|

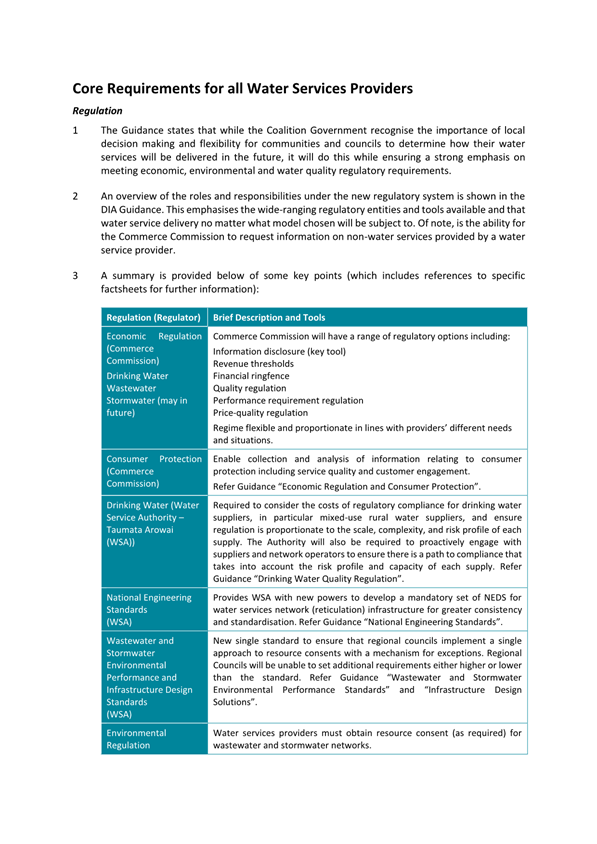

|

Council

26 February 2025

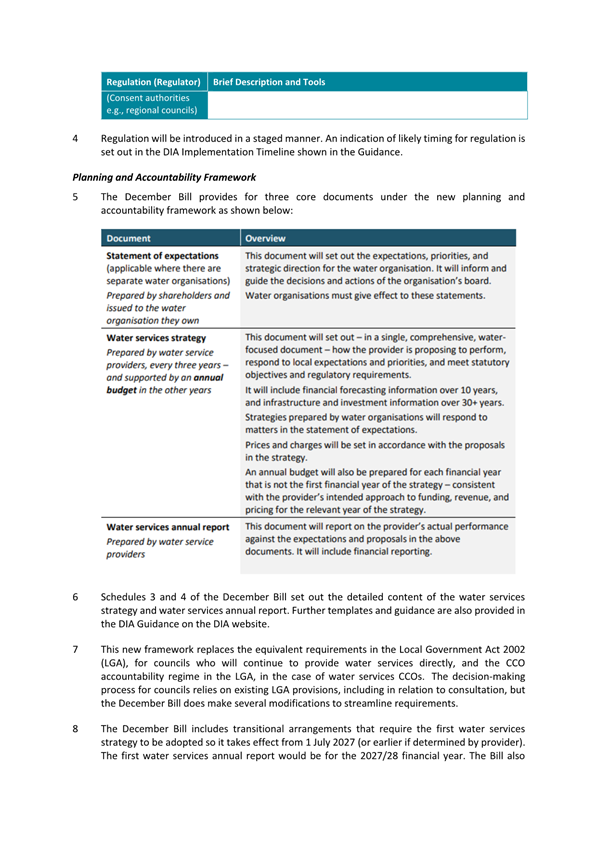

|

Reports

Submission on the Local Government (Water Services) Bill

Department: 3 Waters and Legal Services

EXECUTIVE SUMMARY

1 This

report seeks the Council’s approval of a draft Dunedin City Council (DCC)

submission (Attachment A) to Parliament’s Finance and Expenditure Select

Committee on the Local Government (Water Services) Bill (the Bill). The Bill

was introduced to Parliament on 10 December 2024 and referred to

Parliament’s Finance and Expenditure Committee for consideration. The Committee

is due to report back to Parliament on the Bill by 17 June 2025.

2 This

Bill is the third step in a legislative programme designed to give effect to

the Government’s ‘Local Water Done Well’ policy.

3 The

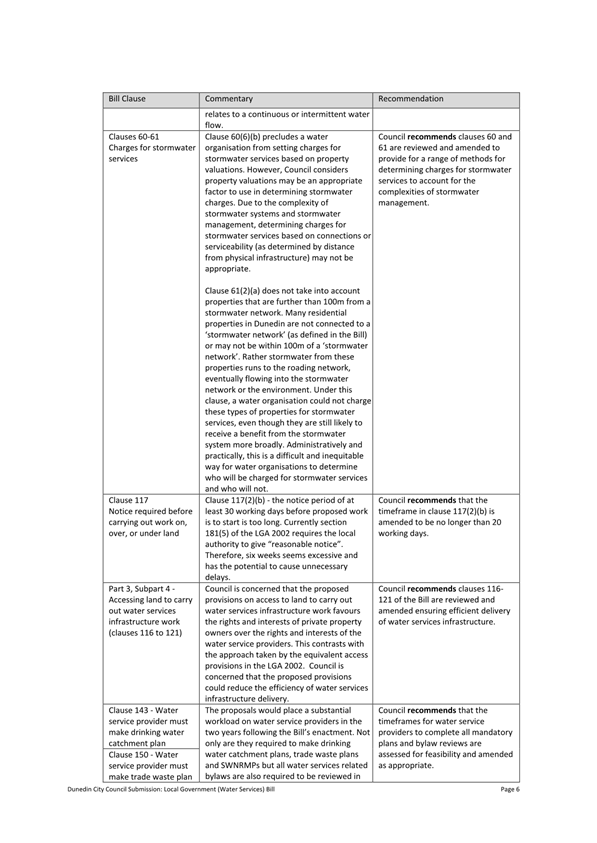

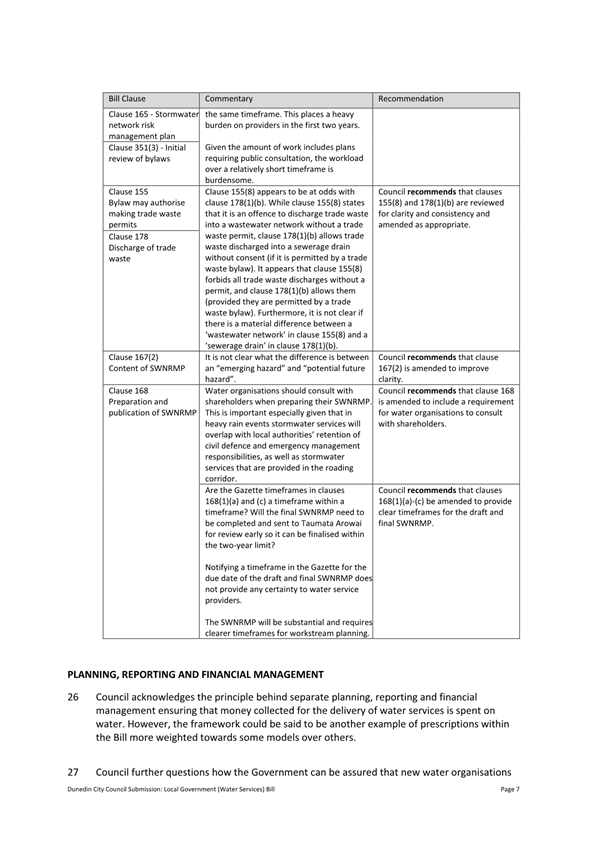

key points from the draft DCC submission relate to:

a) Structural

arrangements;

b) Provision

of water services – operational matters;

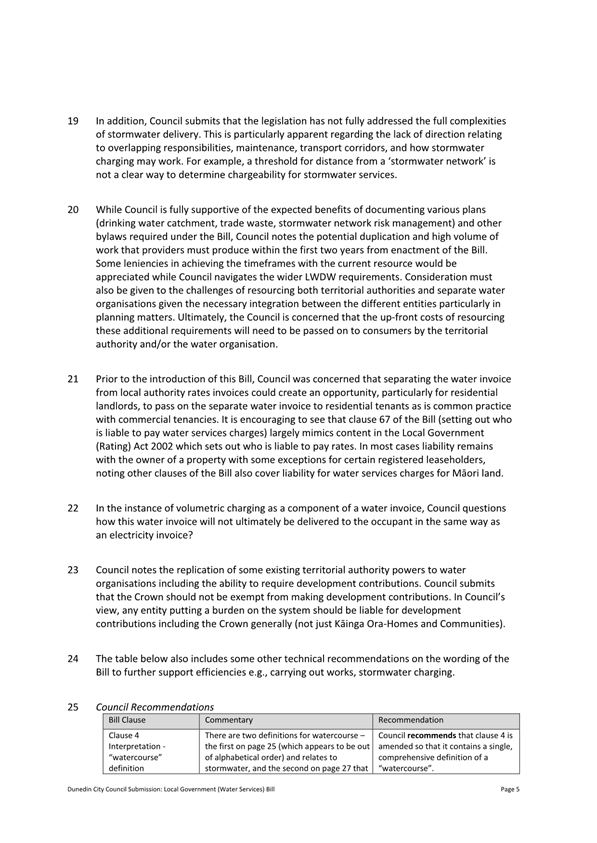

c) Planning,

reporting and financial management;

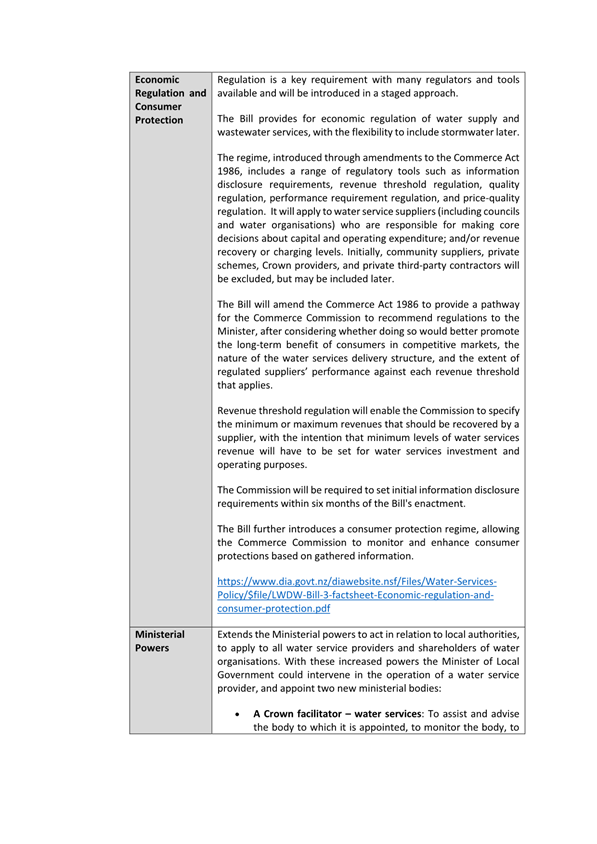

d) Economic

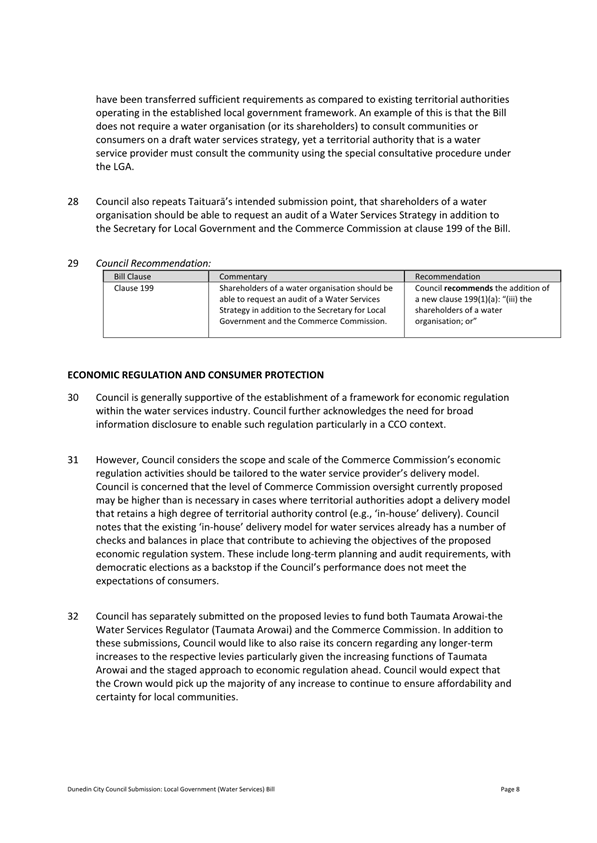

regulation and consumer protection;

e) Taumata

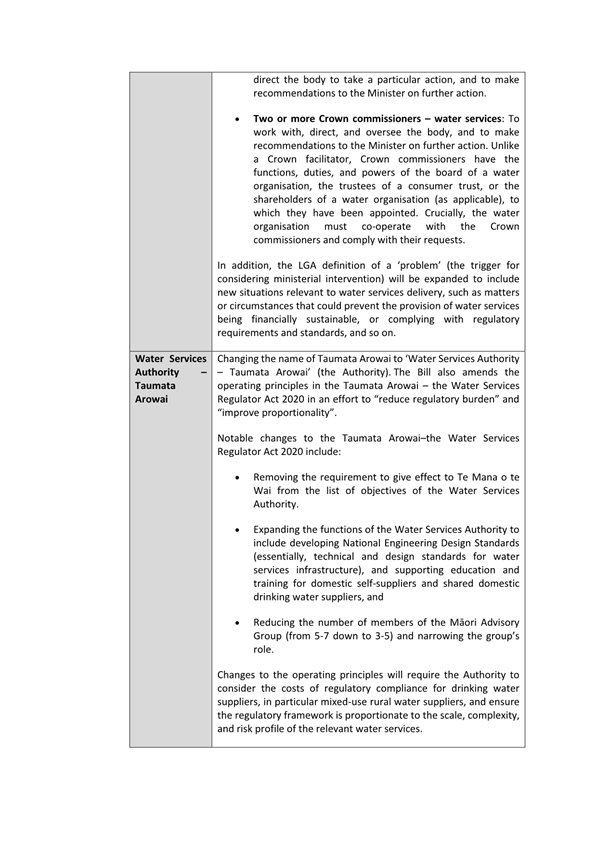

Arowai – the Water Services Regulator;

f) National

Engineering Design Standards for water networks; and

g) Environmental

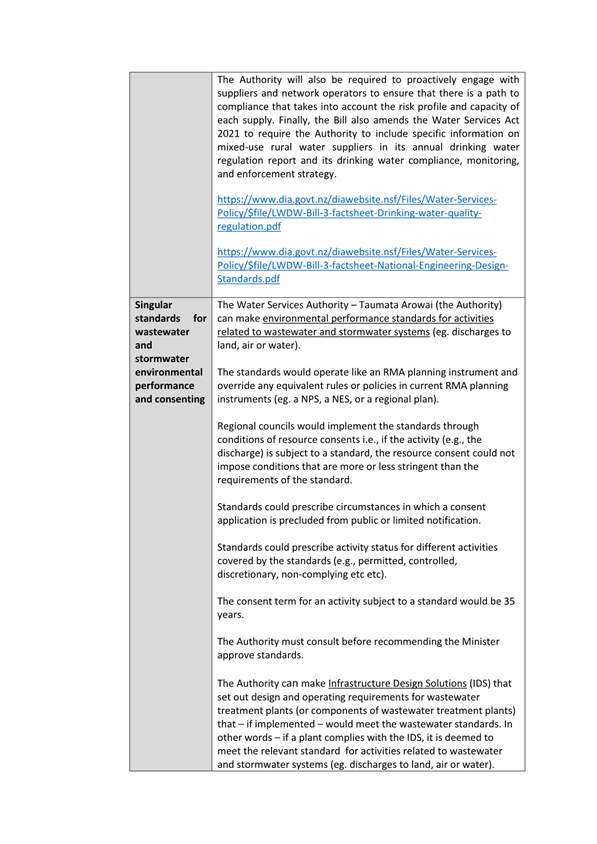

performance standards and infrastructure design solutions for wastewater and

stormwater systems.

4 The

deadline for submissions on the Bill was 23 February 2025. On 20 December 2024

staff requested an extension from the Finance and Expenditure Committee for a

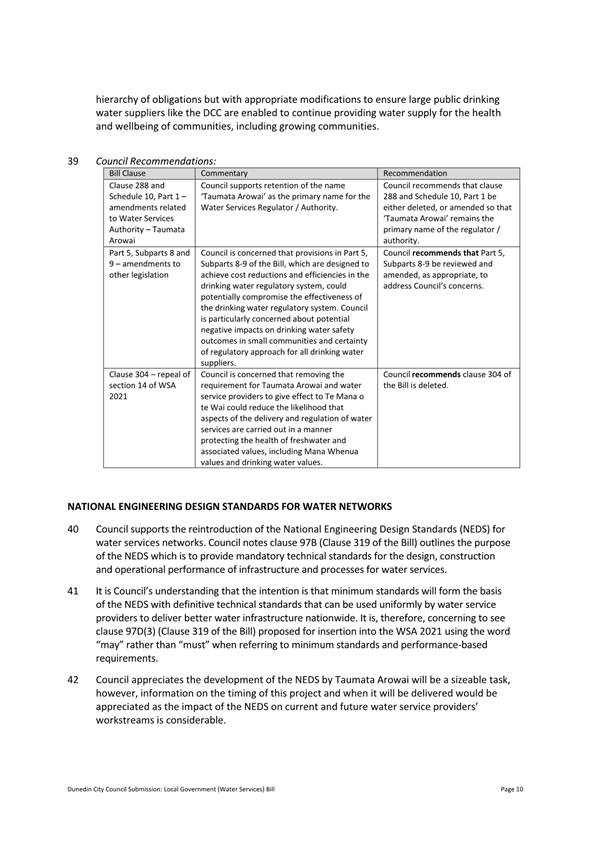

date after the Council meeting of 26 February 2025. An extension was granted on

29 January 2025, with an extended due date of 2 March 2025.

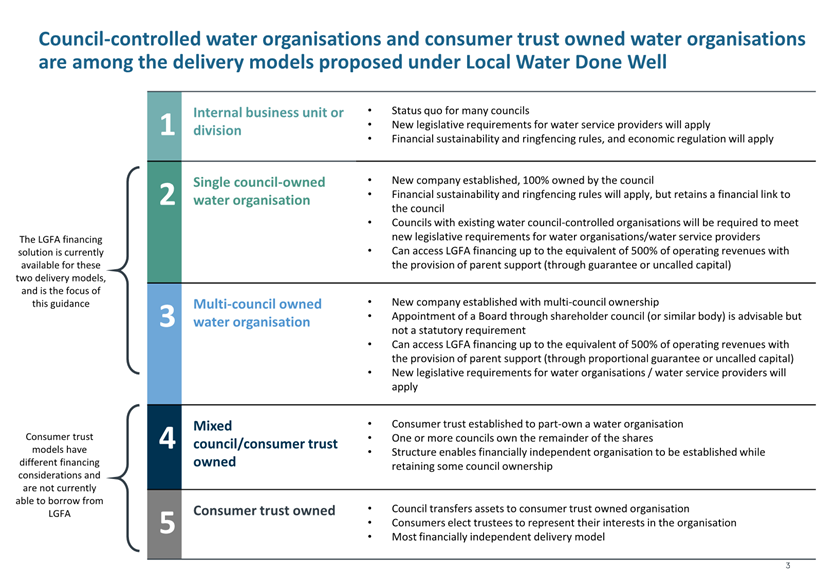

RECOMMENDATIONS

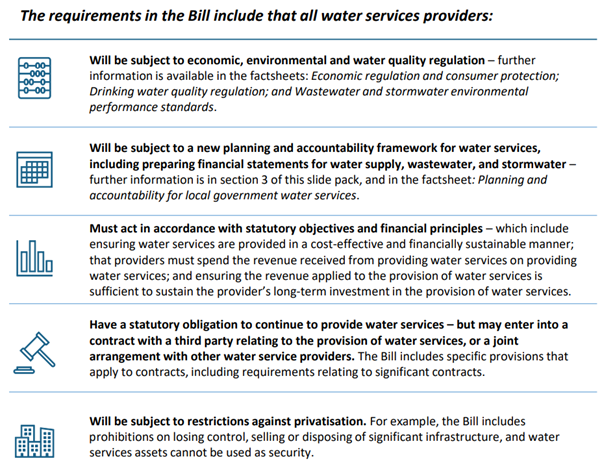

That the Council:

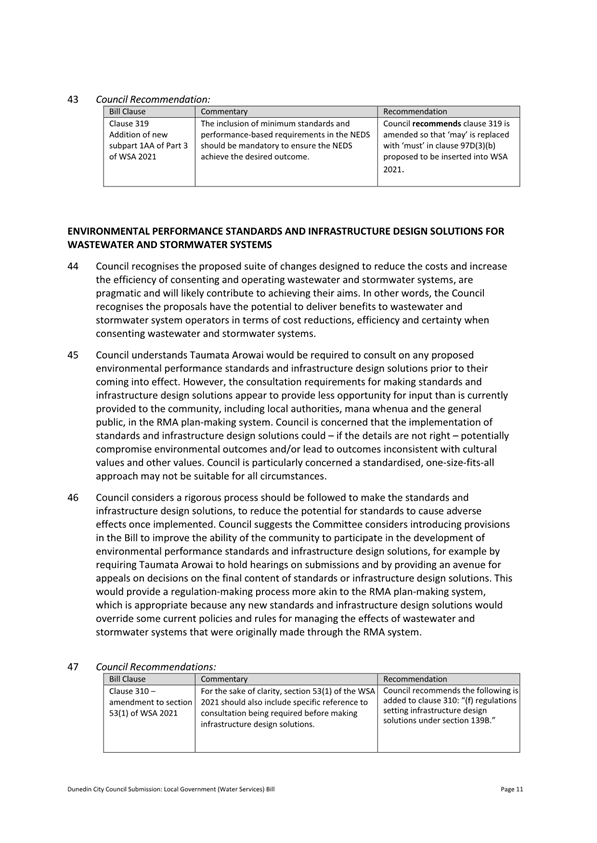

a) Approves the draft DCC

submission to Parliament’s Finance and Expenditure Committee on the Bill.

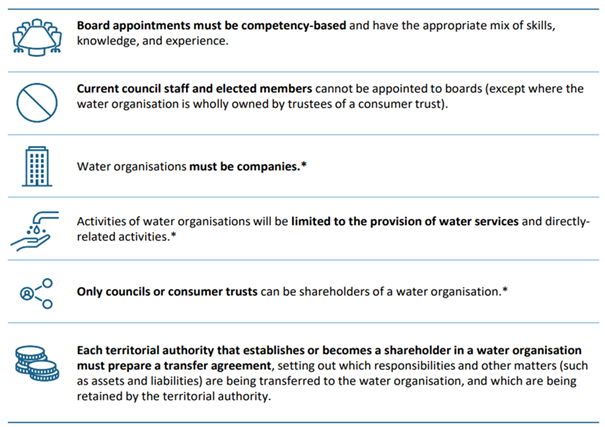

b) Authorises the Mayor

and/or his delegate to speak to the submission.

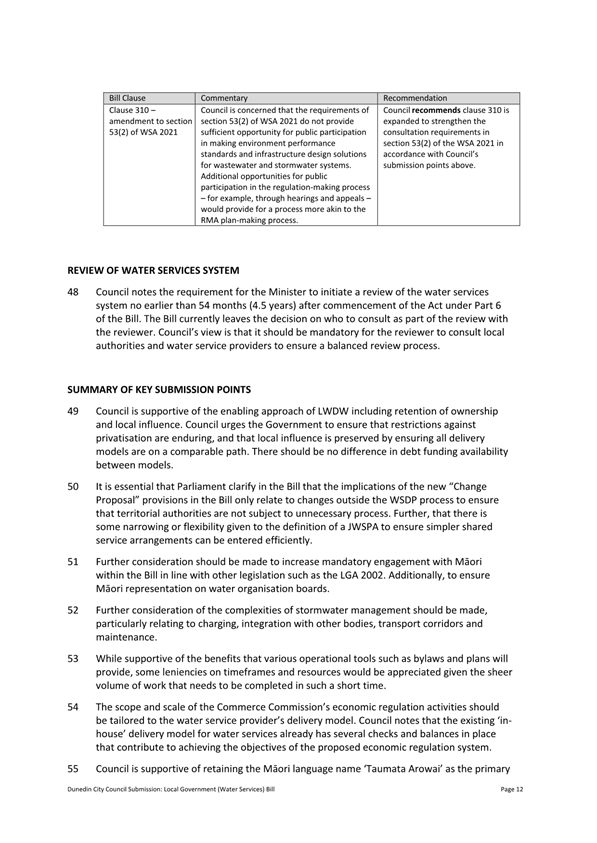

c) Authorises the Chief

Executive to make any minor editorial changes if needed.

BACKGROUND

5 Local

Water Done Well (LWDW) is the Coalition Government’s plan for water

services delivery improvement in New Zealand. LWDW is being implemented in

three stages, each with its own piece of legislation. This Bill is stage three.

6 The

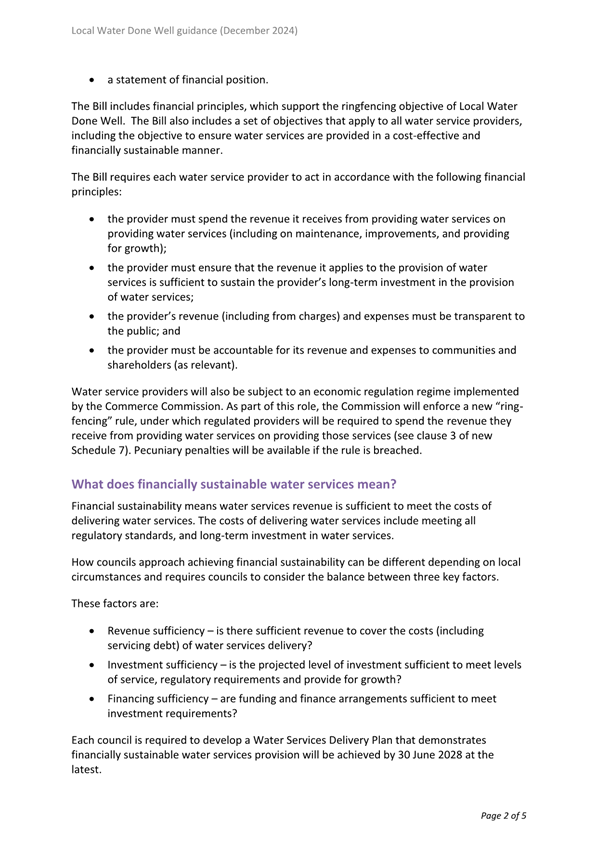

first bill, the Water Services Acts Repeal Act 2024 repealed the previous

Government’s water services reform legislation. The second bill, the

Water Services (Preliminary Arrangements) Act 2024 (Preliminary Act),

established the LWDW framework and the preliminary arrangements for the new water

services system.

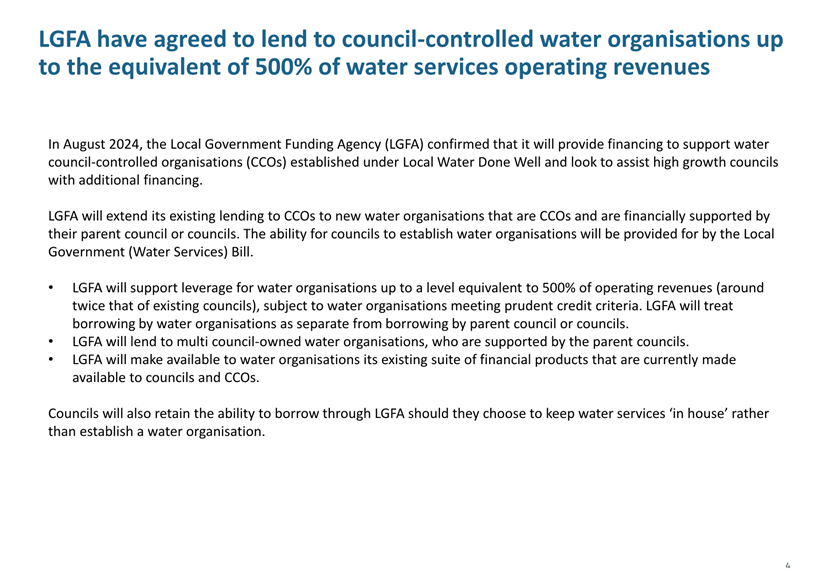

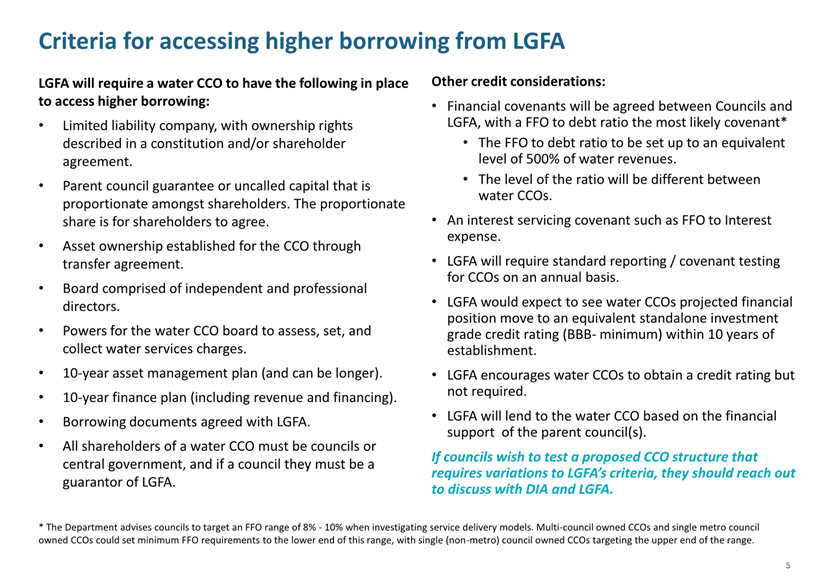

7 The

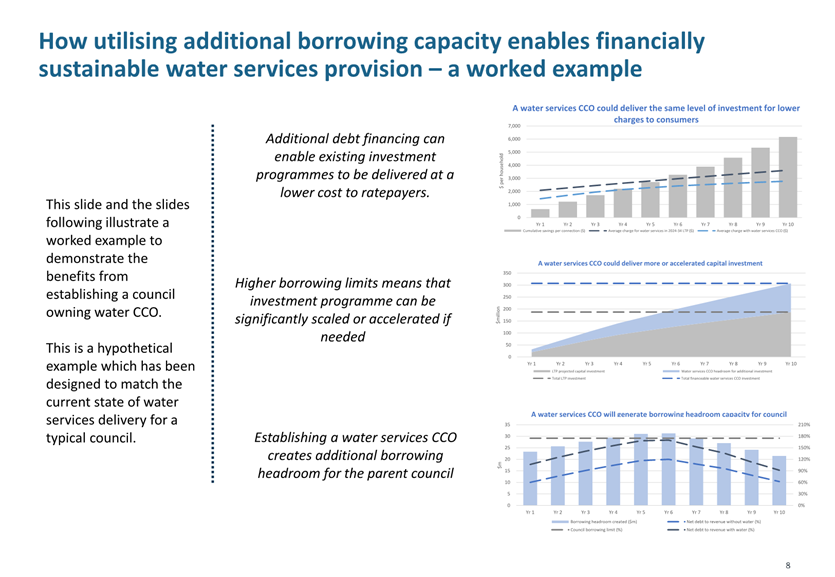

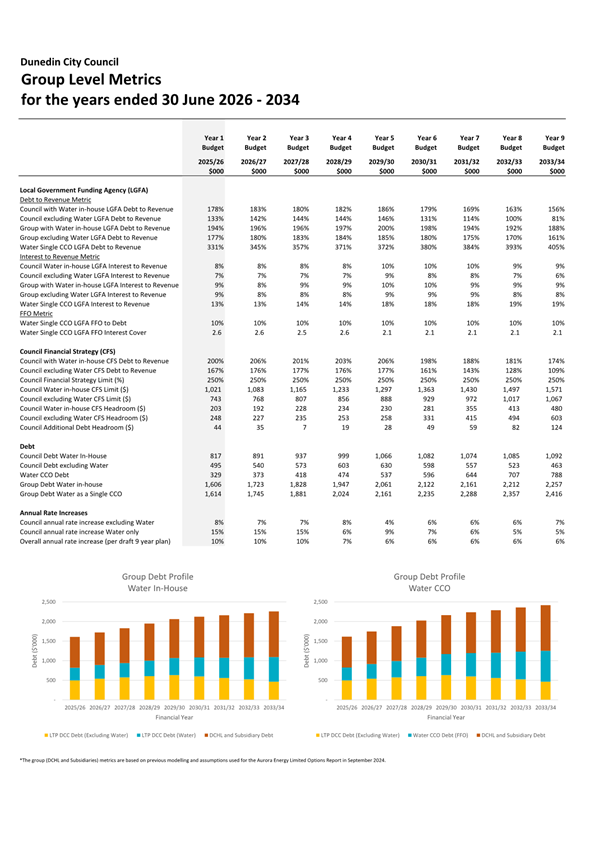

Bill provides for:

a) arrangements

for the new water services delivery system, including both the structural

arrangements and the enduring settings;

b) a new

economic regulation and consumer protection regime for water services; and

c) changes

to the water quality regulatory framework and the water services regulator.

8 The

arrangements for new water services delivery systems include:

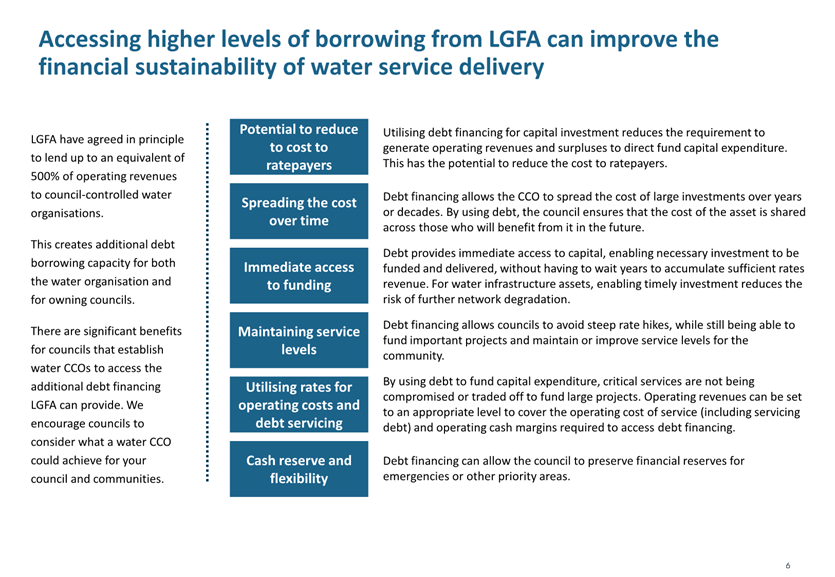

a) structural

arrangements for water services provision such as establishment, ownership, and

governance of water organisations;

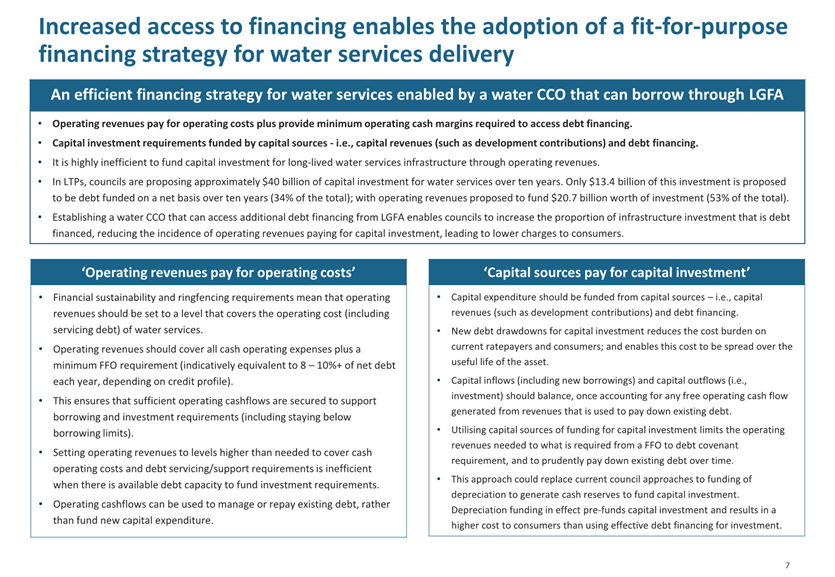

b) operational

matters such as arrangements for charging, bylaws, and management of stormwater

networks; and

c) planning,

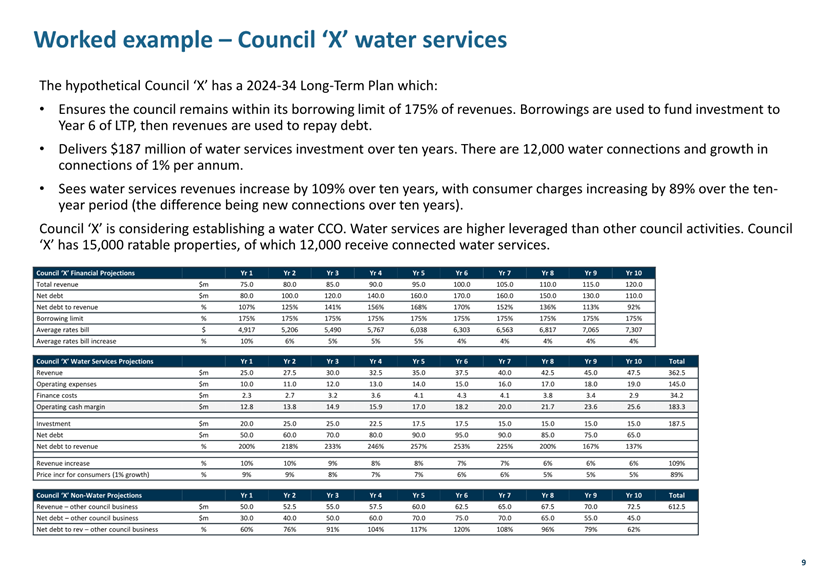

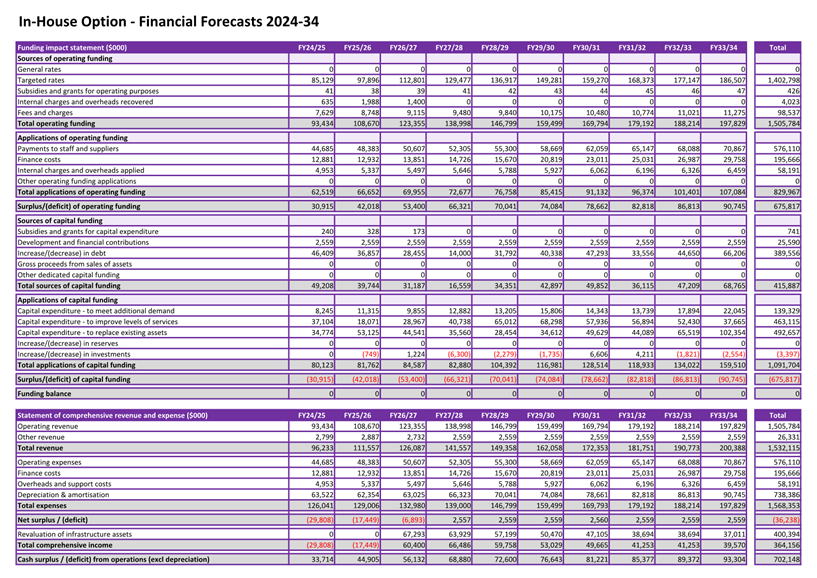

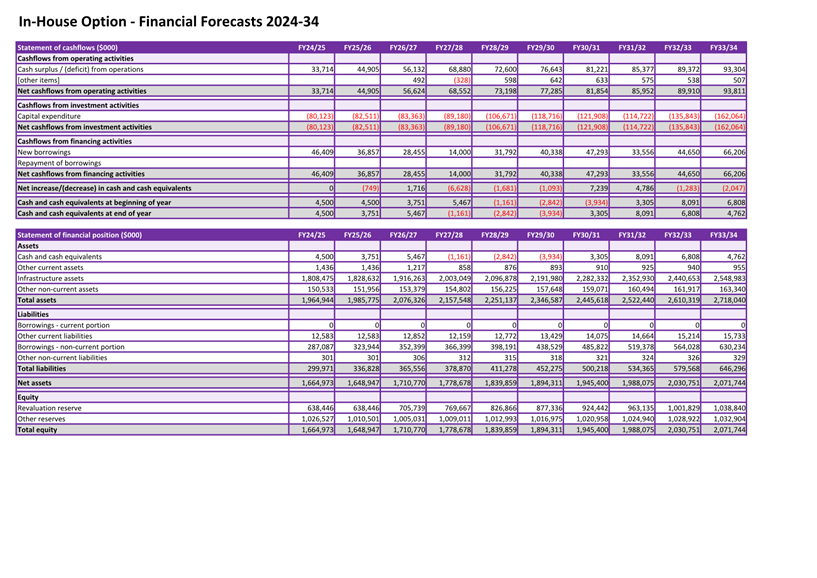

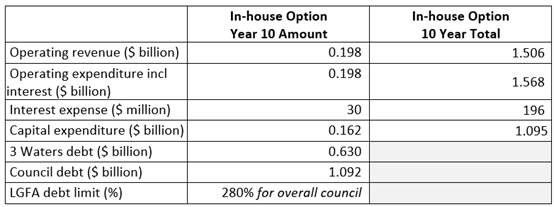

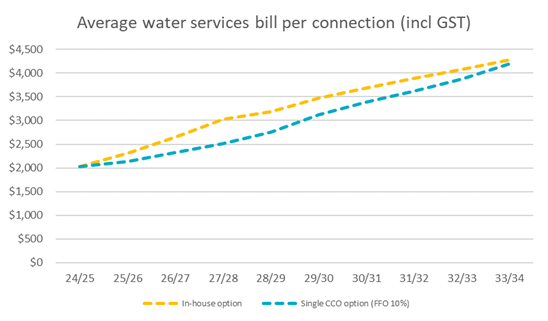

reporting and financial management.

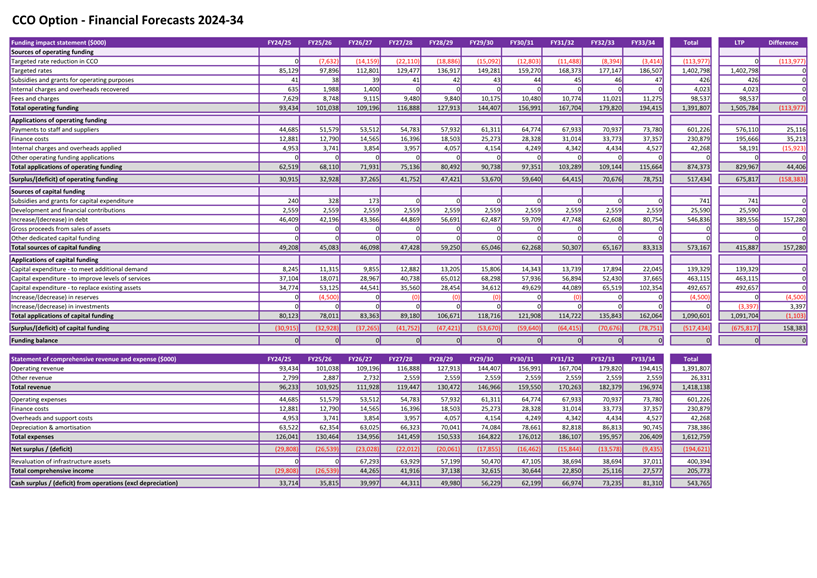

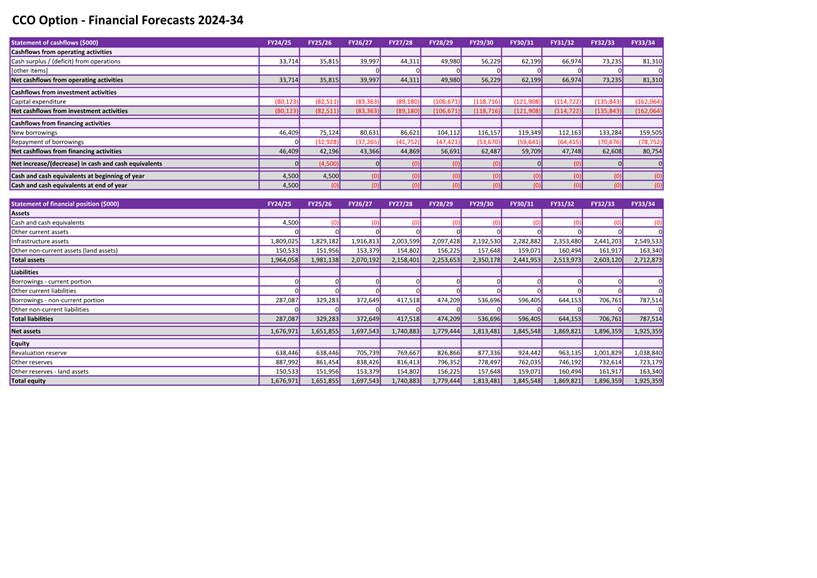

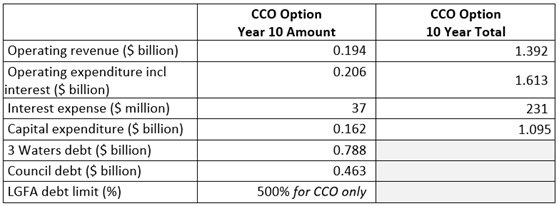

9 The

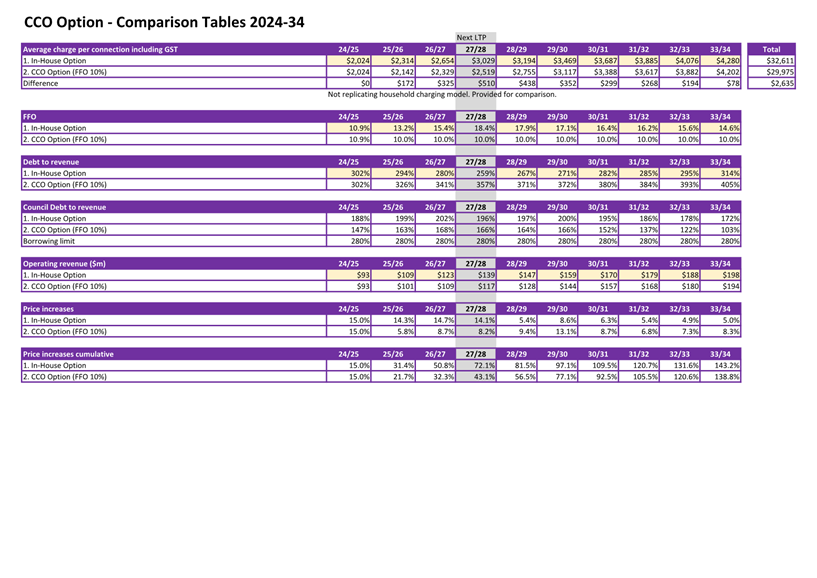

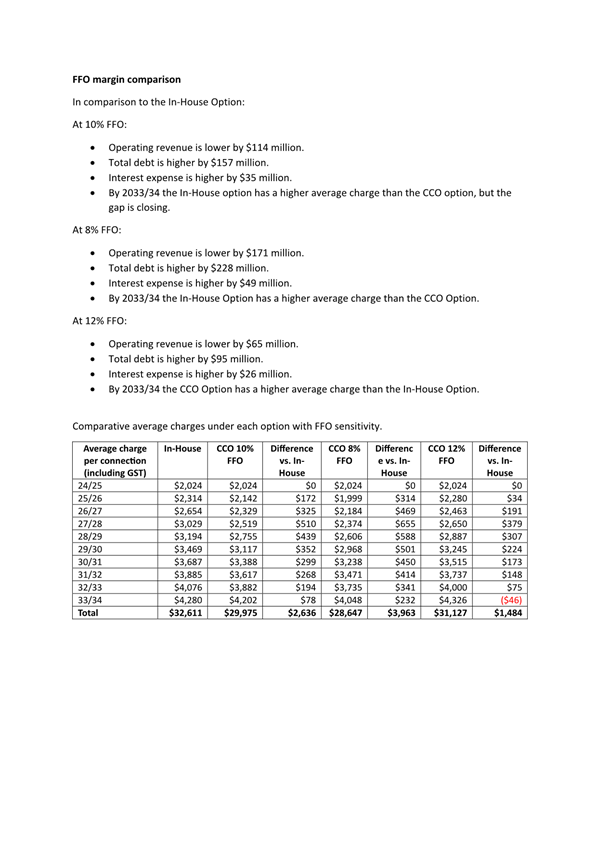

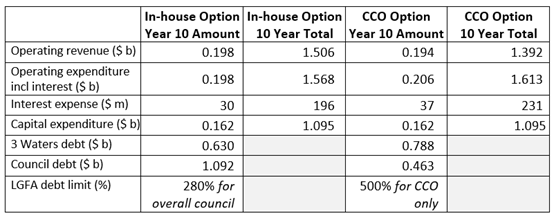

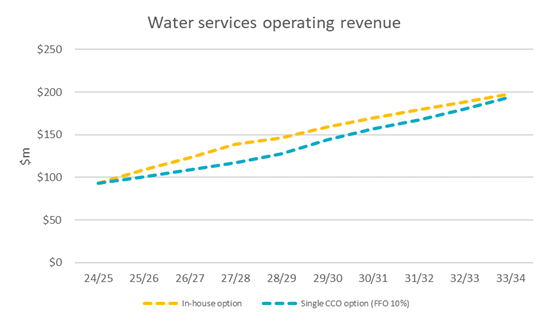

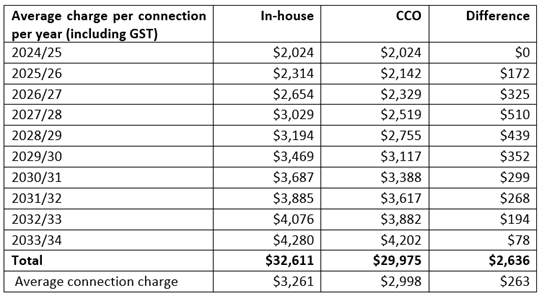

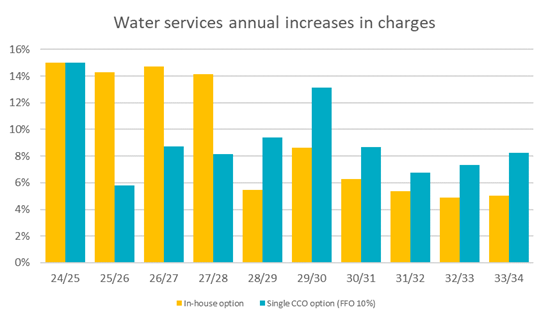

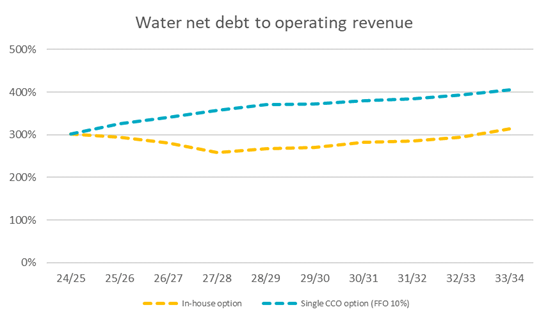

new economic regulation and consumer protection regime in the Bill is based on

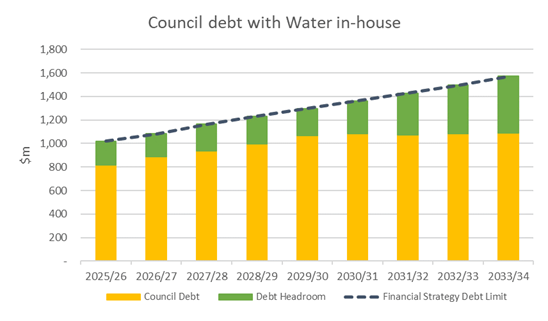

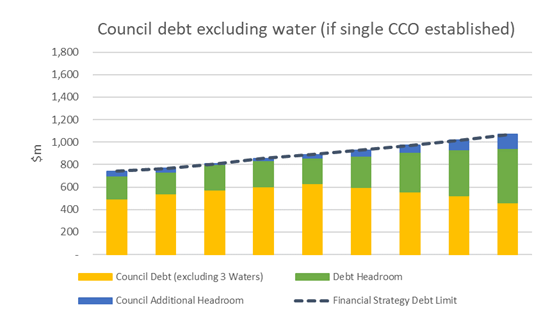

existing economic regulation in the Commerce Act 1986, which already applies to

other industries across New Zealand, e.g., electricity lines services. The

Commerce Commission will also enforce a new “ring-fencing” rule

which requires regulated suppliers to spend the revenue they receive from

providing water services on providing those services.

10 Changes to

the water quality regulatory framework and the water services regulator,

include:

a) change

the Taumata Arowai-the Water Services Regulator Act 2020 to amend the

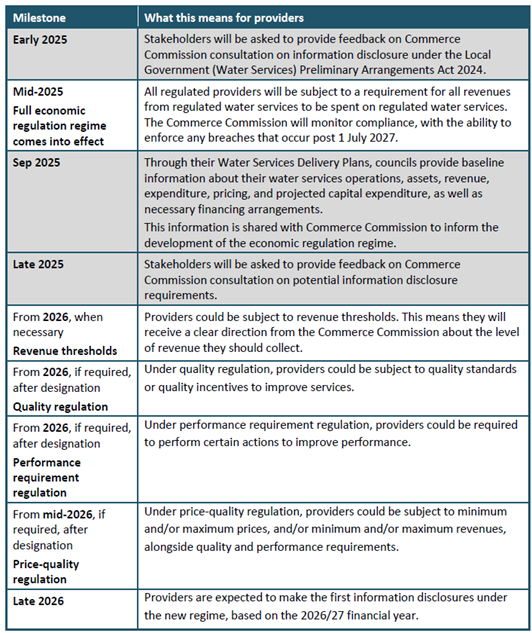

regulator’s name to ‘Water Services Authority – Taumata

Arowai’;

b) changes to

the Water Services Act 2021 (WSA 2021) designed to reduce the regulatory burden

of the drinking water quality regime and improve proportionality in the

application of regulatory powers;

c) a

change in the approach to Te Mana o te Wai; and

d) enabling

the introduction of environmental performance standards for wastewater and

stormwater networks.

11 The Bill is

available on the New Zealand Legislation website: https://www.legislation.govt.nz. A

summary of the Bill can be found at Attachment B.

12 It is

expected the Bill will be enacted in mid-2025.

DISCUSSION

13 The Bill

enables greater flexibility in terms of delivery models and more provision for

local ownership and influence when compared with previous water reform

legislation. As such, DCC’s draft submission is generally supportive of

the Bill and its enabling approach, specifically around ownership and local

influence.

14 The draft

submission states, however, that Council is concerned that the level of

regulation and widening ministerial influence contained in the Bill could have

the effect of diluting Council control, regardless of which water services

delivery model is adopted.

15 Similarly,

the draft submission also states the Bill’s structural arrangements are

more weighted towards some water service delivery models over others, with what

appears to be council controlled organisations being given more benefits (e.g.,

higher debt level thresholds) than in-house delivery models.

16 The draft

submission urges the Government to ensure that restrictions against

privatisation are enduring, and that local influence is preserved.

Structural

Arrangements

17 The draft

submission questions aspects of the structural arrangements outlined in the

Bill including comprehensive and staged economic regulation and different debt

leverage percentages for different water service models. Of most immediate

concern, however, is the conflicting consultation provisions between the

Preliminary Act and the Bill, and the draft submission requests clarification

to ensure a “Change Proposal” only relates to changes outside the

Water Services Delivery Plan process so that Council is not subject to

unnecessary consultative processes.

18 Further,

the draft submission states the definition of Joint Water Service Provider

Arrangement (JWSPA) is too wide and requests there is a narrowing or

flexibility given to the definition of a JWSPA to ensure simpler shared service

arrangements can be efficiently entered. Further that there is an explicit

exemption for contractual shared service arrangements from the new Change

Proposal provisions.

19 The Bill

provides limited mandated direction on mana whenua participation in water

service delivery. The Bill states that water service providers must act in a

manner that is consistent with Treaty settlement obligations, and shareholding

councils may set expectations for how water organisations conduct its

relations with Māori in the Statement of Expectations. The draft

submission urges the Select Committee to consider amending the Bill to mandate

engagement with Māori in line with other legislation e.g., Local

Government Act 2002, as well as a requirement to include Māori

representation on the board of a water organisation.

Provision of

Water Services – Operational Matters

20 The Bill

provides tools designed to improve operational efficiencies and manage risks,

including management plans and bylaws relating to drinking water catchments,

trade waste and stormwater networks (including private watercourses). The draft

submission states that, given the complexities of stormwater, further

consideration is needed in relation to the integration of its management with

asset owners, property owners and regulators, the management transport

corridors, infrastructure maintenance, and how charging for stormwater may

work.

21 The Bill

requires water service providers to produce a drinking water catchment plan, a

trade waste plan, and stormwater network risk management plan in the first two

years after the Bill’s enactment. Within the same timeframe, all water

services bylaws must also be identified and reviewed. A plan must also be developed

for each where they are either amended, revoked, or revoked and replaced.

22 Given the

high volume of work for water service providers within the first two years post

enactment of the Bill, relating to reviewing and/or preparing new bylaws and

producing management plans, the draft submission requests some leniencies on

timeframe given resource limitations.

23 The Bill

specifies who can be charged for water services as the customer. These

provisions are consistent with the provisions in the Local Government (Rating)

Act 2002 that set out who is liable to pay rates. The draft submission supports

this approach.

24 The Bill

allows for the Crown to be exempt from paying development contributions. The

draft submission opposes Crown exemption and states that any entity putting a burden

on the system should be liable for development contributions.

Planning,

Reporting and Financial Management

25 The Bill

sets out new planning, reporting and financial management requirements for all

water service providers. The requirements include a statement of expectations

(for shareholders to provide to water organisations), a water services strategy,

water services annual budget, and a water services annual report.

26 The draft

submission states that Council acknowledges the principle of separate planning,

reporting and financial management to ensure that money collected for the

delivery of water services is spent on water. However, Council questions

whether the new planning and accountability framework is another example of

prescriptions within the Bill that are more weighted towards some models over

others.

Economic

Regulation and Consumer Protection

27 The Bill

provides for the establishment of an economic and consumer protection system to

be overseen by the Commerce Commission. Water service providers would be

subject to core regulatory requirements, including information disclosure

requirements, and may be subject to further regulation as determined by the

Commerce Commission.

28 The draft

submission states Council is generally supportive of the new economic

regulation framework for water services, but that it considers the scope and

scale of the Commerce Commission’s economic regulation activities should

be tailored to the water service provider’s delivery model.

29 Further,

the draft submission states that the level of oversight that is proposed for

the Commerce Commission may be higher than is necessary in cases where

territorial authorities adopt a delivery model that retains a high degree of

control (e.g., in-house delivery). Council notes that the existing

‘in-house’ delivery model for water services already has several

checks and balances that contribute to achieving the objectives of the proposed

economic regulation system.

Taumata

Arowai – the Water Services Regulator

30 The Bill

would amend existing legislation to change the name of Taumata Arowai –

the Water Services Regulator. These amendments would give effect to the

Government’s preference for Government agencies to have an English

language name first. The draft submission expresses support for retention of

‘Taumata Arowai’ as the primary name for the water services

regulator / authority.

31 Parts of

the Bill have been designed to reduce the cost and burden for drinking water

suppliers associated with complying with the WSA 2021. These include:

a) adding a

requirement to take compliance costs into account in Taumata Arowai’s

operating principles;

b) adding scope for

Taumata Arowai to grant general exemptions to drinking water suppliers from

regulatory requirements in order to provide flexibility where compliance is

impractical, inefficient, unduly costly or unduly burdensome;

c) excluding

‘shared domestic drinking water supplies’ (i.e., supplies servicing

up to 25 consumers for domestic use) from the requirements of the drinking

water regulatory system;

d) excluding

community drinking water supplies serving fewer than 25 consumers from the

requirement to have a drinking water safety plan; and

e) adding a

definition of ‘mixed-use rural water scheme’ and requirements for

Taumata Arowai to tailor aspects of its regulatory approach to these supplies.

32 The draft

submission states that although Council recognises the proposed changes are

likely to be pragmatic and will likely reduce costs, it is concerned the

changes should not come at the expense of drinking water safety outcomes. This

is particularly the case in communities serviced by domestic self-suppliers or

shared domestic drinking water suppliers that may be more vulnerable to

drinking water safety issues.

33 The draft

submission also states the Council does not support the proposed amendment to

the WSA 2021 that would remove the requirements for Taumata Arowai and water

service providers to give effect to the Te Mana o te Wai hierarchy of

obligations. Council is concerned this may have an adverse effect on the health

of freshwater and associated values, including mana whenua and drinking water values.

National

Engineering Design Standards for Water Networks

34 The Bill

reintroduces the National Engineering Design Standards (NEDS) for water

services networks. The NEDS, which were part of the previous reform, would

provide mandatory technical standards for the design, construction and

operational performance of infrastructure and process. The draft submission

supports the reintroduction of the NEDS, however, it requests further

information regarding the timing of these standards given their significant

impact on water service providers’ workstreams.

Environmental

Performance Standards and Infrastructure Design Solutions for Wastewater and

Stormwater Systems

35 The Bill

proposes a suite of changes designed to reduce the costs and increase the

efficiency of consenting and operating wastewater and stormwater systems. These

include:

a) amendments

to Taumata Arowai’s existing powers to make environmental performance

standards for wastewater and stormwater networks – these would be single

(not maximum or minimum) standards that would be implemented through resource

consents; and

b) providing

Taumata Arowai with powers to introduce infrastructure design solutions, which

would set

out design and operating requirements for wastewater treatment plants (or

components of wastewater treatment plants) that – if implemented –

would meet applicable wastewater environmental performance standards.

36 The draft

submission states that these changes are pragmatic, however, additional

opportunities should be provided for interested parties to participate in the

process of making environmental performance standards and infrastructure design

solutions for wastewater and stormwater systems.

37 Further,

the draft submission states that following a robust process to develop the

content of these tools will reduce the risk that their implementation

unintentionally leads to adverse effects on environmental or cultural values.

OPTIONS

Option One – Submit on the Local Government (Water

Services) Bill (Recommended Option)

38 Approve,

with any suggested amendments, the draft submission to the Finance and

Expenditure Select Committee on the Local Government (Water Services) Bill

(Attachment A).

39 There is no

impact on debt, rates, and city-wide and DCC emissions.

Advantages

· Opportunity

to provide feedback on implementation of the Government’s ‘Local Water

Done Well’ plan.

· Opportunity

to recommend changes to Parliament’s Finance and Expenditure Committee on

particular provisions of the Bill.

Disadvantages

· There

are no identified disadvantages for this option.

Option Two – Do not submit on the Local Government

(Water Services) Bill

40 Do not

approve the draft submission (Attachment A).

41 There is no

impact on debt, rates, and city-wide and DCC emissions.

Advantages

· There

are no identified advantages for this option.

Disadvantages

· Missed

opportunity to provide feedback on implementation of the Government’s

‘Local Water Done Well’ plan.

· Missed

opportunity to recommend changes to Parliament’s Finance and Expenditure

Committee regarding the provisions of the Bill.

NEXT STEPS

42 If

approved, the draft submission will be finalised and sent to Parliament’s

Finance and Expenditure Committee by 2 March 2025.

Signatories

|

Author:

|

Katherine Quill - Policy Analyst

Scott Campbell - Regulation and Policy Team Leader

Nadia McKenzie - In-House Legal Counsel

|

|

Authoriser:

|

David Ward - General Manager, 3 Waters and Transition

Karilyn Canton - Chief In-House Legal Counsel

|

Attachments

|

|

Title

|

Page

|

|

⇩a

|

Draft DCC submission -

Local Government (Water Services) Bill

|

13

|

|

⇩b

|

Summary of the Local

Government (Water Services) Bill

|

26

|

|

SUMMARY OF CONSIDERATIONS

|

|

Fit with purpose of Local Government

This decision enables democratic local

decision making and action by, and on behalf of communities,

and promotes the social, economic,

environmental and cultural well-being of communities in the present and for

the future.

|

|

Fit with strategic framework

|

|

Contributes

|

Detracts

|

Not applicable

|

|

Social Wellbeing Strategy

|

☐

|

☐

|

✔

|

|

Economic Development Strategy

|

☐

|

☐

|

✔

|

|

Environment Strategy

|

✔

|

☐

|

☐

|

|

Arts and Culture Strategy

|

☐

|

☐

|

✔

|

|

3 Waters Strategy

|

✔

|

☐

|

☐

|

|

Future Development Strategy

|

✔

|

☐

|

☐

|

|

Integrated Transport Strategy

|

☐

|

☐

|

✔

|

|

Parks and Recreation Strategy

|

☐

|

☐

|

✔

|

|

Other strategic projects/policies/plans

|

✔

|

☐

|

☐

|

This report has been prepared with reference to the

Dunedin strategic framework.

|

|

Māori Impact Statement

The draft submission urges Parliament to further mandate

engagement by water service providers with Māori in line with other

existing legislation. The draft submission also states it does not support

the proposed amendment to the Water Services Act 2021 that would remove the

requirements for Taumata Arowai and water service providers to give effect to

Te Mana o te Wai hierarchy of obligations.

|

|

Sustainability

Financial sustainability of local government water

services is a key objective of the Government’s “Local Water Done

Well” plan. The suite of legislation is designed to implement this

programme and ensure delivery of water services is financially sustainable.

The draft submission states it does not support the

proposed amendment to the Water Services Act 2021 that would remove the

requirements for Taumata Arowai and water service providers to not give

effect to Te Mana o te Wai hierarchy of obligations, as this may have an

adverse effect on environmental values.

The draft submission also states that a robust process

needs to be followed when developing the content of the Environmental

Performance Standards and Infrastructure Design Solutions for Wastewater and

Stormwater Systems to ensure there are no adverse effects on the environment.

|

|

Zero carbon

There

is no impact on city-wide or DCC emissions directly associated with this

report and the decision to approve the draft submission to Parliament’s

Finance and Expenditure Committee.

|

|

LTP/Annual Plan / Financial Strategy /Infrastructure

Strategy

This report and the decision to approve the submission to

Parliament’s Finance and Expenditure Committee have no direct implications

for these plans and strategies.

|

|

Financial considerations

There are no financial implications directly associated

with this report and the decision to approve the draft submission to

Parliament’s Finance and Expenditure Committee.

|

|

Significance

The decision to approve the draft DCC submission is

considered low in terms of the Council’s Significance and Engagement

Policy.

|

|

Engagement – external

A workshop was held with Councillors on Friday 14 February

2025 to inform the development of the draft submission. The workshop was open

to the public.

|

|

Engagement - internal

Staff from the Legal Team, 3 Waters Group, and Executive

Leadership Team have contributed to the development of the draft DCC

submission.

|

|

Risks: Legal / Health and Safety etc.

There are no identified risks directly related to the DCC

submission on the Local Government (Water Services) Bill.

|

|

Conflict of Interest

There is no known conflict of interest.

|

|

Community Boards

Community Boards are likely to be interested in the

proposed water services delivery changes and staff will consider how to

update the Community Boards.

|

|

|

Council

26 February 2025

|

Local Water Done Well - Decision on water

models for consultation

Department: Legal Services, Finance and 3 Waters

EXECUTIVE SUMMARY

1 The

purpose of this report is to provide information and analysis so that Council

can decide, for the purposes of consultation, on:

a) its

preferred water services delivery model (Preferred Option); and

b) what

other option(s) it will consult on (Alternative Option(s))

(together, referred to as “the Water Consultation

Options”).

2 Staff

recommend the following two options as the Water Consultation Options:

a) in-House

delivery of 3 Waters (In-House Option); and

b) an

asset owning council-controlled organisation for 3 Waters, with Council as the

sole shareholder (CCO Option).

3 It

is for Council to decide whether it prefers the In-House Option, the CCO Option

or any other option. This will require careful weighting by Council of

financial and non-financial considerations.

4 This

report provides detailed information to help inform Council’s decision,

including information on:

a) Financial

and non-financial considerations;

b) the

Local Government (Water Services Preliminary Arrangements) Act 2024

(Preliminary Act); and

c) the

Local Government (Water Services) Bill 2024 (December Bill).

5 There

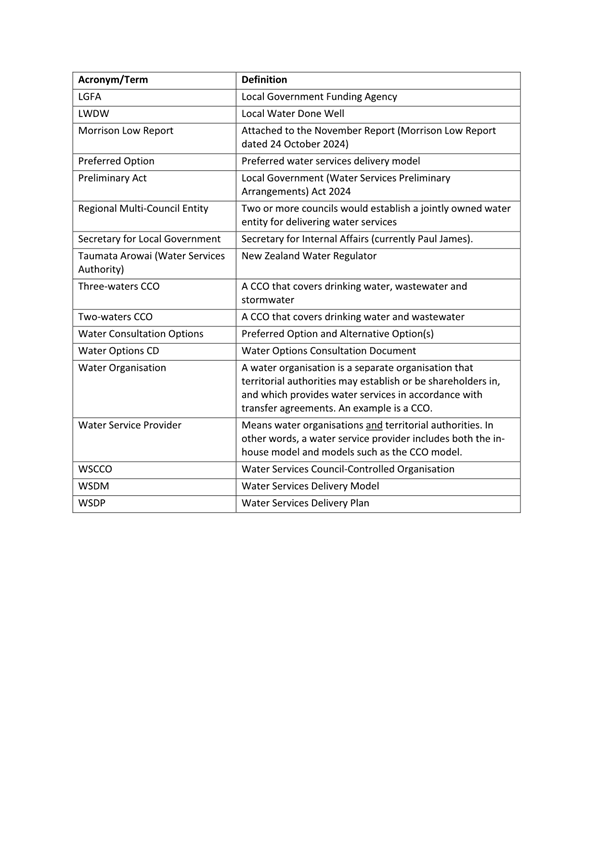

are a lot of acronyms and definitions used in the context of water

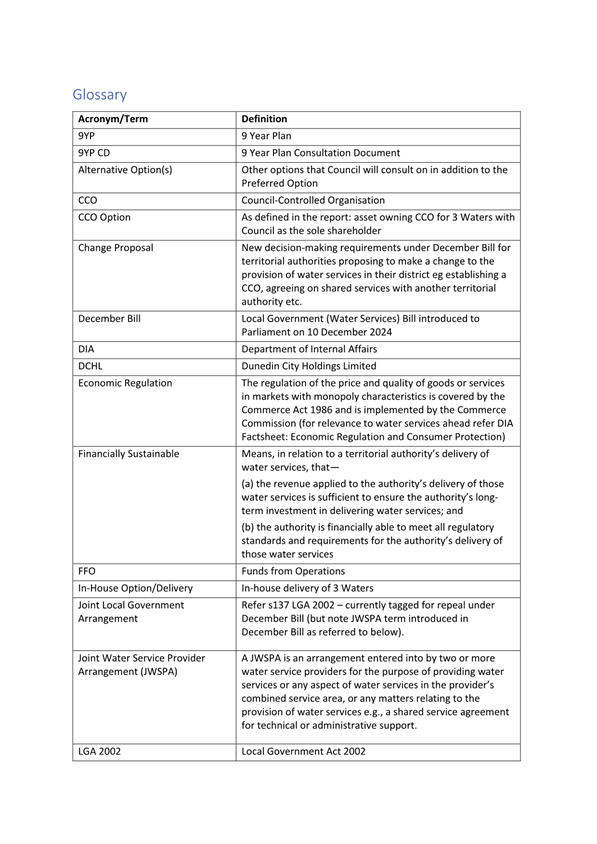

reforms. A glossary is attached as Attachment A.

RECOMMENDATIONS

That the Council:

a) Decides to consult on the following two options under the Local

Government (Water Services Preliminary Arrangements) Act 2024:

i) In-House delivery of 3 Waters (the

In-House Option); and

ii) An asset owning CCO for 3 Waters, with

Council as the sole shareholder (the CCO Option).

b) Decides that its Preferred Option for consultation is the In-House Option.

c) Notes that there will be a report to Council on 18 March 2024

asking Council to approve the water options consultation document.

BACKGROUND

Water

Services Reform

Local Water Done

Well

6 The

Government is now in the final stage of their three-stage process implementing

its “Local Water Done Well” (LWDW) reform programme.

7 The

first stage of LWDW saw the repeal of legislation relating to large water

services entities. This was in February 2024.

8 The

second stage of LWDW was implemented with the passing of the Preliminary Act on

2 September 2024. As a result, Council is required to prepare and submit a WSDP

to the Secretary for Local Government by 3 September 2025.

9 The

third stage of LWDW is now underway with the introduction of the December Bill

on 10 December 2024. The December Bill provides the enduring settings for LWDW

including the framework for economic regulation as well as the more detailed

powers and duties for service delivery models.

10 Further

information on the Preliminary Act and the December Bill is included later in

this report.

Requirement for a

Water Services Delivery Plan

11 Council’s

immediate action resulting from the Preliminary Act is to prepare and submit a

WSDP to the Secretary for Local Government by 3 September 2025.

12 As

reported to Council in earlier reports, the WSDP requires information on the

WSDM including:

a) the

anticipated or proposed WSDM or arrangements for delivering water services;

b) a

summary of consultation undertaken as part of developing the WSDM; and

c) an

implementation plan for delivering the WSDM.

13 If

Council decided to enter a joint arrangement with one or more other territorial

authorities, it could choose to prepare and submit a joint WSDP.

14 There

is an opportunity to amend a WSDP within a specified timeframe if the proposed

amendments are significant and necessary due to exceptional circumstances.

15 Council

is required by law to give effect to the proposals or undertakings specified in

the WSDP. Not doing so could be a ground for appointing a Crown

facilitator.

Timeline and Process

16 DIA’s

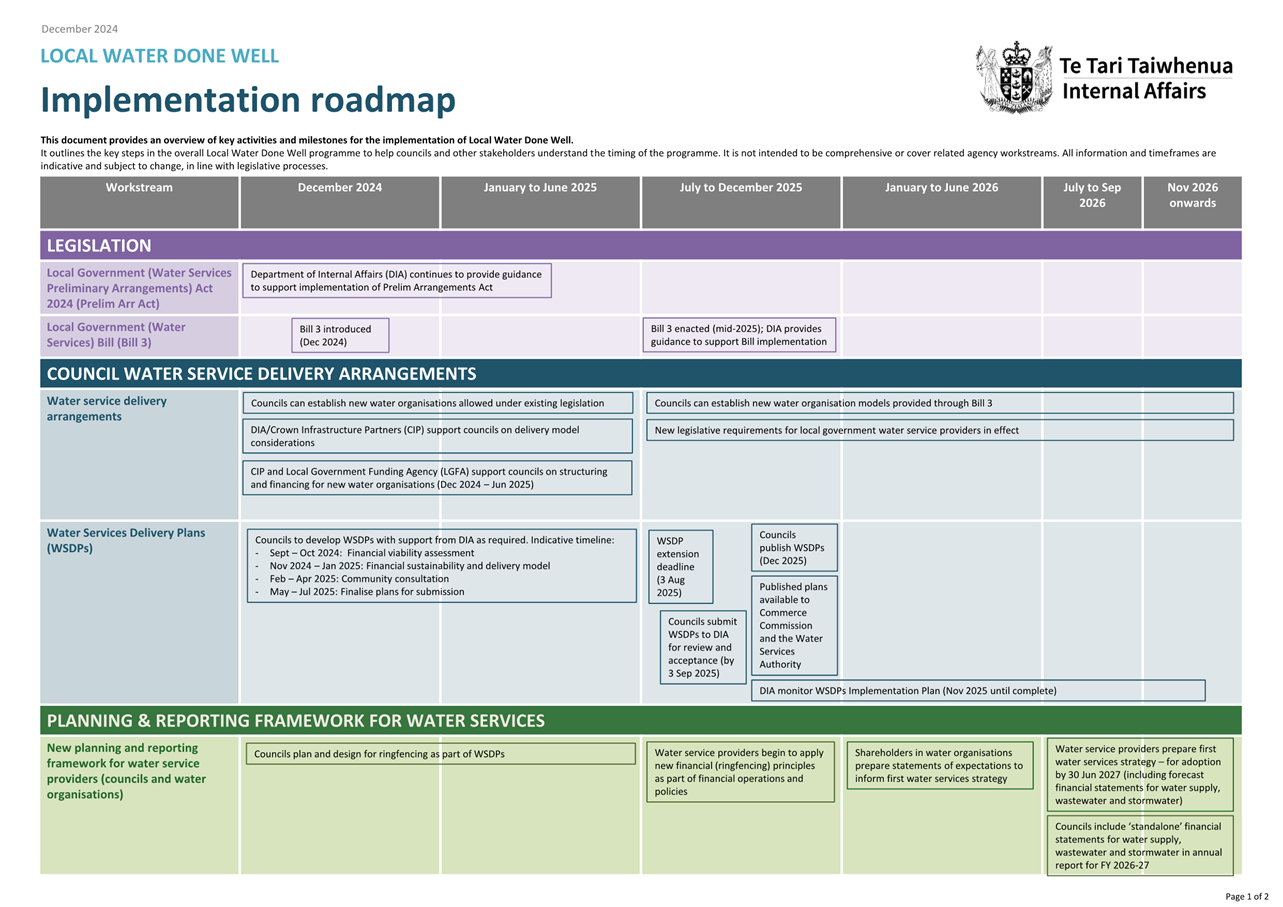

implementation roadmap for LWDW is shown at Attachment B.

17 DIA

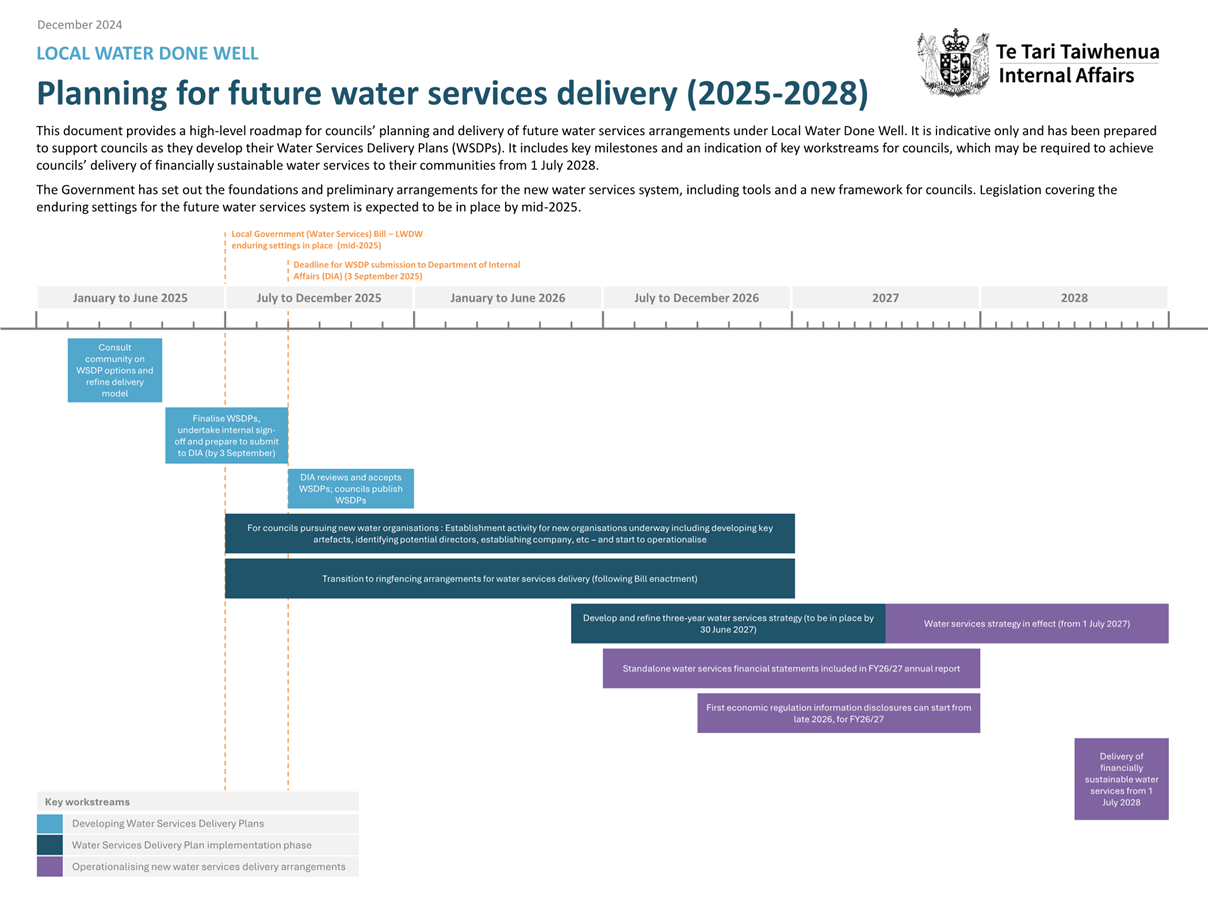

has also provided a high-level roadmap for Council’s planning and

delivery, as shown at Attachment C.

18 Staff

have presented on the WSDP (including on possible WSDMs) to Council at various

workshops and meetings since the passing of the Preliminary Act on 2 September

2024. Council adopted a shortlist of three WSDM options at its Council meeting

on 25 November 2024: https://infocouncil.dunedin.govt.nz/Open/2024/11/CNL_20241125_AGN_3009_AT_WEB.htm

An

overview of the December Bill

19 The

December Bill is currently going through the Parliamentary process and will be

subject to amendment. It is anticipated that the December Bill will be enacted

in mid-2025 and that most of the content will come into effect the day after

Royal Assent.

20 Staff

have prepared a draft submission on the December Bill. Councillors have had the

opportunity to provide feedback through a workshop. Adoption of the submission

is the subject of another Council Report on 26 February 2025.

21 It

is expected that the December Bill will be divided during the Parliamentary

process into two separate Bills (perhaps intended to separate the standalone

provisions of the December Bill and the amendments to several other Acts). The

two likely names of the separate Bills are:

a) Local

Government (Water Services) Bill; and

b) Local

Government (Water Services Repeals and Amendments) Bill.

22 DIA

has now updated its guidance materials given the introduction of the December

Bill (Guidance). A copy of the updated Guidance can be found at https://www.dia.govt.nz/Water-Services-Policy-Future-Delivery-System#Financing.

Specific factsheets have also been referred to through this report. Further

general information on LWDW is also available on the DIA website: https://www.dia.govt.nz/Water-Services-Policy-and-Legislation

.

23 As

expected, the December Bill is comprehensive covering all aspects of the new

water services delivery system and delivery entities. Specific impacts on the

options presented in this report are discussed throughout this report. A

Summary of the key themes of the December Bill (as previously provided to

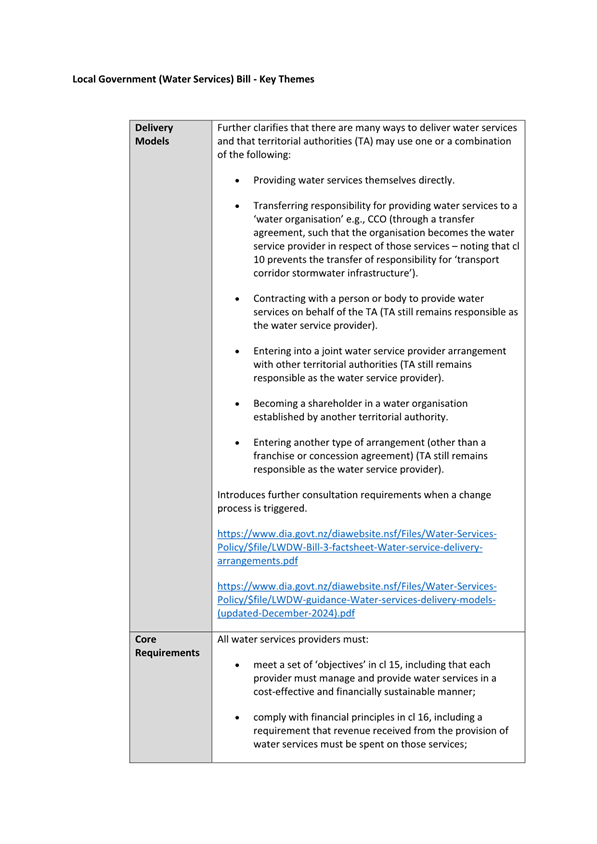

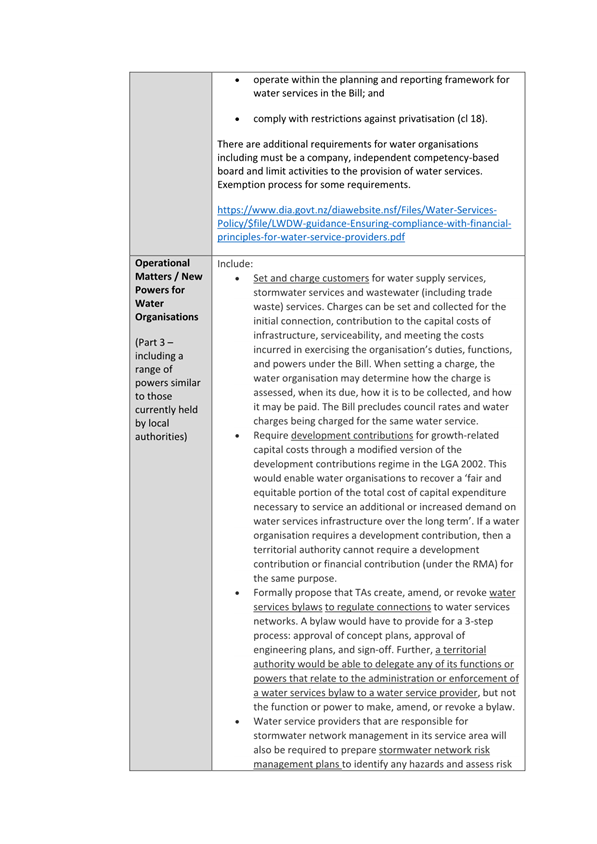

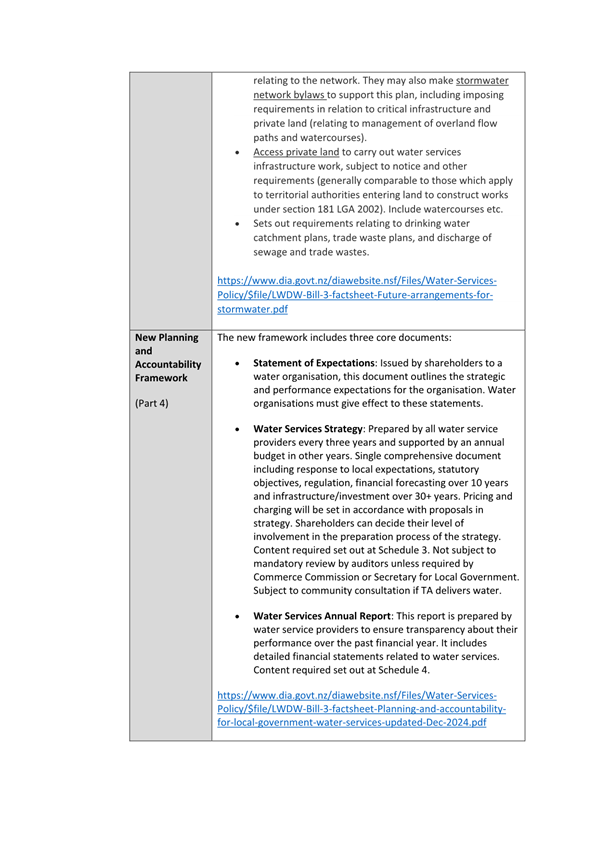

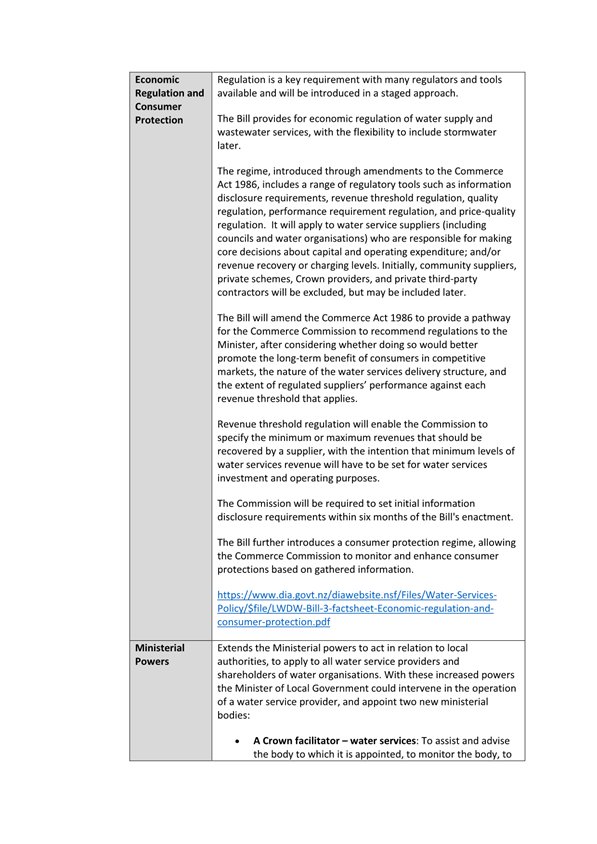

Councillors) is included at Attachment D.

Preliminary

Act

24 As

presented to Council in earlier reports, the Preliminary Act prescribes the

process that Council must use for decision making and consultation on the WSDM.

25 Council

is not required to comply with the corresponding requirement in the Local

Government Act 2002 (LGA 2002) where an alternative process under the

Preliminary Act applies.

26 The

options presented in this report comply with the Preliminary Act.

Requirement to

identify at least two potential options

27 The

Preliminary Act specifies that, during decision making, the Council:

a)

Must identify both of the following two options for delivering

water services:

i) Remaining

with the existing approach for delivering water services; and

ii) Establishing,

joining, or amending (as the case may be) a water services CCO (WSCCO) or a

joint local government arrangement.

b) May

also identify additional options for delivering water services and must assess

the advantages and disadvantages of all options identified.

Information to be

included in Consultation Document

28 During

consultation, Council must make the following information publicly available:

a) The proposal (being the Preferred Option), an explanation of the

proposal and the reasons for the proposal.

b) An analysis of the reasonably practicable options,

which must include:

i) the

option to remain with the existing approach for delivering water services; and

ii) the

option to establish, join or amend (as the case may be) a water services CCO

(WSCCO) or a joint local government arrangement.

c) How

proceeding (or not) with the proposal is likely to affect Council’s

rates, debt, levels of service and water services charges.

d) Community

implications (if joint) and accountability/monitoring arrangements (if assets

transferred).

e) Any

other relevant implications of the proposal that Council considers will be of

interest to the public.

Potential

for shared services

29 Under

either the In-House or CCO Options, there is the potential to add shared water

services. There is a separate report to Council on 26 February 2025 regarding a

proposed memorandum of understanding between the Dunedin City Council and the

Christchurch City Council to investigate the possibility of shared water

services.

Overlapping

consultation with the 9 Year Plan

30 Council

is only required to consult once but may decide to undertake further

consultation before deciding on a WSDM.

31 Consultation

on the Water Consultation Options is a separate process from the 9YP

consultation process. Consultation on the Water Consultation Options will be

under the Preliminary Act whereas consultation on the 9YP will be under the LGA

2002.

32 There

will be one consultation document for the 9YP and another consultation document

for the Water Consultation Options. Each consultation document will cross

reference the other.

33 Given

that a decision on the Water Consultation Options has the potential to impact

the 9YP, there will be combined Hearings in May for both the 9YP and the Water

Consultation Options.

Consultation

requirements with mana whenua

34 Council

is required to consult with mana whenua under both section 77(1)(c) and section

81 of the LGA 2002 given both references are included under section 60 of the

Preliminary Act. Further, section 14(1)(d) of the LGA 2002 also provides that a

local authority should provide opportunities for Māori to contribute to

its decision-making processes.

Decision

Making on a Change Proposal (after enactment of the December Bill)

35 The

December Bill, as currently drafted, includes new decision-making requirements

if there is a “Change of Proposal”. This would only apply following

enactment of the December Bill (mid-2025).

36 A

Change Proposal includes things like establishing a council-controlled

organisation (CCO) or agreeing on shared services with another territorial

authority.

37 If

a Change Proposal is triggered, Council would need to consult on three options;

being the existing approach, the change proposal and at least one further

reasonably practicable option, if available.

38 This

contrasts with the minimum of two options under the Preliminary Act.

39 There

is some uncertainty on whether Council would be required to re-consult if

Council decided on the CCO Option for its WSDP and the CCO was not established

until after enactment of the December Bill. However, DIA has indicated by

e-mail to staff that the new decision-making requirements in the December Bill

are intended to apply to future decisions by Council outside

current decision making required to inform the WSDP. Staff are hoping that the

December Bill will be amended to clarify this.

40 If

Council decided on the In-House Option for its WSDP and then later (for

example, in 2 years’ time) decided that it wanted the CCO Option then,

based on the current drafting of the December Bill, Council would need to go

through a fresh consultation process.

Legal

Requirements for Water Service Providers

41 As

noted in earlier reports:

a) A

‘water organisation’ means the separate organisation that

territorial authorities may establish or be shareholders in, and which provides

water services in accordance with transfer agreements. A water organisation

does not include the in-house model. An example of a water organisation is a

CCO.

b) A

‘water service provider’ is a wider term and means water

organisations and territorial authorities. In other words, a water

service provider includes both the in-house model and models such as the CCO

model.

42 Legislative

requirements are set out in the December Bill for all water service providers.

Additional requirements are included for water organisations. Both sets of

requirements are described below.

All Water Service

Providers

43 The

requirements for all water service providers (including in-house delivery)

broadly follow earlier DIA guidance with some updates.

44 The

following summary of these core requirements is taken from the DIA Guidance.

Staff have provided further detail on each requirement at Attachment E:

Additional

Requirements for Water Organisations

45 Additional

requirements also apply to those councils forming a water organisation e.g., a

CCO. These are set out in the Guidance as below including a new requirement

relating to a transfer agreement:

46 It

is possible to apply for exemptions from the marked (*) requirements on a

case-by-case basis through a legislated process.

DISCUSSION

PART A: Which base models does

Council want to consult on?

47 At

Council’s meeting on 25 November 2024, Council decided to shortlist three

base WSDMs:

a) In-House

Delivery;

b) Single

CCO; and

c) Regional

Multi-Council Entity

(the “shortlist”).

48 Some

initial explanations and comparative analysis on the Shortlist were discussed

in the November Report and included some advantages and disadvantages for each:

https://infocouncil.dunedin.govt.nz/Open/2024/11/CNL_20241125_AGN_3009_AT_WEB.htm

49 Following

Council’s decision on the Shortlist, there have been discussions with

staff at Christchurch City Council regarding the potential for shared water

services. This is discussed in a separate report to Council, also on the agenda

for 26 February 2025. The intention is to manage shared services through

contracts rather than a multi-council entity.

50 There

have also been discussions with other territorial authorities, but those

discussions have not progressed to the stage where there is an identified

practicable option suitable for consultation. Without knowing who the

participants would be in a Regional Multi-Council Entity, it is difficult to

provide any further analysis than what has already been provided through the

Morrison Low Report dated 24 October 2024. The Morrison Low report was attached

to the November

Report.

51 As

part of considering the Shortlist, staff have considered whether a two waters

CCO may be a reasonably practicable option or whether it would be reasonably

practicable to use one of Council’s existing CCOs for the delivery of

water services. For a variety of reasons, these two variations on the CCO

Option have not been considered further because they are not seen as being

reasonably practicable options.

52 Staff

consider that the “reasonably practicable options” under the

Preliminary Act are:

a) the

In-House Option; and

b) the

CCO Option.

Part B: Which is Council’s

Preferred Option?

53 Council

will need to carefully weigh a variety of financial and non-financial

considerations before deciding on its preferred WSDM.

Summary of Financial Considerations

Financially

Sustainable

54 A

WSDP needs an explanation of:

a) How

revenue from and delivery of water services will be separated from the

territorial authority’s other functions and activities; and

b) How

Council proposes to ensure delivery of water services will be financially

sustainable by 30 June 2028.

55 The

December Bill specifies the financial principles for water service providers.

The financial principles support the ringfencing objectives of LWDW and are

supported by DIA guidance: “Ensuring compliance with financial principles

for water service providers” (Attachment F). The December Bill also includes

objectives to ensure water services are provided in a cost-effective and

financially sustainable manner.

56 Ringfencing

of water services is critical for financial sustainability and revenue sufficiency. The DIA guidance states that

ringfencing requires:

a) Water

revenues be spent on water services; and

b) Water

services charges and expenses be transparent and accountable.

57 The

Preliminary Act defines ‘financially sustainable’, in relation to a

council’s delivery of water services, as:

a) The

revenue applied to the council’s delivery of those water services is

sufficient to ensure the council’s long-term investment in delivering

water services; and

b) The

council is financially able to meet all regulatory standards and requirements

for the council’s delivery of those water services.

58 The

DIA Guidance suggests three components to assessing financial sustainability.

How councils approach achieving financial sustainability can be different

depending on local circumstances and requires councils to consider the balance

between the three components:

a) Revenue

sufficiency - having sufficient revenue to cover the costs (including servicing

debt) of water services delivery.

b) Investment

sufficiency - having a sufficient level of investment to meet levels of

service, regulatory requirements and provide for growth.

c) Financing

sufficiency - having sufficient funding and financing arrangements to meet

investment requirements.

59 The

DIA Guidance makes further recommendations about how councils can demonstrate

ringfencing. It also provides further information about financial

sustainability as well as providing a template for financial projections and a

financial sustainability test (See DIA link https://www.dia.govt.nz/diawebsite.nsf/Files/Water-Services-Policy/$file/Guidance-for-preparing-Water-Services-Delivery-Plans-September-2024.pdf).

60 Further

DIA guidance: “Financing water services delivery through establishing new

water CCOs” (Attachment G) provides advice on financing options for

councils considering the CCO model for water services delivery. The guidance

outlines criteria for accessing higher borrowing from the Local Government

Funding Agency (LGFA).

Financial Analysis

61 The

following financial analysis has been prepared to support Council’s

decision making in preparation of the WSDP. The analysis does not provide the

level of detail required in the WSDP but does provide a level of analysis and

information that demonstrates the financial impacts of each option being

considered.

62 Two

sets of forecast financial statements for the 10 year period 2024-34 have been

prepared:

a) The

In-House Option - as per the approved 2024/25 Annual plan and draft 9 year plan

2025-34 (9 year plan) (Attachment H) and

b) The

CCO Option – a 3 Waters CCO, as at 1 July 2025 (Attachment I).

63 A

series of tables comparing the two options have been included in Attachment J.

64 Although

in practice a CCO probably would not be established until 1 July 2027, the

modelling assumes a date of 1 July 2025 to provide financial comparison over

the longest period possible.

65 The

WSDP requires a minimum of ten years of financial

projections for water services, covering the financial years 2024/25 - 2033/34.

Due to the inherent uncertainties with forecasting, the financial forecasts

provided do not go beyond the 2033/34 year.

66 As

mentioned above, DIA provided a template to use for the financial sections of

the WSDP. This includes financial projections, measures and charts required in

the financial sustainability assessment. Staff have used these templates for

the financial analysis of the two options.

Assumptions

67 Key

assumptions underlying both options are:

a) 1

July 2024 opening balance sheet to ringfence 3 Waters for modelling purposes.

b) The

2024/25 Annual Plan is year 1 (due to the 9 year plan only being 9 years).

c) The

starting point is the draft 9 year plan 2025-34.

d) Total

operating expenditure of $1.568 billion and total capital expenditure of $1.095

billion is forecast over the 9 year plan.

e) No

allowance is made for savings as a result of efficiencies.

68 Each

option assumes additional operating costs as follows:

a) An

increase in staff resourcing to meet new regulatory requirements, customer

service, finance and billing.

b) Additional

levies to Taumata Arowai (Water Services Authority) and the Commerce

Commission.

c) Additional

audit fees for additional financial reporting requirements.

69 The

CCO Option attracts further operational costs, in particular governance and

leadership.

70 Some

corporate costs, including fleet, would shift from Council to the CCO, however

some internal costs could remain as stranded costs within Council and need to

be managed over time. Further work on this is required and will be

underway in the coming months. An update on this work will be provided to

Council in May.

71 LGFA

have agreed in principle to lend up to 500% of operating revenues to a 3 Waters

CCO, creating additional borrowing capacity. The CCO Option assumes access to

this borrowing limit. It also assumes a Funds From Operations (FFO) of 10% of

debt. LGFA has advised that most water CCOs will have a minimum FFO to debt

ratio of between 8% and 12%, depending on credit profile. These will be

negotiated with each water CCO.

72 Transitional

costs need to be accounted for but these are yet to be determined.

73 In

order to ensure compliance with the financial principles and financial

sustainability provisions, current systems (including finance and asset

management) are likely to need investment, for either option. A provisional

amount for this has been included in the 9 year plan.

Funding Approach

74 The

funding approach for the In-House Option aligns with Council’s draft

Financial Strategy and draft 9 year plan as follows:

a) Balanced

budget - the LGA 2002 requires councils to have a balanced budget unless it is

prudent to do otherwise. This means fully funding depreciation, which in turn

is used to pay for capital expenditure. For 3 Waters, the draft 9 year plan

provides 15% per annum rate increases for the first three years leading to a

balanced budget (for 3 Waters) by the 2027/28 year.

b) Debt

limit – Council’s gross debt limit is 250% of revenue. The LGFA

financial covenants limit net debt to 280% of revenue.

75 The

funding approach for the CCO Option follows DIA guidance as follows:

a) Operating

revenues pay for operating costs - DIA guidance indicates that financial

sustainability and ringfencing requirements mean that operating revenues should

be set to a level that covers the operating cost (including debt) of water

services. This ensures sufficient operating cashflows are secured to support

borrowing and investment requirements (including staying below borrowing

limits). Operating revenues, including 3 Waters rates, should cover all cash

operating costs plus a minimum FFO.

b) Capital

sources pay for capital investment - DIA guidance indicates that capital

expenditure should be funded by capital revenues (such as development

contributions) and debt financing.

76 The

DIA guidance on CCO funding states:

“This approach could

replace current council approaches to funding of depreciation to generate cash

reserves to fund capital investment. Depreciation funding in effect pre-funds

capital investment and results in a higher cost to consumers than using

effective debt financing for investment.”

77 The

difference in funding approaches means that under the CCO Option, over the 10

year period modelled, charges to customers could be lower and debt higher. This

is because more debt is used to pay for capital expenditure. For the In-House

Option, more rates income is used to pay for capital expenditure.

In-House Option

78 Under

this option, 3 Waters remains in-house. This option is consistent with the

draft 9 year plan. The key financial outcomes are:

Table 1

a) Operating

revenue (excludes development contributions of $26 million) over the 10 years

is $1.506 billion.

b) Rate

increases of 15% per annum for the first three years, followed by an average of

6% for the remaining years.

c) The

average customer charge per connection (including GST) increases from $2,024 in

2024/25 to $4,280 in 2033/34.

d) Operating

expenditure over the 10 years is $1.568 billion, including interest costs of

$196 million.

e) Net

surplus is achieved in the 2027/28 year.

f) Capital

expenditure over the 10 years is $1.095 billion.

g) 3

Waters debt is $630 million by 30 June 2034.

h) Total

Council debt is $1.092 billion by 30 June 2034. Council debt remains within the

250% debt limit throughout the period. By year 10, debt reaches 174% of

revenue. Council debt remains within the LGFA net debt limit of 280%. By year

10, net debt reaches 156% of revenue.

CCO Option

79 Under

this option, a 3 Waters CCO is established. As indicated above, operating revenue

covers cash operating expenses plus an FFO margin of 10%. The key financial

outcomes are:

Table 2

a) Operating

revenue (excludes development contributions of $26 million) over the 10 years

is $1.392 billion.

b) Annual

increases in water charges range from 5.8% in 2025/26 to 13.1% in 2029/30. The

average price increases over the 9 year plan timeframe is 8.5%.

c) The

average customer charge per connection (including GST) increases from $2,024 in

2024/25 to $4,202 in 2033/34.

d) Operating

expenditure over the 10 years is $1.613 billion including interest costs of

$231 million.

e) The

CCO Option does not achieve a balanced budget during the 10 year period because

operational revenues cover operational cash expenses only (not depreciation)

plus the FFO requirement (modelled at 10%). Over time, as debt and therefore

the FFO requirement increases, the deficit reduces.

f) Capital

expenditure over the 10 years is $1.095 billion.

g) Debt

is $788 million by 30 June 2034. This is within the 500% LGFA net debt limit.

By year 10, debt reaches 405% of revenue.

h) Council

debt excluding 3 Waters is considered in paragraphs 80-83 below.

In-House Option

compared to the CCO Option

80 The

key financial differences between the two options are discussed below. Table 3

summarises financial information for year 10 (2033/34) and the 10 year total

for each of the options.

Table 3

a) Over

the 10 year period, operating revenue under the CCO Option is $114 million less

than the In-House Option. As discussed in paragraph 76 above, charges to

customers are lower. More debt is used to pay for capital expenditure than

under the In-House Option, where more rates funding is used to fund capital

expenditure. The CCO Option would debt fund an additional $157 million over the

10 year period. Chart 1 below shows the profile of operating revenue under each

option over the 10 year period. By the 2033/34 year, operating revenue is $198

million in the In-House Option and $194 million in the CCO Option.

Chart 1

b) The

average charge per connection under both options is provided in Table 4 and

Chart 2 below. The average charge per connection is lower in the CCO Option,

however the difference (saving) reduces as more debt is raised. While this does

not reflect the current charging model, it provides a comparison:

Table 4

Chart 2

c) Annual

increases in charges for water services are higher for the In-House Option for

the first three years of the 9 year plan period (2025/26 – 2027/28),

reflecting Council fully funding depreciation by 2027/28. From the 2028/29

year, the annual increases are higher in the CCO Option. This is illustrated in

the Chart 3 below:

Chart 3

d) Operating

expenditure under the CCO Option is $44 million higher than the In-House Option

due to additional interest ($35 million) and CCO related operational costs

($9 million).

e) Net

surplus/(deficit) is different in each option and this reflects the different

funding approaches. The In-House Option achieves a balanced budget in the

2027/28 year. The CCO Option does not achieve a balanced budget during the 10

year period because operational revenues cover operational cash expenses

only (not depreciation) plus the FFO requirement (modelled at 10%). As debt

increases so does the FFO requirement therefore the deficits will reduce.

f) Capital

expenditure over the 10 year period is the same for each option.

g) Under

the CCO Option, 3 Waters debt is $157 million higher than the In-House Option

due to the reduction in operating revenue and the additional interest and

operating costs. By year 10, net debt reaches 405% of revenue in the CCO Option

and 314% in the In-House Option. The graph below shows the debt to revenue

metric for each option:

Chart 4

Council excluding 3

Waters

81 The

establishment of a CCO for 3 Waters results in Council having less debt. This

would create additional debt headroom compared to the in-house option, as shown

in the two charts below, due to the ratio of revenue to debt improving without

3 waters. The debt limit indicated on each chart is the Council 250% limit.

82 Chart

5 shows the in-house option. The headroom in the 2033/34 year is $480 million.

Chart 5

83 Chart

6 shows Council excluding 3 Waters. The headroom in the 2033/34 year is $603

million, $124 million higher than the In-House Option.

Chart 6

84 The

debt forecast for both options, for Council companies and the total Council

group have been summarised in Attachment J. This attachment also provides

associated financial metrics. Group debt under the In-House Option

reaches $2.26 billion by 2033/34 and under the CCO Option group debt reaches

$2.42 billion by 2033/34.

Other Considerations

85 There

are a number of possible scenarios. For example, in the CCO Option, expenditure

could be increased if customer charges are maintained at the in-house

level. Noting that all scenarios will be subject to the regulatory

compliance.

86 The

FFO margin is required to meet revenue sufficiency requirements and ensure debt

is appropriately serviced. Financial modelling for the single CCO option

has used a 10% FFO, the mid-point of the LGFA’s suggested range of 8-12%.

Attachment K compares the In-House Option against the CCO option with the FFO

margin set at 8% and 12%. Generally:

a) A

higher FFO margin increases operating revenue, resulting in higher customer

charges, lower debt and lower interest expense.

b) A

lower FFO margin decreases operating revenue, resulting in lower customer

charges, higher debt and higher interest expense.

Summary of Non-financial Considerations

87 There

are a wide range of considerations that are non-financial considerations,

including the following:

· Regulatory Compliance: The

capacity to meet current and future water quality, environmental, and economic

regulations.

· Service Delivery and Operations: The effectiveness and efficiency of day-to-day operations,

including resource allocation and infrastructure management. Includes ease in

modernising the customer experience, access and leveraging specialist

skills/staff as well as digital systems.

· Governance and Control: The

degree of Council oversight, including through development of the water

services strategy.

· Implementation Feasibility: The practicality, cost, and risk of transitioning to the

model, ensuring minimal disruption to services.

88 Staff

set out below an analysis of these non-financial considerations.

Regulatory

Compliance:

89 Regulatory

compliance is non-negotiable for water services delivery in both the In-House

Option and CCO Option. Whether Council establishes a CCO or decides on an

In-House Option, it will be subject to:

a) economic

regulation; and

b) environmental

and infrastructure regulation.

90 The

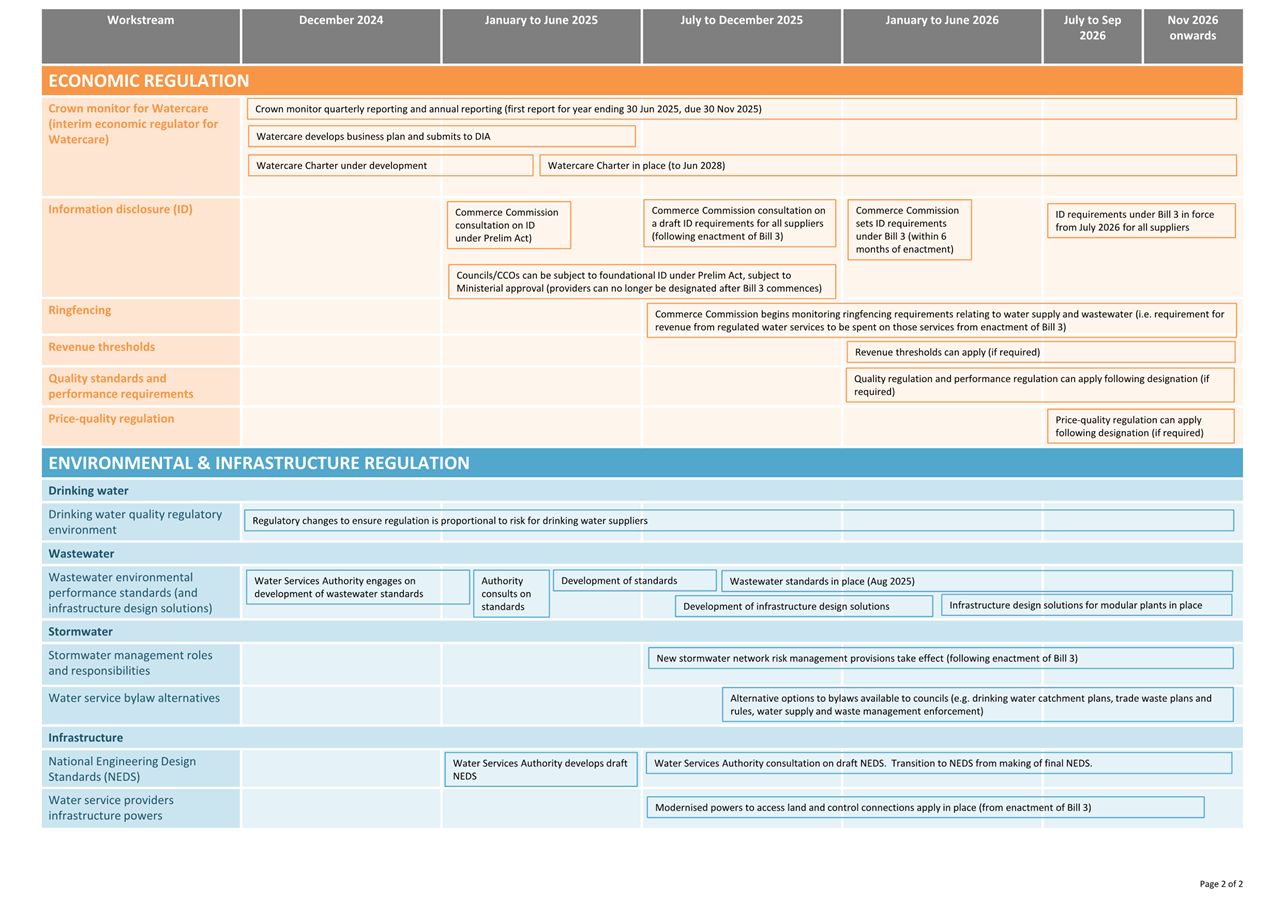

second page of the Implementation Roadmap (Attachment B) shows the different

types of economic, environmental and infrastructure regulation.

91 Regarding

economic regulation:

a) The

Commerce Commission will have a range of tools to promote sufficient revenue

recovery, and efficient investment and maintenance so that water services meet

regulatory requirements. These are summarised in the DIA Guidance called

“Economic regulation and consumer protection”: https://www.dia.govt.nz/diawebsite.nsf/Files/Water-Services-Policy/$file/LWDW-Bill-3-factsheet-Economic-regulation-and-consumer-protection.pdf

b) The

expected timelines for economic regulation tools are set out in the table

below:

c) If

Council decides on the CCO Option for its WSDP, then the Commerce Commission

would regulate the CCO.

d) If

Council decides on the In-House Option for its WSDP, then:

i) the

Commerce Commission would regulate those parts of the Council that directly and

indirectly deal with water services; and

ii) there

will be a significant amount of work required (in a short period of time) to

ensure that Council complies with the regulatory framework, particularly the

requirement to ringfence water services from the finances of the rest of

Council.

92 Regarding

environmental and infrastructure regulation:

a) Council

already has established governance frameworks that facilitate strong compliance

with water quality and environmental regulations.

b) A

CCO would focus solely on water services, which creates a dedicated focus.

However, the CCO Option would require significant work to establish compliance

management during a transition period and would require strong ongoing

collaboration with Council to ensure alignment with broader environmental and

community goals.

Service Delivery and

Operations:

93 At

present:

a) Water

services are integrated with other Council functions, as there are a lot of

interdependencies. For example, flood management, parks, urban planning, resource

consenting and the transport network. This enhances co-ordination and

efficiency.

b) The

three waters team routinely co-ordinates with other teams within Council.

94 If

there was a CCO for water services, then there is a risk of a

“silo-type” approach. This would particularly be the case if the

CCO offices were not co-located within the Council’s offices. While there

is provision in the December Bill for a stormwater network service agreement

between those entities having a role, function or interest in the operation of

stormwater infrastructure in the area (including the Council and a CCO), there

is a risk that the approach would be less co-ordinated than the In-House

Option.

95 There

is a perception within parts of the water sector that the CCO Option may be

better able to attract and retain specialised expertise in water management,

engineering, and compliance. It is difficult at this stage to know whether that

is true. If Council proceeds with shared services (eg with Christchurch City

Council), then it is likely that Council staff would get the opportunity to

work with their peers.

96 Systems

will need to be upgraded to ensure financial separation in both the In-House

and CCO Options. The cost of these systems is expected to be substantial.

Governance and

Control:

97 This

topic is covered under the DIA’s factsheet called: Planning and

accountability for local government water services: https://www.dia.govt.nz/diawebsite.nsf/Files/Water-Services-Policy/$file/LWDW-Bill-3-factsheet-Planning-and-accountability-for-local-government-water-services-updated-Dec-2024.pdf.

98 Under

the In-House Option, Council would remain as the governing body for water

services, and it would retain control (subject to regulatory requirements) over

how water services are funded and charged to the community, including rates and

the possibility of volumetric charging.

99 Under

the CCO Option:

a) Strategic

oversight would remain with Council, but operational control would be

transferred to the CCO’s board and management.

b) Staff

expect that, if Council chooses the CCO Option as its WSDM, then the most

likely date that it would be established would be 1 July 2027 although it could

in theory be earlier.

c) Council

(as shareholder) would prepare a statement of expectations setting out the

expectations, priorities, and strategic direction for the water organisation to

inform and guide the decisions and actions of the board. Water organisations

must give effect to these statements.

d) Council

would be the sole shareholder. The shareholding would not be through Dunedin

City Holdings Limited (DCHL). This is because the legislative framework

specifies that a water organisation must be wholly owned by one or more local

authorities (or trustees of consumer trusts).

e) Council

could appoint directors to a board directly (or could appoint a committee) and

ensure that relevant perspectives were brought to the director appointment

process (flexibility to appoint mana whenua, community or consumer

representatives) subject to statutory requirements including competency,

collective skills, knowledge and experience.

f) The

CCO would have less flexibility in how it charges for water being restricted

from using property value-based charges and requires transition to specific

water charges, such as fixed fees or volumetric billing within five years.

100 Under

both the In-House Option and the CCO Option, there is a requirement to prepare:

a) a

water services strategy; and

b) a

water services annual report.

101 The

water services strategy is a single comprehensive water focused document which

must be prepared every three years. There will be an annual budget in the

intervening years.

102 The

first water services strategy is to be adopted so it takes effect from 1 July

2027 (or an earlier date as determined by the water service provider) and

ending on the 30 June 2030. Likewise, the first water services annual report

would start on 1 July 2027 (or earlier in line with the water services

strategy) and end on 30 June 2028.

103 The

water services strategy will set out how the provider is proposing to perform,

respond to local expectations and priorities, and meet statutory objectives and

regulatory requirements. It will include financial forecasting information over

10 years, and infrastructure and investment information over more than 30

years. Strategies prepared by water organisations will respond to matters in

the statement of expectations. Prices and charges will be set in accordance

with the proposals in the strategy.

104 Under

the In-House Option, Council would be required to consult communities in

relation to its proposed water services strategy. Under the CCO Option, the CCO

would be required to consult with Council (as its shareholder).

105 Under

the CCO Option, the Council would determine the nature of its involvement in

preparing and finalising the water services strategy. Council would ensure that

information on its preparation and finalisation of the water services strategy

is included in the CCO’s constitution, or elsewhere.

106 The

water services annual report is a document reporting on the water service

provider’s actual performance against the expectations and proposals in

water services strategy and, if applicable, in the statement of expectations.

Implementation

Feasibility

107 The

In-House Option is expected to have the least initial setup costs and to be the

most straightforward to implement. However, there will be significant costs and

changes required to meet the regulatory regime. For example, there will need to

be new systems for ring-fencing and water billing.

108 The CCO

Option provides an opportunity to invest in a new fit for purpose entity within

the new water services framework. However, the CCO Option has a higher initial

cost to implement as well as being potentially more disruptive in the short

term due to transition.

109 There

is a perception in parts of the water sector that the CCO Option may offer

long-term efficiencies (assuming a successful transition, operational

integration, a robust implementation plan and resource allocation).

110 Shared

services could be added to either the In-House Option or the CCO Option (noting

that shared services may trigger a requirement for further consultation).

OPTIONS

111 The

Preliminary Act requires Council to choose its future WSDM.

112 There

are a range of advantages and disadvantages for both the In-House Option and

the CCO Option. In essence, the In-House Option provides Council with direct

control over water services, ensuring residents can participate in decision

making through usual local democracy practices, and there is alignment with

broader Council strategies and Council functions. However, the CCO has access

to higher borrowing and operates under different financial arrangements.

113 The

Council’s financial modelling is over a 10-year period (2024-2034). It is

not possible to accurately model beyond this period, but the models prepared

show that the option to reduce charges to customers decreases towards the end

of the modelled period when there is increased debt.

114 Although

it is finely balanced, staff recommend that Council:

a) Consult

on the In-House Option and the CCO Option; and

b) Decides

its Preferred Option for consultation is the In-House Option.

115 This

recommendation is set against the context that:

a) Council’s

decision on its Preferred Option will be subject to public consultation.

b) The

draft 9YP supports the ability of Council to retain 3 Waters.

c) Council

has a proven ability to deliver water services to a high standard. Council over

the last 5 years has invested in the capital programme and has accelerated

investment in both planning and delivery. This means the 3 Waters Team and

Council’s contractor base are well positioned to continue delivery at

pace.

d) Council

is in the process of investigating shared services with Christchurch City

Council. It would be helpful to have time to see how and to what extent the

shared services, in practice, assist Council to achieve cost reductions and enhance

water services.

e) Subject

to changes in legislation or Government direction, if Council chooses the

In-House Option now it would still be open to Council to later decide that it

wants to establish a CCO. For example, Council could decide as part of

its next long term plan process in 2027 that it would like to re-consult the

public on the Council’s WSDM.

f) If

Council chooses the CCO Option, then this may be difficult to unwind in the

future.

g) It

is unclear what the long-term benefits or risks would be after the end of the

modelled period.

116 It is

possible that there will be future water reforms. Without knowing what those

reforms may be, it is not clear whether Council would be in a better position

for legislative change under the In-House Option or the CCO Option. The

potential for legislative change has not therefore been discussed as an

advantage or a disadvantage under the options.

117 Similarly,

it is likely that there will be systems, staff and technology costs under both

the In-House and CCO Options, so these have not been discussed as an advantage

or disadvantage.

118 The

governance arrangements under the In-House Option and the CCO Option are

different, but there are mechanisms available to ensure that each entity has

specialist advice available.

119 The

impact on emissions and zero carbon is likely to be similar whether the

Preferred Option is the In-House Option or the CCO Option. Should Council

decide on the CCO Option, then the Statement of Expectations for the CCO could

include provisions regarding emissions and zero carbon.

Option

One – Recommended Option - In-House Delivery as the Preferred Option, and

CCO is the additional reasonably practicable option

120 Under

this option, Council would:

a) Decide

to consult on the following two options under the Local Government (Water

Services Preliminary Arrangements) Act 2024:

i) In-House

delivery of 3 Waters (the In-House Option); and

ii) An

asset owning CCO for 3 Waters, with Council as the sole shareholder (the CCO

Option).

b) Decide

that its Preferred Option for consultation is the In-House Option.

c) Note

that there will be a report to Council on 18 March 2024 asking Council to

approve the water options consultation document.

Advantages

· Retains

local control and accountability.

· Strong

integration with other Council functions (e.g., flood management and urban

planning) which supports operational efficiencies and aligns with Council’s

broader strategies and city-wide priorities (subject to regulation).

· Builds

on Council’s successful delivery of water services.

· Financial

modelling indicates that the Council Group would take on less debt under the

In-House Option.

· Avoids

the costs of establishing a CCO and minimises transition costs (noting however

that the In-House Option will have significant costs associated with setting

Council up so that it can comply with the new regulatory regime).

· Council’s

draft 9YP retains water while remaining within Council’s debt-to-revenue

limit of 250% and the LGFA net debt limit of 280%.

· This

option would allow Council time to test how the In-House Option works under the

new regulatory regime, and to see the effects of any shared services

arrangements (such as those currently being investigated with Christchurch City

Council).

· This

option does not prevent Council from reconsidering its WSDM later, such as in

2027 as part of the next Long Term Plan process and developing a Water Services

Strategy.

Disadvantages

· Financial

modelling shows this option as having fewer potential savings to households.

· Council

does not have access to the 500% debt to revenue ratio that is available under

the CCO Option.

· The

In-House Option could constrain Council’s ability to spend in areas other

than water and/or to deal with large-scale infrastructure investments not

already budgeted for in the draft 9YP.

· Council

will need to establish new mechanisms for ringfencing water revenue and costs.

· The

Commerce Commission will have wide powers, with the ability to consider matters

relating directly and indirectly to water services.

· Lacks

single focus on delivering water services and does not ringfence legal

liability to within the CCO.

· Arguably,

less commercial and/or agile due to the legislative framework for councils.

· Does

not capture scale benefits and may not attract specialist staff, although this

may be mitigated through shared services arrangements.

Option

Two – CCO is the preferred option and In-House Delivery is the additional

reasonably practicable option, with the option of any add-ons, subject to

further analysis

121 This

option is the same as option one, except Council’s Preferred Option would

be a CCO instead of In-House. Therefore, under this option, Council would:

a) Decide

to consult on the following two options under the Local Government (Water

Services Preliminary Arrangements) Act 2024:

i) In-House

delivery of 3 Waters (the In-House Option); and

ii) An

asset owning CCO for 3 Waters, with Council as the sole shareholder (the CCO

Option).

b) Decide

that its Preferred Option for consultation is the CCO Option.

c) Note

that there will be a report to Council on 18 March 2024 asking Council to

approve the water options consultation document.

Advantages

· Financial

modelling shows this option as having potentially greater savings to households

-$114 million over the 10 years modelled.

· LGFA

will allow a debt to revenue ratio of 500% (compared to 280% for Council under

the In-House Option).

· Does

not constrain Council’s ability to spend in areas other than water.

· The

Council would not be subject to the new regulatory regime, and the associated

compliance costs associated with that regime.

· The

CCO’s single focus would be on delivering water services.

· Legal

liability would be ringfenced to within the CCO (at least to some extent).

· The

CCO must give effect to statement of expectations (if consistent with

CCO’s purpose and statutory objectives).

· A

director of a CCO must be appointed based on their competency to perform the

role, and the directors of a CCO must collectively have an appropriate mix of

skills, knowledge, and experience in relation to providing water services.

· Accountability

to the Council as shareholder via regular reporting and annual reporting.

· Arguably,

a CCO may be more commercial and/or agile due to it not operating under the

same legislative framework as councils.

Disadvantages

· Potential

for higher debt, with the associated risk and cost of servicing higher debt.

Council Group will have an extra $157 million of debt.

· Risks

reduced co-ordination with Council functions if not adequately managed.

· Independent

governance introduces risks of misalignment with Council priorities (unless

effectively managed through governance arrangements and key accountability

documents).

· Potential

for reduced community input.

· Accountability

to consumers for service delivery potentially blurred.

· Establishment

and transition costs reduce immediate value.

· If

Council found that the CCO Option was problematic, it would be difficult to

unwind the arrangements.

NEXT STEPS

122 The

next steps are currently being discussed with Audit New Zealand, who are

currently in the process of auditing Council’s 9YP CD. The Water Options

CD does not need to be audited.

123 Although

the 9YP process and the WSDP process are two separate processes undertaken

under separate legislation, the 9YP CD and the Water Options CD will need to be

cross-referenced and the processes will need to run in parallel.

124 Staff

expect that the process will be essentially as follows (although this is

subject to change depending on the approach taken by Audit New Zealand):

a) Staff

will report back to Council on 18 March 2025 with a draft Water Options CD for

approval by Council.

b) The

Water Options CD and 9YP CD will be released and open for submissions from 31

March 2025 to 30 April 2025.

c) There

will be combined Hearings in the week commencing 5 May 2025 on the Water

Options and the 9YP.

d) As

soon as possible after the Hearings (mid-May), Council will decide on its WSDM.

A decision on the WSDM would need to be made in mid-May so that staff can

update the 9YP to reflect the WSDM, as required, and to allow time for the

Audit Report on the 9YP.

e) Council

will adopt its 9YP prior to 30 June 2025, and will submit its WSDP to the

Secretary for Local Government before 3 September 2025.

Signatories

|

Author: