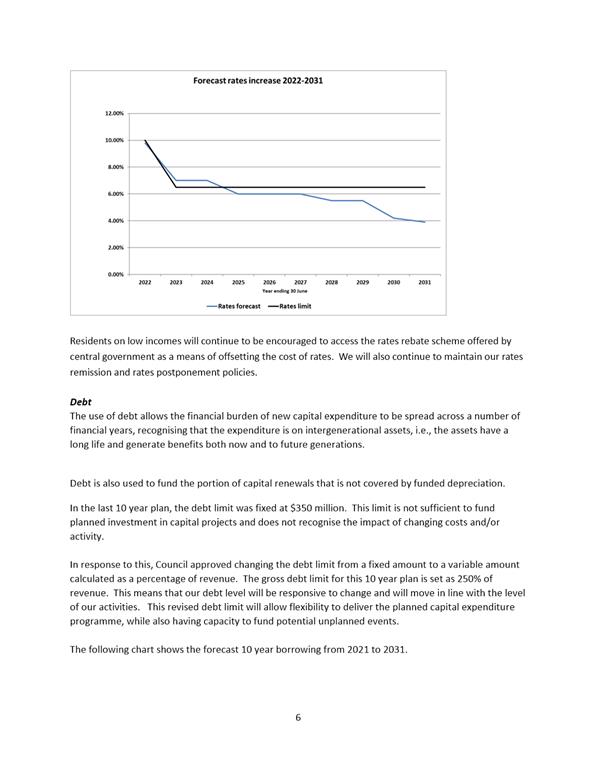

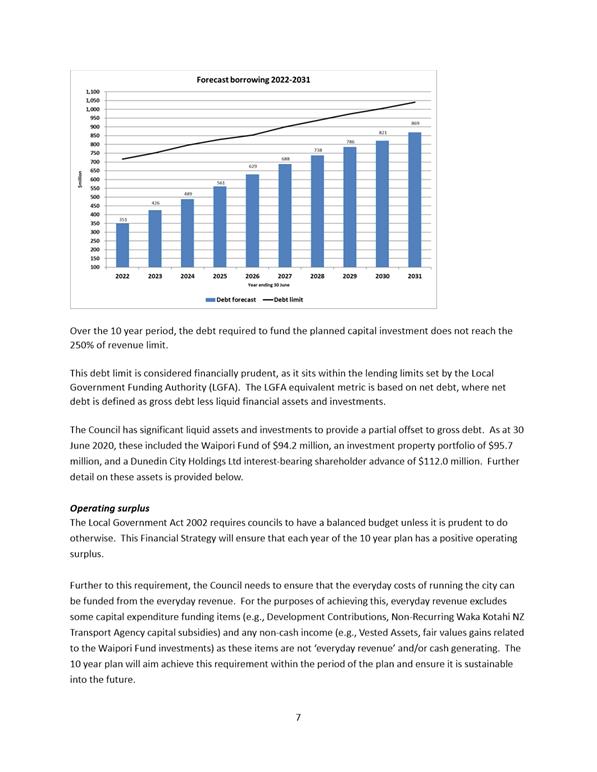

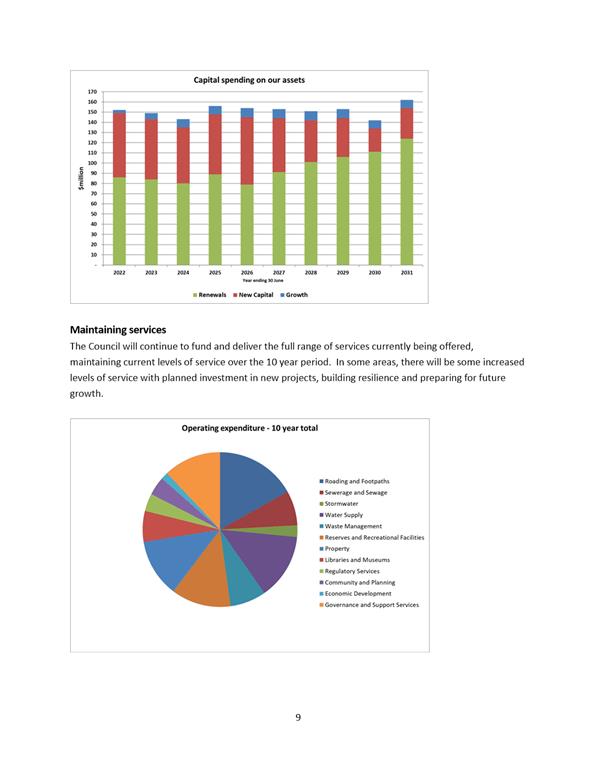

|

|

Audit and Risk Subcommittee

18 February 2021

|

10 year plan 2021-31 Update Report

Department: Corporate Policy

EXECUTIVE SUMMARY

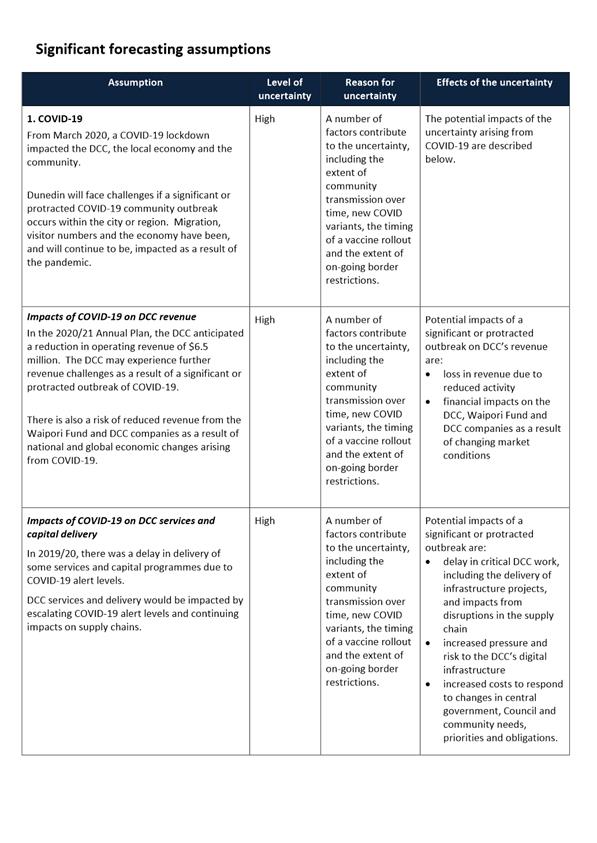

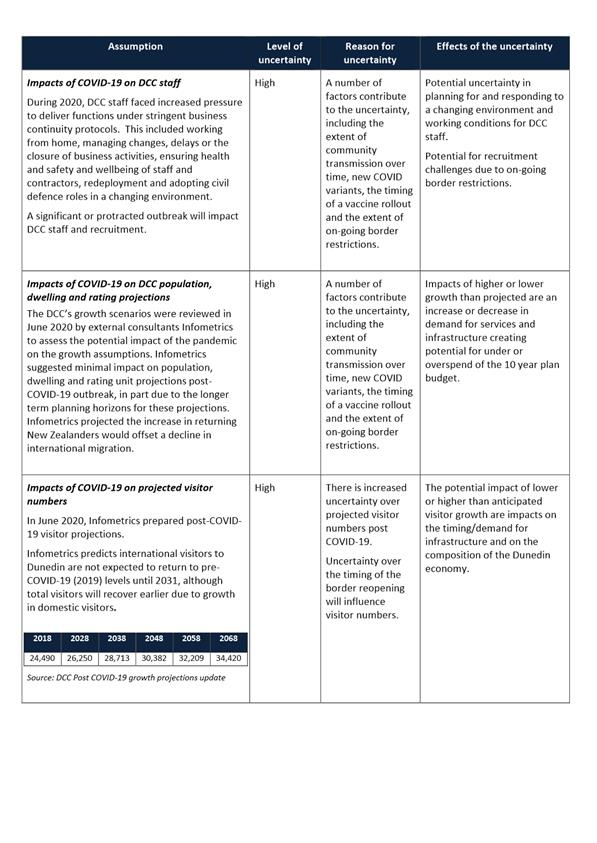

1 The

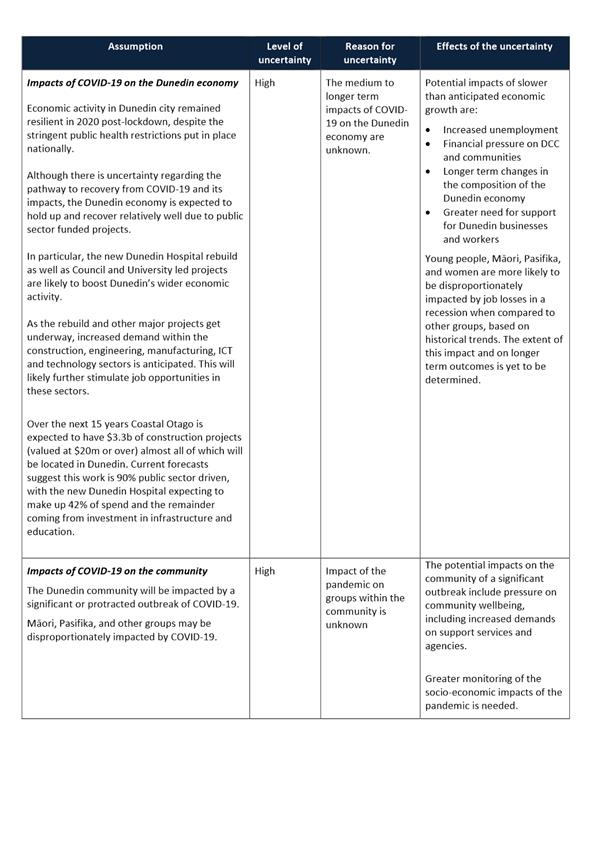

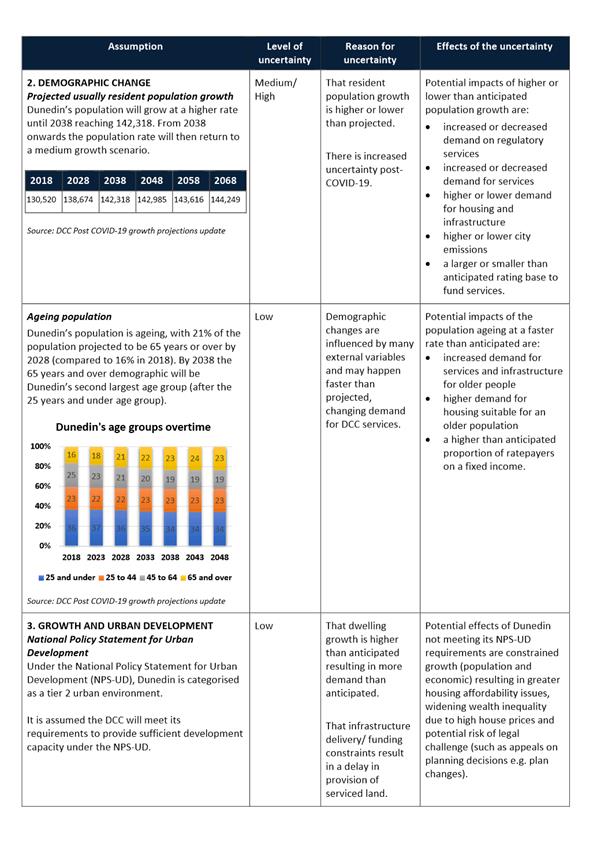

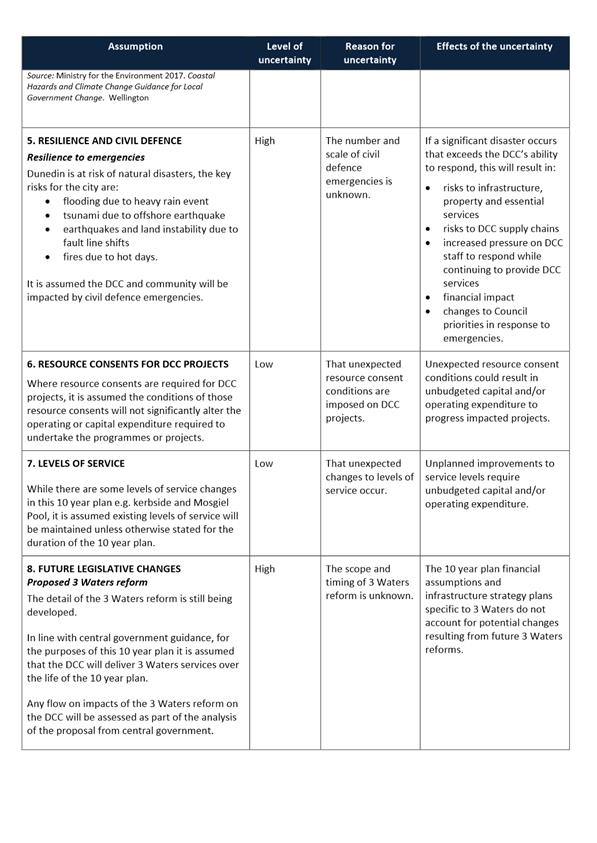

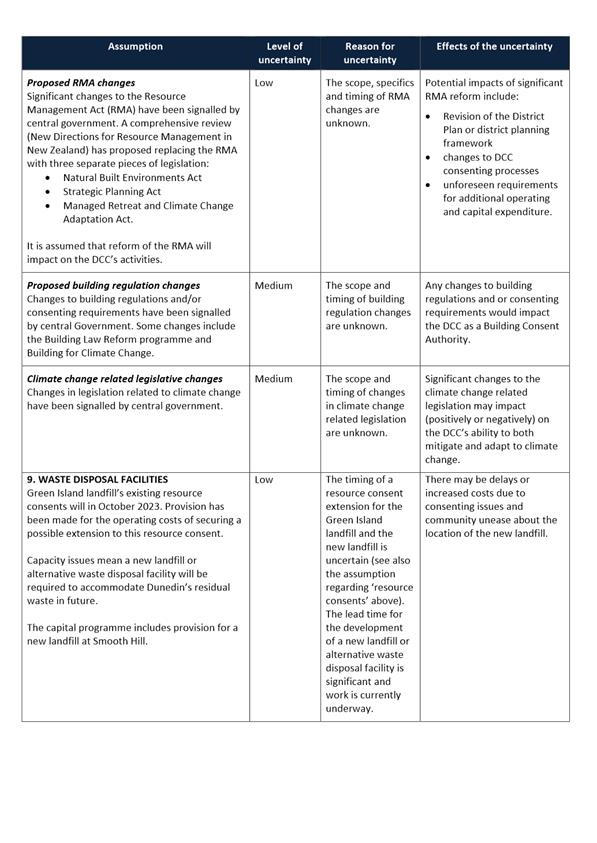

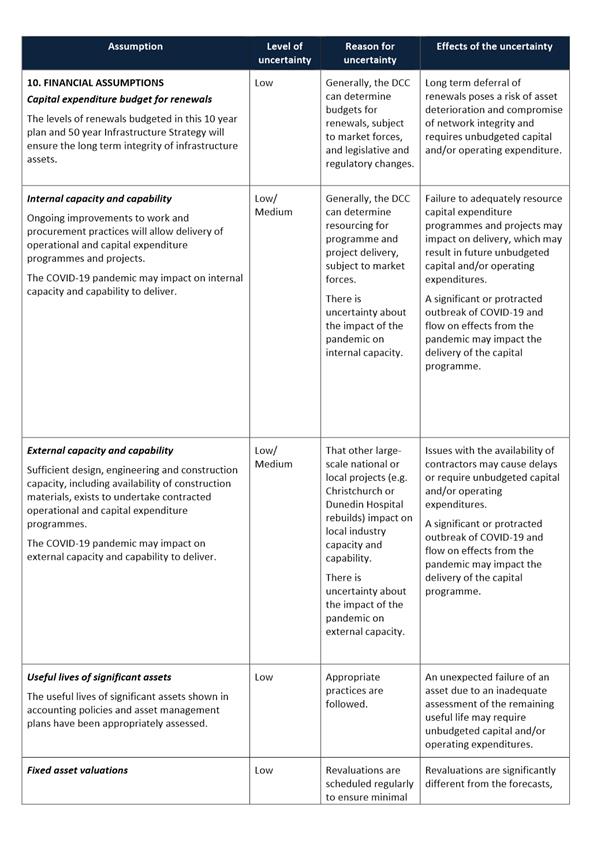

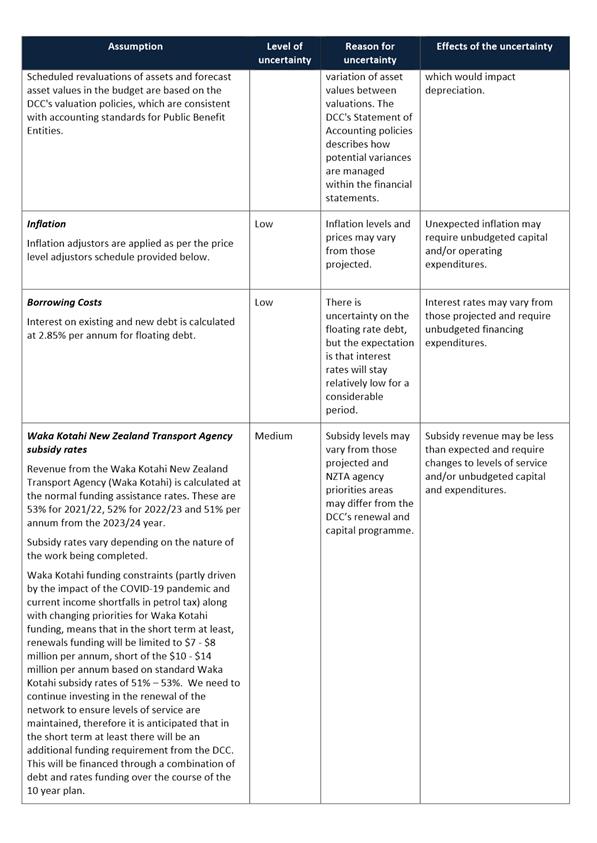

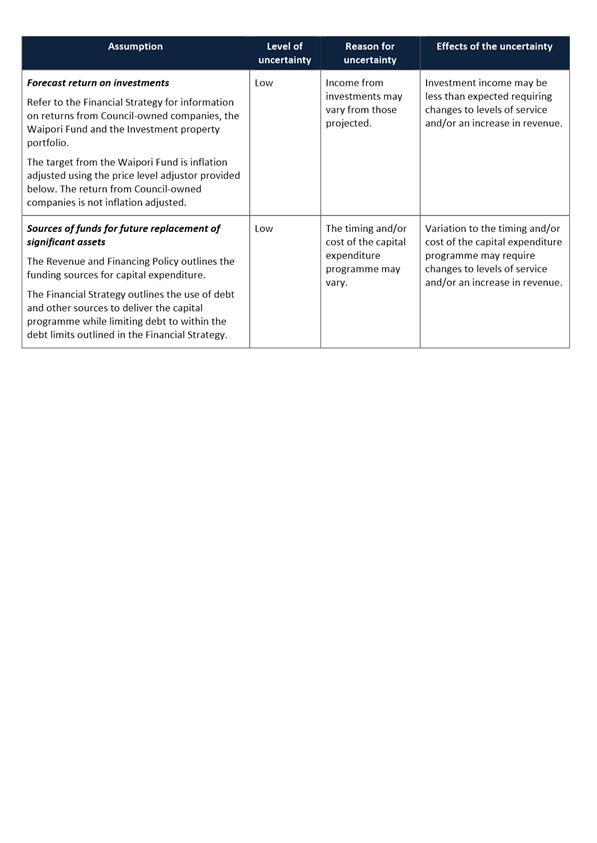

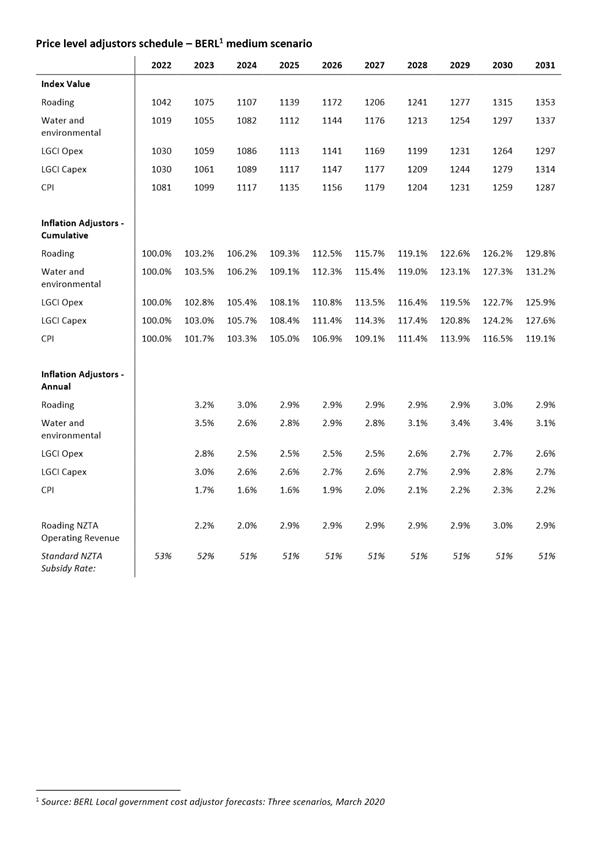

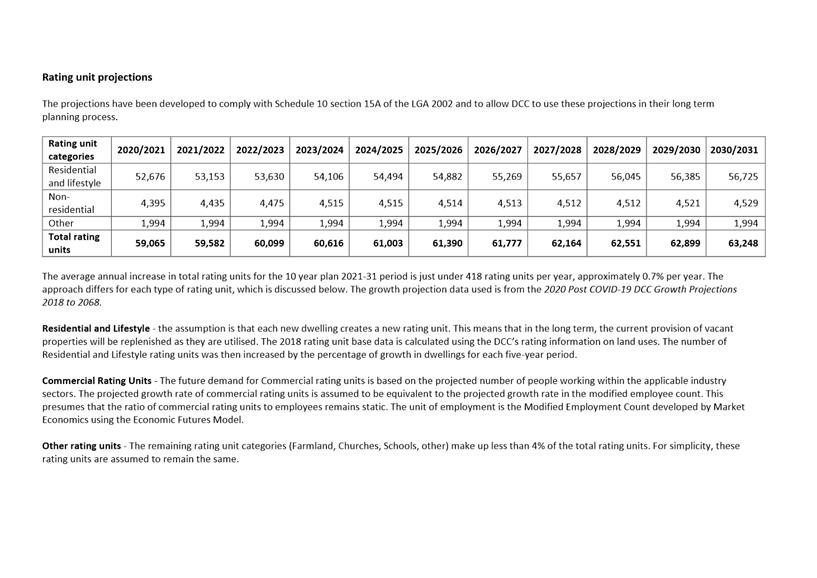

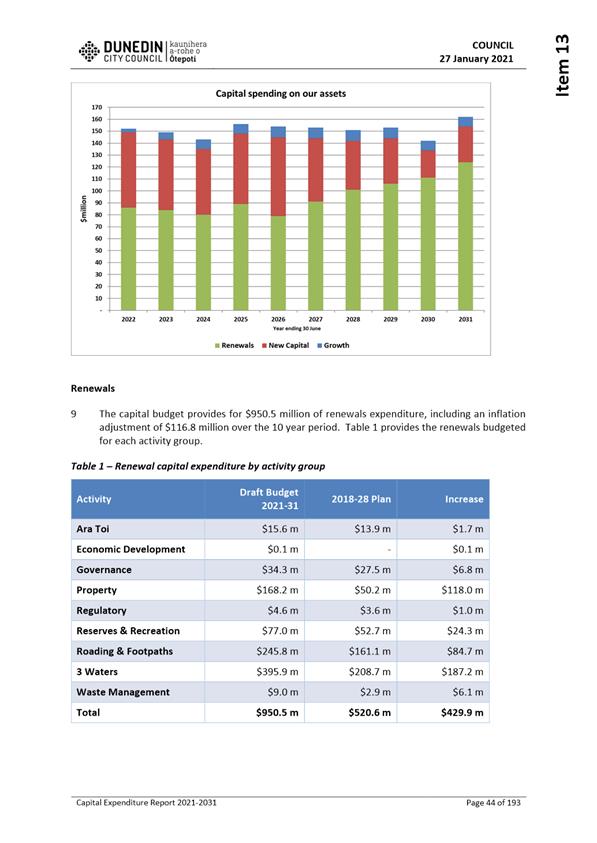

purpose of this report is to provide the Audit and Risk Subcommittee with an

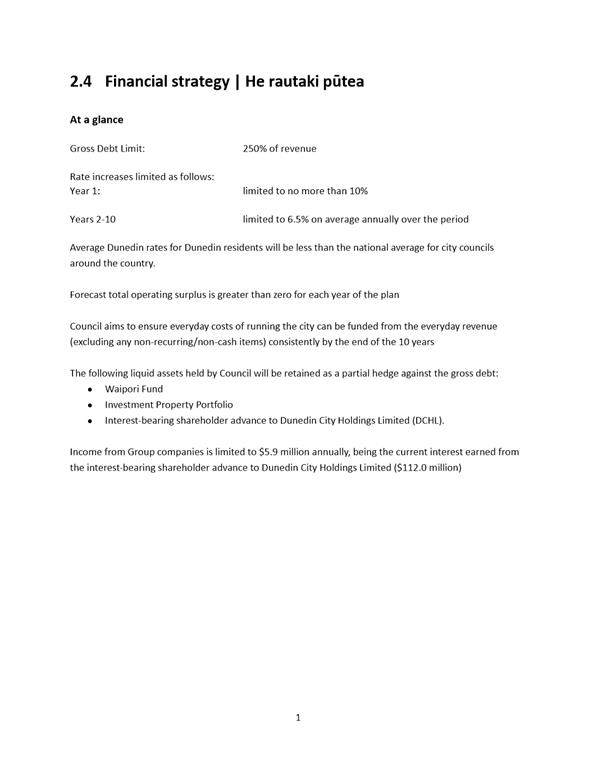

update on the development of the 10 year plan 2021-31 (10 year plan).

2 As

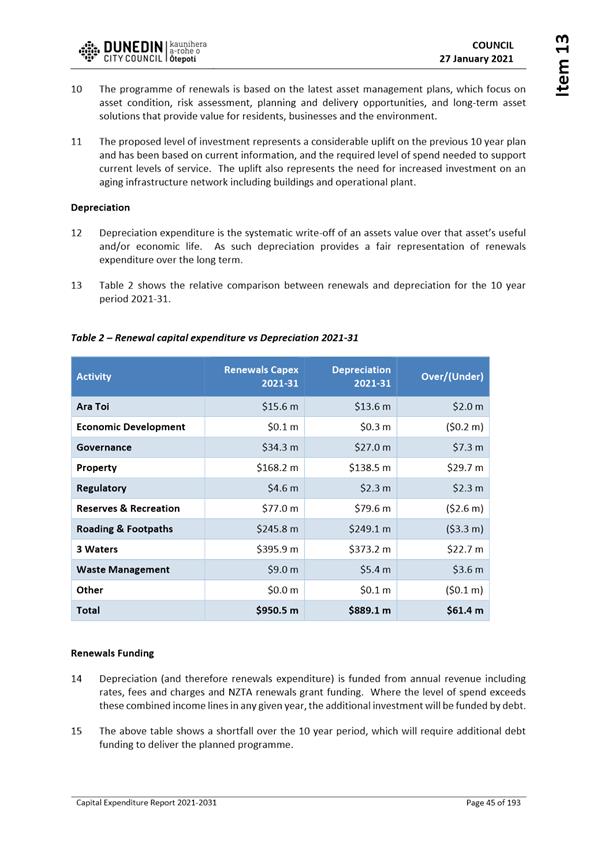

this is an update report, there are no options or Summary of

Consideration.

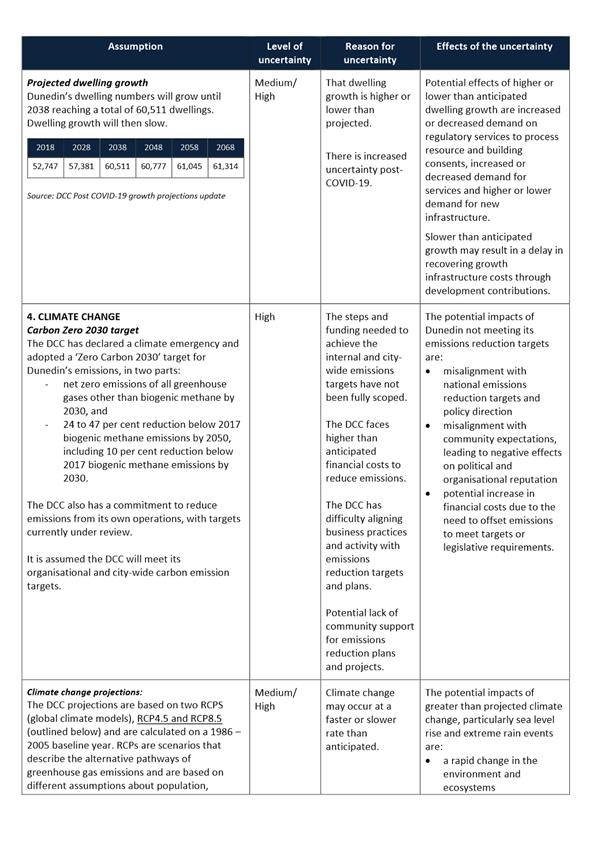

|

RECOMMENDATIONS

That the Committee:

a) Notes the 10 Year Plan 2021-31 Update Report.

|

DISCUSSION

3 Since

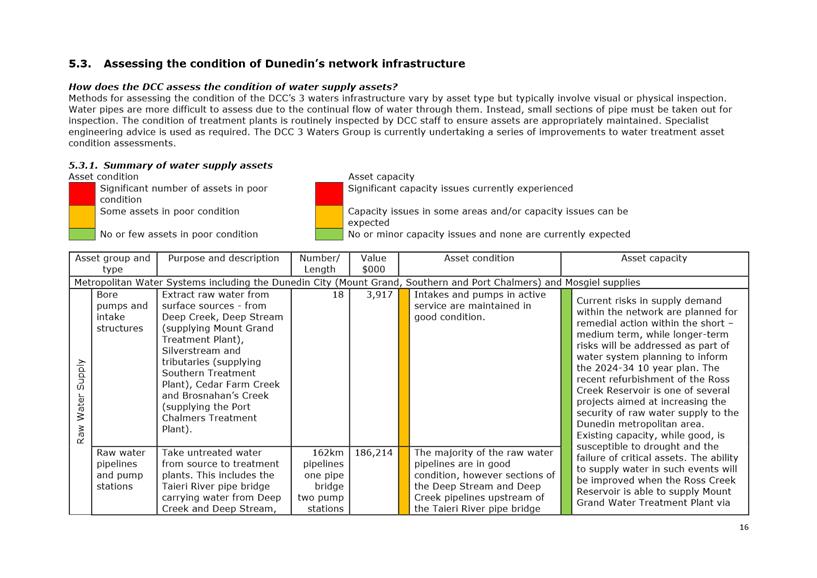

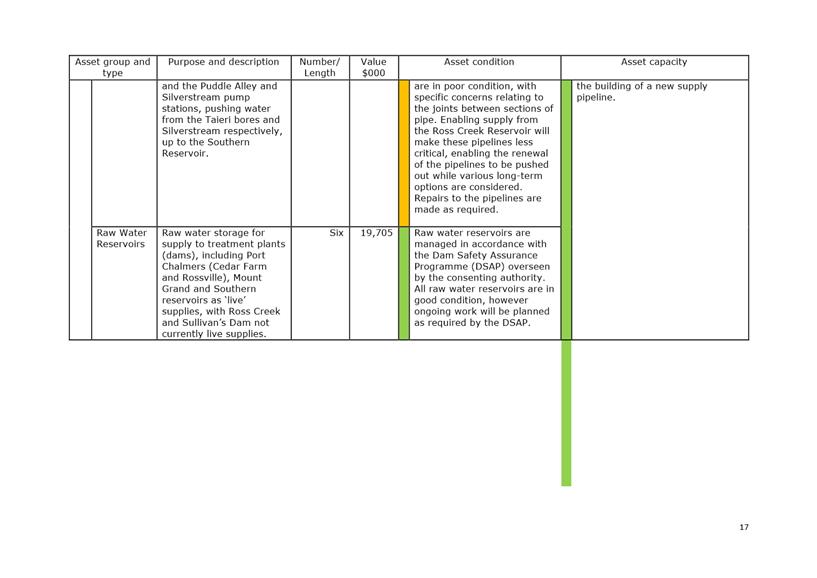

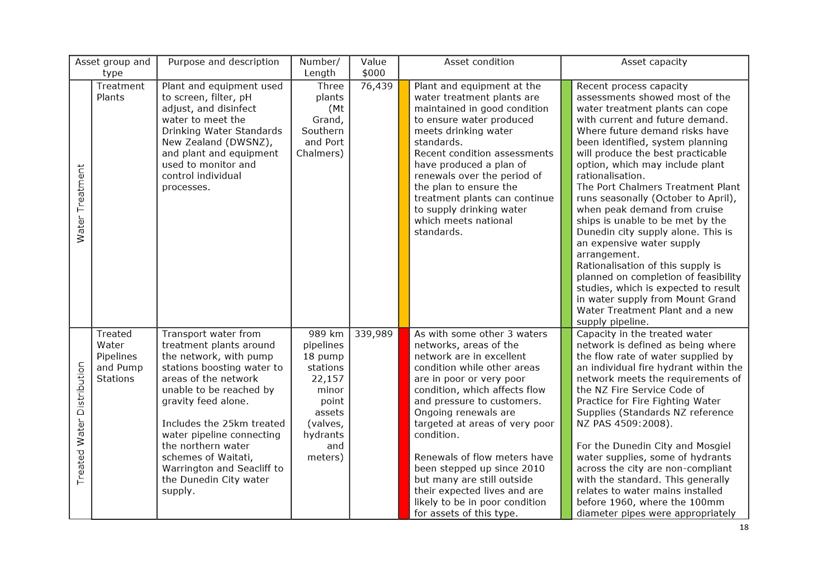

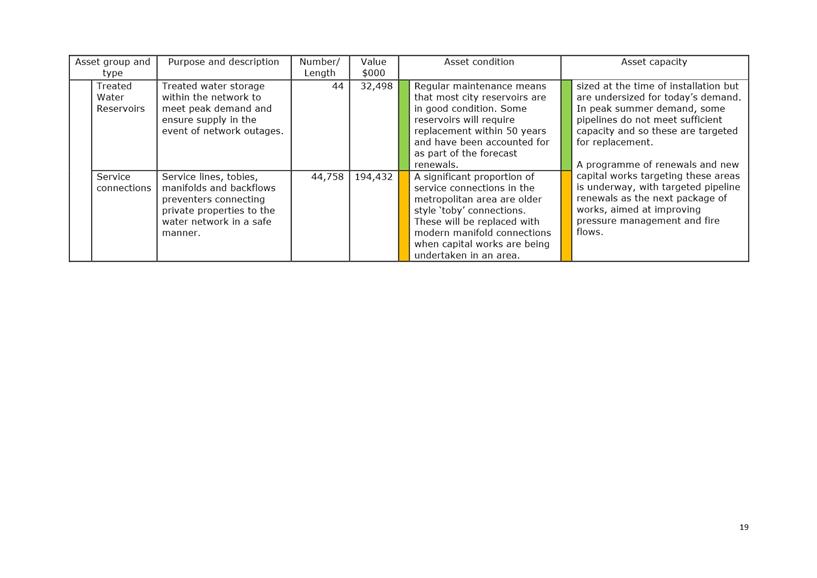

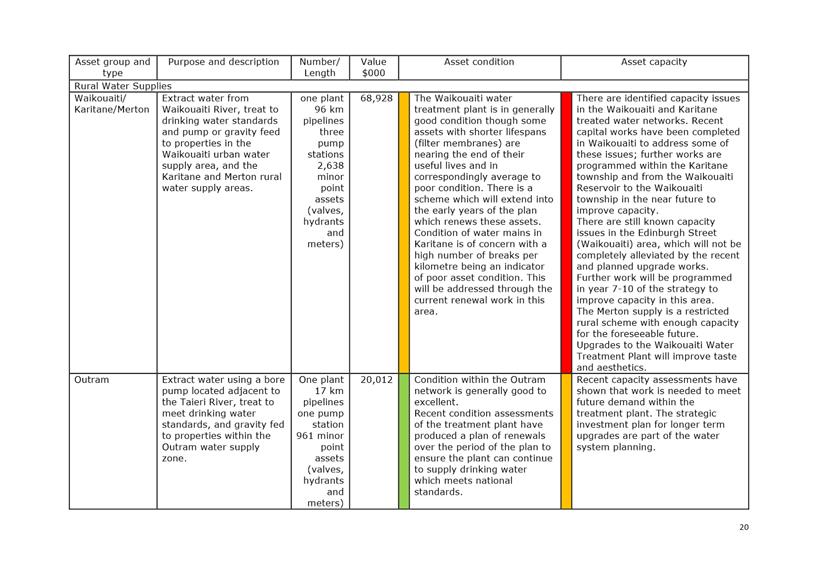

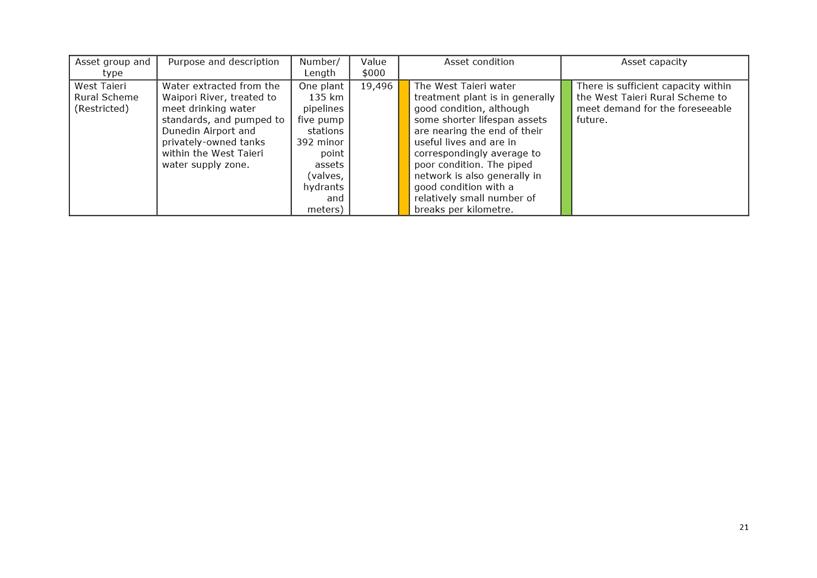

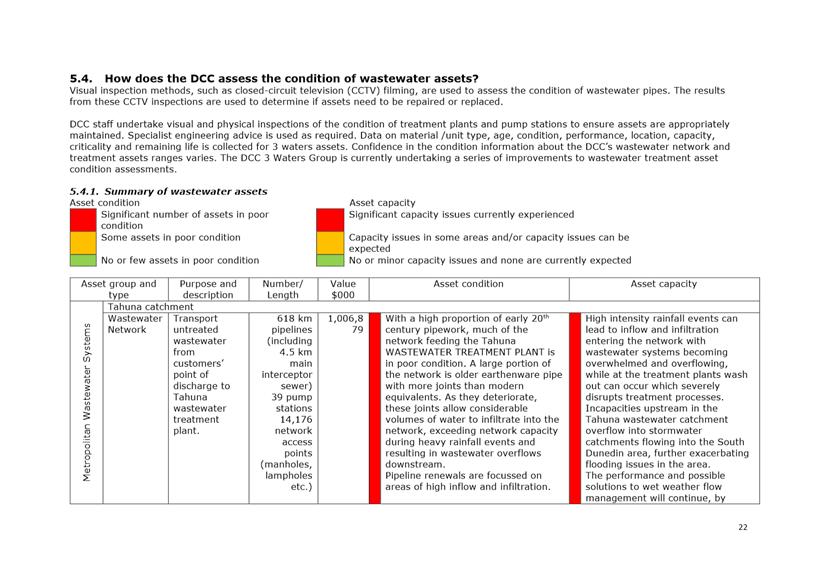

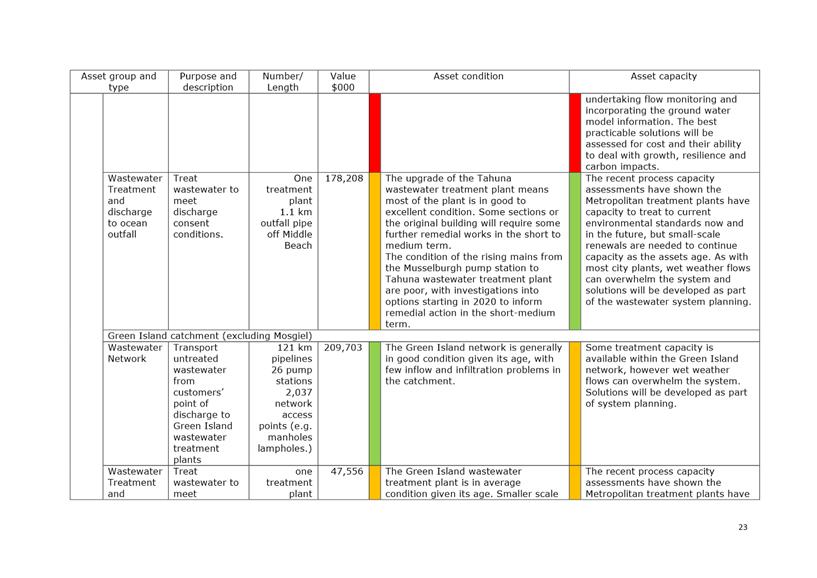

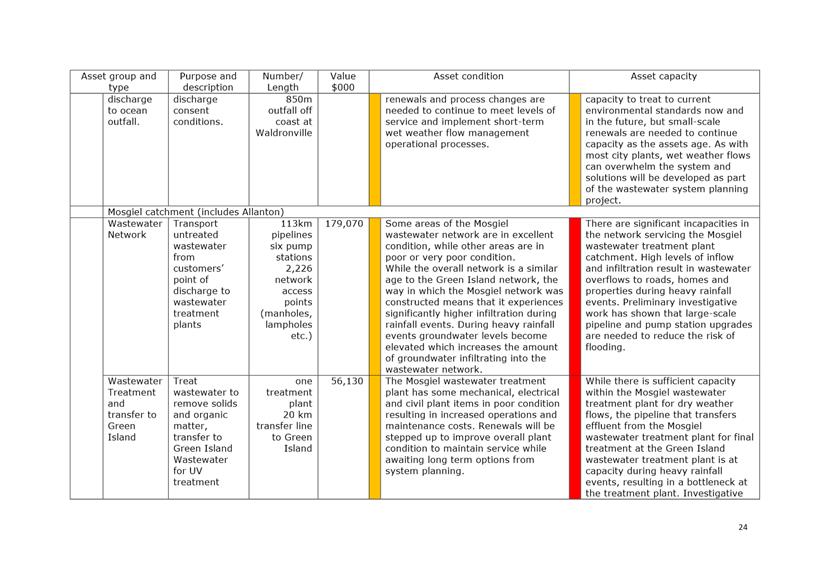

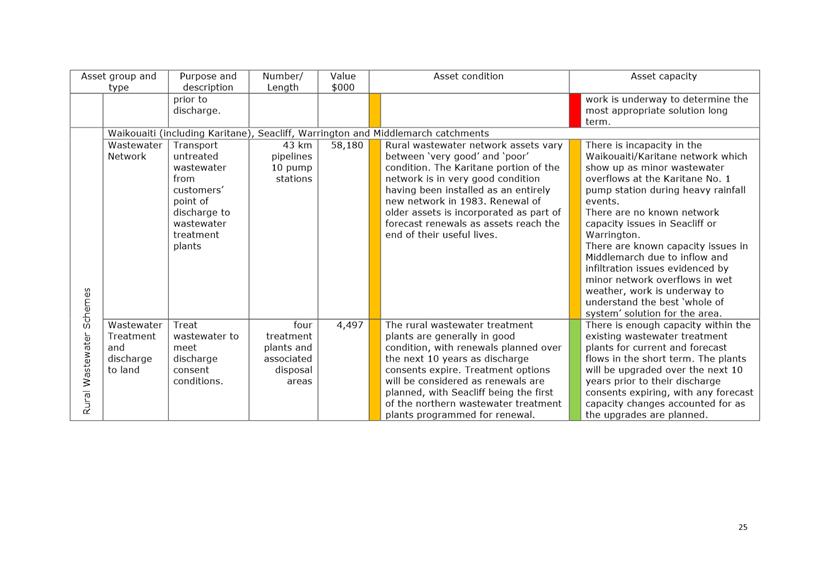

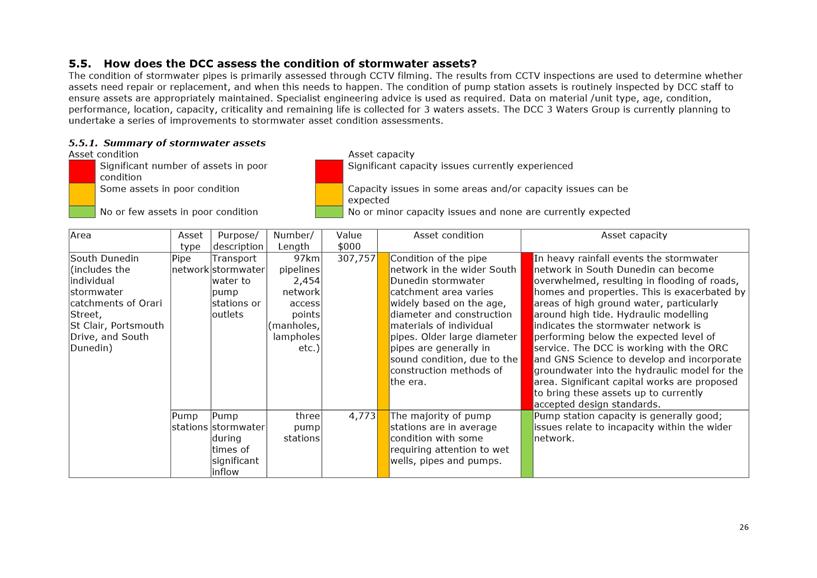

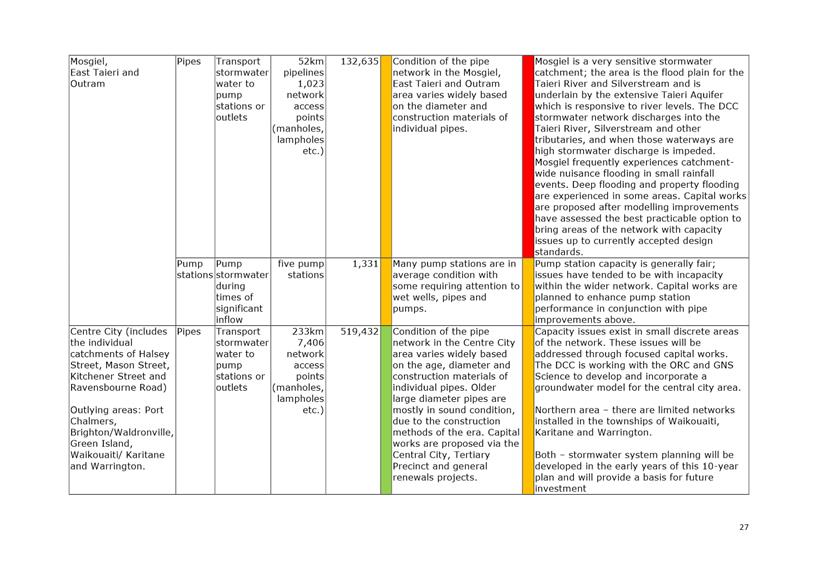

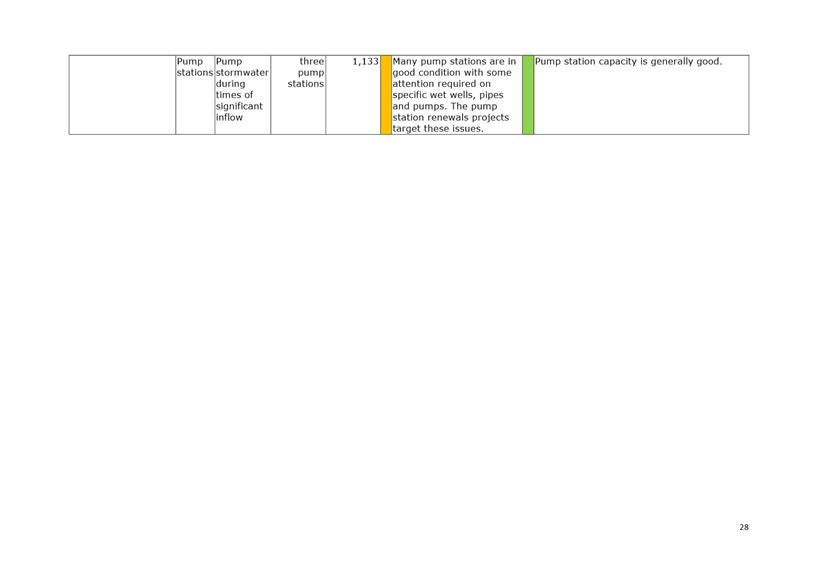

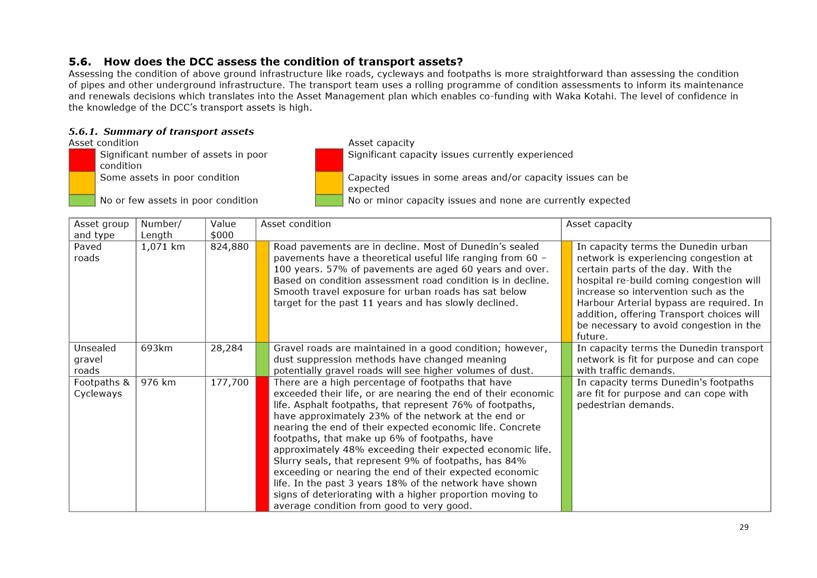

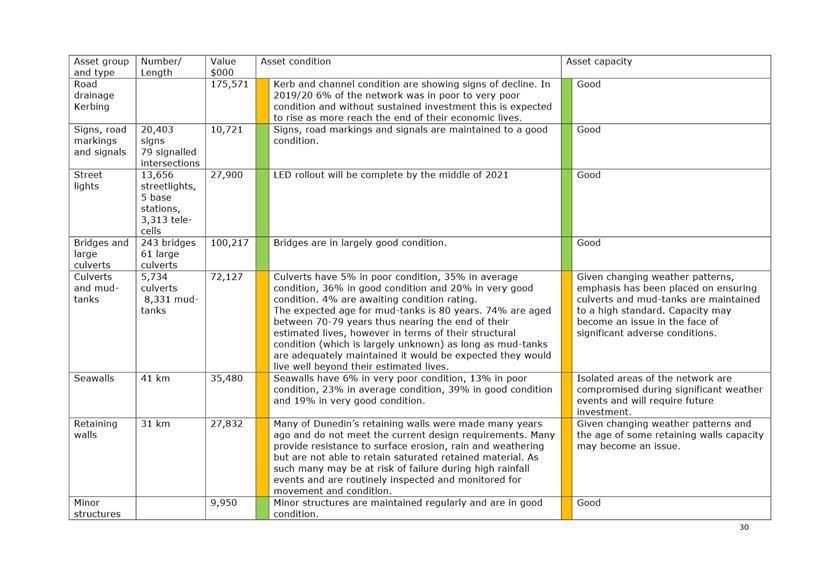

the last update to the Audit and Risk Subcommittee on 2 December 2020,

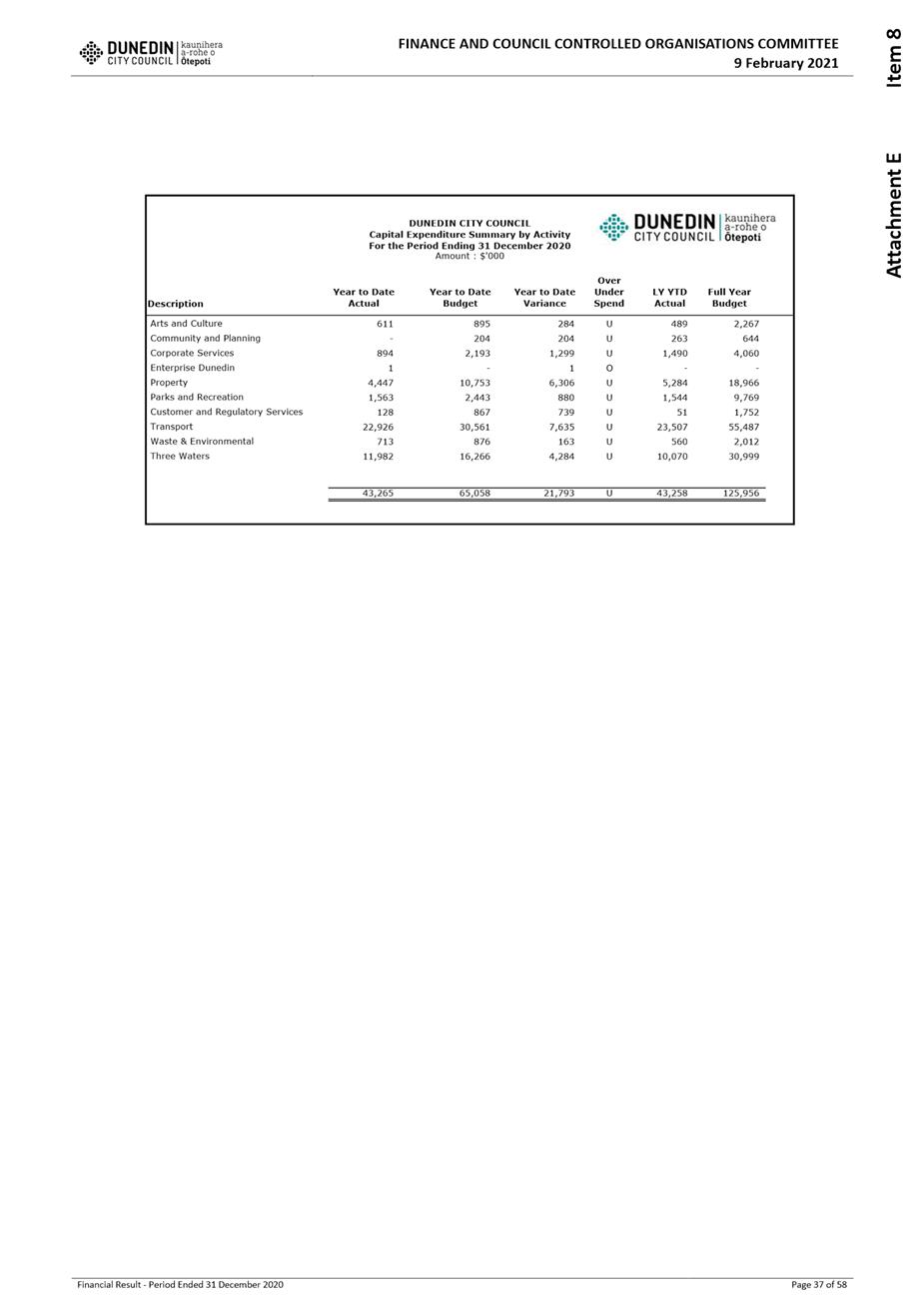

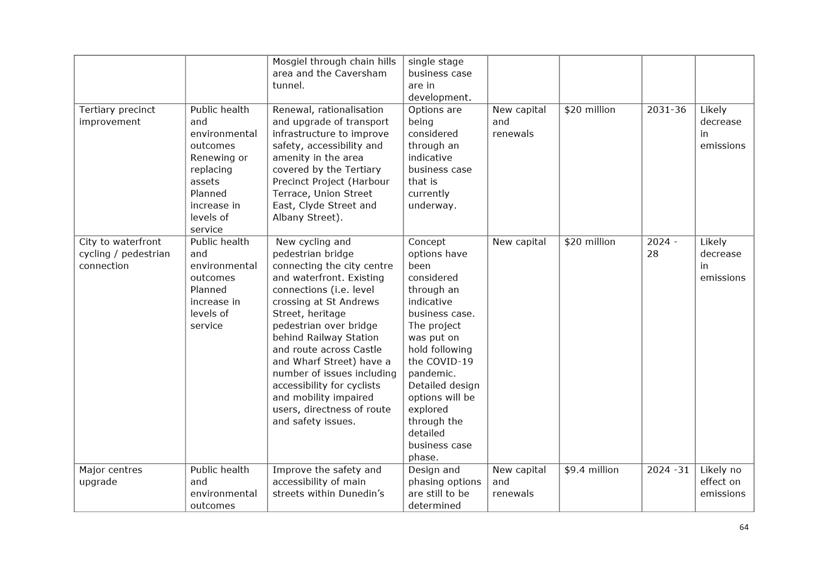

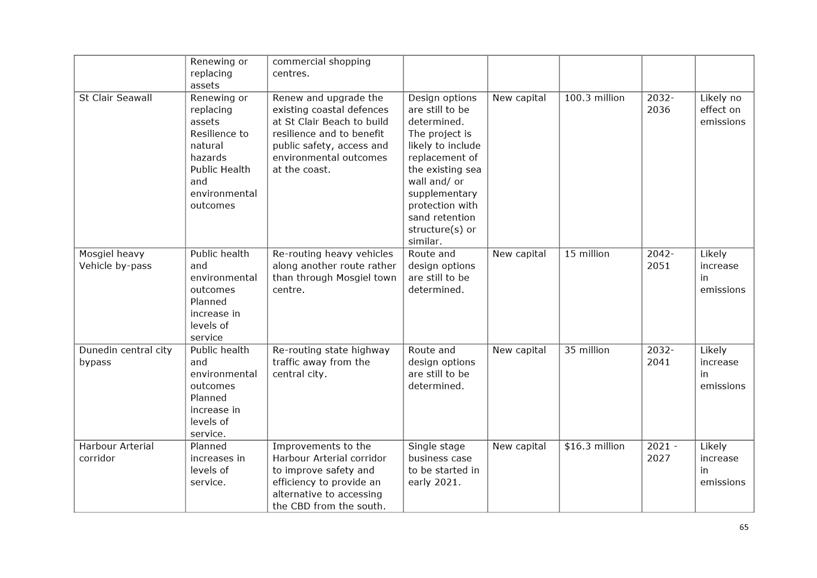

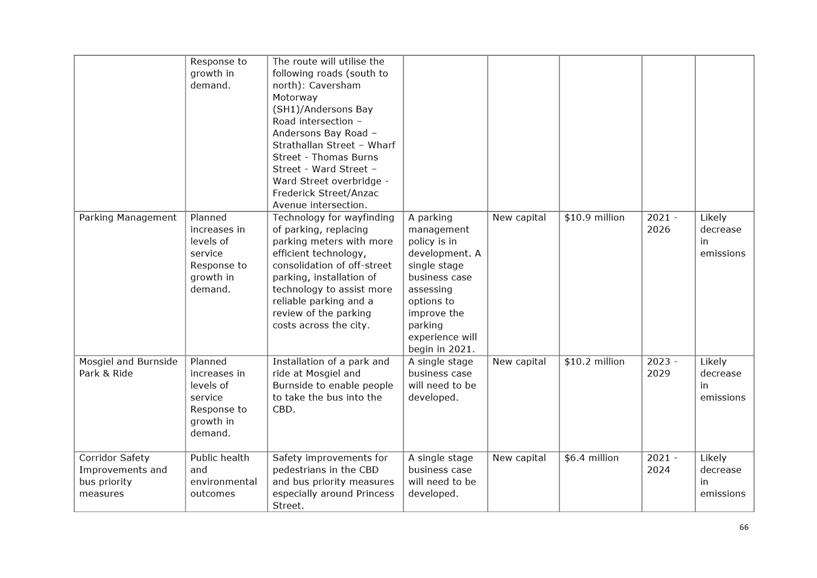

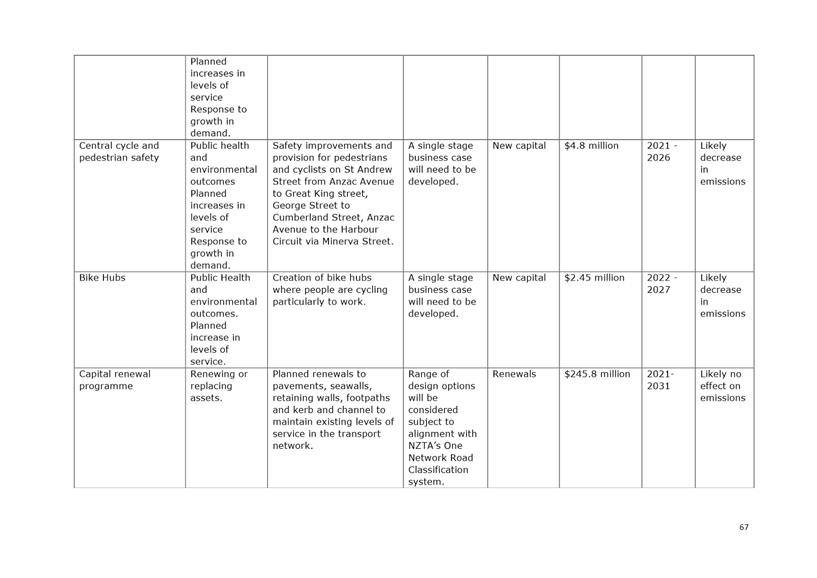

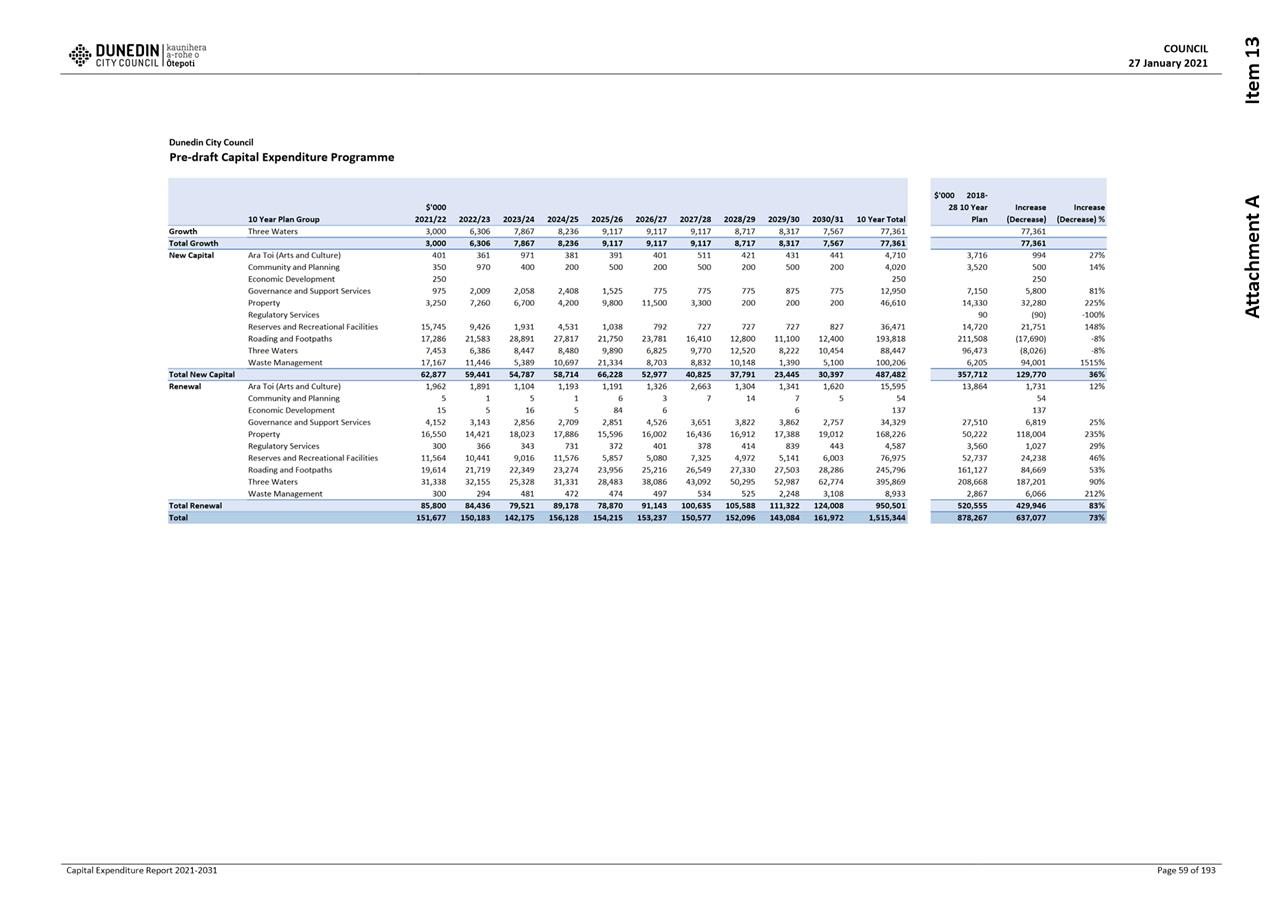

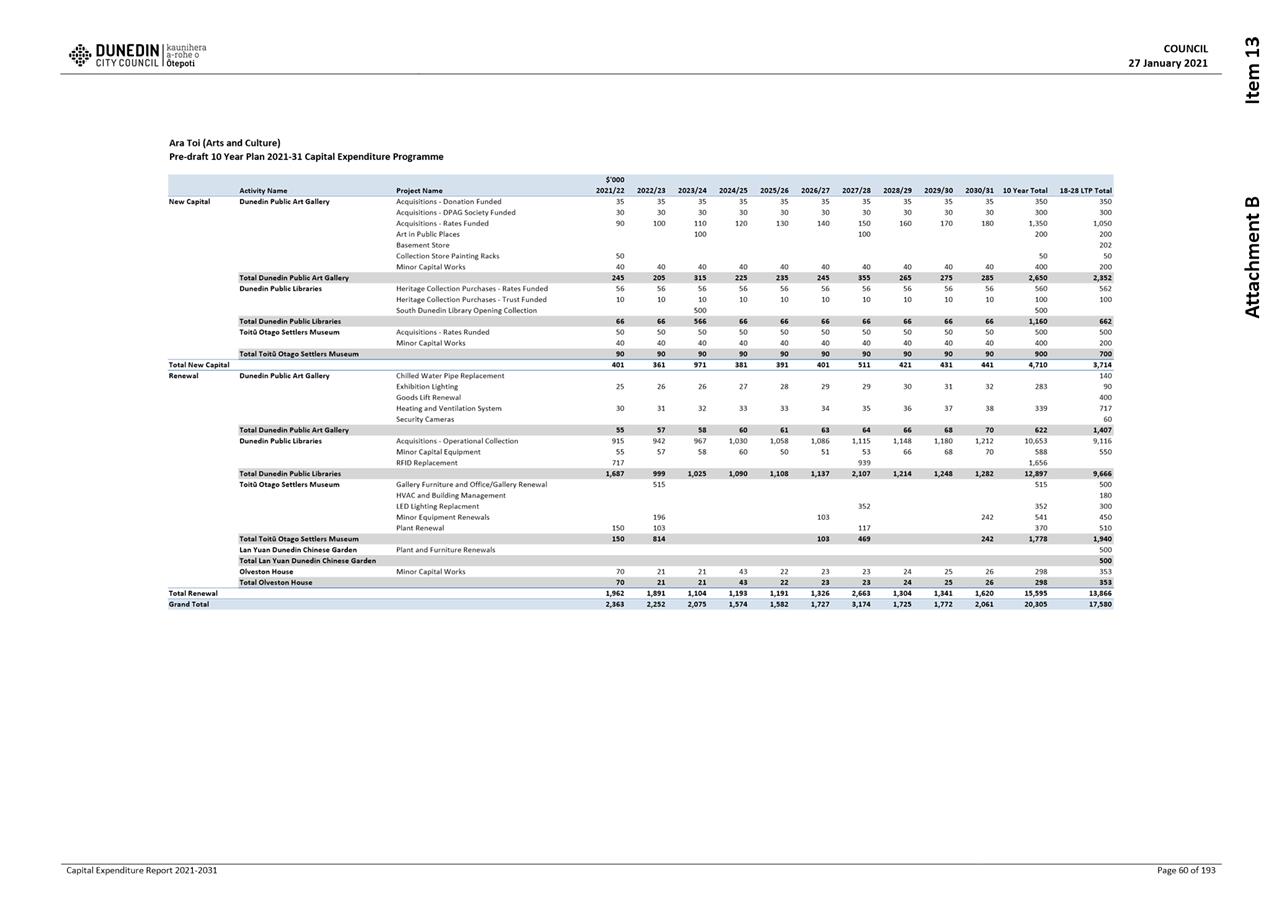

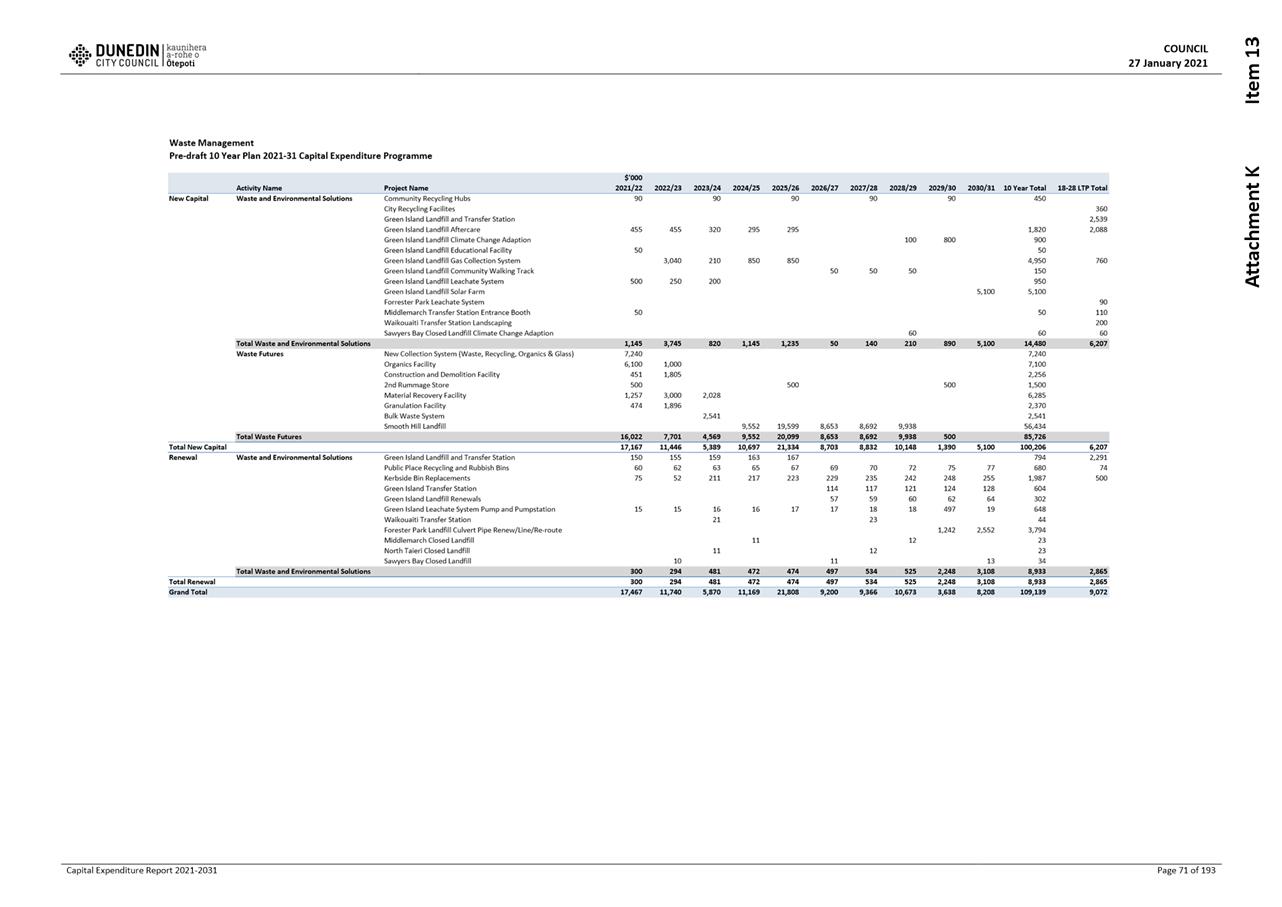

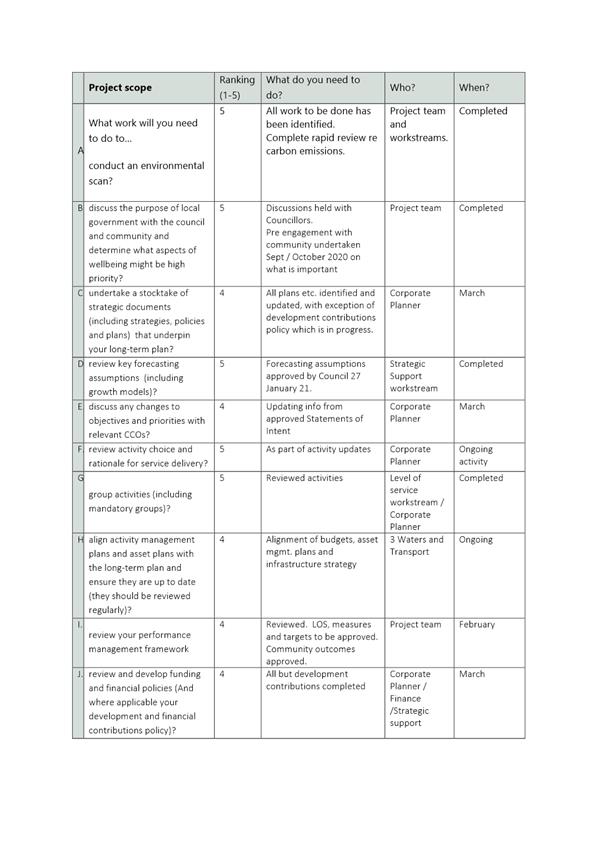

significant progress has been made on the development of the 10 year

plan.

4 A

Council meeting was held on 14/15 December 2020, to consider option reports for

capital projects. Decisions made at that meeting have assisted the

development of capital budgets, and identified options, both preferred and

alternative, for projects that will be included in the consultation

document.

5 A

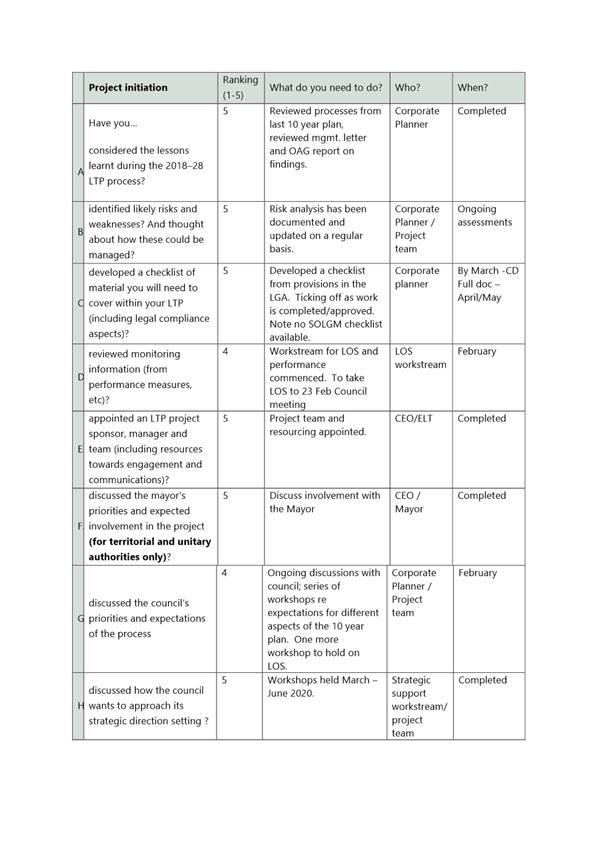

further Council meeting was held on 27 – 29 January 2021, to consider the

following:

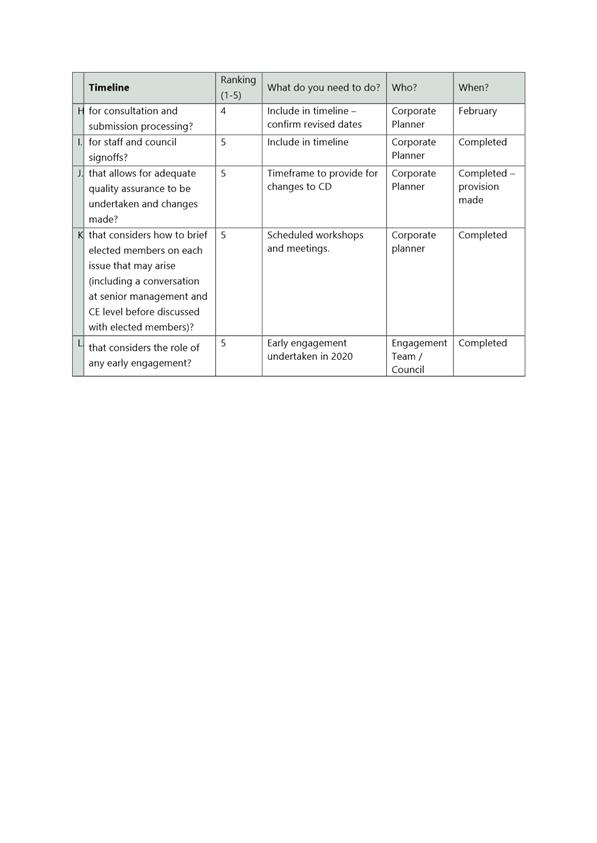

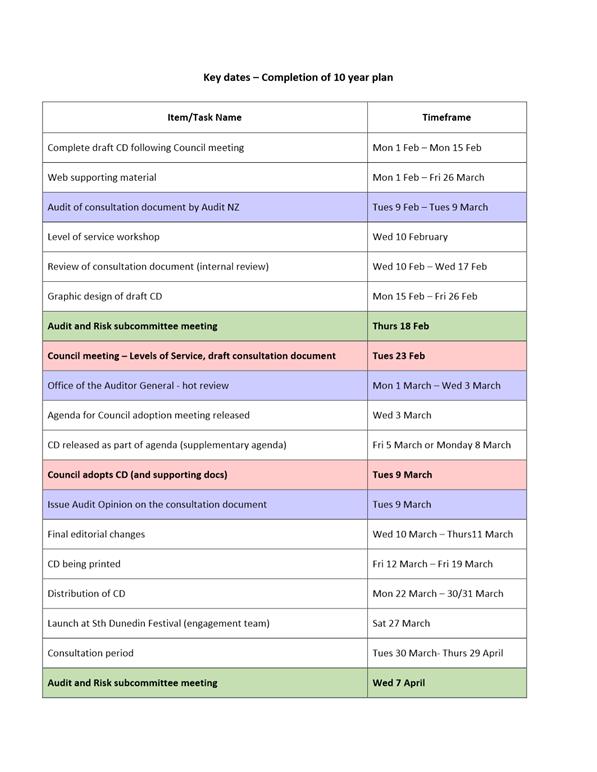

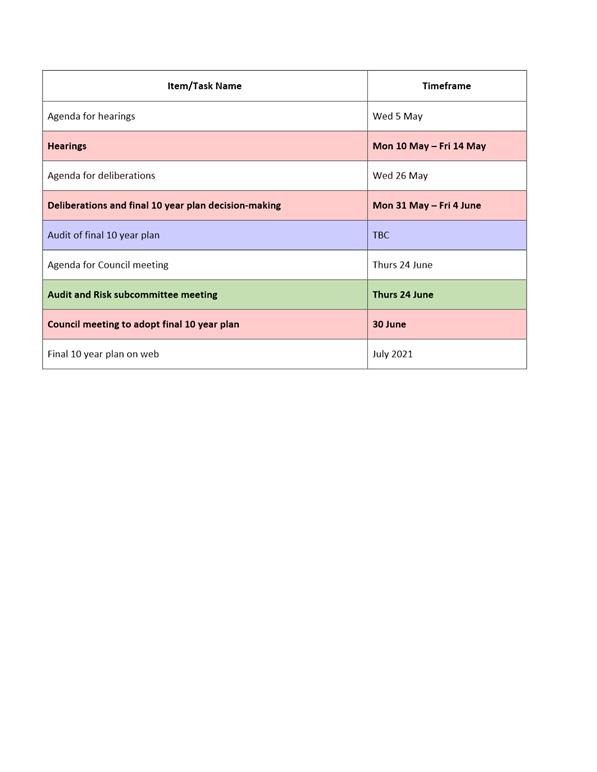

· Capital

and operating budgets,

· Financial

and infrastructure strategies,

· Significant

forecasting assumptions,

· Climate

2030 Rapid Review and DCC emissions reduction opportunities,

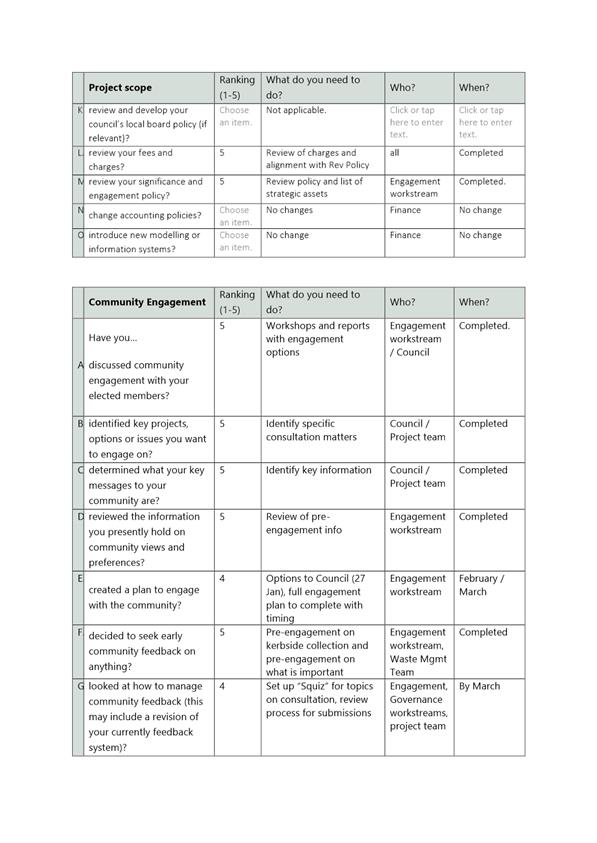

· Significance

and Engagement, Revenue and Financing, and Rates Remission and Postponement

policies, and

· Rating

method for 2021/22.

6 Levels

of service will be considered at a meeting on 23 February 2021.

7 There

are some key areas that our auditors are expected to focus on during the 10

year plan audit and our response to these are discussed below.

COVID-19

8 The

impacts of COVID-19 have been taken account of in the development of the draft

10 year plan.

9 The

Significant Forecasting Assumptions, provided at Attachment A, discuss the

possible impacts of COVID-19 on DCC revenue, services and capital delivery,

staff, population, dwellings and rating projections, visitor numbers, the

economy, and the community. These assumptions have a high level of

uncertainty for reasons including the extent of any possible future community

transmission, new variants, the timing of a vaccine rollout, and the extent of

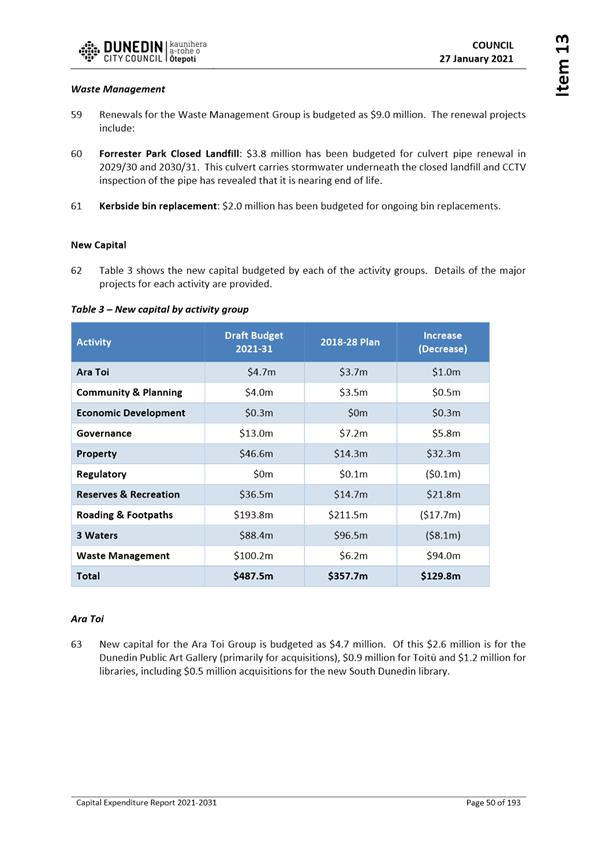

ongoing border restrictions.

10 The

Financial Strategy, provided at Attachment B, recognises the upheaval from

COVID-19, and the resulting uncertainty around Dunedin’s growth and

economic performance into the future.

11 The

Consultation Document will include commentary on COVID-19, recognising the

important role that the DCC needs to play in the way the city recovers, and the

need to keep investing in the city.

Climate change and zero

carbon

12 Climate

change and Council’s zero carbon 2030 target have been considered

throughout the development of the draft 10 year plan. All option reports

presented to Council included an analysis of the impacts of each presented

option on climate change and zero carbon, to assist decision making.

13 The

Financial Strategy discusses two workstreams, climate change adaptation, and

zero carbon 2030 which is focused on climate change mitigation. The

Financial Strategy recognises that sea level rise and adverse weather events

causing flooding are significant risks for Dunedin, and of particular concern

is the South Dunedin area.

14 The

Financial Strategy also discusses the zero carbon work programme, that has two

targets as follows:

· Net

zero emissions of all greenhouse gases other than biogenic methane by 2030, and

· 24%

to 47% reduction below 2017 biogenic methane emissions by 2050, including 10%

reduction below 2017 biogenic methane emissions by 2030.

15 While

the target is for the city as a whole, it also includes reducing emissions from

Council’s own activities, and transport and waste have been identified in

the 10 year plan as priority areas for investment to reduce emissions.

16 The

10 year plan includes budget for additional staff to progress the zero carbon

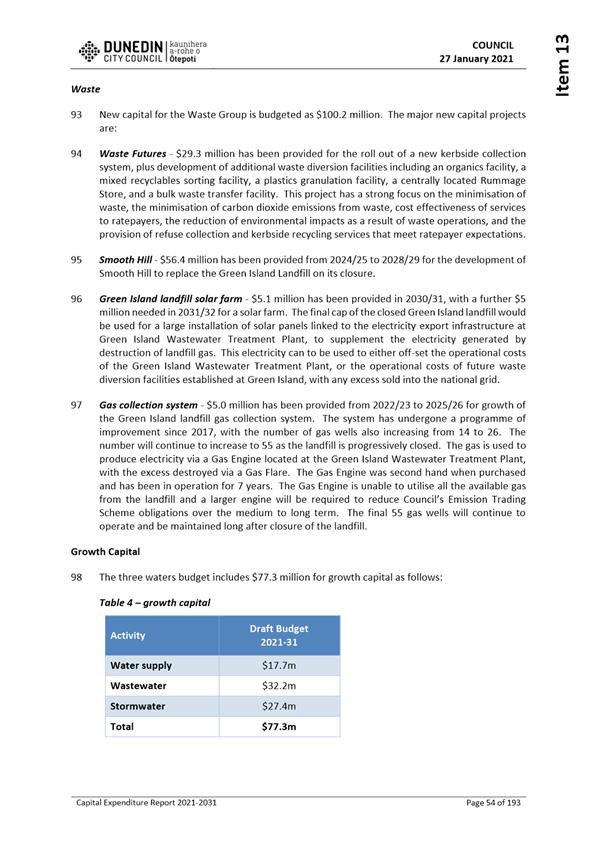

and South Dunedin Future projects and further budget for the “South

Dunedin Future” programme that is being developed with the Otago Regional

Council.

17 In

2020, a “rapid review” was undertaken to look at planned work

programmes alongside the DCC’s emissions reduction ambitions and Zero

Carbon 2030 target, and to identify initiatives to reduce and/or offset

Dunedin’s greenhouse gas emissions. Key findings were presented to

Council at the 27 January 2021 Council meeting, to consider draft 10 Year Plan

budgets with identified emissions reduction opportunities.

18 The

Infrastructure Strategy, provided at Attachment C, identifies climate change

and zero carbon 2030 as significant issues for Dunedin. Increased demand

on both the transport network and the 3 waters network are recognised in terms

of the effects of flooding, drought, catchment fire, and rising

groundwater. The strategy also considers other natural hazards in

addition to climate change.

19 New

levels of service are being proposed for the draft 10 year plan that will

assist monitoring progress towards achieving Council’s zero carbon 2030

target. These are marked with a green leaf symbol -  . Examples

include targets to reduce the amount of energy used by DCC properties,

increasing the amount of diversion of recyclable or reusable materials, and

reducing the amount of solid waste.

. Examples

include targets to reduce the amount of energy used by DCC properties,

increasing the amount of diversion of recyclable or reusable materials, and

reducing the amount of solid waste.

20 The

Consultation Document will include commentary on climate change, the zero

carbon 2030 target and reducing waste initiatives.

Condition and performance of

critical assets

21 The

Infrastructure Strategy provides information about the current condition of

Dunedin’s network infrastructure for 3 waters and transport assets.

It discusses how asset condition is assessed, and the need to increase the

level of renewals to improve resilience.

22 The

capital budget proposes that $1.5 billion be spent over the 10 year period

compared to

$878 million in the current 10 year plan 2018-28. Of this $950 million

(including inflation) is proposed to be spent on renewals compared to $520

million in the current plan. This budget recognises that renewals are a

priority for Council, with budgets based on the latest asset management plans

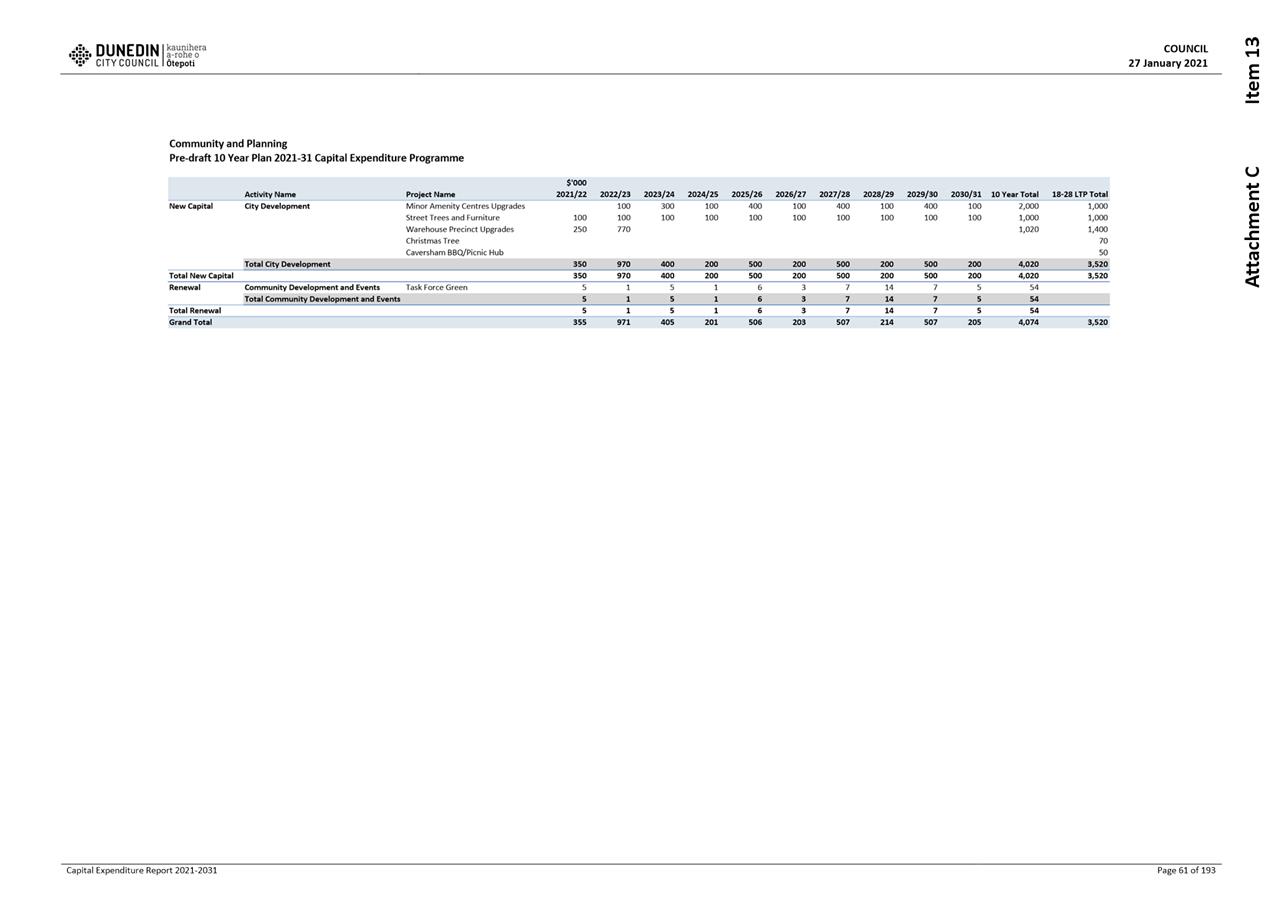

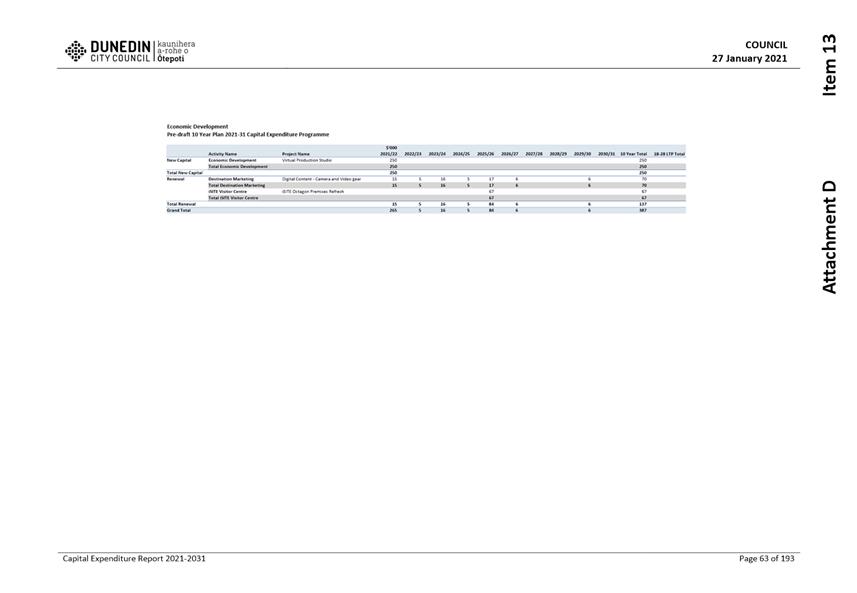

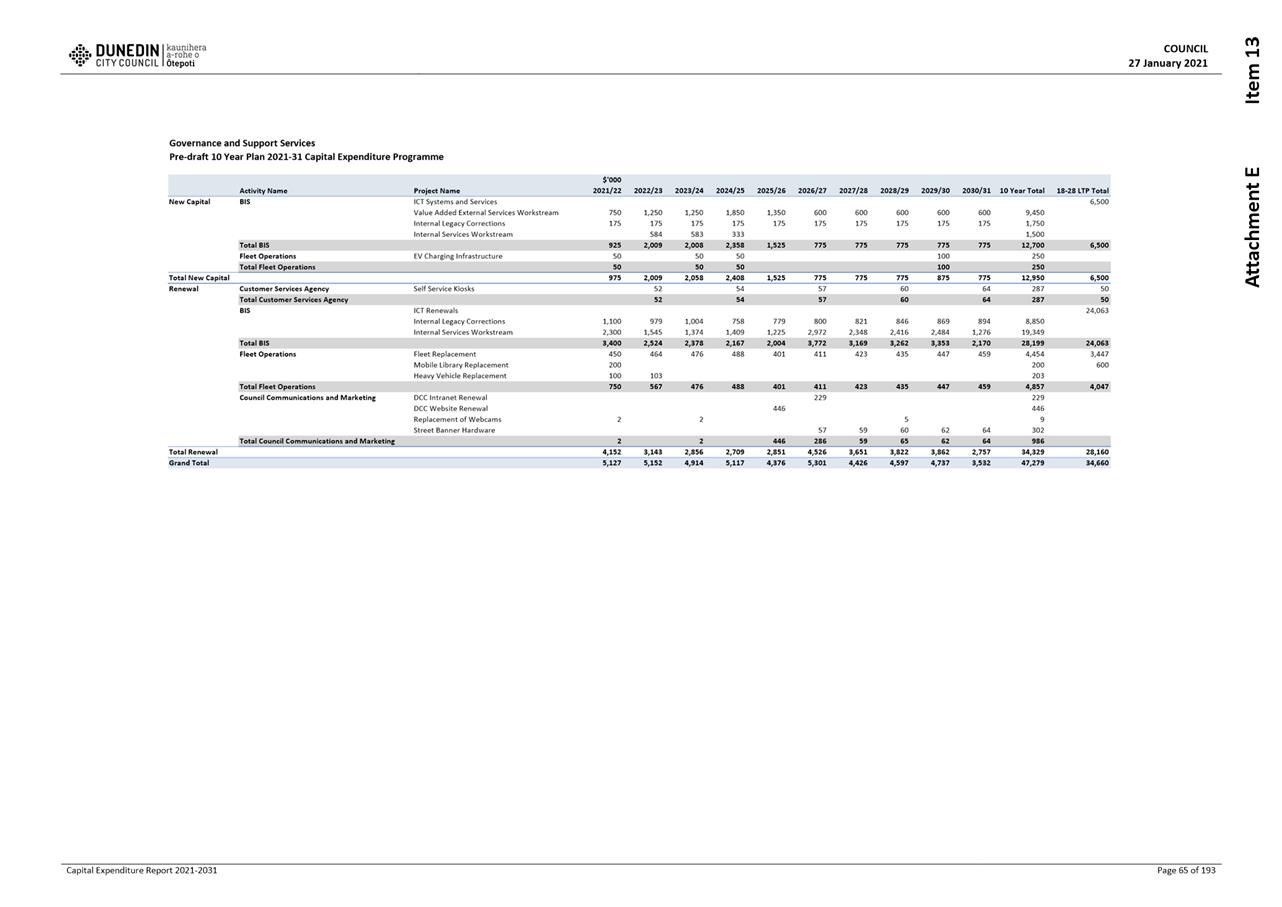

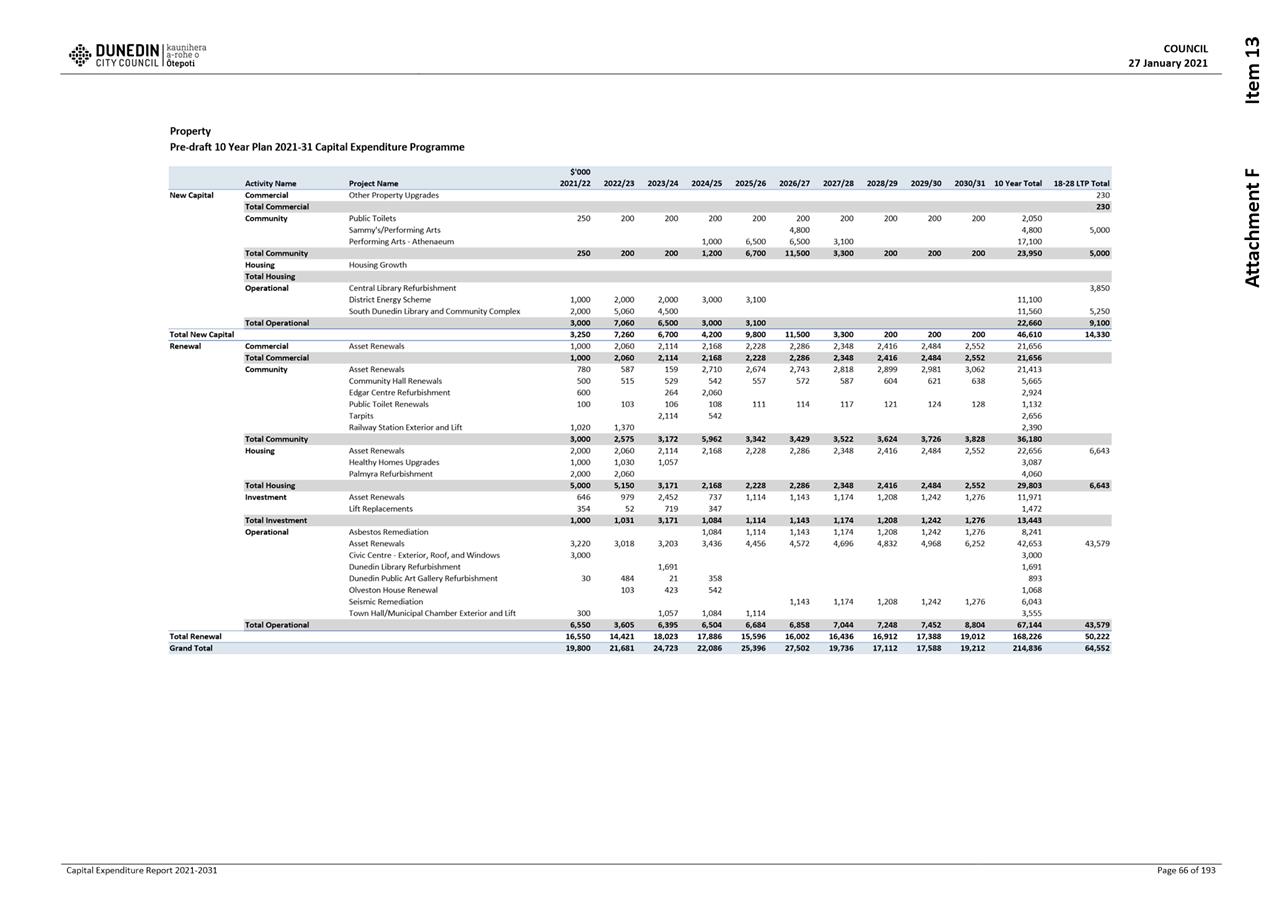

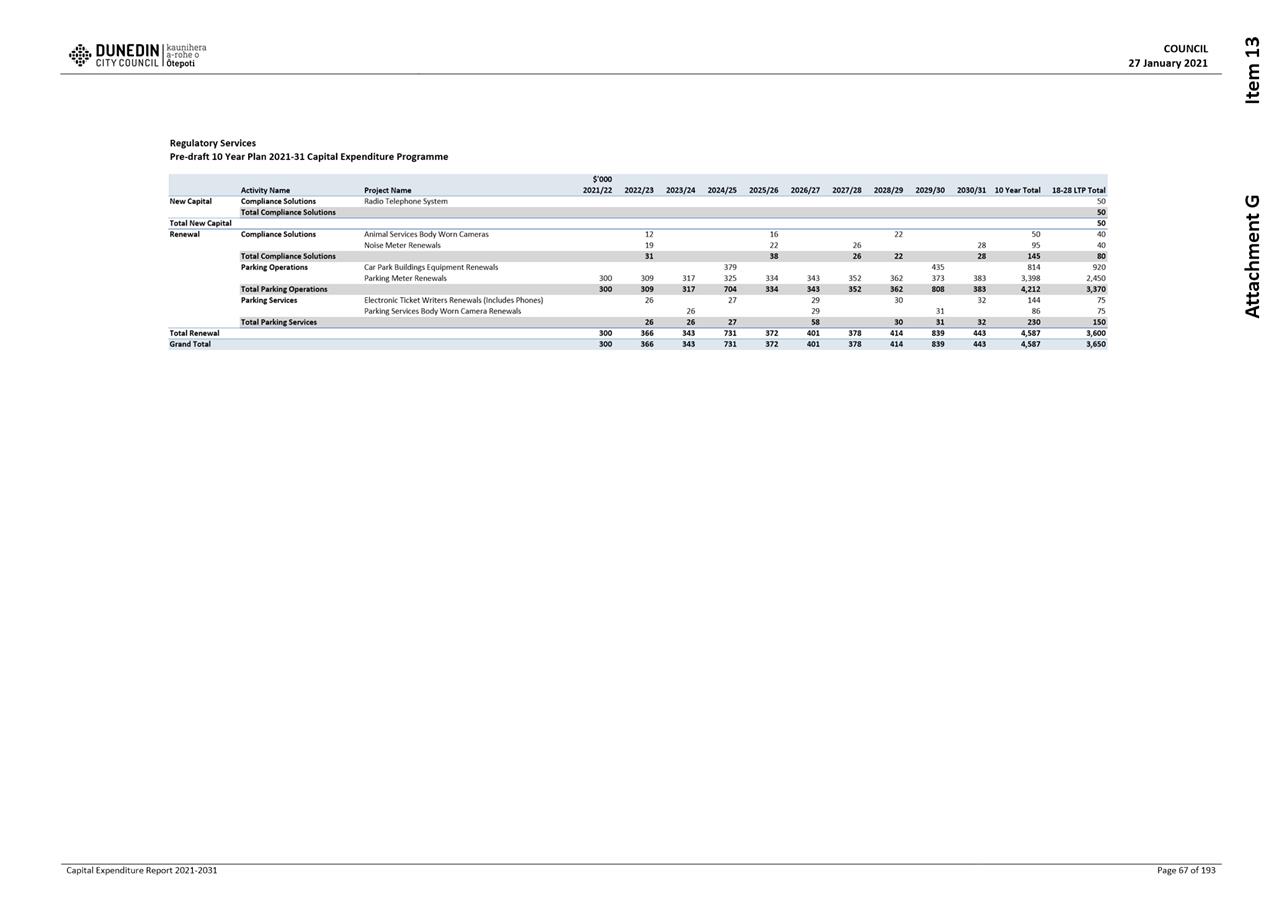

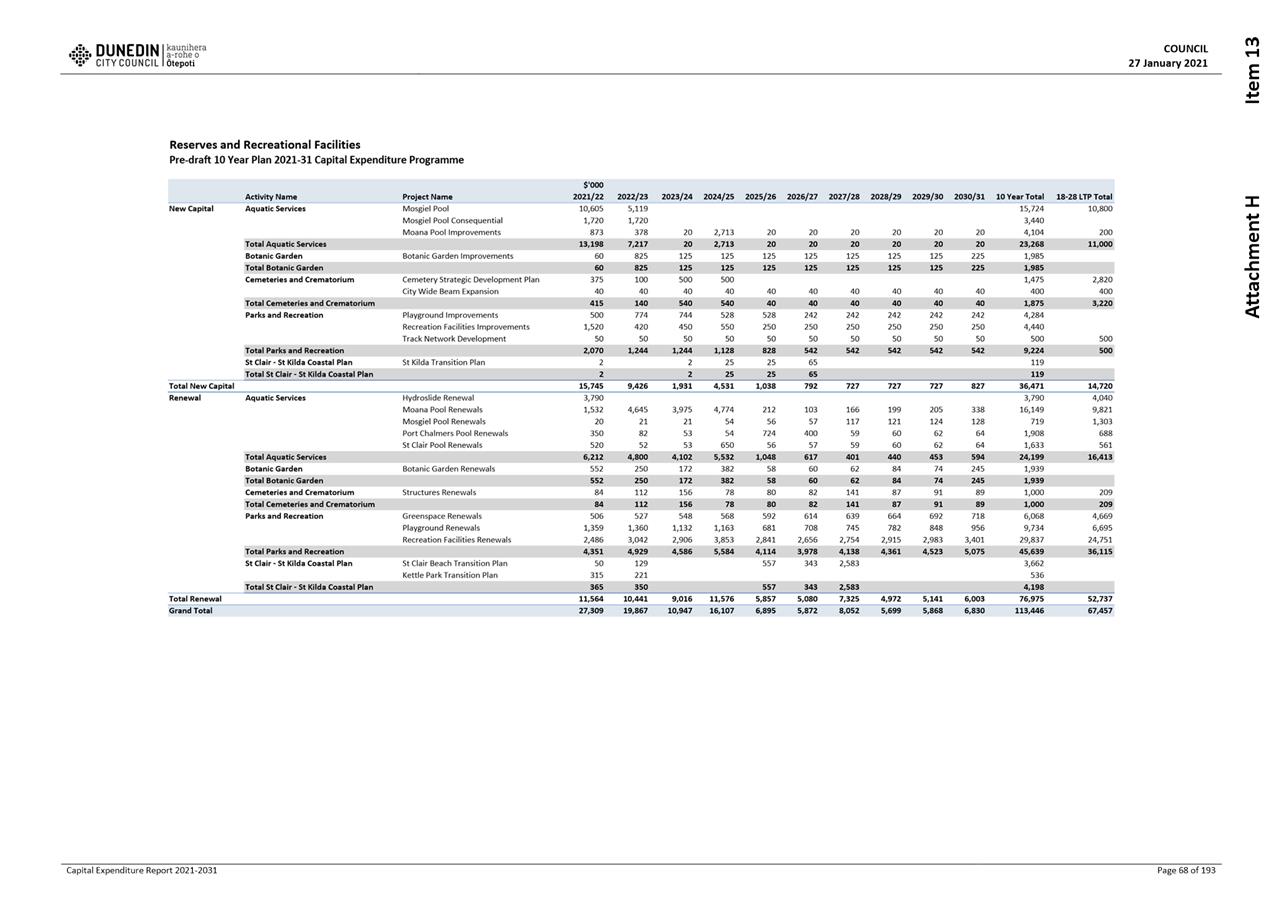

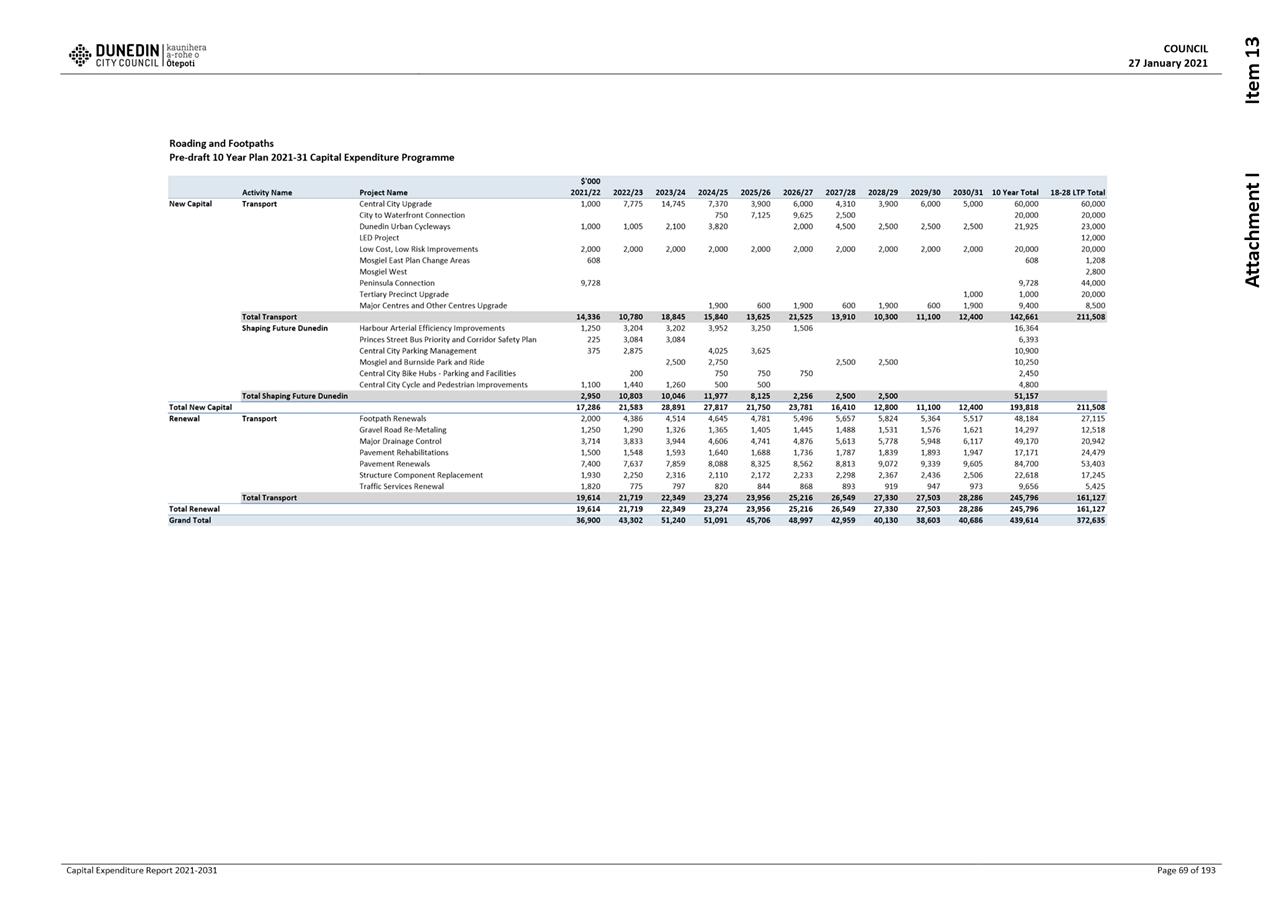

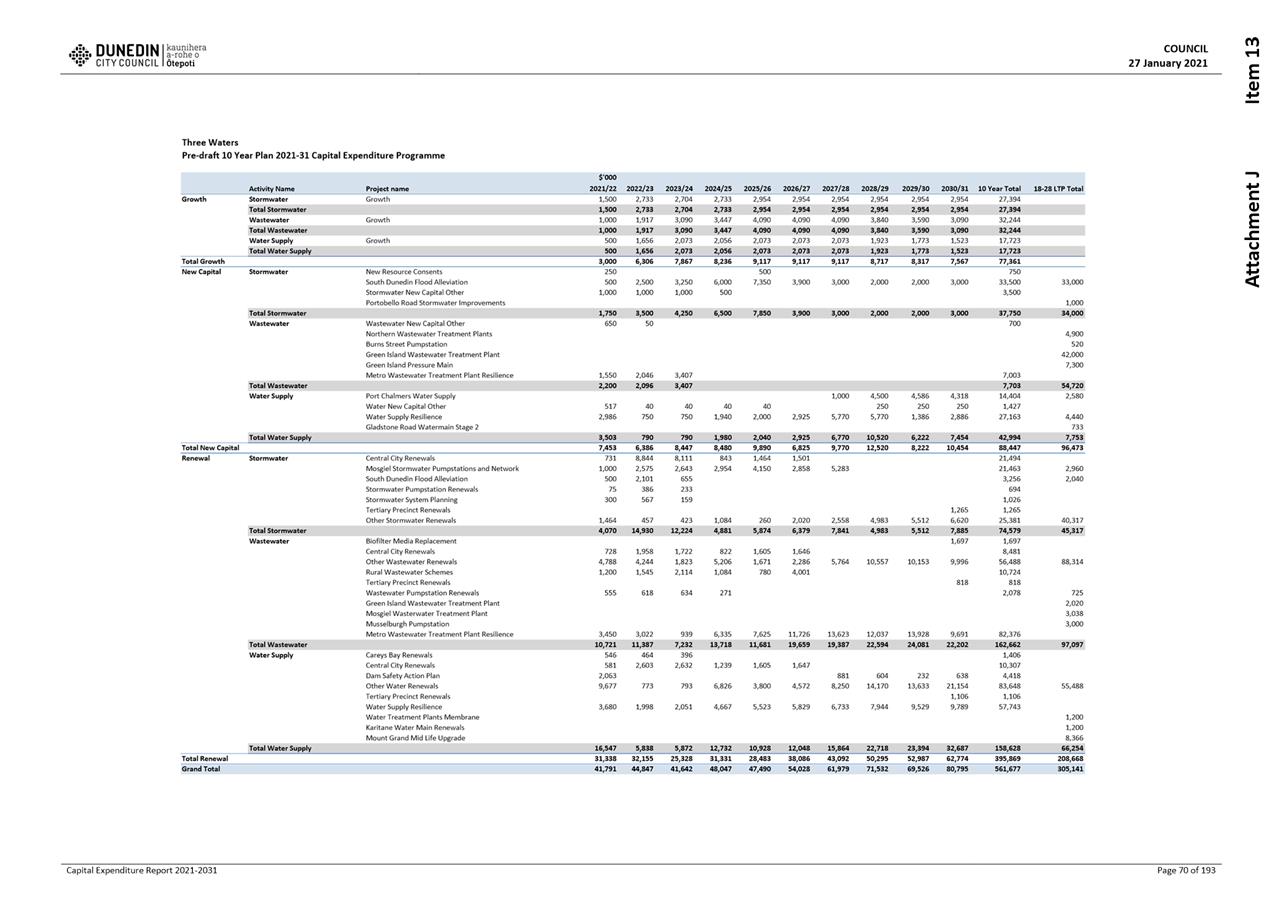

that focus on asset condition and risk. A copy of the Capital Expenditure

Report 2021-31 presented to the 27 January 2021 Council meeting is provided at

Attachment D.

23 The

Financial Strategy discusses the need to prioritise funding maintenance and

renewals, with decisions based on asset management plans, asset condition and

risks.

24 The

Consultation Document will include commentary on looking after our assets, and

that replacing aging assets is a major priority for Council. It will acknowledge

the recent water contamination issue of intermittent peaks of lead in found the

water supply at Waikouaiti, Karitane and Hawksbury Village. Ongoing

investigations may result in a reprioritisation of the timing of planned

capital works, to place higher priority on pipe replacement works.

Ability to deliver

25 The

budget overview report to the 27 January 2021 Council meeting, provided at

Attachment E, recognised the challenge of delivering on the proposed level of

capital spend.

26 The

Financial Strategy also discusses our ability to deliver on the planned capital

programme, acknowledging that the annual targets are higher than previous

achievements, and the lead time for delivery is always longer than

anticipated. The Financial Strategy notes that these risks will be

managed through improved forward planning, early contractor engagement,

innovative procurement strategies, and strong disciplines around project

management and monitoring.

Consultation Document

27 A

draft consultation document is currently being reviewed. It will be

presented to the 23 February Council meeting, in non-public, for Councillor

input. To ensure the Audit and Risk Subcommittee receive a most up to

date draft, a copy of the 23 February Council report and draft consultation

document will be circulated to the Audit and Risk Subcommittee as a non-public

supplementary agenda item by Wednesday 17 February 2021.

28 The

audited consultation document will be presented to Council on 9 March for

adoption.

29 A

list of the proposed content of the consultation document has been provided to

our auditors.

30 Consultation

questions have arisen from decisions made at the December 2020 and January 2021

Council meetings.

Compliance

31 Taituarā,

previously called SOLGM, has not provided a legal checklist for this 10 year

plan, as it has done in the past. Staff have prepared a checklist based

on the requirements in the Local Government Act, and this is being used to

ensure the content of the consultation document and the final 10 year plan will

meet all Local Government Act requirements.

32 A

copy of the most recent SOLGM health checklist is provided at Attachment F.

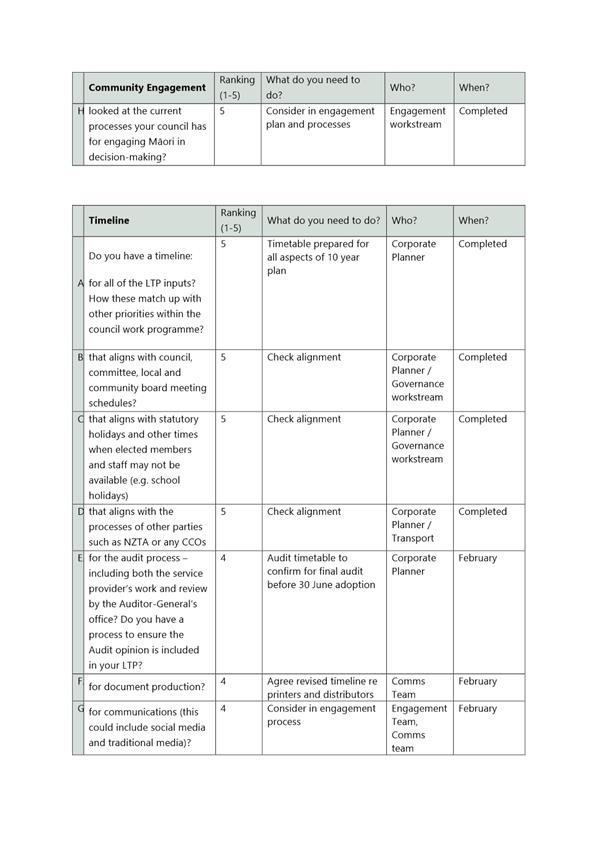

Timetable

33 A

timetable for the remainder of the process through to adoption of the final 10

year plan is provide at Attachment G.

OPTIONS

34 As

this is an update report, there are no options.

NEXT STEPS

35 An

update report will be provided to the Audit and Risk Subcommittee at its next

meeting on

7 April 2021.

Signatories

|

Author:

|

Sharon Bodeker - Corporate Planner

|

|

Authoriser:

|

Gavin Logie - Acting General Manager Finance

Sandy Graham - Chief Executive Officer

|

Attachments

|

|

Title

|

Page

|

|

⇩a

|

Significant Forecasting

Assumptions

|

50

|

|

⇩b

|

Financial Strategy

|

63

|

|

⇩c

|

Infrastructure Strategy

|

75

|

|

⇩d

|

Capital Expenditure

Report

|

148

|

|

⇩e

|

10 Year Plan Overview

Report

|

181

|

|

⇩f

|

SOLGM Health Checklist

|

191

|

|

⇩g

|

Timetable

|

197

|