Notice of Meeting:

I hereby give notice that an ordinary meeting of the Audit

and Risk Subcommittee will be held on:

Date: Wednesday

4 December 2024

Time: 2.00

pm

Venue: Council

Chamber, Dunedin Public Art Gallery, The Octagon, Dunedin

Sandy Graham

Audit and Risk Subcommittee

PUBLIC AGENDA

|

Chairperson

|

Warren Allen

|

|

|

Deputy Chairperson

|

Janet Copeland

|

|

|

Members

|

Cr Christine Garey

|

Cr Cherry Lucas

|

|

|

Mayor Jules Radich

|

Cr Lee Vandervis

|

Senior Officer Carolyn

Allan, Chief Financial Officer

Governance Support Officer Wendy

Collard

Wendy Collard

Governance Support Officer

Telephone: 03 477 4000

Wendy.Collard@dcc.govt.nz

www.dunedin.govt.nz

Note: Reports

and recommendations contained in this agenda are not to be considered as

Council policy until adopted.

|

|

Audit and Risk Subcommittee

4 December 2024

|

ITEM TABLE OF CONTENTS PAGE

1 Apologies 4

2 Confirmation

of Agenda 4

3 Declaration

of Interest 5

4 Confirmation

of Minutes 10

4.1 Audit and Risk

Subcommittee meeting - 7 October 2024 10

4.2 Audit and Risk

Subcommittee meeting - 25 October 2024 21

Part

A Reports (Committee has power to decide these matters)

5 Audit

and Risk Subcommittee Work Plan 2024/2025 25

6 Audit

and Risk Subcommittee Updates Report 29

7 DCC

Policy Update Report 37

8 Health

and Safety Monthly Reporting for October 2024 138

9 Financial

Report - Period Ended 30 September 2024 158

10 Waipori

Fund - Quarter ending 30 September 2024 185

Resolution to Exclude the Public 192

|

|

Audit and Risk Subcommittee

4 December 2024

|

1 Apologies

At the close of the agenda no

apologies had been received.

2 Confirmation

of agenda

Note:

Any additions must be approved by resolution with an explanation as to why they

cannot be delayed until a future meeting.

|

|

Audit and Risk Subcommittee

4 December 2024

|

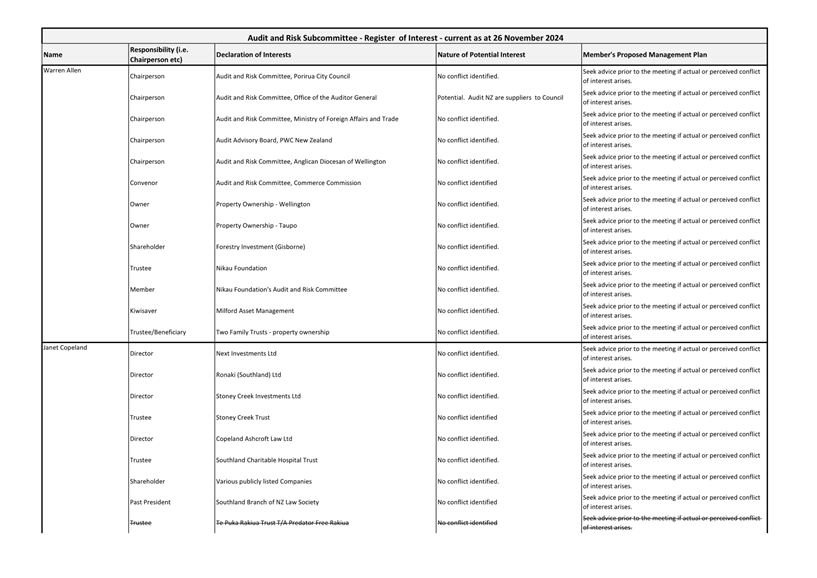

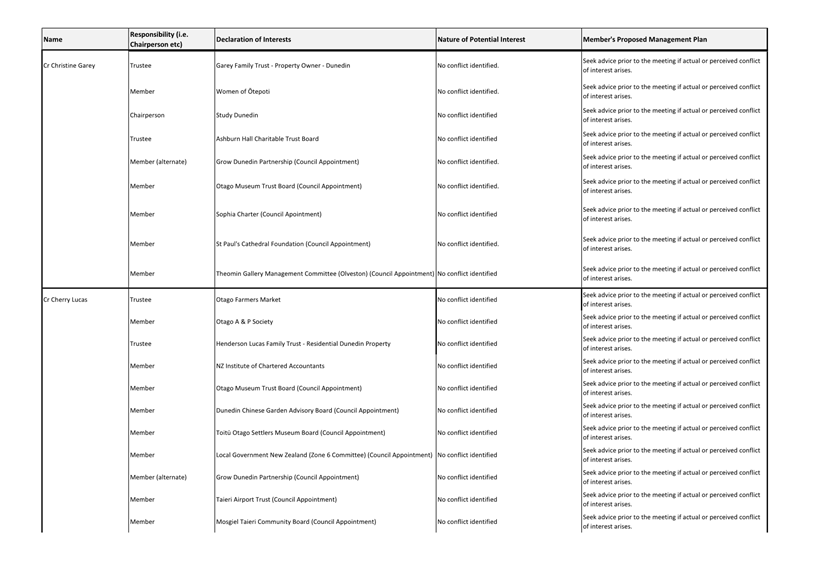

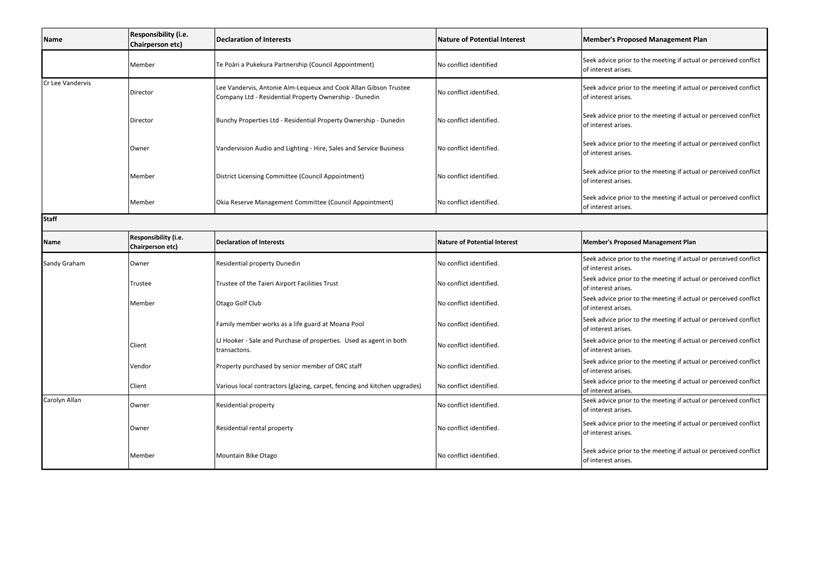

Declaration of Interest

EXECUTIVE SUMMARY

1. Members

are reminded of the need to stand aside from decision-making when a conflict

arises between their role as an elected or independent representative and any

private or other external interest they might have.

2. Elected

and Independent members are reminded to update their register

of interests as soon as practicable, including amending the register at this

meeting if necessary.

RECOMMENDATIONS

That the Committee:

a) Notes/Amends if

necessary the Elected or Independent Members' Interest Register attached as

Attachment A; and

b) Confirms/Amends the

proposed management plan for Elected or Independent Members' Interests.

Attachments

|

|

Title

|

Page

|

|

⇩a

|

Register of Interests

|

6

|

|

|

Audit and Risk Subcommittee

4 December 2024

|

|

|

Audit and Risk Subcommittee

4 December 2024

|

Confirmation

of Minutes

Audit

and Risk Subcommittee meeting - 7 October 2024

RECOMMENDATIONS

That the Subcommittee:

a) Confirms the public

part of the minutes of the Audit and Risk Subcommittee meeting held on 07

October 2024 as a correct record.

Attachments

|

|

Title

|

Page

|

|

A⇩

|

Minutes of Audit and

Risk Subcommittee meeting held on 7 October 2024

|

11

|

|

|

Audit and Risk

Subcommittee

4 December 2024

|

Audit and Risk Subcommittee

MINUTES

Minutes of

an ordinary meeting of the Audit and Risk Subcommittee held in the Council

Chamber, Dunedin Public Art Gallery, The Octagon, Dunedin on Monday 07 October

2024, commencing at 12.36 pm

PRESENT

|

Chairperson

|

Warren

Allen

|

|

|

|

|

|

|

Members

|

Cr

Christine Garey

|

Cr

Cherry Lucas

|

|

|

Mayor

Jules Radich

|

Cr Lee

Vandervis

|

|

IN ATTENDANCE

|

Sandy Graham

(Chief Executive Officer), Carolyn Allan (Chief Financial Officer), Robert

West (General Manager Corporate Services), Hayley Knight (Assurance Manager),

Rebecca Graham (Head of People and Capability), Fiona Laing (Project Advisor,

People and Capability), Rudie Tomlinson (Director, Audit New Zealand) and

Monique Kruger (Manager, Audit New Zealand), Cr Sophie Barker.

|

Governance Support Officer Lauren Riddle

|

1 Apologies

|

|

|

Moved (Warren Allen/Cr Cherry Lucas):

That the

Subcommittee:

Accepts

the apologies from Janet Copeland (for absence)

and Mayor Jules Radich (for lateness)

Motion carried

|

|

2 Confirmation

of agenda

|

|

|

Warren Allen advised that Rudie Tomlinson

and Monique Kruger from Audit NZ would be in attendance to provide an update

on progress of the audit of the Annual Report financial statements.

The Chair also advised to accommodate

staff attendance that items 5-7 would be taken in the order of item 7,5 item

and item 6.

|

|

|

Moved (Warren Allen/Cr Cherry Lucas):

That the

Subcommittee:

Confirms the agenda with the following alteration:

Item 7 –

DCC Policy Update Report to be taken before Item 5 – Audit and Risk

Subcommittee Workplan 2024/2025

Motion

carried

|

3 Declarations

of interest

Members were reminded of the need to stand aside from decision-making

when a conflict arose between their role as an elected representative and any

private or other external interest they might have.

|

|

Moved (Warren Allen/Cr Cherry Lucas):

That the

Subcommittee:

a) Notes the Elected or Independent Members' Interest Register and

b) Confirms the proposed management plan for

Elected or Independent Members' Interests.

Motion

carried

|

4 Confirmation

of Minutes

|

4.1 Audit

and Risk Subcommittee meeting - 4 July 2024

|

|

|

Moved (Warren Allen/Cr Christine Garey):

That the

Subcommittee:

Confirms the public part of the minutes of the

Audit and Risk Subcommittee meeting held on 04 July 2024 as a correct record.

Motion carried (AR/2024/025)

|

Part

A Reports

|

7 DCC

Policy Update Report

|

|

|

A report

from provided an update on DCC policies as identified in the Audit and

Risk Subcommittee (ARS) Workplan and ongoing audit and business improvement

activities.

The Chief

Financial Officer (Carolyn Allan) and the Assurance Manager (Hayley Knight)

spoke to the report and responded to questions on the policies contained in

the report.

Members provided feedback on the policy

updates, including: Legislative Compliance,

Internal Audit, Koha, Risk Management, Child Protection, and Treasury Risk

Management.

Internal Audit

Following discussion on review periods

for current contracts, the Chair (Warren Allen) requested that staff review

the policy and procedures in place for the Procurement Policy and provide a

list of current contracts .

Koha Policy

Approval Process for giving koha (clause

5.16) - Following discussion members agreed for clauses b, c and d to remain

in the policy.

Ms Knight confirmed a copy of the Koha

Policy guidelines would be circulated to elected members and be provided as

an attachment to the Koha Policy.

The Subcommittee requested that the Gift

and Hospitality register be presented to the Audit and Risk Subcommittee in

addition to the Executive Leadership Team.

Child Protection Policy

The Project Advisor – People &

Capability (Fiona Laing ) and Head of People and Capability (Rebecca Graham)

spoke to report and responded to questions.

Mayor Jules Radich entered the meeting at

1:36pm.

Treasury Risk Management Policy

Ms Knight spoke to Treasury Risk

Management Policy and the feedback provided.

Following discussion on preferential

rates to Council and interest rates for DCC Group Companies, the Chair

requested an update be provided to a future meeting

|

|

|

Moved (Warren

Allen/Cr Cherry Lucas):

That the

Subcommittee:

a) Notes the Policy Update Report – October 2024.

b) Provides feedback on the updated Legislative Compliance

Policy.

c) Provides feedback on the updated Internal Audit Policy.

d) Provides feedback on the updated Risk Management Policy.

e) Provides feedback on the updated Koha Policy.

f) Provides feedback on the updated Child Protection Policy.

g) Provides feedback on the current Treasury Risk Management

Policy.

h) Notes the Contract Management Framework.

Motion carried (AR/2024/026)

|

|

5 Audit

and Risk Subcommittee Work Plan 2024/2025

|

|

|

A report

from Civic provided a copy of the Audit and Risk Subcommittee Work Plan for

2024/2025 which aligned with work programmes scheduling and decision making.

The

Chief Financial Officer (Carolyn Allan) spoke to the report and responded to

questions.

|

|

|

Moved (Warren Allen/Cr Cherry Lucas):

That the

Subcommittee:

Notes the Audit and Risk Subcommittee Work

Plan for 2024/2025

Motion carried (AR/2024/027)

|

|

6 Audit

and Risk Subcommittee Updates Report

|

|

|

A report

from Finance provided updates on the progress of various sundry matters that

have been noted by the Subcommittee.

The Chief

Financial Officer (Carolyn Allan) spoke to the report and responded to

questions.

Warren Allen

(Chairperson) requested that the Water Services Delivery Plan (WSDP) be

provided to the subcommittee, and that the Auditor

General’s report on the 2023-24 year be

provided to all elected members, as a useful “snapshot”

of the sectors and indicates the challenges faced by all Councils.

|

|

|

Moved (Warren Allen/Cr Cherry Lucas):

That the

Subcommittee:

Notes the Audit and Risk Subcommittee Updates

Report.

Motion carried (AR/2024/028)

|

Audit NZ

Rudie Tomlinson and Monique Kruger(Audit

NZ) joined the meeting to provide an update on the audit of the Annual

Report financial statements. A review of the asset valuations provided in

the Beca report of 10 October was being undertaken.

Rudie Tomlinson and Monique Kruger left the

meeting at 2:17pm.

|

8 Financial

Report - Period Ended 30 June 2024

|

|

|

A report

from Finance provided the provisional financial results for the period ended

30 June 2024 and the financial position as at that date which were presented

to the Finance and Council Controlled Organisations Committee held on

Wednesday, 7 August 2024.

The Chief Financial Officer (Carolyn

Allan) spoke to the report and responded to questions.

|

|

|

Moved (Warren Allen/Cr Lee Vandervis):

That the

Subcommittee:

a) Notes the Financial Performance for the period ended 30 June

2024 and the Financial Position as at that date.

b) Notes the year 30 June result is subject to final adjustments

and external audit, conducted by Audit New Zealand.

Motion carried (AR/2024/029)

|

|

9 Waipori

Fund - Quarter ending 30 June 2024

|

|

|

A report

from Dunedin City Treasury Limited provided information on the results of the

Waipori Fund for the quarter ended 30 June 2024 which was presented to the

Finance and Council Controlled Organisation Committee meeting held on 7

August 2024.

The Chief Financial Officer (Carolyn

Allan) spoke to the report and responded to questions.

|

|

|

Moved (Mr Warren Allen/Mayor Jules

Radich):

That the

Subcommittee:

Notes the report from Dunedin City Treasury

Limited on the Waipori Fund for the quarter ended 30 June 2024.

Motion carried (AR/2024/030)

|

|

10 Financial

Report - Period ended 31 July 2024

|

|

|

A report

provided the financial results for the period ended 31 July 2024 and the

financial position as at that date which was presented to the Finance and

Council Controlled Organisations Committee meeting held on Wednesday, 18

September 2024.

The Chief Financial Officer Carolyn Allan

Spoke to the report and responded to questions.

|

|

|

Moved (Warren Allen/Cr Lee Vandervis):

That the

Subcommittee:

Notes the Financial Performance for the period

ended 31 July 2024 and the Financial Position as at that date.

Motion carried (AR/2024/031)

|

|

|

|

|

|

Moved (Warren Allen/Mayor Jules Radich):

That the

Subcommittee:

Adjourn

the meeting for five minutes

Motion

carried

|

|

|

|

Cr Lee Vandervis left the meeting at

2:35pm.

The meeting adjourned at 2.35pm and. The

meeting recommenced at 2:40pm.

|

11 Health

and Safety Monthly Reporting for August 2024

|

|

|

The report

from Health and Safety provided the monthly Health, Safety and Wellbeing

report for August 2024 for the Subcommittee information and included a copy

of the health and safety structure of the Council for noting.

The Manager, Health and Safety (Jane

Pearce) spoke to the report and responded to questions.

|

|

|

Moved (Warren Allen/Mayor Jules Radich):

That the

Subcommittee:

a) Notes the monthly Health, Safety and Wellbeing report for August

2024.

b) Notes the health and safety structure of the organisation.

Motion carried (AR/2024/032)

|

|

Resolution

to Exclude the Public

|

|

Moved (Warren Allen/Cr Christine Garey):

That the

Subcommittee:

Pursuant to the

provisions of the Local Government Official Information and Meetings Act

1987, exclude the public from the following part of the proceedings of this

meeting namely:

|

General

subject of the matter to be considered

|

Reasons for passing this resolution

in relation to each matter

|

Ground(s) under section 48(1) for

the passing of this resolution

|

Reason for Confidentiality

|

|

C1 Audit and Risk Subcommittee meeting - 4 July 2024 -

Public Excluded

|

S7(2)(i)

The

withholding of the information is necessary to enable the local authority

to carry on, without prejudice or disadvantage, negotiations (including

commercial and industrial negotiations).

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or

could be compelled to provide under the authority of any enactment, where

the making available of the information would be likely to prejudice the supply

of similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

S7(2)(b)(i)

The

withholding of the information is necessary to protect information where

the making available of the information would disclose a trade secret.

S7(2)(h)

The

withholding of the information is necessary to enable the local authority

to carry out, without prejudice or disadvantage, commercial activities.

S7(2)(b)(ii)

The

withholding of the information is necessary to protect information where

the making available of the information would be likely unreasonably to

prejudice the commercial position of the person who supplied or who is the

subject of the information.

S7(2)(a)

The withholding

of the information is necessary to protect the privacy of natural persons,

including that of a deceased person.

|

.

|

|

|

C2 Audit and Risk Subcommittee Updates Report

|

S7(2)(h)

The

withholding of the information is necessary to enable the local authority

to carry out, without prejudice or disadvantage, commercial activities.

|

S48(1)(a)

The

public conduct of the part of the meeting would be likely to result in the

disclosure of information for which good reason for withholding exists

under section 7.

|

|

|

C3 Finance Assurance Report

|

S7(2)(h)

The

withholding of the information is necessary to enable the local authority

to carry out, without prejudice or disadvantage, commercial activities.

|

S48(1)(a)

The

public conduct of the part of the meeting would be likely to result in the

disclosure of information for which good reason for withholding exists

under section 7.

|

The

information in this report is commercially sensitive..

|

|

C4 DCC Internal Audit Actions Update

|

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or

could be compelled to provide under the authority of any enactment, where

the making available of the information would be likely to prejudice the

supply of similar information or information from the same source and it is

in the public interest that such information should continue to be

supplied.

|

S48(1)(a)

The public

conduct of the part of the meeting would be likely to result in the

disclosure of information for which good reason for withholding exists

under section 7.

|

|

|

C5 Treasury Risk Management Compliance Report

|

S7(2)(h)

The

withholding of the information is necessary to enable the local authority

to carry out, without prejudice or disadvantage, commercial activities.

|

S48(1)(a)

The

public conduct of the part of the meeting would be likely to result in the

disclosure of information for which good reason for withholding exists

under section 7.

|

|

|

C6 Dunedin City Holdings Ltd - Update on Audit and Risk

Activity

|

S7(2)(b)(ii)

The

withholding of the information is necessary to protect information where

the making available of the information would be likely unreasonably to

prejudice the commercial position of the person who supplied or who is the

subject of the information.

|

S48(1)(a)

The

public conduct of the part of the meeting would be likely to result in the

disclosure of information for which good reason for withholding exists

under section 7.

|

|

|

C7 DCC Risk 'Deep Dive' - Fraud Risk Management

|

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to prejudice the supply

of similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

|

S48(1)(a)

The

public conduct of the part of the meeting would be likely to result in the

disclosure of information for which good reason for withholding exists

under section 7.

|

|

|

C8 Protected Disclosure Register - September 2024

|

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of

natural persons, including that of a deceased person.

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or

could be compelled to provide under the authority of any enactment, where

the making available of the information would be likely to prejudice the

supply of similar information or information from the same source and it is

in the public interest that such information should continue to be

supplied.

|

S48(1)(a)

The

public conduct of the part of the meeting would be likely to result in the

disclosure of information for which good reason for withholding exists

under section 7.

|

|

|

C9 Investigation Register - September 2024

|

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of

natural persons, including that of a deceased person.

S7(2)(c)(i)

The withholding

of the information is necessary to protect information which is subject to

an obligation of confidence or which any person has been or could be

compelled to provide under the authority of any enactment, where the making

available of the information would be likely to prejudice the supply of

similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

|

S48(1)(a)

The

public conduct of the part of the meeting would be likely to result in the

disclosure of information for which good reason for withholding exists

under section 7.

|

|

This resolution

is made in reliance on Section 48(1)(a) of the Local Government Official

Information and Meetings Act 1987, and the particular interest or interests

protected by Section 6 or Section 7 of that Act, or Section 6 or Section 7 or

Section 9 of the Official Information Act 1982, as the case may require,

which would be prejudiced by the holding of the whole or the relevant part of

the proceedings of the meeting in public are as shown above after each item.

Motion carried (AR/2024/033)

|

The meeting moved into non-public at 2:50

pm and concluded at 3.50 pm

..............................................

CHAIRPERSON

|

|

Audit and Risk Subcommittee

4 December 2024

|

Audit and Risk Subcommittee meeting - 25

October 2024

RECOMMENDATIONS

That the Subcommittee:

a) Confirms the public

part of the minutes of the Audit and Risk Subcommittee meeting held on 25

October 2024 as a correct record.

Attachments

|

|

Title

|

Page

|

|

A⇩

|

Minutes of Audit and

Risk Subcommittee meeting held on 25 October 2024

|

22

|

|

|

Audit and Risk

Subcommittee

4 December 2024

|

Audit and Risk Subcommittee

MINUTES

Minutes of an ordinary

meeting of the Audit and Risk Subcommittee held in the Council Chamber, Dunedin

Public Art Gallery, The Octagon, Dunedin on Friday 25 October 2024, commencing

at 3.30 pm

PRESENT

|

Chairperson

|

Warren Allen

|

|

|

Deputy Chairperson

|

Janet Copeland

|

|

|

Members

|

Cr Christine Garey

|

Cr Cherry Lucas

|

|

|

Mayor Jules Radich

|

Cr Lee Vandervis

|

|

IN ATTENDANCE

|

Sandy Graham (Chief Executive

Officer), Carolyn Allan (Chief Financial Officer), Bryan Staunton (Financial

Accounting Manager), Rudie Tomlinson (Director, Audit New Zealand) and

Monique Kruger (Manager, Audit New Zealand)

|

Governance Support Officer Wendy

Collard

|

1 Apologies

|

|

|

There were no apologies.

|

|

2 Confirmation

of agenda

|

|

|

Moved (Warren Allen/Mayor Jules Radich):

That the Subcommittee:

Confirms the agenda

without addition or alteration

Motion

carried (AR/2024/032)

|

1 Declarations

of interest

Members were

reminded of the need to stand aside from decision-making when a conflict arose

between their role as an elected representative and any private or other

external interest they might have.

|

|

Moved (Warren Allen/Cr Cherry Lucas):

That the Subcommittee:

a) Notes the Elected and Independent Members' Interest Register;

and

b) Confirms the proposed management plan for

Elected and Independent Members' Interests.

Motion

carried (AR/2024/033)

|

|

Resolution to Exclude the Public

|

|

Moved (Warren Allen/Janet Copeland):

That the Subcommittee:

Pursuant

to the provisions of the Local Government Official Information and Meetings

Act 1987, exclude the public from the following part of the proceedings of

this meeting namely:

|

General

subject of the matter to be considered

|

Reasons for

passing this resolution in relation to each matter

|

Ground(s) under

section 48(1) for the passing of this resolution

|

Reason for

Confidentiality

|

|

C1

Dunedin City Council Annual Report for the year ended 30 June 2024

|

S7(2)(b)(i)

The withholding of

the information is necessary to protect information where the making

available of the information would disclose a trade secret.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

This resolution is made in

reliance on Section 48(1)(a) of the Local Government Official Information and

Meetings Act 1987, and the particular interest or interests protected by

Section 6 or Section 7 of that Act, or Section 6 or Section 7 or Section 9 of

the Official Information Act 1982, as the case may require, which would be

prejudiced by the holding of the whole or the relevant part of the

proceedings of the meeting in public are as shown above after each item.

That Rudie Tomlinson and

Monique Kruger (Audit NZ) be permitted to attend the meeting, after the

public has been excluded, because of their knowledge of Item C1. This

knowledge, which would been of assistance in relation to the matters

discussed, was relevant because they would be reporting on the item under

consideration.

Motion

carried (AR/2024/034)

|

The meeting moved to non-public at 3.38 pm and concluded at

4.30 pm.

..............................................

CHAIRPERSON

|

|

Audit and Risk Subcommittee

4 December 2024

|

Part

A Reports

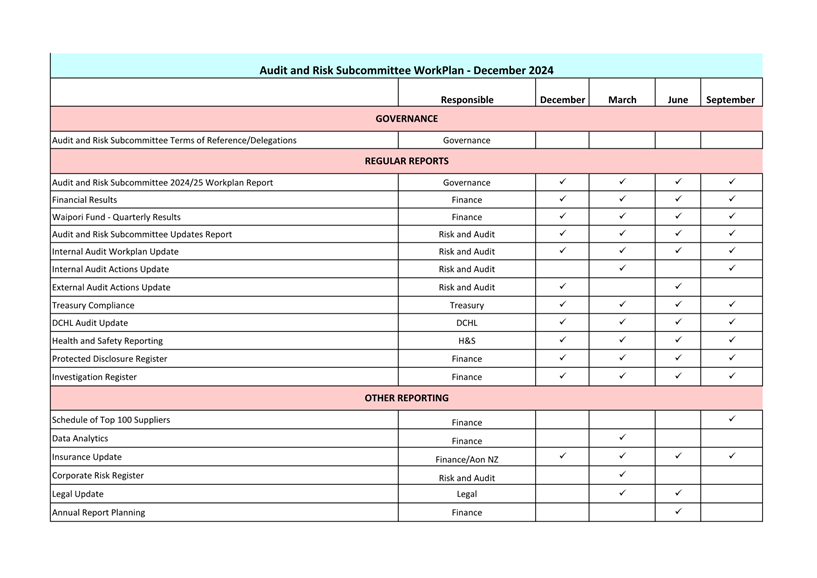

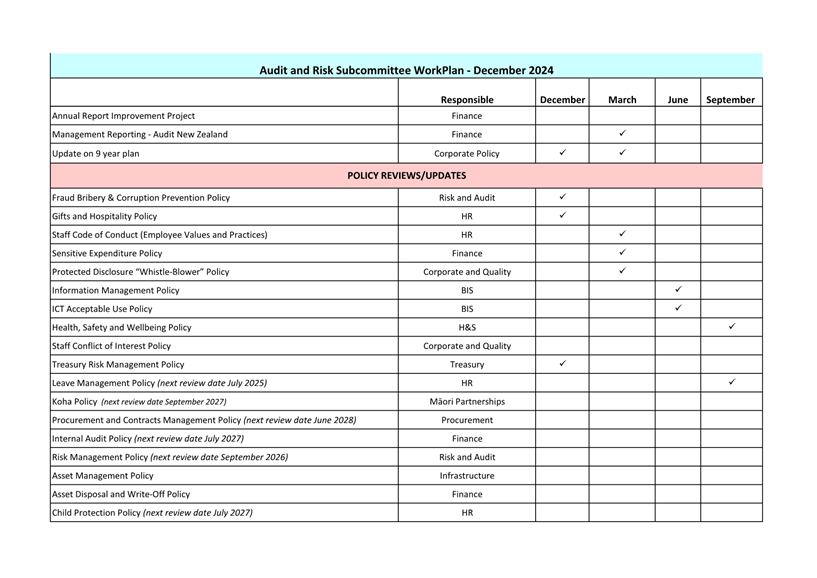

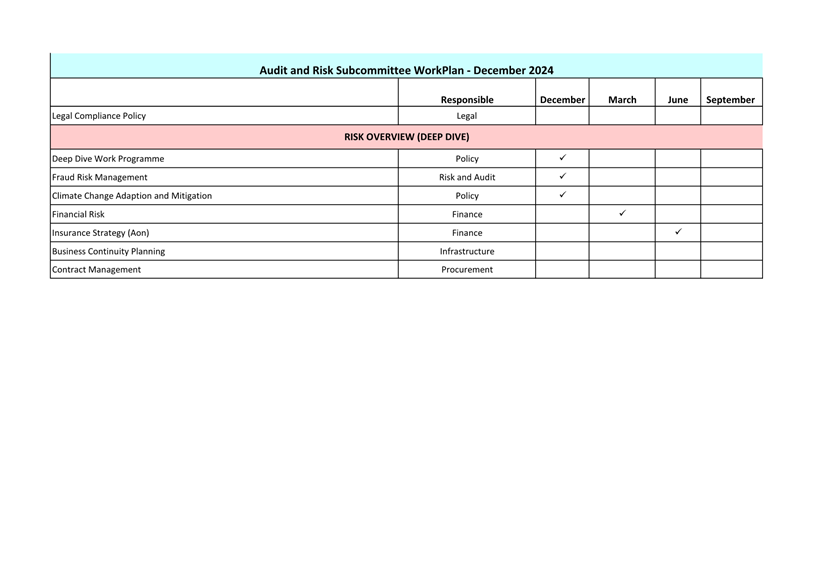

Audit and Risk Subcommittee Work Plan 2024/2025

Department: Civic

EXECUTIVE SUMMARY

1 This

report provides a copy of the Audit and Risk Subcommittee Work Plan 2024/2025

which has been aligned with work programme scheduling and decision making.

2 It

should be noted that the items without ticks shown have not been scheduled for

action.

3 As

this is an administrative report only, the Summary of Consideration is not

required.

RECOMMENDATIONS

That the Subcommittee:

a) Notes the Audit and

Risk Subcommittee Work Plan for 2024/2025

Signatories

|

Author:

|

Wendy Collard - Governance Support Officer

|

|

Authoriser:

|

Carolyn Allan - Chief Financial Officer

|

Attachments

|

|

Title

|

Page

|

|

⇩a

|

Work Plan - December

2024

|

26

|

|

|

Audit and Risk Subcommittee

4 December 2024

|

|

|

Audit and Risk Subcommittee

4 December 2024

|

Audit and Risk Subcommittee Updates Report

Department: Finance

EXECUTIVE SUMMARY

1 This

report provides updates on the progress of various sundry matters that have

been noted by the Subcommittee.

|

RECOMMENDATIONS

That the Subcommittee:

a) Notes the Audit and

Risk Subcommittee Updates Report.

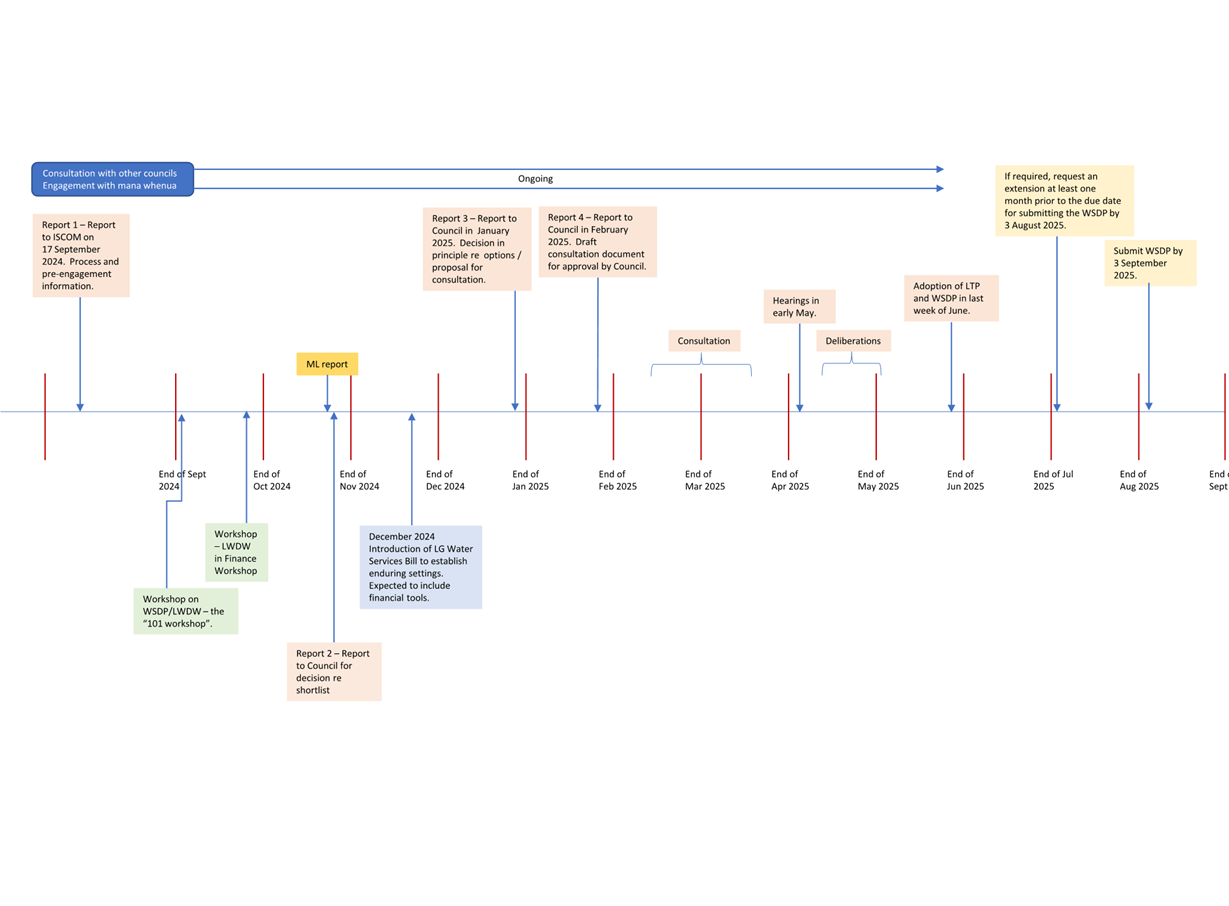

b) Notes the Timeline

for Water Services Delivery Plan (Attachment A).

|

DISCUSSION

Insurance

Renewal 2024/25 Financial Year

2 The

liability programme has now been fully renewed with effect from 1 November 2024:

· Primary Public

Liability

· Professional

indemnity

· Employers

Liability

· Statutory

Liability

· Excess Public

Liability and Professional Indemnity

3 Since

the update to the National Seismic Hazard Model, Council has work underway

modelling below-ground assets to understand what the insurance loss limits

should look like. This modelling has now been completed and Council is

expecting a report back on this prior to the end of the year. While the

outcome isn’t yet known, initial indications are that no significant

changes will be required.

4 Additional

pieces of additional work were also underway, requiring a post-renewal

adjustment to cater for changes. These included above ground property

valuations, infrastructure/below ground valuations and the Business

Interruption review.

2023/24

Annual Report

5 The

Annual Report was adopted by Council on 31st October with an

unqualified audit opinion issued. The Annual Report was published on the

DCC website on 11th November 2024.

6 The

Summary Annual Report has been prepared in draft form and is currently being audited.

The audit is due to be completed before Friday 29th November so that

the Summary Annual Report can be published online within one month of the

Annual Report adoption date as required by the Local Government Act 2002.

7 The

draft management report has been provided by Audit NZ for review and management

comments.

9 Year Plan

8 Work

is progressing on developing budgets, updating policies and strategies, writing

reports and planning an engagement programme.

9 The

asset management plans for 3 Waters and Transport and the draft Infrastructure

Strategy have been provided to Audit NZ.

10 Timing of

work is challenging. Along with the development of the Plan, other

priorities include the development of a Water Services Delivery Plan.

11 An extensive series of workshops and briefings with

Councillors is due to be completed next week.

12 The December 2024 Council meeting will be considering a

number of 9 year plan reports.

13 A 9 year plan Council meeting is scheduled for late January,

where activities and budgets are to be presented to Council for its

consideration. Immediately following this, the draft consultation document

needs to be provided to Audit NZ.

14 A high

level timetable for the 9 year plan project is as follows:

|

Timing

|

Task

|

|

To December 2024

|

Various reports for

approval as the 9 year plan develops, including:

· Policy updates

· Engagement plans

· Significant forecasting assumptions

· Option reports

Workshops on key

components of the Plan.

|

|

December 2024 – early

February 2025

|

Develop Consultation

Document

|

|

Late January 2025

|

Audit commences

Council meeting to

consider:

· Budgets

· Option reports

· Financial and Infrastructure strategies

|

|

February 2025

|

Council approval of

consultation document

|

|

March / April 2025

|

Engagement and

submission period

|

|

May 2025

|

Hearings and

deliberations

|

|

June 2025

|

Adoption of the 9 year

plan

|

Local Water

Done Well

New direction for water services delivery

15 In February

2024 the Government announced the three-stage process and timetable for the

implementation of the Local Water Done Well programme including:

a) First

Stage (now completed) – Repeal of current legislation relating to water

service entities resulting in the passing of the Water Services Acts Repeal Act

2024 on 16 February 2024 which included:

i. Repealing

the Water Services Entities Act 2022, Water Services Legislation Act 2023 and

Water Services Economic Efficiency and Consumer Protection Act 2023.

ii. Providing

support options to help councils complete and include water services in their

2024-34 long-term plans.

iii. An

option to defer the LTP by 12 months and have an enhanced Annual Plan for the

2024/25 year.

b) Second

Stage has now been implemented with the Local Government (Water Services

Preliminary Arrangements) Act 2024 becoming law on 2 September 2024 providing

the following key points:

i. Council

must prepare a one-off Water Service Delivery Plan (WSDP) by 3 September 2025.

A timeline for the preparation of the WSDP has been provided as Attachment A.

ii. Foundational

information disclosure will be provided through the WSDP to lay the groundwork

for comprehensive economic regulation.

iii. Introduces

an alternative streamlined consultation and decision-making process (as opposed

to the standard requirements under Part 6 of the Local Government Act 2002 (LGA

2002)) that:

· may be used for

consulting and decision making on establishing, joining or amending a water

services council-controlled organisation (WSCCO) (or are deciding whether or

not to do so), or a joint local government arrangement (made under section 137

of the LGA 2002) (or are deciding whether or not to do so); and

· must be used for

consulting or decision making in relation to an anticipated or proposed model

or arrangement for delivering water services; and other parts of the WSDP if

consulted on.

c) Third

Stage – Establish enduring settings by introducing the Local Government

Water Services Bill in December 2024 (with anticipated enactment) in mid-2025

to:

i. Set

long-term requirements for financial sustainability.

ii. Provide

a range of structural and financing tools.

iii. Ensure

regulatory regime is efficient, effective, and fit for purpose.

iv. Provide

for a complete economic regulation regime.

v. Establish

regulatory backstop powers.

vi. Refine

water service delivery system settings.

16 Guidance on

the future water services delivery system was released by the DIA on 8 August 2024,

and further on the WSDP on 3 September 2024. Much of this guidance was

based on the LWDW Cabinet decisions announced by the Minister of Local

Government in August 2024.

17 Staff are

continuing to undertake further analysis on shortlisted delivery models ((in-house delivery, single CCO and regional multi-council entity)

and any optional add-on(s) subject to further analysis in accordance with the

Council resolution dated 26 November 2024.

Signatories

|

Author:

|

Hayley Knight - Assurance Manager

|

|

Authoriser:

|

Carolyn Allan - Chief Financial Officer

|

Attachments

|

|

Title

|

Page

|

|

⇩a

|

Timeline for Water

Services Delivery Plan

|

35

|

|

SUMMARY OF CONSIDERATIONS

|

|

Fit with purpose of Local Government

This report provides an update on the progress made by

Council to deliver upon the activities identified by the Audit and Risk

Subcommittee, which is a regulatory function and considered good quality and

cost effective.

|

|

Fit with strategic framework

|

|

Contributes

|

Detracts

|

Not applicable

|

|

Social Wellbeing Strategy

|

|

☐

|

☐

|

|

Economic Development Strategy

|

☒

|

☐

|

☐

|

|

Environment Strategy

|

☒

|

☐

|

☐

|

|

Arts and Culture Strategy

|

☒

|

☐

|

☐

|

|

3 Waters Strategy

|

☒

|

☐

|

☐

|

|

Spatial Plan

|

☒

|

☐

|

☐

|

|

Integrated Transport Strategy

|

☒

|

☐

|

☐

|

|

Parks and Recreation Strategy

|

☒

|

☐

|

☐

|

|

Other strategic projects/policies/plans

|

☐

|

☐

|

☒

|

The work of the Audit and Risk Subcommittee seeks to

underpin the ongoing critical review and improvement of Council business

activities, governance mechanisms and support the realisation of its

strategic objectives.

|

|

Māori Impact Statement

There are no known impacts for Māori.

|

|

Sustainability

There are no implications for sustainability.

|

|

LTP/Annual Plan / Financial Strategy /Infrastructure

Strategy

There are no known implications.

|

|

Financial considerations

No financial implications have been identified.

|

|

Significance

This report is considered low in terms of the

Council’s Significance and Engagement Policy.

|

|

Engagement – external

No external engagement has been undertaken.

|

|

Engagement - internal

Activities noted herein include cross Council engagement

and collaboration.

|

|

Risks: Legal / Health and Safety etc.

No risks have been identified.

|

|

Conflict of Interest

No conflicts of interest have been identified.

|

|

Community Boards

There are no known implications for the Community Boards.

|

|

|

Audit and Risk Subcommittee

4 December 2024

|

|

|

Audit and Risk Subcommittee

4 December 2024

|

DCC Policy Update Report

Department: Finance

EXECUTIVE SUMMARY

1 This

report provides an update on DCC policies as identified in the Audit and Risk

Subcommittee (ARS) Workplan and ongoing audit and business improvement

activities.

RECOMMENDATIONS

That the Subcommittee:

a) Notes the Policy

Update Report – December 2024.

b) Endorse approval of

the Treasury Risk Management Policy (Clean: Attachment A, Track Changes:

Attachment B).

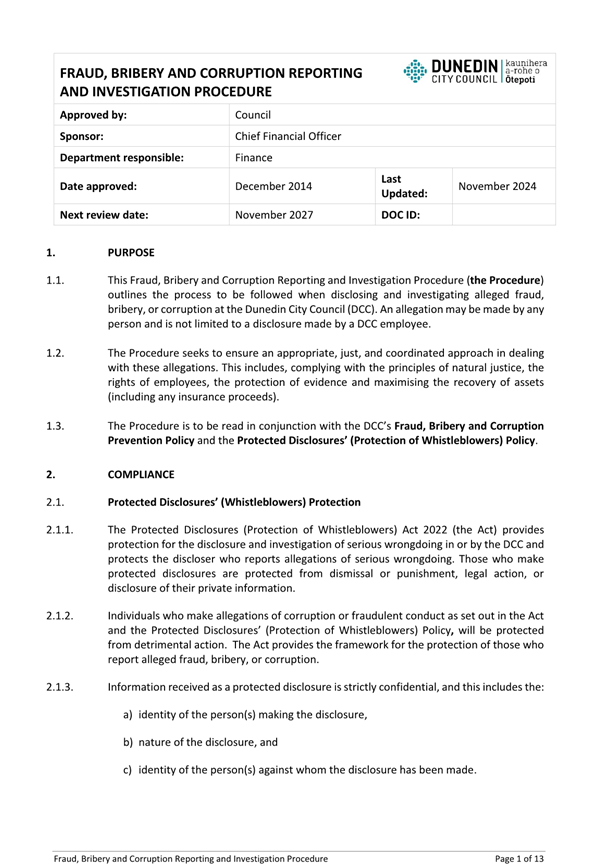

c) Approve the Fraud,

Bribery and Corruption Prevention Policy (Clean: Attachment C, Track Changes:

Attachment D).

d) Note the Fraud,

Bribery and Corruption Investigation procedures (Attachment E).

e) Provide feedback on

the Gifts and Hospitality Policy (Clean: Attachment F, Track Changes:

Attachment G).

f) Notes the Gifts and

Hospitality Procedures (Attachment H).

g) Approve the Policy

Review Schedule (Attachment I).

h) Notes the Policy

Review Process for the Audit and Risk Subcommittee.

DISCUSSION

2 At

the 7 October 2024 Audit and Risk Subcommittee meeting there was a

question as to why elected members were excluded from the Child Protection

Policy. The answer is as follows:

a) Following

advice from in-house legal, elected members were specifically excluded from the

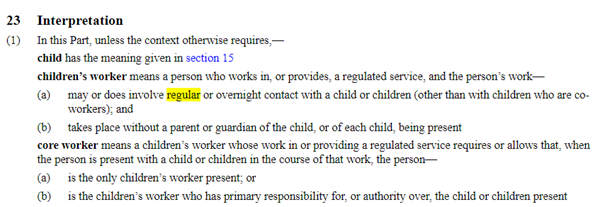

Child protection Policy, as they do not meet the definition of a

Children’s Worker from the Children’s Act 2014.

3 The

following policies are undergoing review:

a) ICT

Acceptable Use Policy

b) Information

Management Policy

c) Asset

Management Policy

d) Asset

Disposal and Write-Off Policy

e) Staff Code

of Conduct

f) Sensitive

Expenditure Policy

4 After

the review process, updated copies of DCC policies will be provided to the

Subcommittee for either feedback or noting.

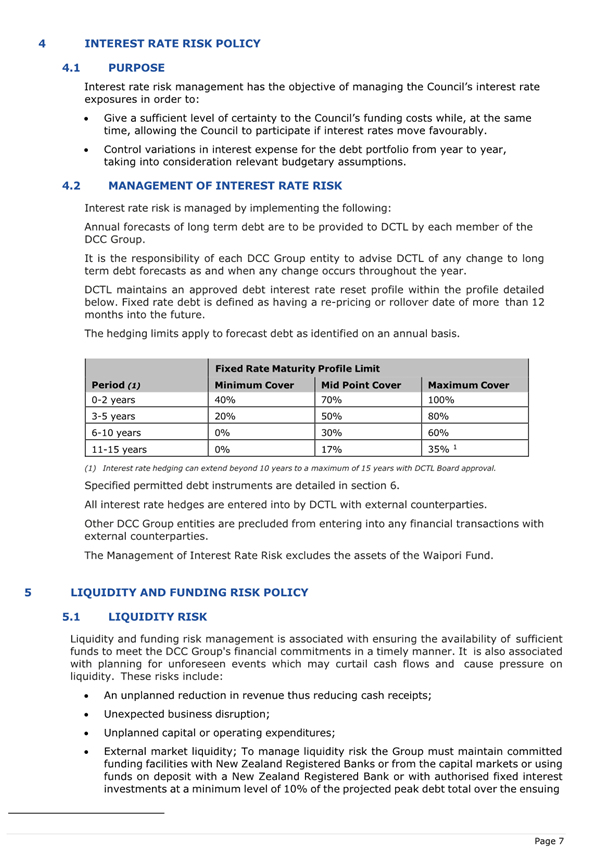

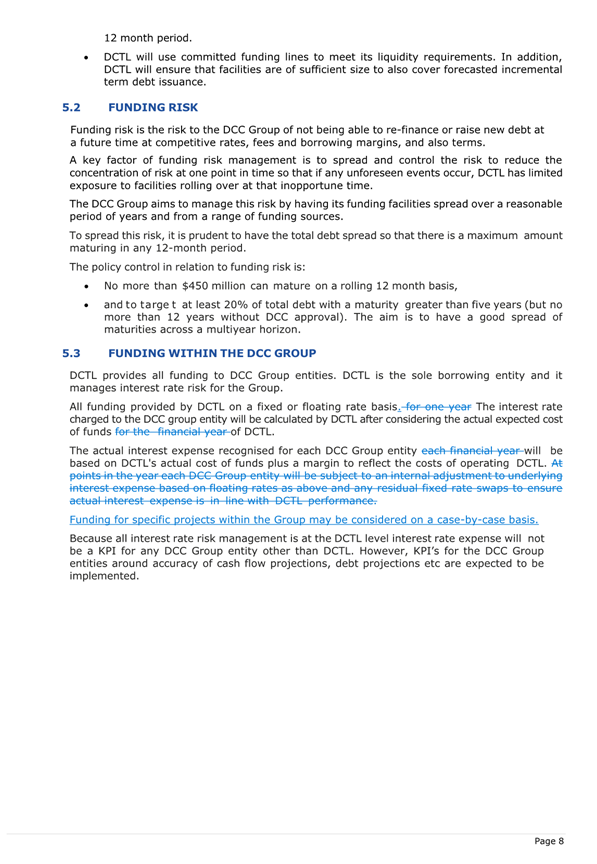

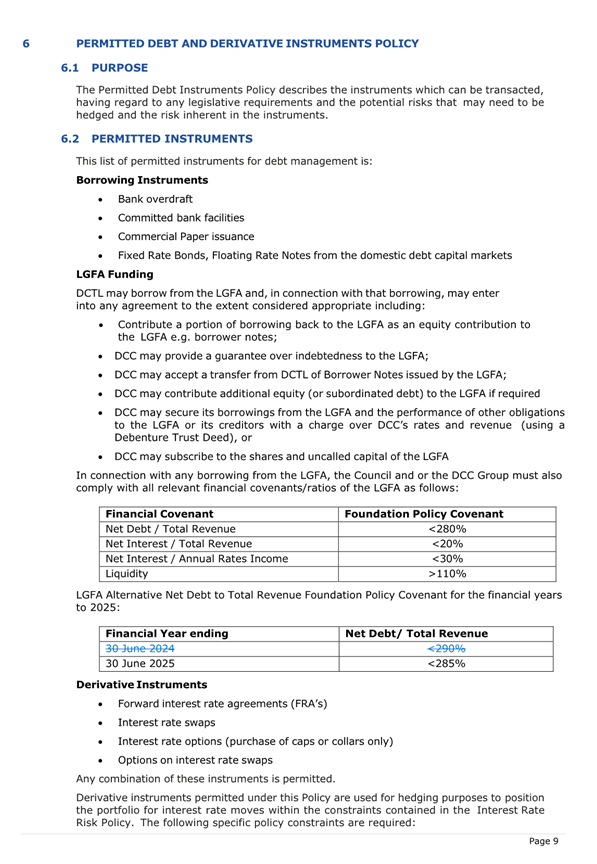

Treasury Risk Management Policy

5 The

Audit and Risk Subcommittee reviewed and provided feedback on the Treasury Risk

Management Policy at the 7 October 2024 meeting. The ARS discussed the approach

to interest rate setting for the DCC group whereby all entities pay the same

rate. Further information on this was requested for a future meeting. Dunedin

City Treasury Limited have been considering this and require further

information on accounting and tax implications before reporting back to

Council.

6 The

policy has since been to the Board of Dunedin City Treasury Ltd, where the

below changes have been approved.

a) Page

2 – Section 1. Purpose – gramma.

b) Page 4

– Section 2.3 DCTL Board – changes to make the required external

review every three years or in line with the Long-Term Plan cycle.

c) Page

4 - Section 2.3 DCTL Board – removal of word “annual” given

DCTL now adjusts the interest rate charged to Group entities quarterly.

d) Page 5

– Sections 2.4 and 2.5 DCTL Management and Breach Reporting –

change of title to DCC “Chief Financial Officer” as General Manager

Finance is no longer relevant.

e) Page 8

– Section 5.3 Funding Within the DCC Group – removal of wording

around the previous annual interest adjustment process given DCTL now adjusts

the interest rate to Group entities quarterly.

f) Wording

has been added, “Funding for specific projects within the Group may be

considered on a case-by-case basis” – This is to enable the on

lending of Green Social and Sustainable loans which are provided by the LGFA

for project lending which are provided at a 0.05% discount to normal LGFA

lending.

g) Page

9 – Section 6.2 Permitted Instruments – wording deleted for LGFA

Covenant which applied in FY 2024 (outdated).

7 The

policy is presented again to ARS to endorse approval of the policy prior to DCC

approval as a part of the 9 Year Plan process.

Fraud, Bribery and Corruption Prevention Policy

8 A

review has been undertaken on the Fraud, Bribery and Corruption Prevention

Policy (Clean: Attachment C, Track Changes: Attachment D) as a part of regular

scheduled review (review date scheduled for July 2023).

9 The

review has been conducted with representatives from Finance, Quality

Improvement, People and Capability, and externally from the staff at the

Counter Fraud Centre at the Serious Fraud Office (SFO).

10 The

following updates have been made to the Fraud, Bribery and Corruption Prevention

Policy:

a) Changed

the scheduled review date period from 2 to 3 years – reviews can be

conducted at any stage as required to address substantial changes.

b) The Policy

has been updated to follow the new template.

c) Added

extra information as to what a ‘zero tolerance stance’ means for

the DCC. The statements used follow that used by the Ministry of Justice and

recommended from the SFO.

d) Added a

statement on ‘Recovery of lost funds or recouping on expenses incurred

because of fraudulent or corrupt behaviour.’ As a part of the fraud

prevention activities of the DCC.

e) The

‘Investigation’ section has been added to align to the Fraud

Bribery and Corruption Investigation Procedures, and the Protected

Disclosure Whistleblower Policy.

11 The Fraud,

Bribery and Corruption Investigation Procedures (Attachment E) have also been

included in this report for noting. These procedures are a working documents

and as such can be updated as and when required to incorporate improvements to

the procedures.

12 There is a

tender underway for fraud prevention and awareness training services and

investigations support. Through working in partnership with the successful

third party there will be further development to the Fraud, Bribery and

Corruption Investigation Procedure.

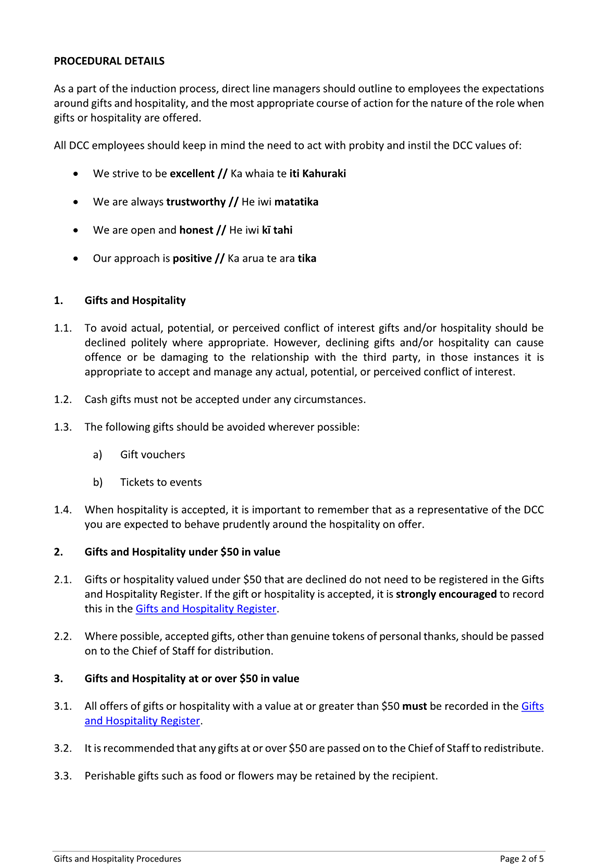

Gifts and

Hospitality Policy

13 A review

has been undertaken on the Gifts and Hospitality Policy (Clean: Attachment F,

Track Changes: Attachment G) as a part of regular scheduled review (review date

scheduled for July 2020). The review has been conducted with representatives

from Risk and Audit, Finance, and Procurement and Contract Management teams.

14 The

following changes have been made to the Gifts and Hospitality Policy:

a) Updated the Responsible Officer to General Manager

Corporate Services, and responsible department to Corporate Services.

b) Changed the scheduled review date period from 2 to 3 years

– reviews can be conducted at any stage as required to address substantial

changes.

c) The Policy has been updated to follow the new template.

d) The order of wording on the policy has been changed to

provide a logical flow and to improve clarity on key points.

e) Policy has been reduced to remove all procedural details

– these have been captured in the procedures document.

f) Integrity definition added from the Office of the Auditor

General Good Practice Guidelines on Integrity.

Integrity:

can be defined as demonstrating honesty and uncompromising adherence to strong

ethical principles. It is about aligning both commitment and behaviour with

strong ethical values or principles in a consistent and uncompromising way.

https://oag.parliament.nz/good-practice/integrity/integrity-framework/about-integrity.htm

g) Conflict of Interest definition has been updated to align

with the conflict-of-interest policy.

h) Employee definition has been added to align with other DCC

policies.

i) Referrals have been made to other DCC internal policies and

procedures where appropriate.

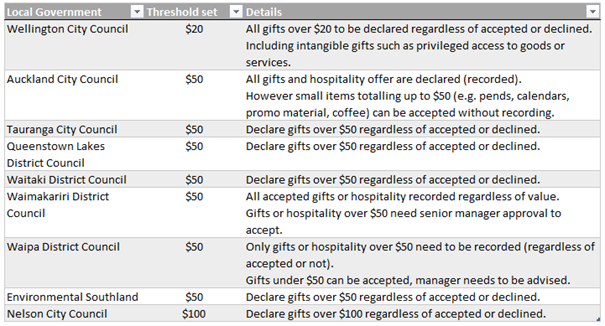

a) The

monetary value limit required for recording gifts and hospitality has been

increased to $50, to align with the other local authorities. See the below

table for an overview of the thresholds set by other local authorities for

declaring gifts and hospitality offered.

b) Greater

emphasis has been placed on understanding that sometimes it is not appropriate

to decline gifts or hospitality offered. This is a recognition of the

need to maintain and honour DCC’s relationships with the party offering

gifts or hospitality.

c) The

policy has been updated to strengthen the alignment with the Conflict of

Interest Policy.

d) Additional

information has been provided on the receiving of koha in line with the koha

policy and guidelines.

e) The

procedure to record offers of gifts and hospitality has been simplified in the

register.

f) Clarity

has been added in the procedures on allowance for keeping perishable items such

as food and flowers, rather than passing these on to the Chief of Staff.

15 The Gifts

and Hospitality Procedures (Attachment H) have also been included in this

report for noting.

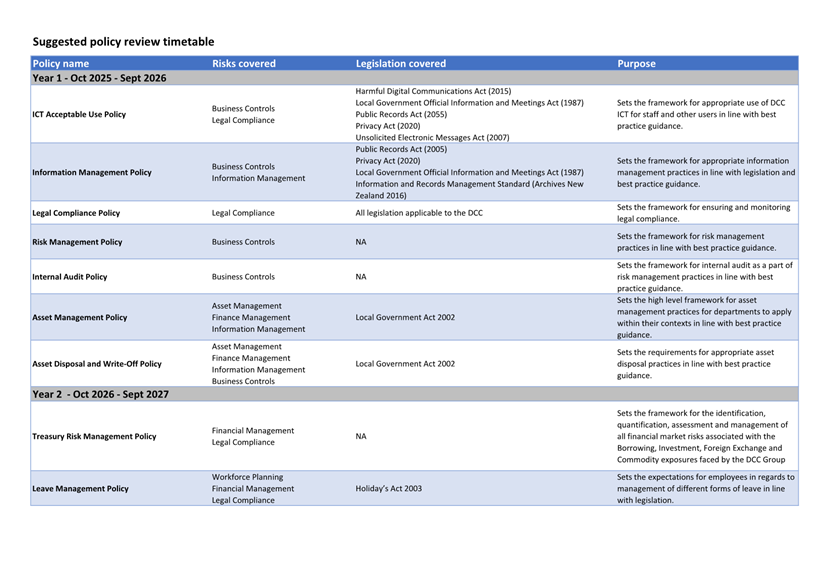

Policy Review

Schedule

16 As per

request from ARS at the last meeting (7th October 2024), management

have provided a suggested review schedule for the DCC policies.

17 The

Assurance Manager has reviewed all the policies that currently go to ARS and

have provided additional information about these policies in terms of:

a) The

risk(s) the policy manages.

b) The nature

of the policy.

c) The

level of prior knowledge required of elected members to understand the

requirements for the policy area.

18 Based on

these criteria, management have provided a suggested review schedule (based on

the local government electoral cycle) for ARS to approve/amend (Attachment I).

A summary is also provided below.

19 Year One

(Oct 2025/Sep 2026): it is recommended that ARS reviews policies that are

designed to be high level guidance to support best practise with minimal no

legal compliance requirements. The following policies fit those criteria:

a) ICT

Acceptable Use Policy

b) Information

Management Policy

c) Legal

Compliance Policy

d) Risk

Management Policy

e) Internal

Audit Policy

f) Asset

Management Policy

g) Asset

Disposal and Write-Off Policy

20 Year Two

(Oct 2026/Sep 2027): it is recommended that ARS reviews policies that are

designed to have a detailed level of guidance to support best practise and

legal compliance requirements. It is advantageous for there to be a better

understanding of the DCC operating environment and values. The following

policies fit those criteria:

a) Treasury

Risk Management Policy

b) Leave

Management Policy

c) Procurement

and Contracts Management Policy

d) Staff

Conflict of Interest Policy

e) Gifts and

Hospitality Policy

f) Sensitive

Expenditure Policy

g) Koha

Policy

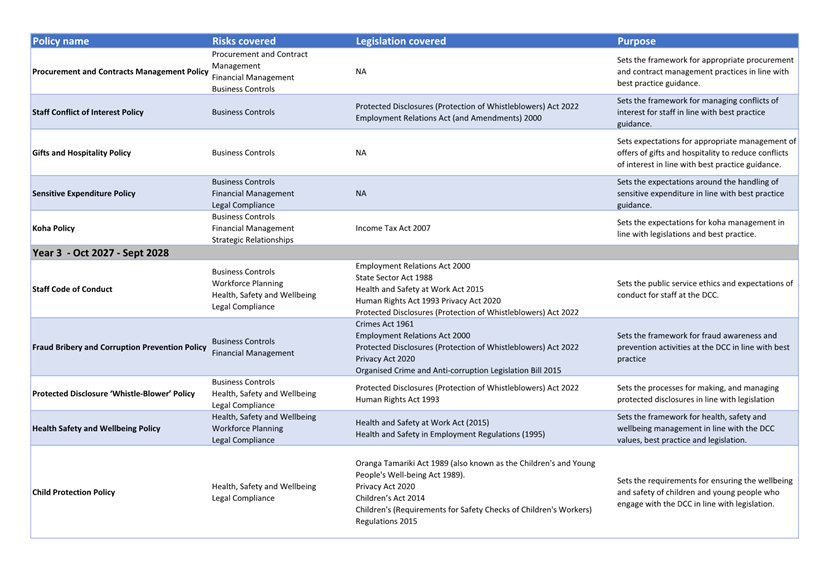

21 Year Three

(Oct 2027/Sep 2028): it is recommended that ARS reviews policies that are

detailed to ensure specific legal compliance requirements. It is advantageous

for there to be advanced understanding of the legal compliance associated to

the policies, and the DCC operating environment and values. The following

policies fit those criteria:

a) Staff

Code of Conduct

b) Fraud

Bribery and Corruption Prevention Policy

c) Protected

Disclosure ‘Whistle-Blower’ Policy

d) Health

Safety and Wellbeing Policy

e) Child

Protection Policy

22 In the

meantime, the following policies will be brought to ARS before the next local

government election (October 2025) as they are currently overdue for review:

a) ICT

Acceptable Use Policy

b) Information

Management Policy

c) Asset

Management Policy

d) Asset

Disposal and Write-Off Policy

e) Staff Code

of Conduct

f) Sensitive

Expenditure Policy

Policy Review Process for the Audit and Risk

Subcommittee

23 For

clarity, the following is an outline on the purpose and expectations for the

policy review process for ARS.

24 Internal

operational policies are brought to ARS for review, feedback, endorsement for

approval or approval. Most of these policies are then approved by ELT.

25 Policies

will be reviewed as per the set schedule, however, should there be a

legislative, best practice or operational change that requires an earlier

update to a policy the review process will be brought forward to accommodate

this.

26 ARS reviews

policies for the following aspects in relations to an appropriate level of

cover for the nature and level of risk:

a) Clarity

of what the risk(s) is being managed and associated controls.

b) Governance/oversight

responsibilities are set.

c) Monitoring

and reporting activities are set.

d) Clarity on

what a breach may look like and the consequences of this.

27 If

applicable, any supporting documentation (procedures, guidelines, framework)

will also be provided to ARS to provide further context on the

operationalisation of the policy. These will be provided for noting purposes

only. These documents are designed to be working documents that get updated as

the need for improvements are identified.

NEXT STEPS

28 Any

feedback provided by ARS on policies presented will be incorporated into the

policy, which will then go to the Executive Leadership Team for final review

and approval.

29 The Policy

Review Schedule will be implemented for future ARS meetings.

Signatories

|

Author:

|

Hayley Knight - Assurance Manager

|

|

Authoriser:

|

Carolyn Allan - Chief Financial Officer

|

Attachments

|

|

Title

|

Page

|

|

⇩a

|

Policy - Treasury Risk

Management - November 2024 - Clean

|

47

|

|

⇩b

|

Policy - Treasury Risk

Management - November 2024 - Track Changes

|

67

|

|

⇩c

|

Policy - Fraud, Bribery

and Corruption Prevention - Clean - November 2024

|

87

|

|

⇩d

|

Policy - Fraud, Bribery

and Corruption Prevention - Track Changes - November 2024

|

97

|

|

⇩e

|

Procedure - Fraud,

Birbery and Corruption Investigation

|

108

|

|

⇩f

|

Policy - Gifts and

Hospitality - Clean - November 2024

|

121

|

|

⇩g

|

Policy - Gifts and

Hospitality - Track Changes - November 2024

|

126

|

|

⇩h

|

Procedure - Gifts and

Hospitality

|

131

|

|

⇩i

|

Suggested Policy Review

Timetable

|

136

|

|

SUMMARY OF CONSIDERATIONS

|

|

Fit with purpose of Local Government

This report provides an update on Council

Policy documents as identified by the Audit and Risk Subcommittee Workplan,

which is a regulatory function considered good quality and cost effective.

|

|

Fit with strategic framework

|

|

Contributes

|

Detracts

|

Not applicable

|

|

Social Wellbeing Strategy

|

✔

|

☐

|

☐

|

|

Economic Development Strategy

|

✔

|

☐

|

☐

|

|

Environment Strategy

|

✔

|

☐

|

☐

|

|

Arts and Culture Strategy

|

✔

|

☐

|

☐

|

|

3 Waters Strategy

|

✔

|

☐

|

☐

|

|

Spatial Plan

|

✔

|

☐

|

☐

|

|

Integrated Transport Strategy

|

✔

|

☐

|

☐

|

|

Parks and Recreation Strategy

|

✔

|

☐

|

☐

|

|

Other strategic projects/policies/plans

|

☐

|

☐

|

✔

|

The Audit and Risk Subcommittee monitors and provides

assurance for the effective review and management of core Council Policies

– thereby supporting business controls and delivery, governance and the

realisation of strategic objectives.

|

|

Māori Impact Statement

There are no know impacts for mana whenua.

|

|

Sustainability

There are no implications for sustainability.

|

|

LTP/Annual Plan / Financial Strategy /Infrastructure

Strategy

There are no known implications.

|

|

Financial considerations

No financial implications have been identified.

|

|

Significance

This report is considered low in terms of the

Council’s Significance and Engagement Policy.

|

|

Engagement – external

The Serious Fraud Office was consulted on for the review

of the Fraud, Bribery and Corruption Prevention Policy.

Other local authorities were contacted to understand their

threshold for declaring gifts and hospitality offered as a part of the Gifts

and Hospitality Policy review process.

|

|

Engagement - internal

Activities noted herein include cross Council engagement

and collaboration on Policy review and development.

|

|

Risks: Legal / Health and Safety etc.

A failure to maintain effective and appropriate Policy

framework across core Council functions exposes the DCC to a range of operational

and strategic risks, including financial, business and service performance,

community, business and sector confidence, as well as potential fraud and

litigation.

|

|

Conflict of Interest

No conflicts of interest have been identified.

|

|

Community Boards

There are no known implications for the Community Boards.

|

|

|

Audit and Risk Subcommittee

4 December 2024

|

|

|

Audit and Risk Subcommittee

4 December 2024

|

|

|

Audit and Risk Subcommittee

4 December 2024

|

|

|

Audit and Risk Subcommittee

4 December 2024

|

|

|

Audit and Risk Subcommittee

4 December 2024

|

|

|

Audit and Risk Subcommittee

4 December 2024

|

|

|

Audit and Risk Subcommittee

4 December 2024

|

|

|

Audit and Risk Subcommittee

4 December 2024

|

|

|

Audit and Risk Subcommittee

4 December 2024

|

|

|

Audit and Risk Subcommittee

4 December 2024

|

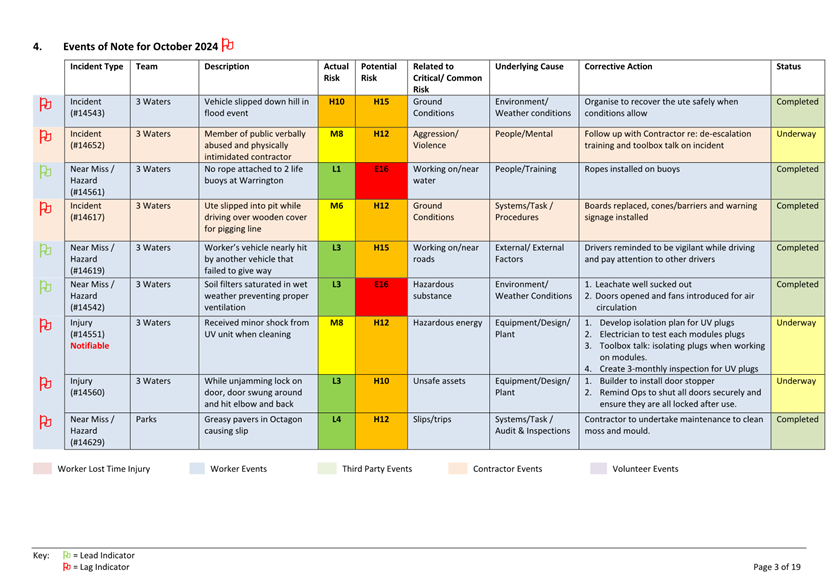

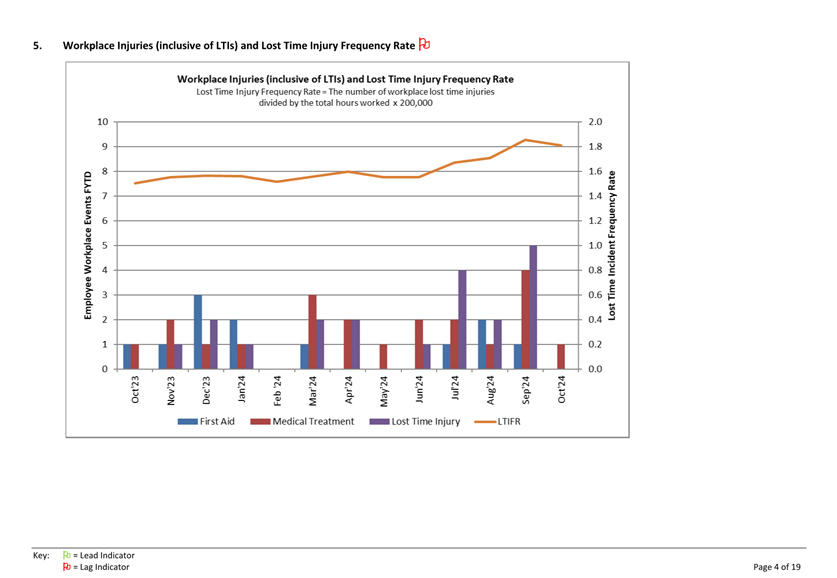

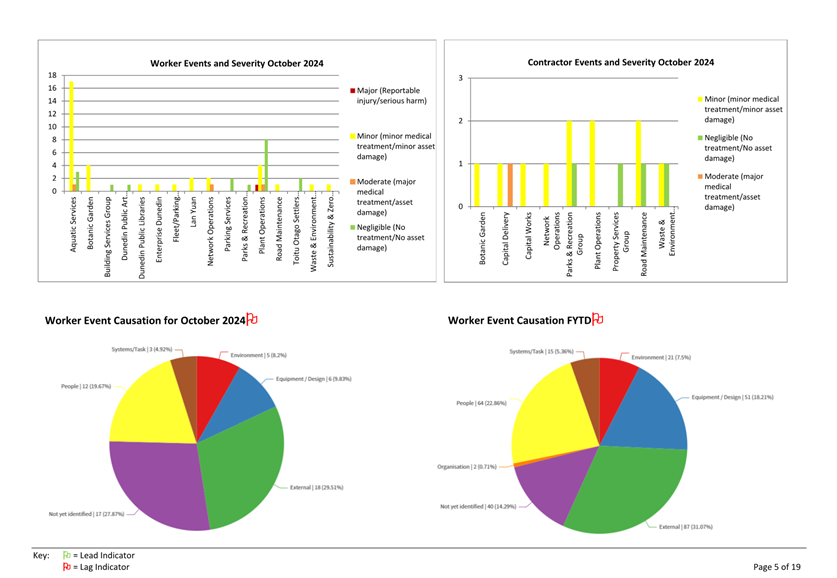

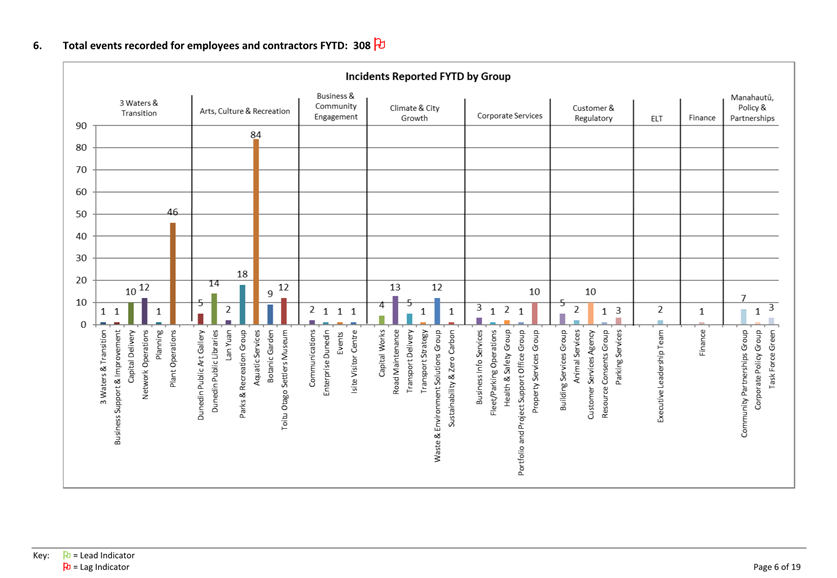

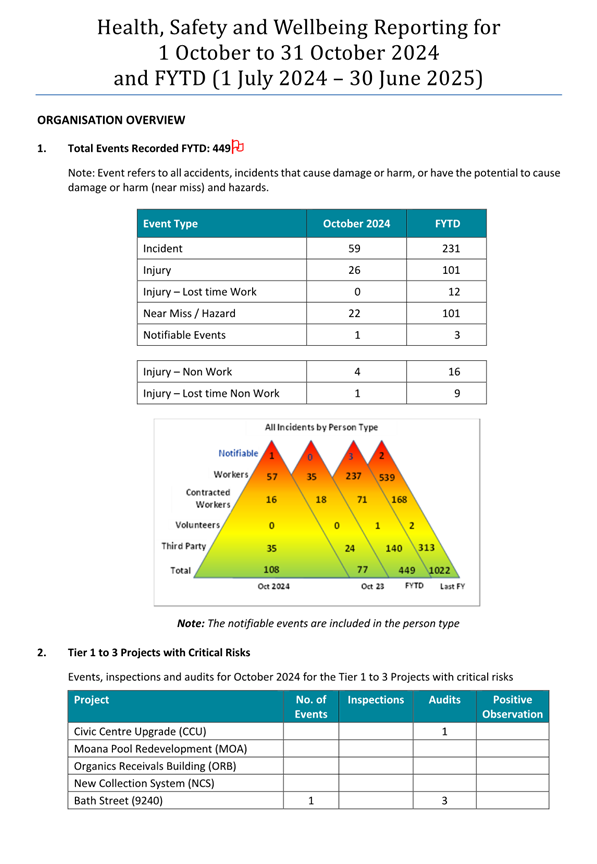

Health and Safety Monthly Reporting for October 2024

Department: Health and Safety

EXECUTIVE SUMMARY

1 The

monthly Health, Safety and Wellbeing report for October 2024 is attached for

consideration.

RECOMMENDATIONS

That the Subcommittee:

a) Notes the monthly

Health, Safety and Wellbeing report for October 2024.

Signatories

|

Author:

|

Jane Pearce - Health and Safety Manager

|

|

Authoriser:

|

Robert West - General Manager Corporate Services

|

Attachments

|

|

Title

|

Page

|

|

⇩a

|

Health, Safety and

Wellbeing report - October 2024

|

139

|

|

|

Audit and Risk Subcommittee

4 December 2024

|

|

|

Audit and Risk Subcommittee

4 December 2024

|

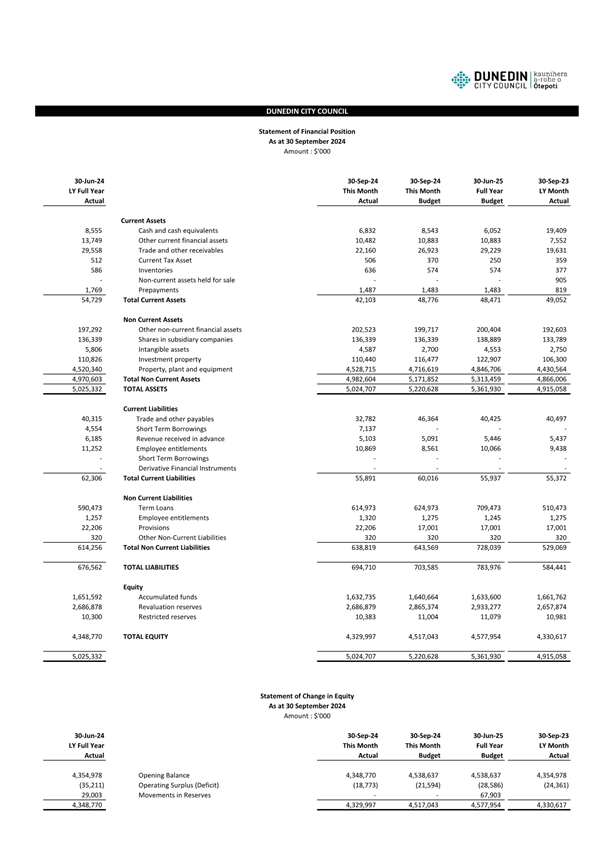

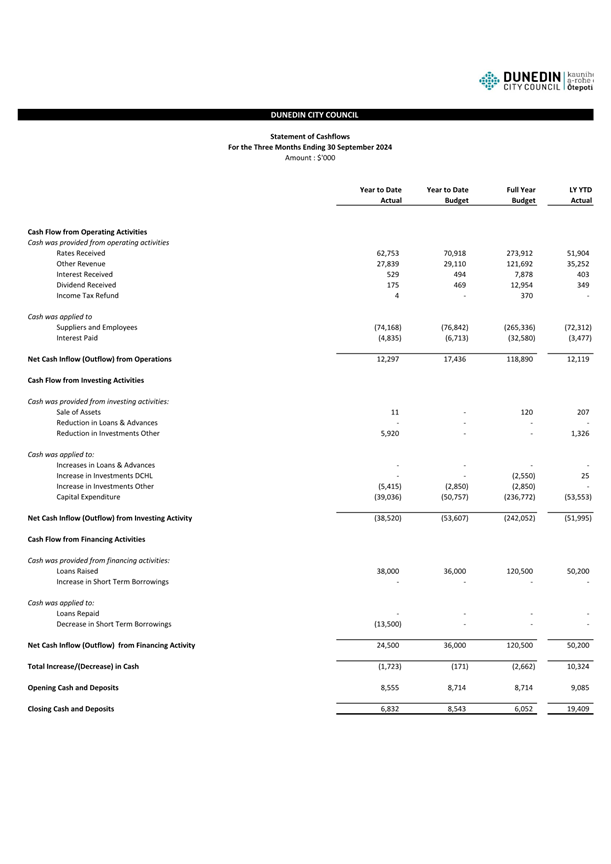

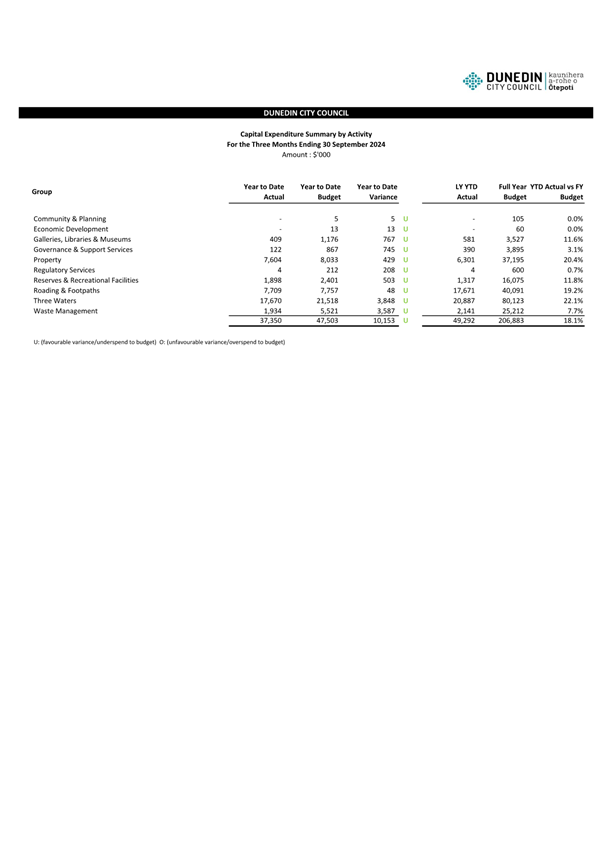

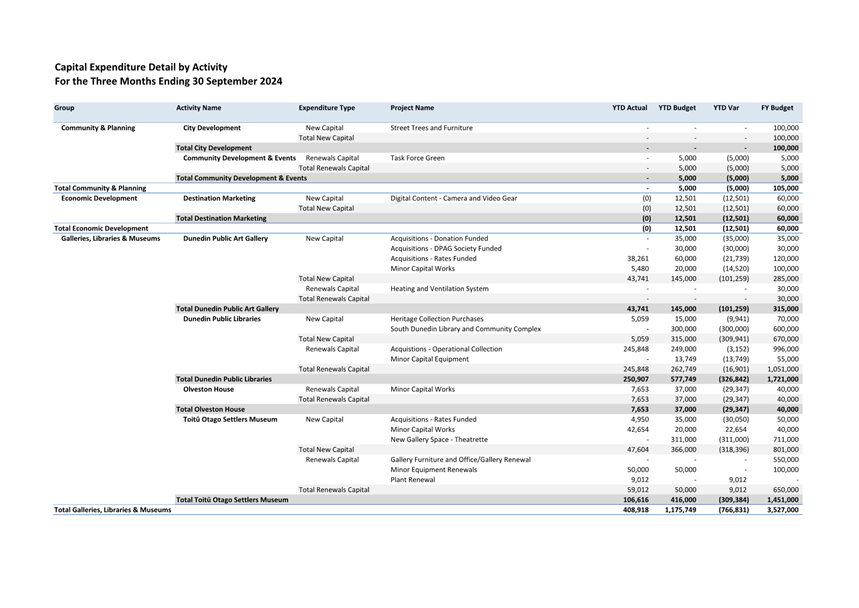

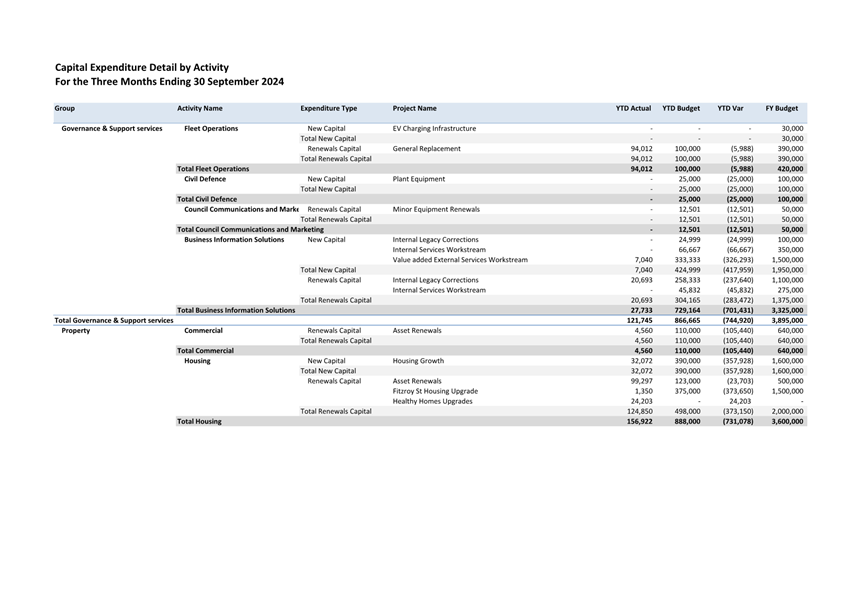

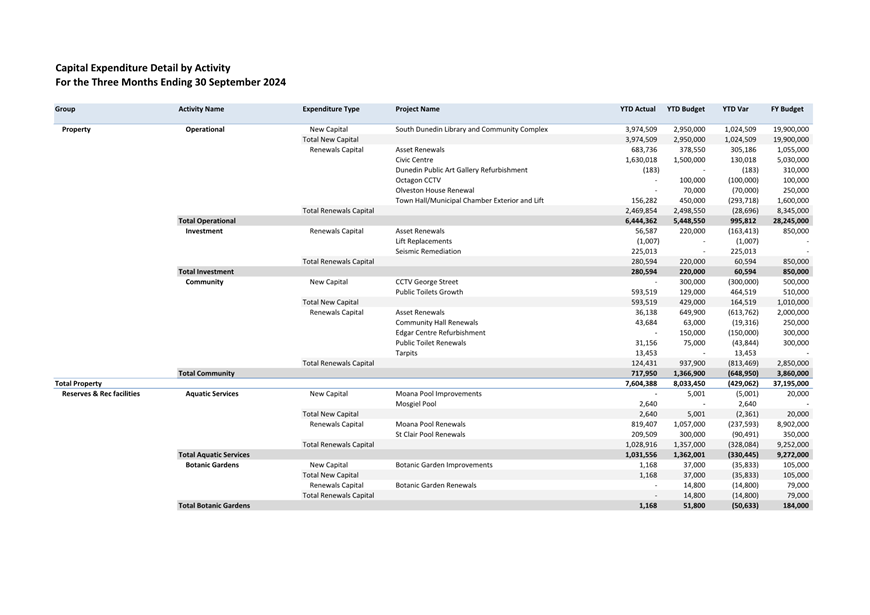

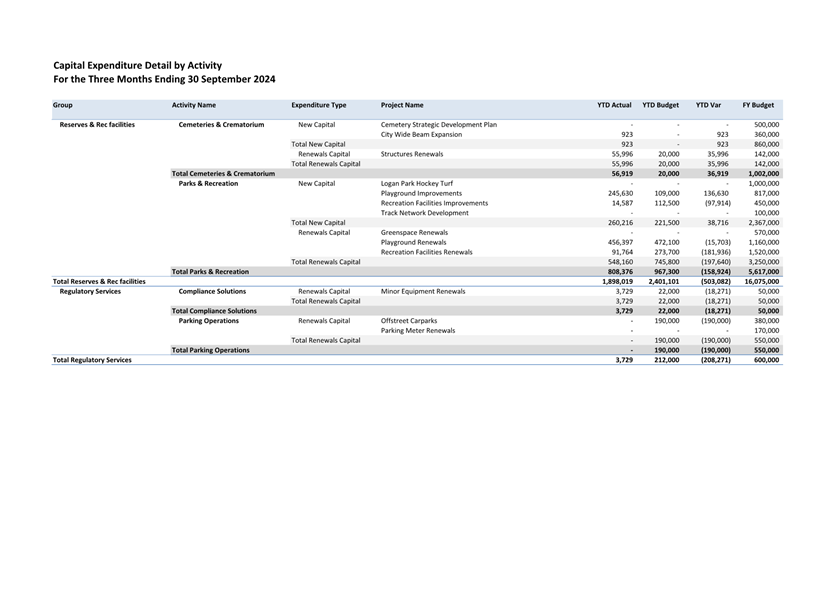

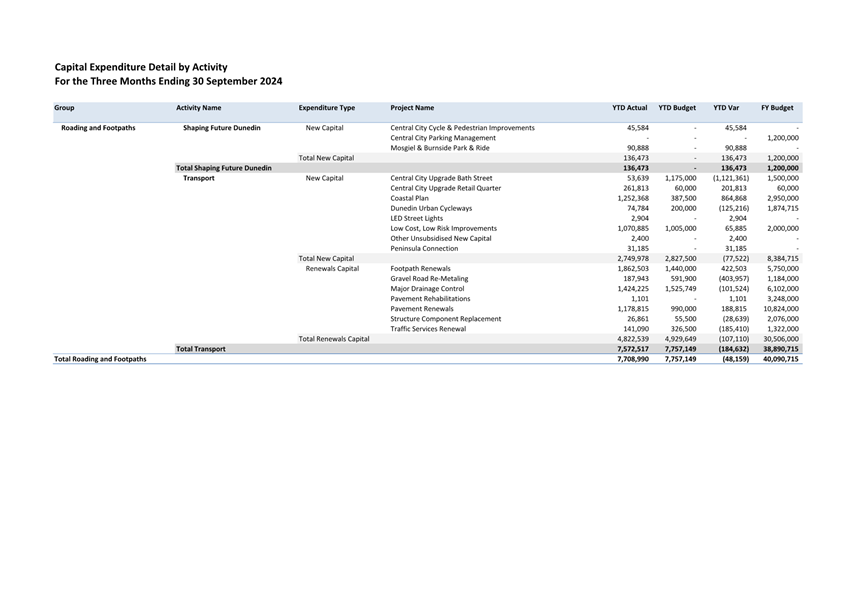

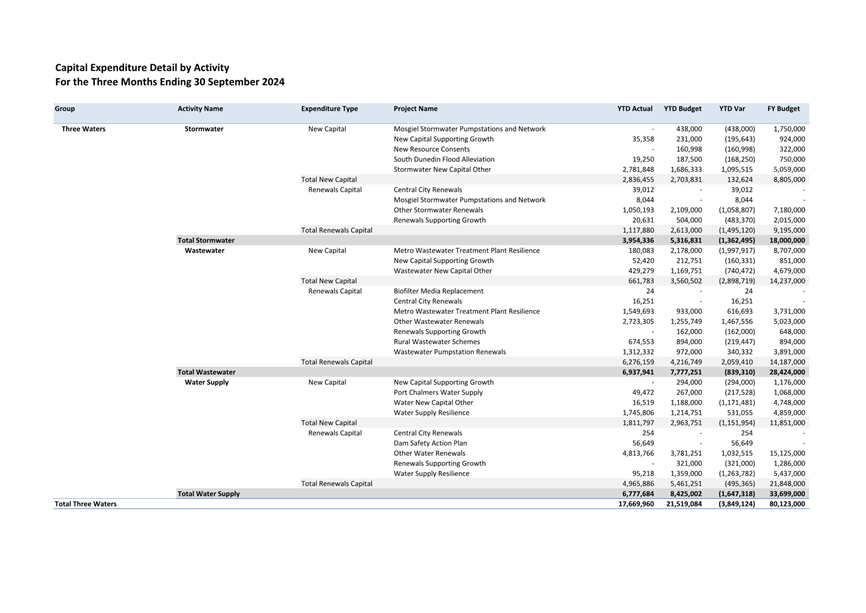

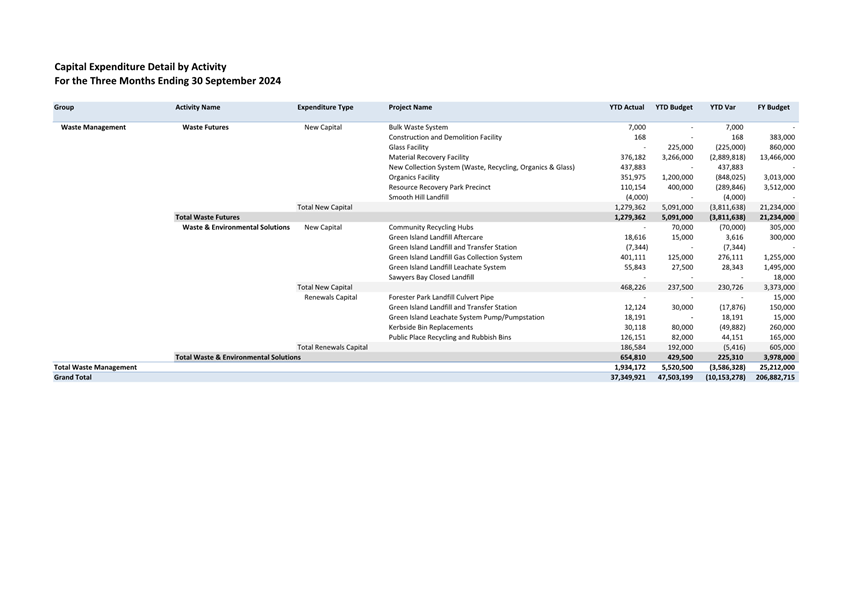

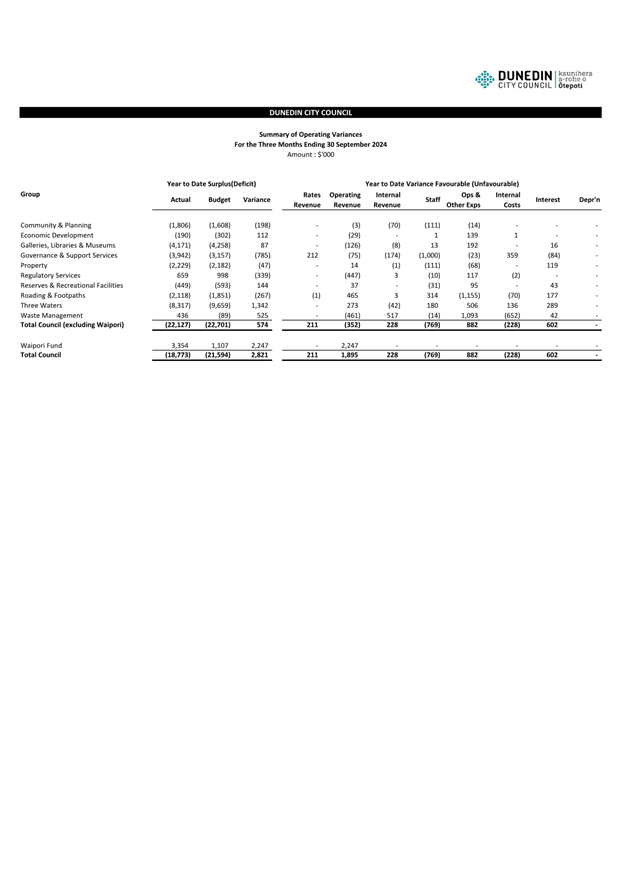

Financial Report - Period Ended 30 September 2024

Department: Finance

EXECUTIVE SUMMARY

1 This

report provides the financial results for the period ended 30 September 2024

and the financial position as at that date which was presented to the Finance

and Council Controlled Organisation Committee meeting held on 14 November 2024.

2 As

this is an administrative report only, there are no options or Summary of

Considerations.

Financial

Overview

For the period

ended 30 September 2024

RECOMMENDATIONS

That the Subcommittee:

a) Notes the Financial

Performance for the period ended 30 September 2024 and the Financial Position

as at that date.

BACKGROUND

3 This

report provides the financial statements for the period ended 30 September 2024. It includes reports on financial performance, financial position,

cashflows and capital expenditure. Summary information is provided in the

body of this report with detailed results attached. The operating result is

also shown by group, including analysis by revenue and expenditure type.

DISCUSSION

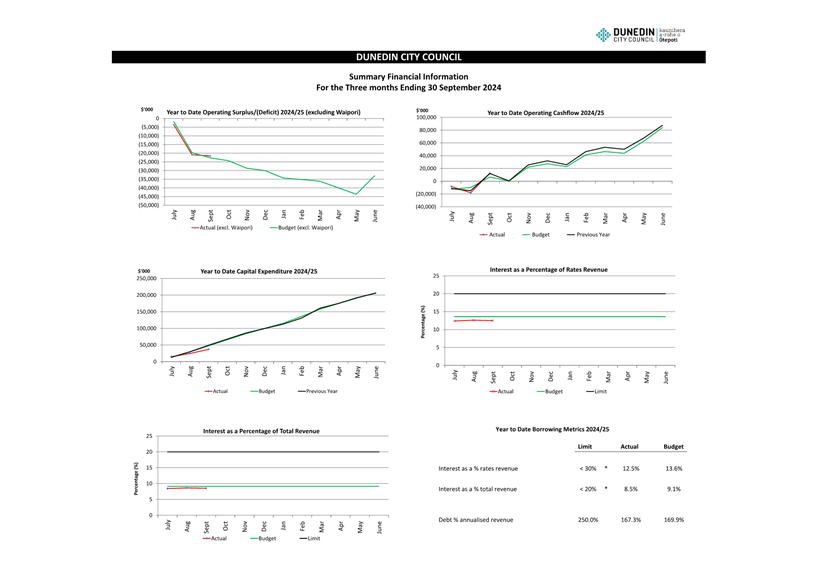

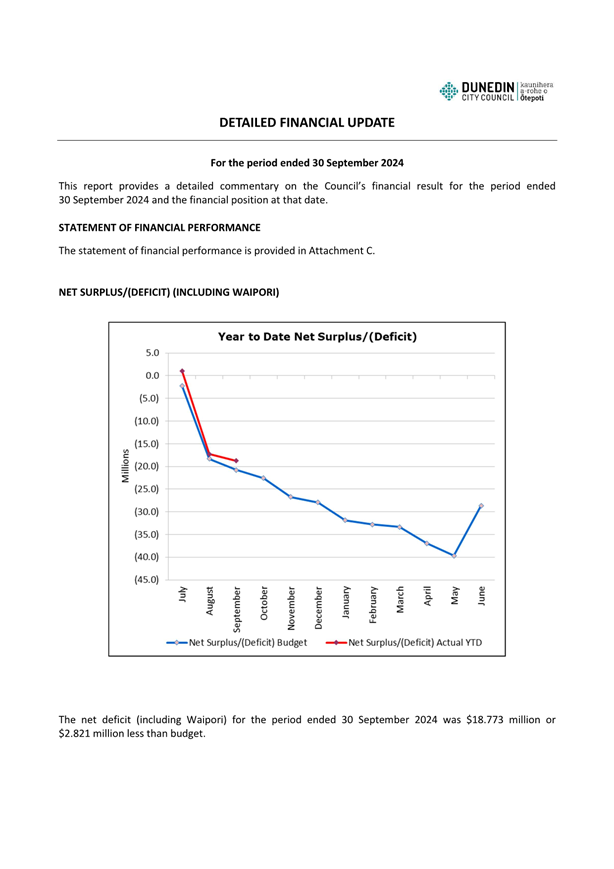

4 This report includes a high-level summary of the financial

information to 30 September 2024. Please refer

to Attachment I for the detailed financial update.

Statement of Financial Performance

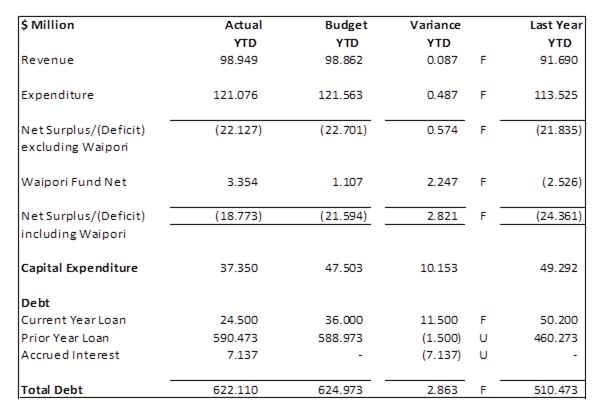

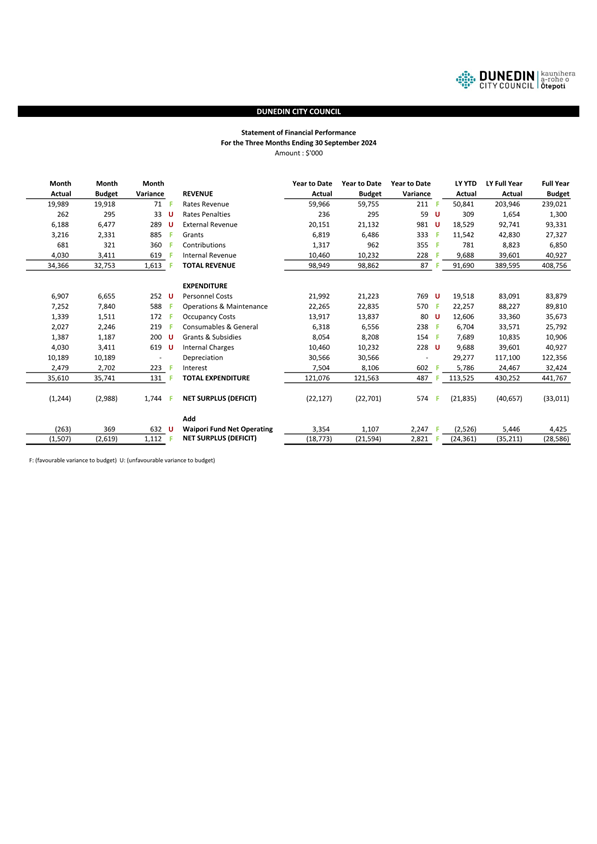

5 Revenue

was $98.949 million for the period or $87k more than budget.

6 External

revenue was unfavourable $981k partly due to landfill revenue being less than

budget. Changes relating to the new kerbside collections contract mean

disposal fees under the contract are reported as internal revenue. There was also lower-than-expected revenue from the Parking and

Building Services activities as well as year to date revenue from water sales.

7 Grants

revenue was favourable $333k reflecting the level of subsidised Transport

operating and capital expenditure. Better Off Funding revenue was

slightly less than budgeted.

8 Expenditure

was $121.076 million for the period, or $487k less than budget.

9 Operations

and maintenance expenditure was favourable $570k with unfavourable Transport

maintenance costs largely offset by under expenditure in other activities,

including Three Waters and Waste and Environmental Services.

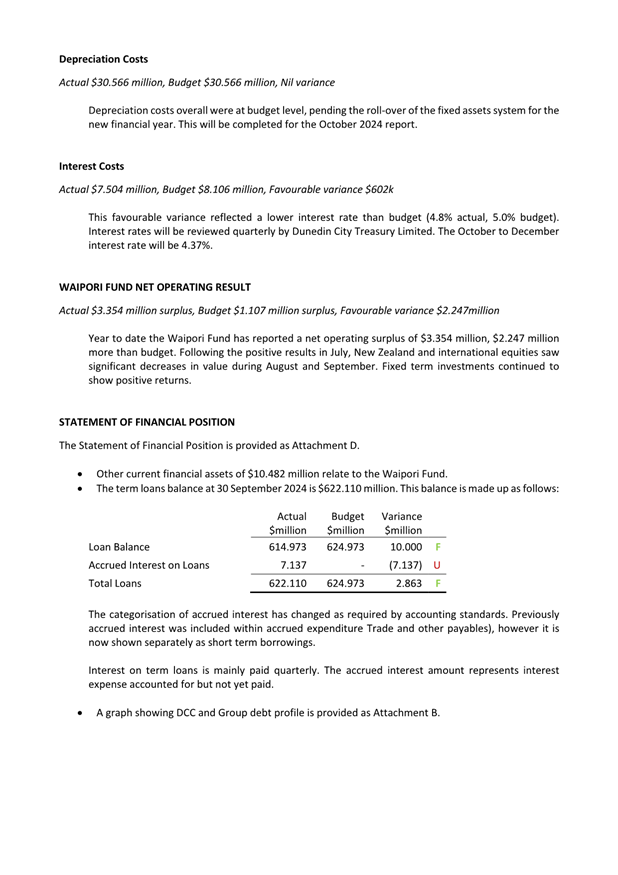

10 Interest

costs were favourable $602k reflecting a lower interest rate than budgeted and

the timing of new loan advances.

11 Year

to date the Waipori Fund has reported a net operating surplus of $3.354

million, $2.247 million more than budget. Following the positive results in

July, New Zealand and international equities saw decreases in value during

August and September. However, fixed term investments continued to show

positive returns.

Statement of Financial Position

12 Capital

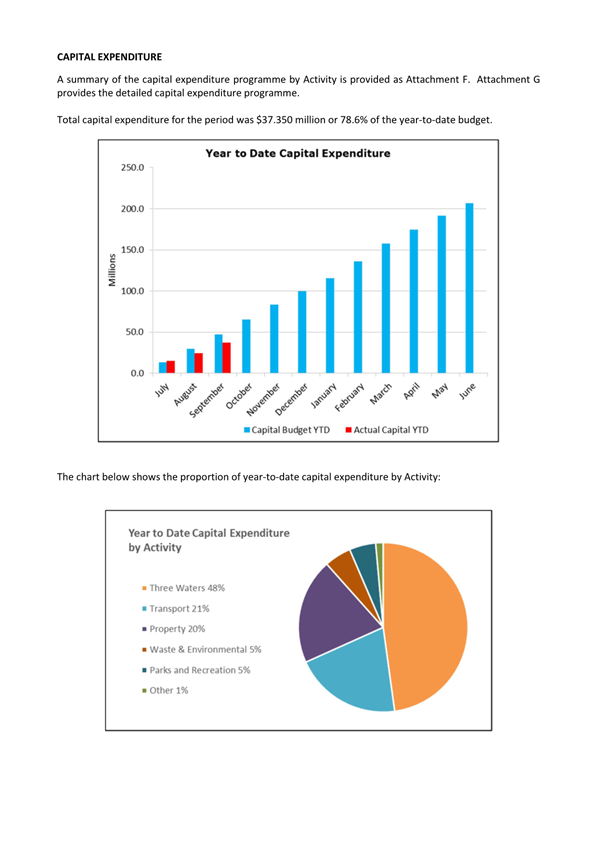

expenditure was $37.350 million or 78.6% of the year-to-date budget. Capital

expenditure in most activities was generally within budget for the period.

13 The loans

balance now includes accrued interest of $7.137 million (representing the loan

interest owing but not yet paid at 30 September shown as short-term loans).

Previously this was classified separate to the loan balance, however the

accounting standards now require this to be included. The actual loan balance

at 30 September was $614.973 million, $10.000 million less than budget.

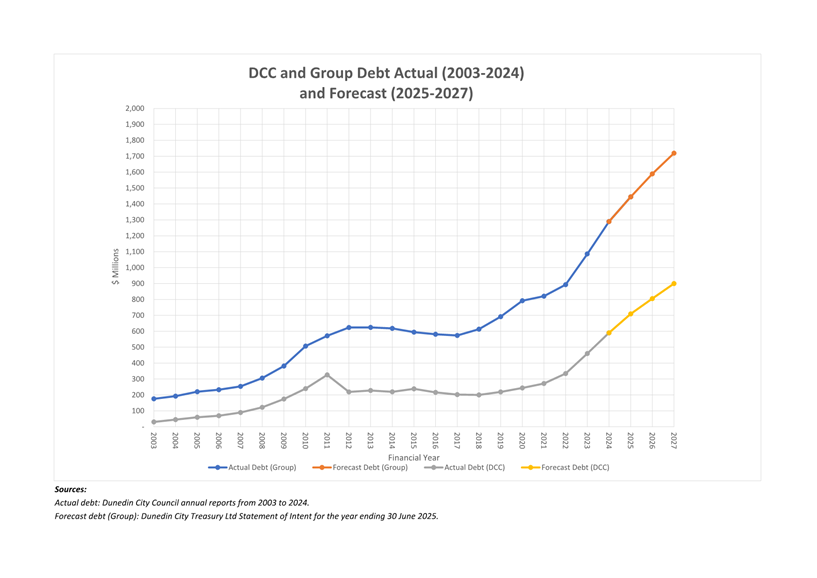

14 Attachment

A includes a chart showing actual group and DCC debt for the years ending June

2003-2024. It provides forecast information for the years ending June 2024-2027

based on the current Statements of Intent (SOI).

OPTIONS

15 As this is an administrative report only, there are no options

provided.

NEXT STEPS

16 Financial

Result Reports continue be presented to future meetings of either the Finance

and Council Controlled Organisation Committee or Council.

Signatories

|

Author:

|

Hayden McAuliffe - Financial Services Manager

|

|

Authoriser:

|

Carolyn Allan - Chief Financial Officer

|

Attachments

|

|

Title

|

Page

|

|

⇩a

|

Dashboard Summary

Financial Information

|

161

|

|

⇩b

|

Debt Graph

|

162

|

|

⇩c

|

Statement of Financial

Performance

|

163

|

|

⇩d

|

Statement of Financial

Position

|

164

|

|

⇩e

|

Statement of Cashflows

|

165

|

|

⇩f

|

Capital Expenditure

Summary

|

166

|

|

⇩g

|

Capital Expenditure

Detail

|

167

|

|

⇩h

|

Operating Variances

|

174

|

|

⇩i

|

Detailed Financial

Update

|

175

|

|

|

Audit and Risk Subcommittee

4 December 2024

|

|

|

Audit and Risk Subcommittee

4 December 2024

|

|

|

Audit and Risk Subcommittee

4 December 2024

|

|

|

Audit and Risk Subcommittee

4 December 2024

|

|

|

Audit and Risk Subcommittee

4 December 2024

|

|

|

Audit and Risk Subcommittee

4 December 2024

|

|

|

Audit and Risk Subcommittee

4 December 2024

|

|

|

Audit and Risk Subcommittee

4 December 2024

|

|

|

Audit and Risk Subcommittee

4 December 2024

|

|

|

Audit and Risk Subcommittee

4 December 2024

|

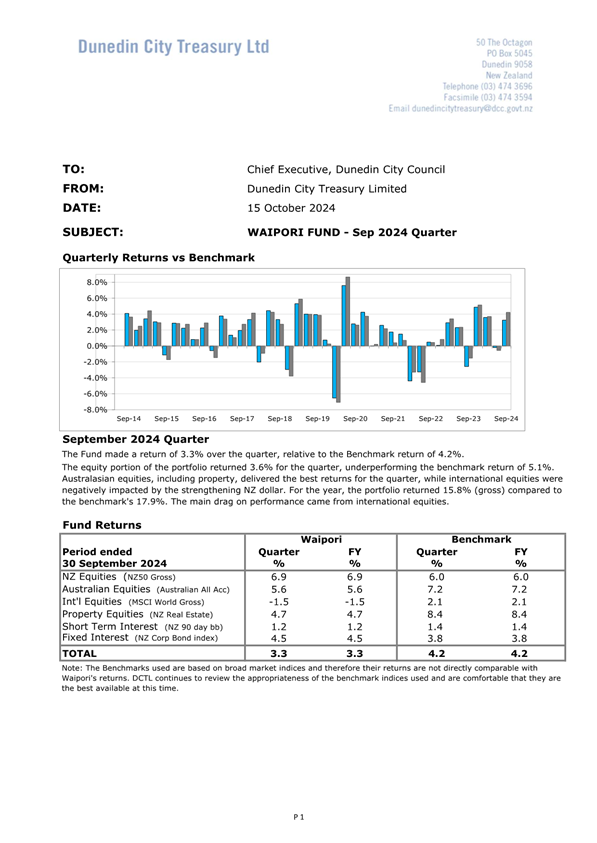

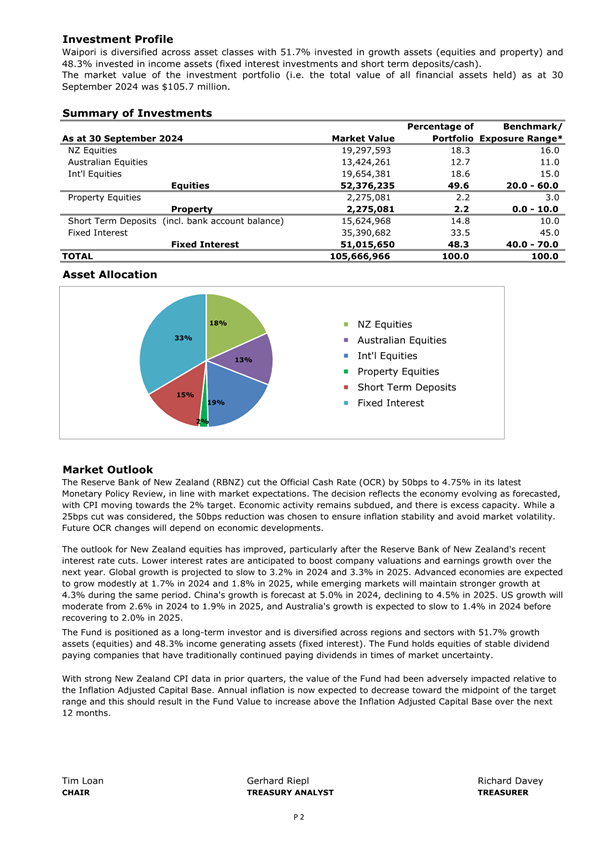

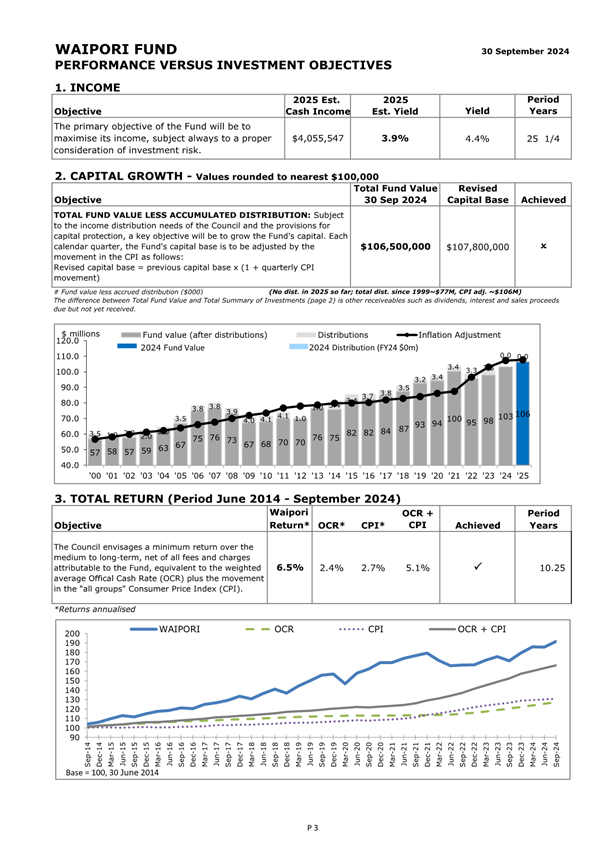

Waipori Fund - Quarter ending 30 September 2024

Department: Finance

EXECUTIVE SUMMARY

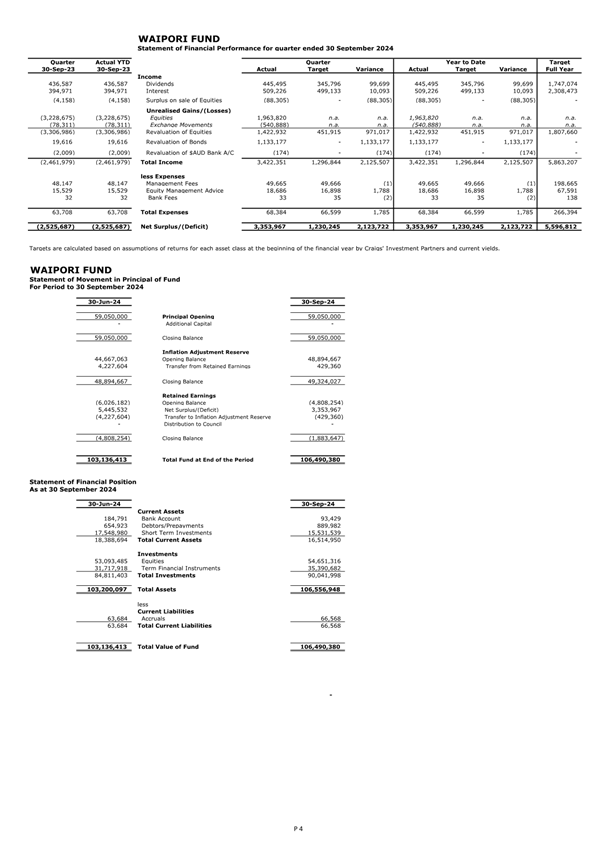

1 The

attached report from Dunedin City Treasury Limited provides information on the

results of the Waipori Fund for the quarter ended 30 September 2024 which was presented to the Finance and Council Controlled

Organisation Committee meeting held on 14 November 2024.

RECOMMENDATIONS

That the Subcommittee:

a) Notes the report from

Dunedin City Treasury Limited on the Waipori Fund for the quarter ended 30

September 2024.

DISCUSSION

2 The

Waipori Fund Statement of Investment Policy and Objectives (SIPO) requires

quarterly reporting on the performance and financial position of the fund.

3 Dunedin

City Treasury Limited has provided the Waipori Fund report for the September

2024 quarter. The report is provided as Attachment A.

OPTIONS

4 As

this is a noting report, no options are provided.

NEXT STEPS

5 Quarterly

reporting on the performance and financial position of the fund will be

provided to future meetings of either the Financial and Council Controlled

Organisations Committee or Council.

6 The

Waipori Fund SIPO is being reviewed as part of the development of the 9-year

plan 2025-34.

Signatories

|

Authoriser:

|

Carolyn Allan - Chief Financial Officer

|

Attachments

|

|

Title

|

Page

|

|

⇩a

|

Waipori Fund -

September 2024 Quarter

|

188

|

|

SUMMARY OF CONSIDERATIONS

|

|

Fit with purpose of Local Government

This decision enables democratic local

decision making and action by, and on behalf of communities.

|

|

Fit with strategic framework

|

|

Contributes

|

Detracts

|

Not applicable

|

|

Social Wellbeing Strategy

|

☐

|

☐

|

✔

|

|

Economic Development Strategy

|

☐

|

☐

|

✔

|

|

Environment Strategy

|

☐

|

☐

|

✔

|

|

Arts and Culture Strategy

|

☐

|

☐

|

✔

|

|

3 Waters Strategy

|

☐

|

☐

|

✔

|

|

Spatial Plan

|

☐

|

☐

|

✔

|

|

Integrated Transport Strategy

|

☐

|

☐

|

✔

|

|

Parks and Recreation Strategy

|

☐

|

☐

|

✔

|

|

Other strategic projects/policies/plans

|

☐

|

☐

|

✔

|

Reporting on the performance of the Waipori Fund does not

contribute directly to the Strategic Framework.

|

|

Māori Impact Statement

Investment returns from the Waipori Fund impact on the

level of rates payable, and therefore impact across all Dunedin communities

including Māori.

|

|

Sustainability

There are no impacts for sustainability.

|

|

LTP/Annual Plan / Financial Strategy /Infrastructure

Strategy

A review of the SIPO for the Waipori Fund will be taken

into account when developing a Financial Strategy for the 9 year plan

2025-34.

|

|

Financial considerations

Financial considerations are presented in the Waipori Fund

report for the March 2024 quarter.

|

|

Significance

This report is considered to be of low significance in

terms of the Council’s Significance and Engagement Policy.

|

|

Engagement – external

There has been no external engagement.

|

|

Engagement - internal

There has been no internal engagement.

|

|

Risks: Legal / Health and Safety etc.

There are no identified risks.

|

|

Conflict of Interest

There are no known conflicts of interest.

|

|

Community Boards

There are no implications for Community Boards.

|

|

|

Audit and Risk Subcommittee

4 December 2024

|

|

|

Audit and Risk Subcommittee

4 December 2024

|

Resolution to Exclude the

Public

That the Audit and Risk Subcommittee:

Pursuant to the provisions of the

Local Government Official Information and Meetings Act 1987, exclude the public

from the following part of the proceedings of this meeting namely:

|

General subject of the matter to be considered

|

Reasons

for passing this resolution in relation to each matter

|

Ground(s) under

section 48(1) for the passing of this resolution

|

Reason for

Confidentiality

|

|

C1

Confirmation of the Confidential Minutes of Audit and Risk Subcommittee

meeting - 7 October 2024 - Public Excluded

|

S7(2)(h)

The

withholding of the information is necessary to enable the local authority to

carry out, without prejudice or disadvantage, commercial activities.

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to prejudice the supply of

similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

S7(2)(b)(ii)

The

withholding of the information is necessary to protect information where the

making available of the information would be likely unreasonably to prejudice

the commercial position of the person who supplied or who is the subject of

the information.

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of natural

persons, including that of a deceased person.

|

.

|

|

|

C2

Confirmation of the Confidential Minutes of Audit and Risk Subcommittee

meeting - 25 October 2024 - Public Excluded

|

S7(2)(b)(i)

The

withholding of the information is necessary to protect information where the

making available of the information would disclose a trade secret.

|

.

|

|

|

C3

Treasury Risk Management Compliance Report

|

S7(2)(h)

The

withholding of the information is necessary to enable the local authority to

carry out, without prejudice or disadvantage, commercial activities.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C4

DCC Risk 'Deep Dive' - Climate Change Mitigation and Adaptation

|

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to prejudice the supply

of similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C5

Internal Audit Workplan Update

|

S7(2)(b)(i)

The

withholding of the information is necessary to protect information where the

making available of the information would disclose a trade secret.

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to prejudice the supply

of similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

S7(2)(h)

The

withholding of the information is necessary to enable the local authority to

carry out, without prejudice or disadvantage, commercial activities.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C6

DCC External Audit Actions Update - November 2024

|

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to prejudice the supply

of similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C7

Audit Engagement Letter (Draft)

|

S7(2)(i)

The

withholding of the information is necessary to enable the local authority to

carry on, without prejudice or disadvantage, negotiations (including

commercial and industrial negotiations).

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C8

Dunedin City Holdings Ltd - Update on Audit and Risk Activity

|

S7(2)(b)(ii)

The

withholding of the information is necessary to protect information where the

making available of the information would be likely unreasonably to prejudice

the commercial position of the person who supplied or who is the subject of

the information.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C9