information would be likely to endanger the safety

of a person.

|

.

|

|

|

C2

Audit and Risk Subcommittee Action List Report

|

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or

could be compelled to provide under the authority of any enactment, where

the making available of the information would be likely to prejudice the

supply of similar information or information from the same source and it is

in the public interest that such information should continue to be

supplied.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C3

DCC Policy Update Report

|

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or

could be compelled to provide under the authority of any enactment, where

the making available of the information would be likely to prejudice the

supply of similar information or information from the same source and it is

in the public interest that such information should continue to be

supplied.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C4

Internal Audit Workplan Update

|

S7(2)(b)(i)

The

withholding of the information is necessary to protect information where

the making available of the information would disclose a trade secret.

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or

could be compelled to provide under the authority of any enactment, where

the making available of the information would be likely to prejudice the

supply of similar information or information from the same source and it is

in the public interest that such information should continue to be

supplied.

S7(2)(h)

The

withholding of the information is necessary to enable the local authority

to carry out, without prejudice or disadvantage, commercial activities.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C5

Annual Plan and 10 year plan Process Update

|

S7(2)(g)

The

withholding of the information is necessary to maintain legal professional

privilege.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C6

Health and Safety Board Monthly Report for February and March 2020

|

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of

natural persons, including that of a deceased person.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

The information

relates to the actions of individual staff who could be identified.

This would breach their privacy and potentially prejudice any processes

which may need to be managed.

|

|

C7

Treasury Risk Management Compliance Report

|

S7(2)(h)

The

withholding of the information is necessary to enable the local authority

to carry out, without prejudice or disadvantage, commercial activities.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C8

Dunedin City Holdings Ltd - Update on Audit and Risk Activity

|

S7(2)(b)(ii)

The

withholding of the information is necessary to protect information where

the making available of the information would be likely unreasonably to

prejudice the commercial position of the person who supplied or who is the

subject of the information.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C9

Protected Disclosure Register

|

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of

natural persons, including that of a deceased person.

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or

could be compelled to provide under the authority of any enactment, where

the making available of the information would be likely to prejudice the

supply of similar information or information from the same source and it is

in the public interest that such information should continue to be

supplied.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C10

Investigation Register

|

S6(b)

The

making available of the information would be likely to endanger the safety

of a person.

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of

natural persons, including that of a deceased person.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 6

and 7.

|

The matters detailed

i this report are subject to investigation and information should remain

confidential so not to prejudice the investigation and any possible

outcomes of the investigation.

|

This resolution is made in

reliance on Section 48(1)(a) of the Local Government Official Information and

Meetings Act 1987, and the particular interest or interests protected by

Section 6 or Section 7 of that Act, or Section 6 or Section 7 or Section 9 of

the Official Information Act 1982, as the case may require, which would be

prejudiced by the holding of the whole or the relevant part of the

proceedings of the meeting in public are as shown above after each item.

Motion

carried (AR/2020/019)

|

The meeting entered into non-public at 2.12 pm and concluded

at 4.53 pm.

..............................................

CHAIRPERSON

|

|

Audit and Risk Subcommittee

2 July 2020

|

Part

A Reports

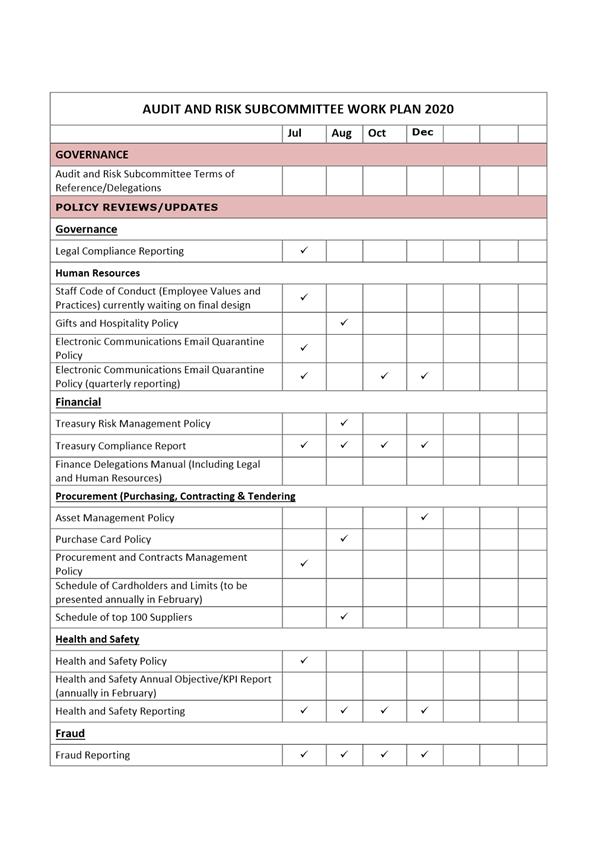

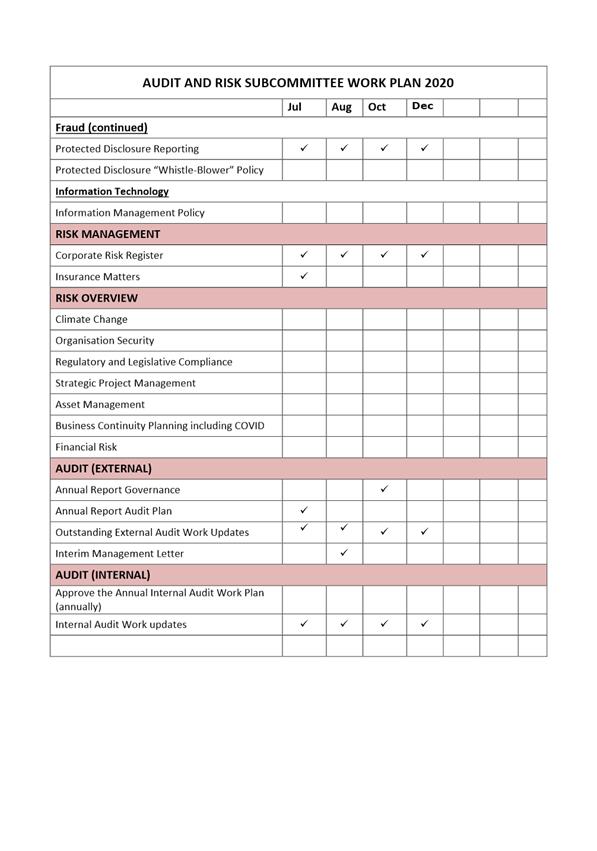

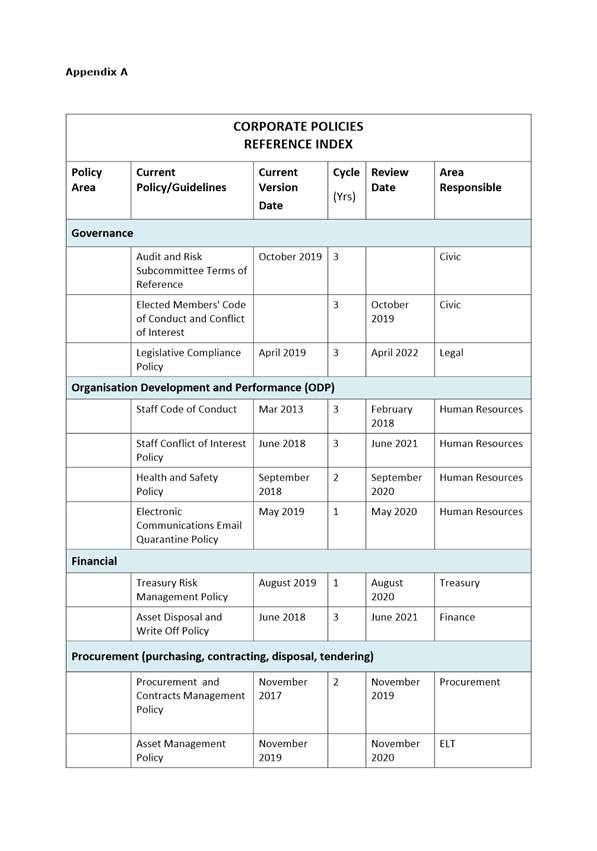

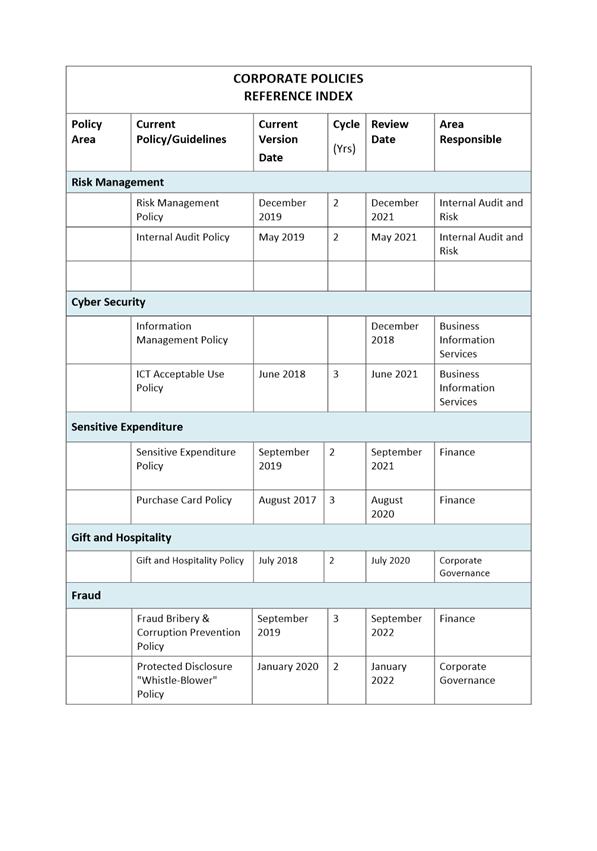

Audit and Risk Subcommittee Work Plan 2020

Department: Civic

EXECUTIVE SUMMARY

1 This

report provides a copy of the updated Audit and Risk Subcommittee Work Plan

2020. Please note that the Governance and Financial Policies are included in an

appendix to the Work Plan.

2 Additional

work streams have been added to the workplan for the Subcommittee’s

consideration.

3 As

this is an administrative report only, the Summary of Considerations is not

required.

|

RECOMMENDATIONS

That the Subcommittee:

a) Notes the

Audit and Risk Subcommittee Work Plan.

|

Signatories

|

Author:

|

Wendy Collard - Governance Support Officer

|

|

Authoriser:

|

Clare Sullivan - Team Leader Civic

|

Attachments

|

|

Title

|

Page

|

|

⇩a

|

Workplan 2020

|

23

|

|

|

Audit and Risk Subcommittee

2 July 2020

|

|

|

Audit and Risk Subcommittee

2 July 2020

|

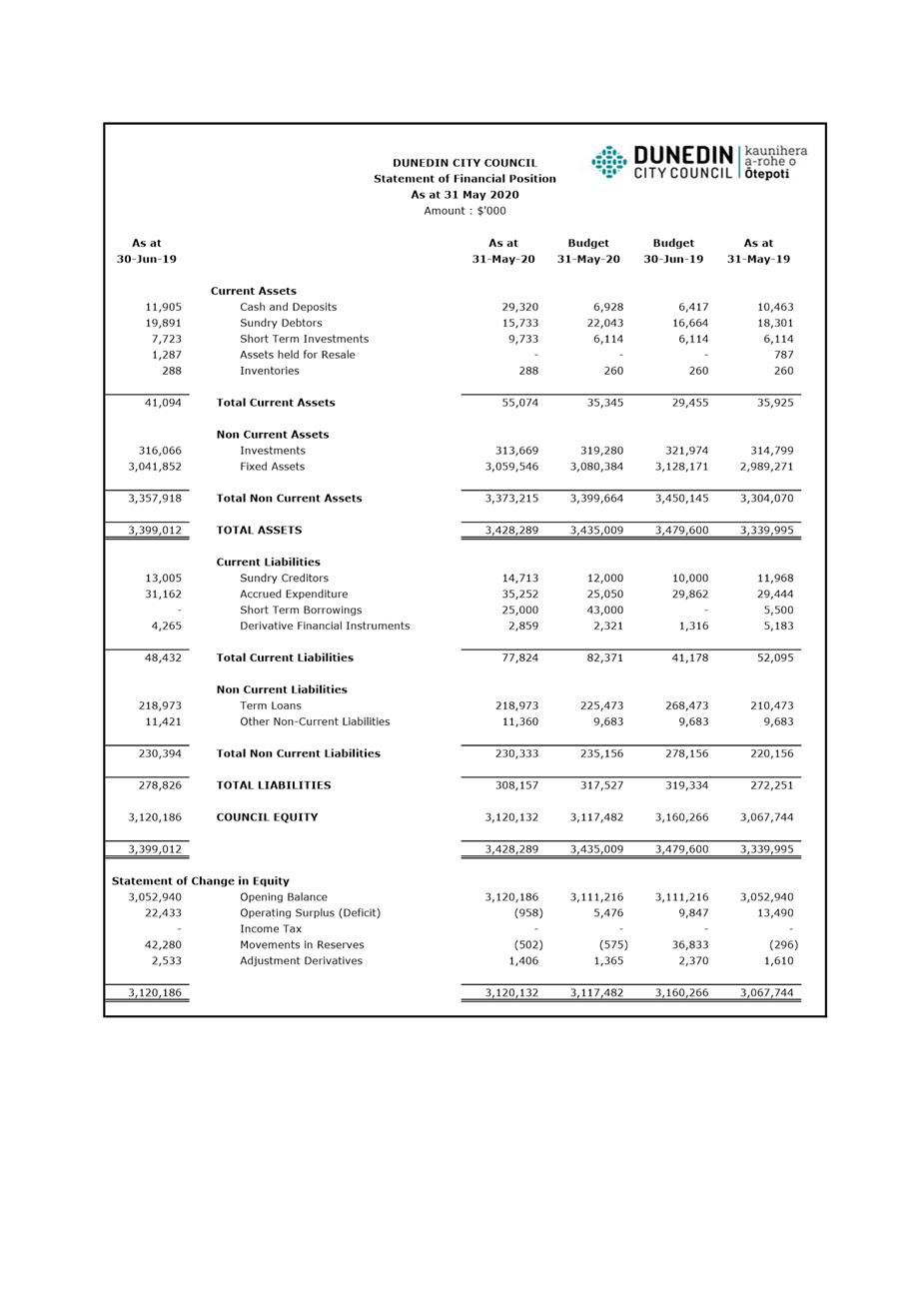

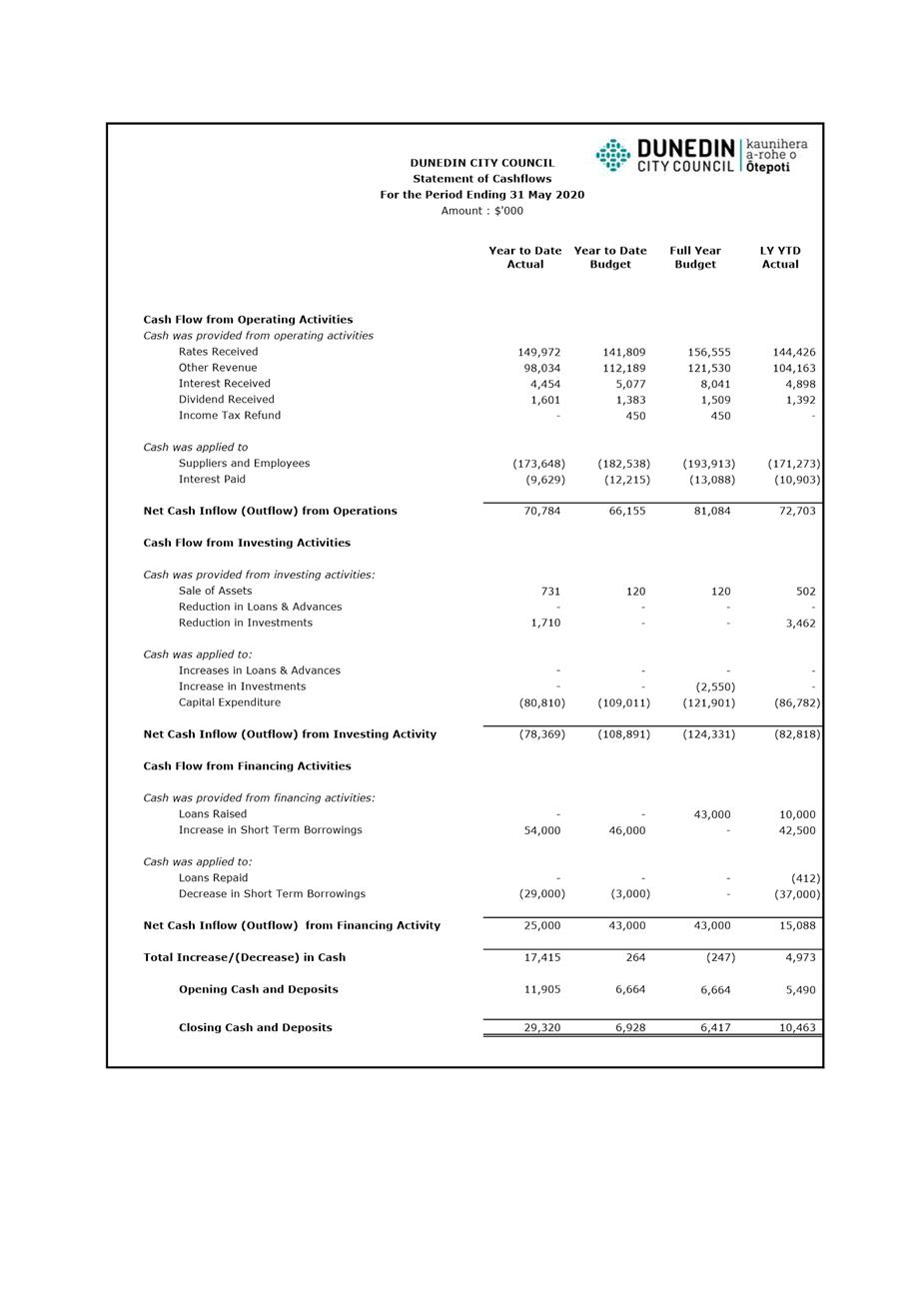

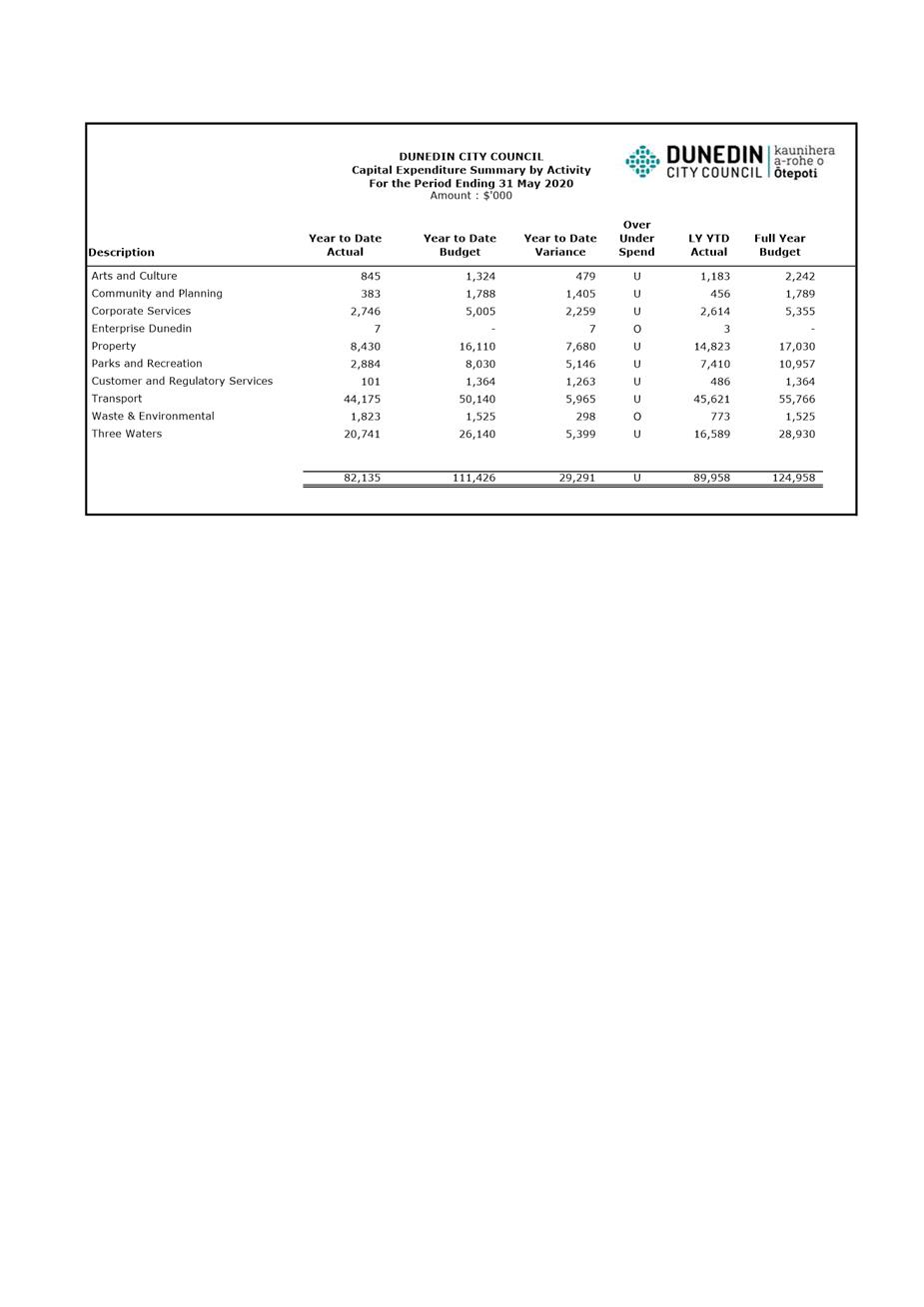

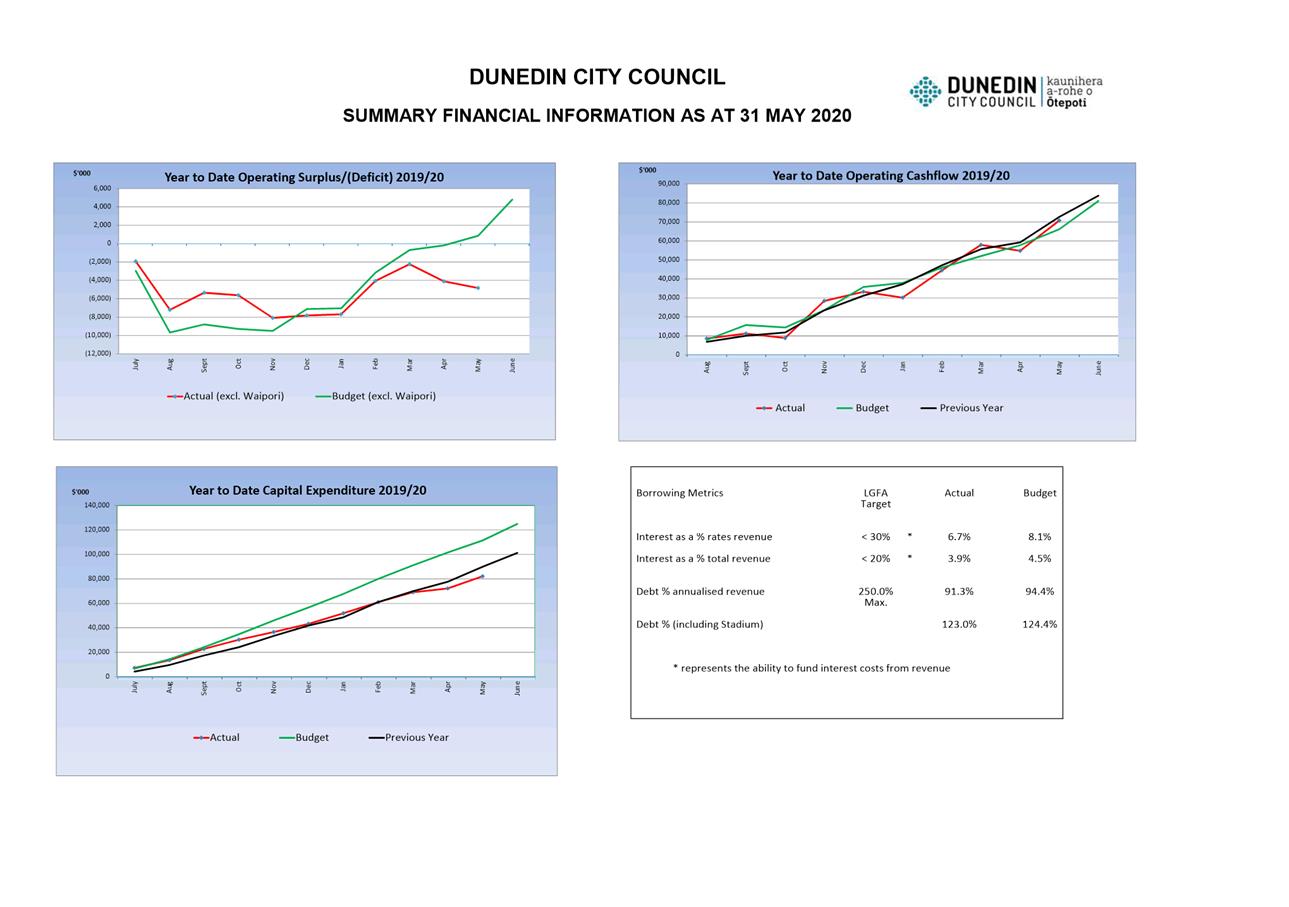

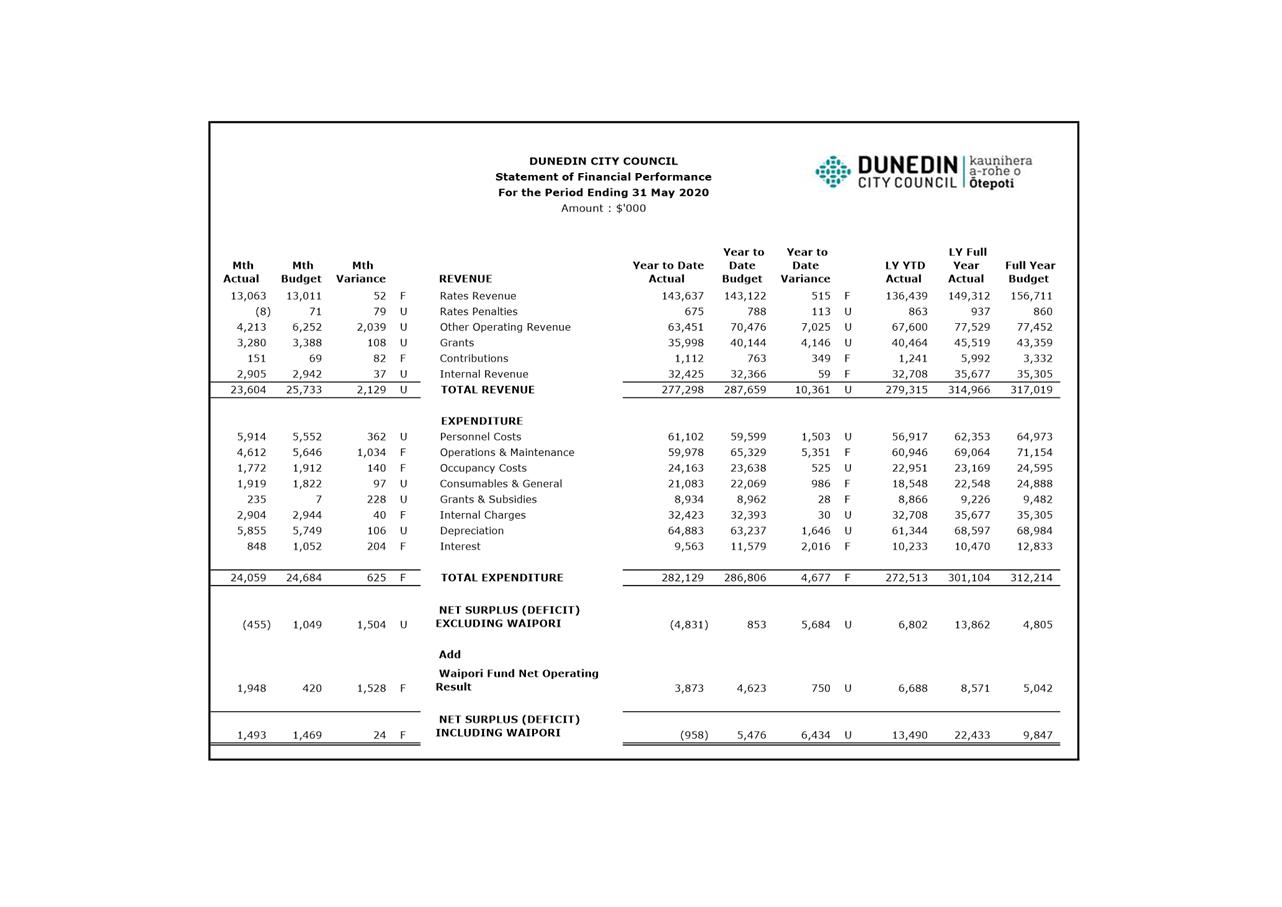

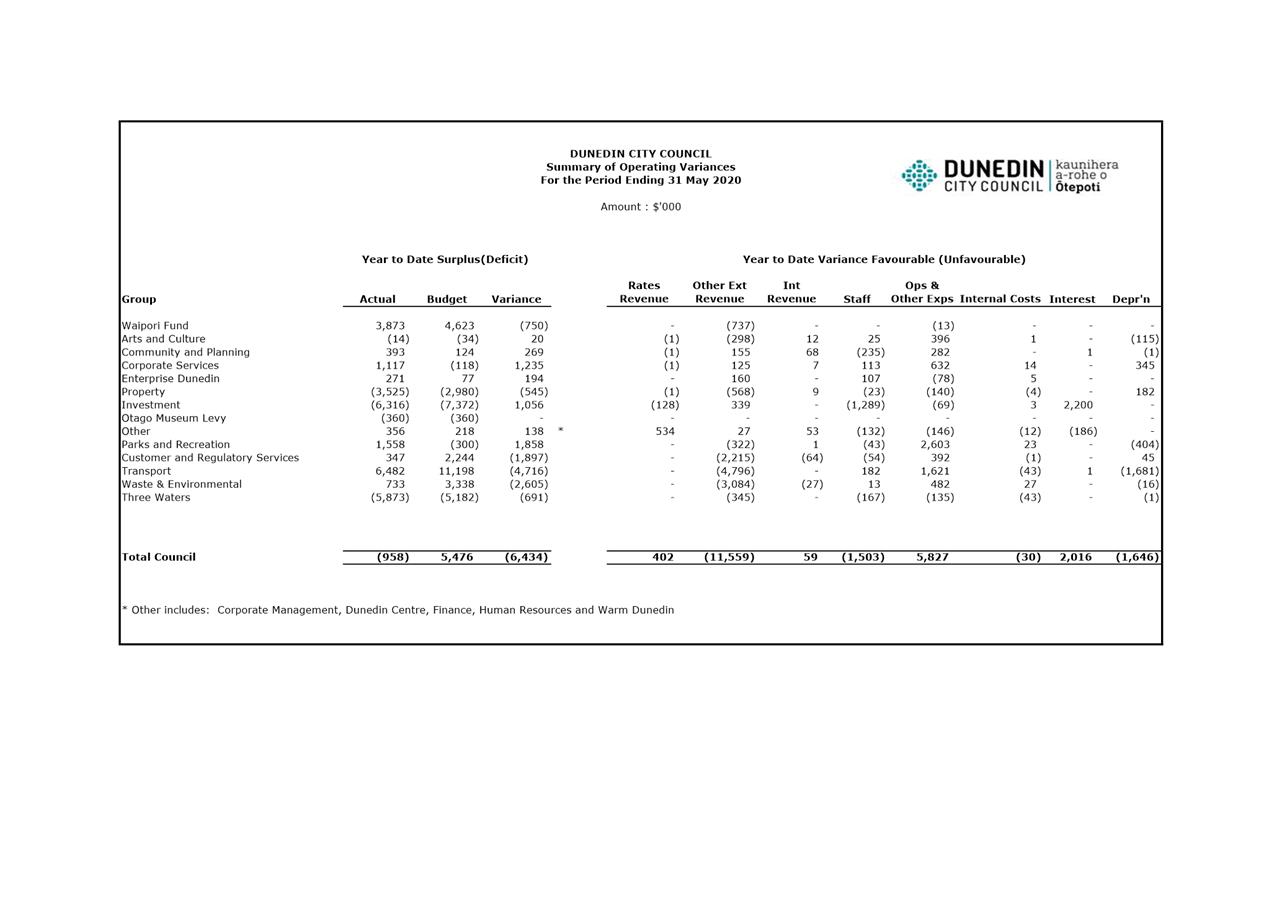

Financial Results

Department: Civic

EXECUTIVE SUMMARY

1 This

report provides a copy of the Financial Results for the period ending 31 May 2020

report which was presented to the Finance and Council Controlled Organisations

Committee meeting held on 15 June 2020.

|

RECOMMENDATIONS

That the Subcommittee:

a) Notes the

Financial Results for the period ending 31 May 2020 report.

|

Signatories

|

Author:

|

Wendy Collard - Governance Support Officer

|

|

Authoriser:

|

Clare Sullivan - Team Leader Civic

|

Attachments

|

|

Title

|

Page

|

|

⇩a

|

Financial Results for

period ending 31 May 2020

|

30

|

|

SUMMARY OF CONSIDERATIONS

|

|

Fit with purpose of Local Government

This decision

enables democratic local decision making and action by, and on behalf of

communities.

|

|

Fit with strategic framework

|

|

Contributes

|

Detracts

|

Not applicable

|

|

Social Wellbeing Strategy

|

☐

|

☐

|

☒

|

|

Economic Development

Strategy

|

☐

|

☐

|

☒

|

|

Environment Strategy

|

☐

|

☐

|

☒

|

|

Arts and Culture Strategy

|

☐

|

☐

|

☒

|

|

3 Waters Strategy

|

☐

|

☐

|

☒

|

|

Spatial Plan

|

☐

|

☐

|

☒

|

|

Integrated Transport

Strategy

|

☐

|

☐

|

☒

|

|

Parks and Recreation

Strategy

|

☐

|

☐

|

☒

|

|

Other strategic

projects/policies/plans

|

☐

|

☐

|

☒

|

This report has no direct

contribution to the Strategic Framework, although the financial expenditure

reported in this report has contributed to all of the strategies.

|

|

Māori Impact Statement

There are no known impacts

for tangata whenua.

|

|

Sustainability

There are no known

implications for sustainability.

|

|

LTP/Annual Plan / Financial Strategy /Infrastructure

Strategy

This report fulfils the

internal financial reporting requirements for Council.

|

|

Financial considerations

Not applicable –

reporting only.

|

|

Significance

Not applicable –

reporting only.

|

|

Engagement – external

There has been no external

engagement.

|

|

Engagement - internal

The report is prepared as a

summary for the individual department financial reports.

|

|

Risks: Legal / Health and Safety etc.

There are no known risks.

|

|

Conflict of Interest

There are no known conflicts

of interest.

|

|

Community Boards

There are no known

implications for Community Boards.

|

|

|

Audit and Risk Subcommittee

2 July 2020

|

|

|

Audit and Risk Subcommittee

2 July 2020

|

Annual Report

Timetable for Year Ended 30 June 2020

Department:

Finance

EXECUTIVE SUMMARY

1 This report provides an

update with regards the timetable related to the preparation and approval of

the Dunedin City Council Annual Report for the year ended 30 June 2020.

2 It also considers new

accounting standards and any other matters that may impact financial reporting

for the year ended 30 June 2020.

|

RECOMMENDATIONS

That

the Subcommittee:

a) Notes the

report as presented.

|

BACKGROUND

3 Following a request from

the Audit and Risk Subcommittee, staff have prepared a high level timetable

associated with the annual report process for the year ended 30 June 2020.

DISCUSSION

4 The following timetable

relates to the preparation and approval of the annual report for the year ended

30 June 2020.

5 The dates are based on

the Audit Plan letter provided by Audit New Zealand, and the relevant meetings

dates for Council and the Audit and Risk Sub-Committee.

6 This report also includes

an update on matters that may impact financial reporting for the year ended 30

June 2020.

|

Date

|

|

Task

|

Completed

|

|

|

|

|

|

|

June 2020

|

|

Audit

Plan Letter - Audit NZ

|

June

2020

|

|

|

|

|

|

|

21-Aug-20

|

|

Draft

parent financial statement available for audit

|

|

|

|

|

|

|

|

24-Aug-20

|

|

Parent

audit commences

|

|

|

|

|

|

|

|

4-Sep-20

|

|

Draft

DCC Group financial statements available for audit

|

|

|

|

|

|

|

|

21-Sep-20

|

|

Final

financial statements incorporating agreed audit

|

|

|

|

|

amendments

|

|

|

|

|

|

|

|

23-Sep-20

|

|

Annual

report available including Mayor’s and CEO reviews

|

|

|

|

|

|

|

|

24-Sep-20

|

|

DCHL

Annual Report presented to Board for approval.

|

|

|

|

|

|

|

|

28-Sep-20

|

|

Verbal

audit clearance from Audit NZ

|

|

|

|

|

|

|

|

15-Oct-20

|

*

|

Annual

report presented to Audit and Risk for confirmation and

|

|

|

|

|

endorsement

|

|

|

|

|

|

|

|

27-Oct-20

|

|

Annual

Report presented to Council for approval.

|

|

|

|

|

Letters

of Representation signed (Governance and Management)

|

|

|

|

|

|

|

|

27-Oct-20

|

|

Audit

Opinion Issued

|

|

|

|

|

|

|

|

19-Oct-20

|

|

Final

detailed draft report issued by Audit NZ

|

|

|

|

|

|

|

|

28-Oct-20

|

|

Summary

annual report available for audit

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

*

Date to be confirmed

|

|

IMPLICATIONS OF COVID19

7 The preparation timeline

for the DCC Group annual report should not be impacted by the current alert

level for Covid19. If the alert level were to increase beyond level one,

then the timeline may come under pressure.

8 Audit New Zealand have

produced reporting bulletins on matters likely to be impacted by the current

environment. In particular, reference has been made to valuation of property.

For the 2019/20 financial year the DCC will be revaluing the following items of

Property, Plant & Equipment:

· Roading Assets 30 June

2020 – fair value based on depreciable replacement cost

· Three Waters 1 July

2019 – fair value based on depreciable replacement cost

· Restricted Assets

(Parks & Recreation) 30 June 2020 – fair value

· Investment Property 30

June 2020 – fair market value

9 The valuers engaged to

complete these valuations will be well versed on the implications associated

with the current environment – in particular the likely impact on the

value of the DCC Investment Property portfolio.

10 In terms of the balance of land and

buildings not due for revaluation until year ended 30 June 2021, we will

provide an internal assessment, supported by guidance from our valuers where

appropriate, on whether the carrying values need to be amended.

11 In terms of the DCC consolidated

accounts, the main matter for consideration will be the valuation of the

Dunedin Railway assets. The DCHL Group Accountant will work with Audit

New Zealand on this matter.

NEW ACCOUNTING STANDARDS

NZ IRFS 16 Leases

12 Effective date 30 June 2020 for

profit entities.

13 Staff will liaise with Group

Accountant around any material impact of the DCC consolidated accounts.

PBE IPSAS 35 Consolidated Financial

Statements

14 Effective date 30 June 2020.

15 The standard provides an updated

definition of control of entities owned by the DCC and when full consolidation

is required.

16 An assessment will be performed on

whether previously separated entities need to be consolidated.

OPTIONS

17 Not applicable.

NEXT STEPS

18 The timetable will continue to be

updated as tasks are completed.

Signatories

|

Author:

|

Gavin Logie - Financial Controller

|

|

Authoriser:

|

Dave Tombs - General Manager Finance and Commercial

|

Attachments

|

|

Title

|

Page

|

|

⇩a

|

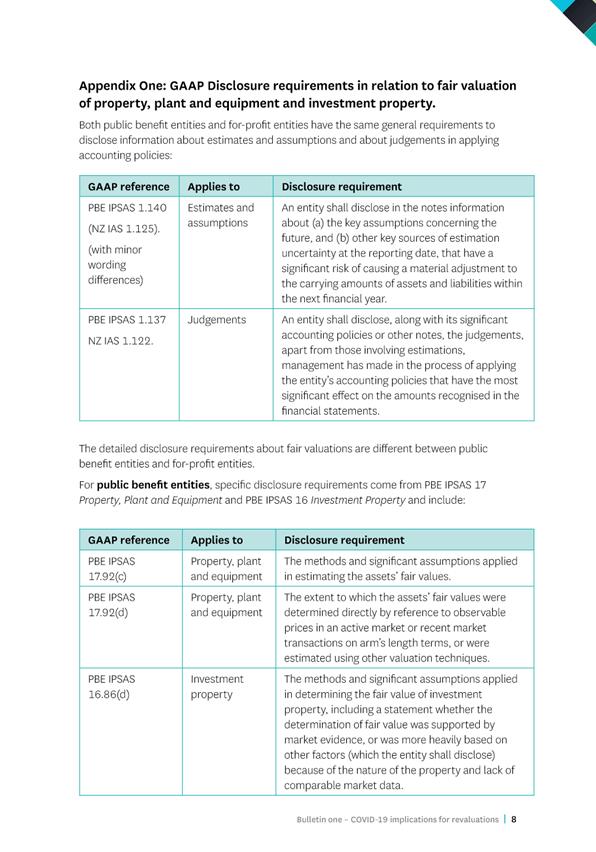

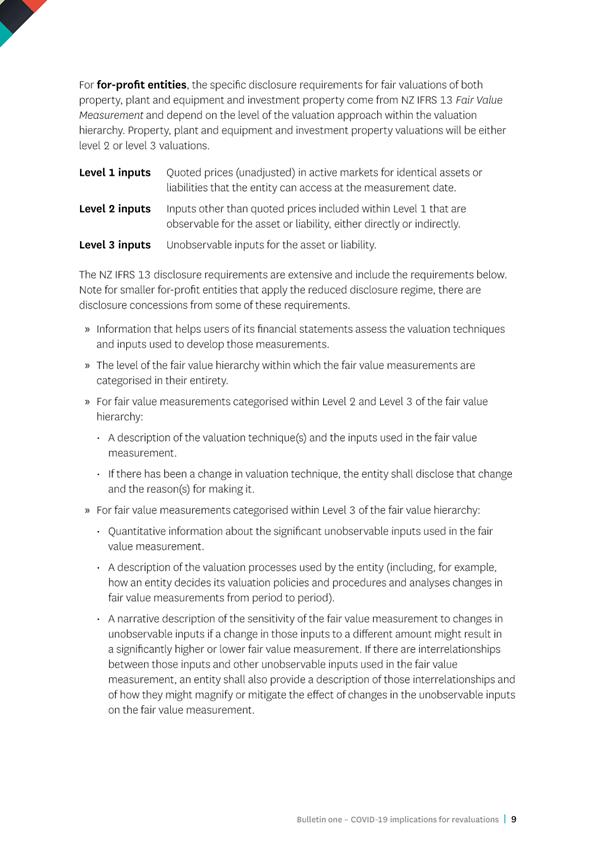

Audit NZ -Bulletin One.

Implications of COVID-19 for revaluations of property, plant and equipment'

and investment property

|

45

|

|

⇩b

|

Audit NZ Bulletin Two -

Implications of COVID-19 for service performance reporting.

|

55

|

|

SUMMARY OF CONSIDERATIONS

|

|

Fit with purpose of

Local Government

This

report provides a guideline of processes and procedures for the Subcommittee.

|

|

Fit with strategic

framework

|

|

Contributes

|

Detracts

|

Not

applicable

|

|

Social

Wellbeing Strategy

|

☐

|

☐

|

☒

|

|

Economic

Development Strategy

|

☐

|

☐

|

☒

|

|

Environment

Strategy

|

☐

|

☐

|

☒

|

|

Arts

and Culture Strategy

|

☐

|

☐

|

☒

|

|

3

Waters Strategy

|

☐

|

☐

|

☒

|

|

Spatial

Plan

|

☐

|

☐

|

☒

|

|

Integrated

Transport Strategy

|

☐

|

☐

|

☒

|

|

Parks

and Recreation Strategy

|

☐

|

☐

|

☒

|

|

Other

strategic projects/policies/plans

|

☐

|

☐

|

☒

|

This

report provides a guideline of processes and procedures for the Subcommittee.

|

|

Māori Impact

Statement

There

are no known impacts for tangata whenua.

|

|

Sustainability

There

are no implications for sustainability.

|

|

LTP/Annual Plan /

Financial Strategy /Infrastructure Strategy

This

report provides a guideline of processes and procedures for the Subcommittee.

|

|

Financial

considerations

Not

applicable – reporting only.

|

|

Significance

Not

applicable – reporting only.

|

|

Engagement –

external

The

timetable has been prepared in conjunction with Audit New Zealand.

|

|

Engagement -

internal

Not

applicable – reporting only.

|

|

Risks: Legal /

Health and Safety etc.

This

report provides a guideline of processes and procedures for the Subcommittee.

|

|

Conflict of

Interest

Not

applicable – reporting only.

|

|

Community Boards

There

are no known implications for Community Boards.

|

|

|

Audit and Risk Subcommittee

2 July 2020

|

|

|

Audit and Risk Subcommittee

2 July 2020

|

|

|

Audit and Risk Subcommittee

2 July 2020

|

Resolution to Exclude the

Public

That the Audit and Risk

Subcommittee:

Pursuant to the provisions of the

Local Government Official Information and Meetings Act 1987, exclude the public

from the following part of the proceedings of this meeting namely:

|

General subject of the matter to be considered

|

Reasons

for passing this resolution in relation to each matter

|

Ground(s) under

section 48(1) for the passing of this resolution

|

Reason for

Confidentiality

|

|

C1

Confirmation of the Confidential Minutes of Audit and Risk Subcommittee

meeting - 20 May 2020 - Public Excluded

|

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to prejudice the supply

of similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

S7(2)(b)(i)

The

withholding of the information is necessary to protect information where the

making available of the information would disclose a trade secret.

S7(2)(h)

The

withholding of the information is necessary to enable the local authority to

carry out, without prejudice or disadvantage, commercial activities.

S7(2)(g)

The

withholding of the information is necessary to maintain legal professional

privilege.

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of natural

persons, including that of a deceased person.

S7(2)(b)(ii)

The

withholding of the information is necessary to protect information where the

making available of the information would be likely unreasonably to prejudice

the commercial position of the person who supplied or who is the subject of

the information.

S6(b)

The

making available of the information would be likely to endanger the safety of

a person.

|

.

|

|

|

C2

Audit Engagement Letter and Audit Arrangements for Year Ending 30 June 2020

|

S7(2)(i)

The

withholding of the information is necessary to enable the local authority to

carry on, without prejudice or disadvantage, negotiations (including

commercial and industrial negotiations).

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C3

Audit and Risk Subcommittee Action List Report

|

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to prejudice the supply

of similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C4

DCC Policy Update Report

|

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to prejudice the supply

of similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C5

DCC Corporate Risk Register Update - June 2020

|

S7(2)(h)

The

withholding of the information is necessary to enable the local authority to

carry out, without prejudice or disadvantage, commercial activities.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C6

COVID-19 Risk Upate Report - June 2020

|

S7(2)(h)

The

withholding of the information is necessary to enable the local authority to

carry out, without prejudice or disadvantage, commercial activities.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C7

Internal Audit Workplan Update

|

S7(2)(b)(i)

The

withholding of the information is necessary to protect information where the

making available of the information would disclose a trade secret.

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is subject

to an obligation of confidence or which any person has been or could be

compelled to provide under the authority of any enactment, where the making

available of the information would be likely to prejudice the supply of

similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

S7(2)(h)

The

withholding of the information is necessary to enable the local authority to

carry out, without prejudice or disadvantage, commercial activities.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C8

Update on the DCC Internal Audit Actions Register

|

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to prejudice the supply

of similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C9

Update on the DCC External Audit Actions Register

|

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to prejudice the supply of

similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C10

ComplyWith Legal Compliance Report (Jan - Dec 2019)

|

S7(2)(c)(ii)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to damage the public

interest.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C11

Health and Safety Monthly Report for April / May 2020

|

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of natural

persons, including that of a deceased person.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C12

Treasury Risk Management Compliance Report

|

S7(2)(h)

The

withholding of the information is necessary to enable the local authority to

carry out, without prejudice or disadvantage, commercial activities.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C13

Dunedin City Holdings Ltd - Update on Audit and Risk Activity

|

S7(2)(b)(ii)

The

withholding of the information is necessary to protect information where the

making available of the information would be likely unreasonably to prejudice

the commercial position of the person who supplied or who is the subject of

the information.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C14

Protected Disclosure Register

|

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of natural

persons, including that of a deceased person.

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to prejudice the supply

of similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C15

Investigation Register

|

S6(b)

The

making available of the information would be likely to endanger the safety of

a person.

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of natural

persons, including that of a deceased person.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 6 and

7.

|

The matters detailed i

this report are subject to investigation and information should remain

confidential so not to prejudice the investigation and any possible outcomes

of the investigation..

|

This resolution is made in

reliance on Section 48(1)(a) of the Local Government Official Information and

Meetings Act 1987, and the particular interest or interests protected by

Section 6 or Section 7 of that Act, or Section 6 or Section 7 or Section 9 of

the Official Information Act 1982, as the case may require, which would be

prejudiced by the holding of the whole or the relevant part of the proceedings

of the meeting in public are as shown above after each item.

That Julian Tan (Audit New Zealand) and Monique Kruger

(Audit New Zealand) be permitted to remain at the meeting, after the public has

been excluded, because of their knowledge of Item C2. This knowledge,

which would be of assistance in relation to the matters discussed, was relevant

because they would be reporting on the item under consideration.