|

|

Council

30 June 2025

|

Setting of Rates for the 2025/26 Financial Year

Department: Finance

EXECUTIVE SUMMARY

1. Following

adoption of the 9 year plan 2025-34, the council now

needs to set the rates as provided for in the Funding Impact Statement for the 2025/26

year.

RECOMMENDATIONS

That the Council:

a) Sets the following

rates under the Local Government (Rating) Act 2002 on rating units in the

district for the financial year commencing 1 July 2025 and ending on 30 June

2026.

1.

General Rate

A general

rate set under section 13 of the Local Government (Rating) Act 2002 made on

every rating unit, assessed on a differential basis as described below:

· A rate of 0.3077 cents in the dollar (including GST) of

capital value on every rating unit in the "residential" category.

· A rate of 0.2923 cents in the dollar (including GST) of

capital value on every rating unit in the "lifestyle" category.

· A rate of 0.7693 cents in the dollar (including GST) of

capital value on every rating unit in the "commercial" category.

· A rate of 0.5385 cents in the dollar (including GST) of

capital value on every rating unit in the "residential heritage bed and

breakfasts" category.

· A rate of 0.2462 cents in the dollar (including GST) of

capital value on every rating unit in the "farmland" category.

· A rate of 0.0563 cents in the dollar (including GST) of

capital value on the “stadium: 10,000+ seat capacity” category.

2.

Community Services Rate

A targeted

rate for community services, set under section 16 of the Local Government

(Rating) Act 2002, assessed on a differential basis as follows:

· $121.00 (including GST) per separately used or inhabited

part of a rating unit for all rating units in the "residential,

residential heritage bed and breakfasts, lifestyle and farmland"

categories.

· $121.00 (including GST) per rating unit for all rating

units in the "commercial and stadium: 10,000+ seat capacity"

categories.

3.

Kerbside Collection Rate

A targeted

rate for kerbside collection, set under section 16 of the Local Government

(Rating) Act 2002, assessed on a differential basis as follows:

· $343.40 (including GST) per separately used or inhabited

part of a rating unit for rating units in the "residential, residential

heritage bed and breakfasts, lifestyle and farmland" categories.

· $343.40 (including GST) per rating unit for rating units in

the "commercial" category.

4.

Drainage Rates

A targeted

rate for drainage, set under section 16 of the Local Government (Rating) Act

2002, assessed on a differential basis as follows:

· $884.40 (including GST) per separately used or inhabited

part of a rating unit for all rating units in the "residential,

residential heritage bed and breakfasts, lifestyle and farmland"

categories and which are "connected" to the public sewerage system.

· $442.20 (including GST) per separately used or inhabited

part of a rating unit for all rating units in the "residential,

residential heritage bed and breakfasts, lifestyle and farmland"

categories and which are "serviceable" by the public sewerage system.

· $884.40 (including GST) per rating unit for all rating

units in the "commercial, residential institutions, schools and stadium:

10,000+ seat capacity" categories and which are "connected" to

the public sewerage system.

· $442.20 (including GST) per rating unit for all rating

units in the "commercial, residential institutions and schools"

categories and which are "serviceable" by the public sewerage system.

· $102.25 (including GST) per rating unit for all rating

units in the "church" category and which are "connected" to

the public sewerage system.

Rating

units which are not "connected" to the scheme, and which are not

"serviceable" will not be liable for this rate. Drainage is a

combined targeted rate for sewage disposal and stormwater. Sewage

disposal makes up 78% of the drainage rate, and stormwater makes up 22%.

Non-rateable land will not be liable for the stormwater component of the

drainage targeted rate. Rates demands for the drainage targeted rate for

non-rateable land will therefore be charged at 78%.

5. Commercial Drainage Rates – Capital Value

A targeted

rate for drainage, set under section 16 of the Local Government (Rating) Act

2002, assessed on a differential basis as follows:

· A rate of 0.3018 cents in the dollar (including GST) of

capital value on every rating unit in the "commercial and residential

institution" category and which are "connected" to the public

sewerage system.

· A rate of 0.1509 cents in the dollar (including GST) of

capital value on every rating unit in the "commercial" category and

which are "serviceable" by the public sewerage system.

· A rate of 0.2264 cents in the dollar (including GST) of

capital value on every rating unit in the "school" category and which

are "connected" to the public sewerage system.

· A rate of 0.1132 cents in the dollar (including GST) of

capital value on every rating unit in the "school" category and which

are "serviceable" by the public sewerage system.

· A rate of 0.0206 cents in the dollar (including GST) of

capital value on the “stadium: 10,000+ seat capacity” category.

This rate

shall not apply to properties in Karitane, Middlemarch, Seacliff, Waikouaiti

and Warrington. This rate shall not apply to churches. Drainage is

a combined targeted rate for sewage disposal and stormwater. Sewage

disposal makes up 78% of the drainage rate, and stormwater makes up 22%.

Non-rateable land will not be liable for the stormwater component of the

drainage targeted rate. Rates demands for the drainage targeted rate for

non-rateable land will therefore be charged at 78%.

6.

Water Rates

A targeted

rate for water supply, set under section 16 of the Local Government (Rating)

Act 2002, assessed on a differential basis as follows:

· $671.80 (including GST) per separately used or inhabited

part of any "connected" rating unit which receives an ordinary supply

of water within the meaning of the Dunedin City Bylaws excepting properties in

Karitane, Merton, Rocklands/Pukerangi, Seacliff, Waitati, Warrington, East

Taieri, West Taieri and North Taieri.

· $335.90 (including GST) per separately used or inhabited

part of any "serviceable" rating unit to which connection is

available to receive an ordinary supply of water within the meaning of the

Dunedin City Bylaws excepting properties in Karitane, Merton, Rocklands/Pukerangi,

Seacliff, Waitati, Warrington, East Taieri, West Taieri and North Taieri.

· $671.80 (including GST) per unit of water being one cubic

metre (viz. 1,000 litres) per day supplied at a constant rate of

flow during a full 24 hour period to any "connected" rating unit

situated in Karitane, Merton, Seacliff, Waitati, Warrington, West Taieri, East

Taieri or North Taieri.

· $335.90 (including GST) per separately used or inhabited

part of any "serviceable" rating unit situated in Waitati,

Warrington, West Taieri, East Taieri or North Taieri. This rate shall not

apply to the availability of water in Merton, Karitane or Seacliff.

7.

Fire Protection Rates

A targeted

rate for the provision of a fire protection service, set under section 16

of the Local Government (Rating) Act 2002, assessed on a differential basis as

follows:

· A rate of 0.0860 cents in the dollar (including GST) of

capital value on all rating units in the "commercial" category.

This rate shall not apply to churches.

· A rate of 0.0645 cents in the dollar (including GST) of

capital value on all rating units in the "residential institutions"

category.

· A rate of 0.0084 cents in the dollar (including GST) of

capital value on the “stadium: 10,000+ seat capacity” category.

· $201.54 (including GST) for each separately used or

inhabited part of a rating unit within the "residential, residential

heritage bed and breakfasts, lifestyle and farmland" category that is not

receiving an ordinary supply of water within the meaning of the Dunedin City

Bylaws.

8.

Water Rates – Quantity of Water

A targeted

rate for the quantity of water provided to any rating unit fitted with a water

meter, being an extraordinary supply of water within the meaning of the Dunedin

City Bylaws, set under section 19 of the Local Government (Rating) Act 2002,

according to the following scale of charges (GST inclusive):

|

|

Annual Meter Rental Charge

|

|

20mm nominal diameter

|

$186.93

|

|

25mm nominal diameter

|

$239.98

|

|

30mm nominal diameter

|

$266.51

|

|

40mm nominal diameter

|

$301.86

|

|

50mm nominal diameter

|

$611.32

|

|

80mm nominal diameter

|

$755.30

|

|

100mm nominal diameter

|

$796.30

|

|

150mm nominal diameter

|

$1,145.58

|

|

300mm nominal diameter

|

$1,486.60

|

|

70mm Hydrant Standpipe

|

$740.15

|

|

Reconnection Fee – includes the removal of water restrictors

installed due to non-compliance of the water bylaw

|

$520.98

|

|

Special Reading Fee

|

$70.80

|

|

|

Backflow Prevention Charge

|

|

Backflow Preventer Test

Fee

|

$147.94

|

|

Rescheduled Backflow

Preventer Test Fee

|

$88.30

|

|

Backflow Programme - incomplete application fee (hourly rate)

|

$51.94

|

|

|

Water Charge

|

|

Merton, Hindon and individual farm supplied Bulk Raw Water Tariff

|

$0.15 per cubic metre

|

|

All other treated water per cubic metre

|

$2.55 per cubic metre

|

|

|

Network Contributions

|

|

Disconnection of Water Supply – AWSCI to excavate

|

$290.12

|

|

Disconnection of Water Supply – DCC contractor to excavate

|

$1,136.73

|

Where the

supply of a quantity of water is subject to this Quantity of Water Targeted

Rate, the rating unit will not be liable for any other targeted rate for the

supply of the same water.

9.

Allanton Drainage Rate

A targeted

rate for the capital contribution towards the Allanton Wastewater Collection

System, set under section 16 of the Local Government (Rating) Act 2002, of

$411.00 (including GST) per rating unit, to every rating unit paying their

contribution towards the scheme as a targeted rate over 20 years.

Liability for the rate is on the basis of the provision of the service to each

rating unit. The Allanton area is shown in the map below:

10.

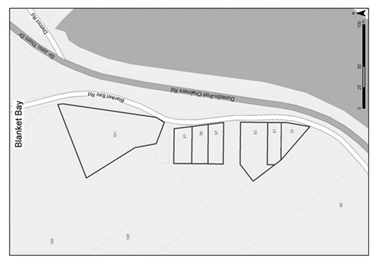

Blanket Bay Drainage Rate

A targeted

rate for the capital contribution towards the Blanket Bay Drainage System, set

under section 16 of the Local Government (Rating) Act 2002, of $636.00

(including GST) per rating unit, to every rating unit paying their contribution

towards the scheme as a targeted rate over 20 years. Liability for

the rate is on the basis of the provision of the service to each rating

unit. The Blanket Bay area is shown in the map below:

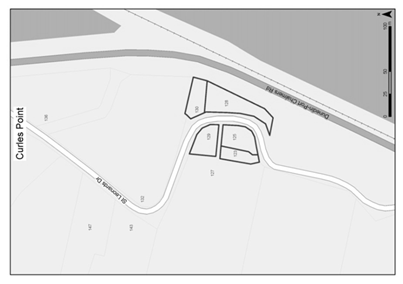

11. Curles Point Drainage Rate

1

A targeted rate for the capital contribution towards the Curles Point

Drainage System, set under section 16 of the Local Government (Rating) Act

2002, of $749.00 (including GST) per rating unit, to every rating unit paying

their contribution towards the scheme as a targeted rate over

20 years. Liability for the rate is on the basis of the provision of

the service to each rating unit. The Curles Point area is shown in the

map below:

12. Warm Dunedin

Targeted Rate Scheme

A targeted rate for the Warm Dunedin Targeted Rate Scheme,

set under section 16 of the Local Government (Rating) Act 2002, per rating unit

in the Warm Dunedin Targeted Rate Scheme.

The targeted rate scheme provides a way for homeowners to

install insulation and/or clean heating. The targeted rate covers the

cost and an annual interest rate. The interest rates have been and will

be:

Rates commencing 1 July 2013 and 1 July 2014 8%

Rates commencing 1 July 2015 and 1 July 2016 8.3%

Rates commencing 1 July 2017 7.8%

Rates commencing 1 July 2018 7.2%

Rates commencing 1 July 2019 6.8%

Rates commencing 1 July 2020 5.7%

Rates commencing 1 July 2021 4.4%

13. Private Street

Lighting Rate

A targeted

rate for the purpose of recovering the cost of private street lights, set under

section 16 of the Local Government (Rating) Act 2002, assessed on a

differential basis as follows:

· $156.80 (including GST) per private street light divided by

the number of separately used or inhabited parts of a rating unit for all

rating units in the "residential and lifestyle" categories in the

private streets as identified in the schedule below.

· $156.80 (including GST) per private street light divided by

the number of rating units for all rating units in the "commercial"

category in the private streets as identified in the schedule below.

Differential Matters and Categories

b) Adopts the following

differential categories for the 2025/26 financial year.

The differential categories are determined in accordance

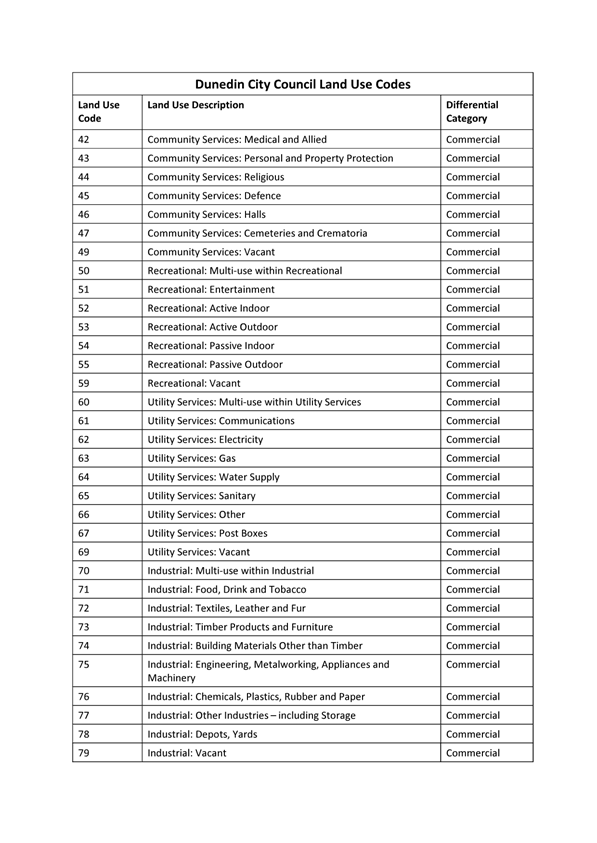

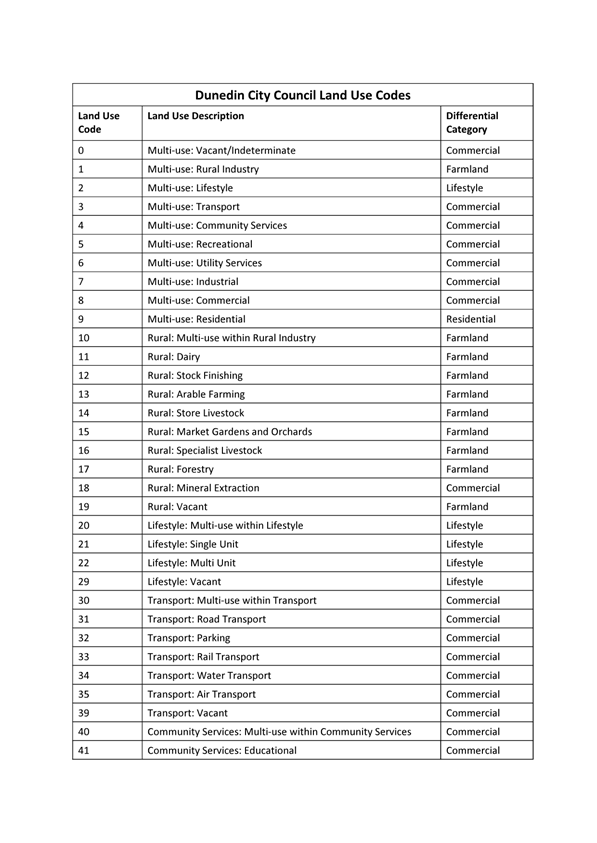

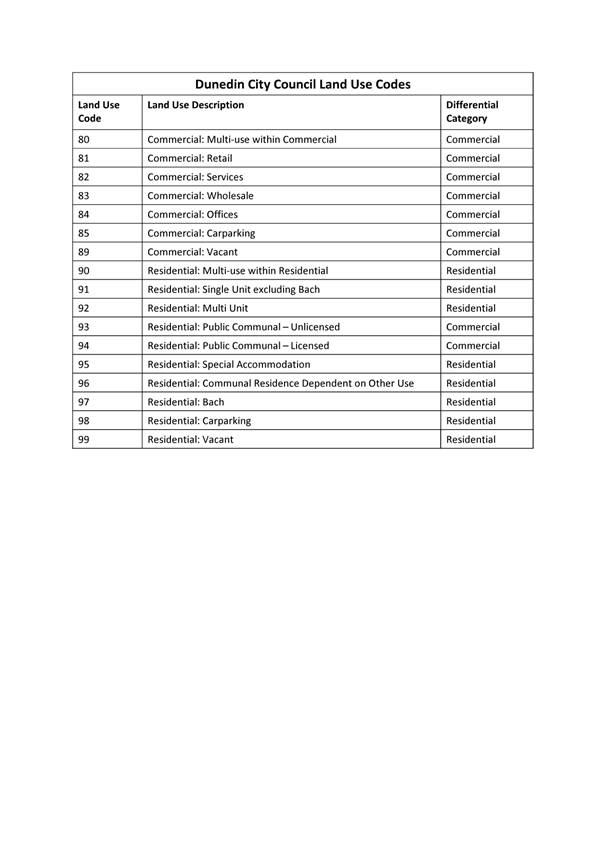

with the Council's land use codes. The Council's land use codes are based

on the land use codes set under the Rating Valuation Rules 2008 and are set out

in Attachment A. In addition, the Council has established categories for

residential institutions, residential heritage bed and breakfasts, the stadium:

10,000+ seat capacity, churches, and schools.

1.

Differentials Based on Land Use

The Council

uses this matter to:

· Differentiate the General rate.

· Differentiate the Community Services rate.

· Differentiate the Kerbside Collection rate.

· Differentiate the Private Street Lighting rate.

· Differentiate the Fire Protection rate.

The

differential categories based on land use are:

· Residential – includes all rating units used for

residential purposes including single residential, multi-unit residential,

multi-use residential, residential special accommodation, residential communal

residence dependant on other use, residential bach/cribs, residential

carparking and residential vacant land.

· Lifestyle – includes all rating units with Council's

land use codes 2, 20, 21, 22 and 29.

· Commercial – includes all rating units with land uses

not otherwise categorised as Residential, Residential Heritage Bed and

Breakfasts, Lifestyle, Farmland or Stadium: 10,000+ seat capacity.

· Farmland - includes all rating units used solely or

principally for agricultural or horticultural or pastoral purposes.

· Residential Heritage Bed and Breakfasts – includes

all rating units meeting the following description:

· Bed and breakfast establishments; and

· Classified as commercial for rating purposes due to the

number of bedrooms (greater than four); and

· Either:

· the majority of the establishment is at least 80 years old,

or

· the establishment has Heritage New Zealand Pouhere Taonga

Registration, or

· the establishment is a Dunedin City Council Protected

Heritage Building as identified in the District Plan; and

· The bed and breakfast owner lives at the facility.

· Stadium: 10,000+ seat capacity – this includes land

at 130 Anzac Avenue, Dunedin, Assessment 4026695, Valuation reference

27190-01403.

2. Differentials Based on Land Use and Provision or

Availability of Service

The Council

uses these matters to differentiate the drainage rate and the commercial

drainage rate.

The

differential categories based on land use are:

· Residential – includes all rating units used for

residential purposes including single residential, multi-unit residential,

multi-use residential, residential special accommodation, residential communal

residence dependant on other use, residential bach/cribs, residential

carparking and residential vacant land.

· Lifestyle - includes all rating units with Council's land

use codes 2, 20, 21, 22 and 29.

· Farmland - includes all rating units used solely or

principally for agricultural or horticultural or pastoral purposes.

· Commercial – includes all rating units with land uses

not otherwise categorised as Residential, Residential Heritage Bed and

Breakfasts, Lifestyle, Farmland, Residential Institutions, Stadium: 10,000+

seat capacity, Churches or Schools.

· Stadium: 10,000+ seat capacity – this includes land

at 130 Anzac Avenue, Dunedin, Assessment 4026695, Valuation reference

27190-01403.

· Residential Heritage Bed and Breakfasts – includes

all rating units meeting the following description:

· Bed and breakfast establishments; and

· Classified as commercial for rating purposes due to the

number of bedrooms (greater than four); and

· Either:

• the

majority of the establishment is at least 80 years old or

• the

establishment has Heritage New Zealand Pouhere Taonga Registration or

• the

establishment is a Dunedin City Council Protected Heritage Building as identified

in the District Plan; and

· The bed and breakfast owner lives at the facility.

· Residential Institutions - includes only rating units with

the Council's land use codes 95 and 96.

· Churches – includes all rating units used for places

of religious worship.

· Schools - includes only rating units used for schools that

do not operate for profit.

The

differential categories based on provision or availability of service are:

· Connected – any rating unit that is connected to a

public sewerage drain.

· Serviceable – any rating unit that is not connected

to a public sewerage drain but is capable of being connected to the sewerage

system (being a property situated within 30 metres of a public drain).

3. Differentials Based on Provision or Availability

of Service

The

Council uses this matter to differentiate the water rates.

The

differential categories based on provision or availability of service are:

· Connected – any rating unit that is supplied by the

water supply system.

· Serviceable – any rating unit that is not supplied

but is capable of being supplied by the water supply system (being a rating

unit situated within 100 metres of the nearest water supply).

Minimum Rates

c) Approves that where

the total amount of rates payable in respect of any rating unit is less than

$5.00 including GST, the rates payable in respect of the rating unit shall be

such amount as the Council determines but not exceeding $5.00 including GST.

Low Value Rating Units

d) Approves that rating

units with a capital value of $8,500 or less will only be charged the general

rate.

Land Use Codes

e) Approves that the land

use codes attached to this report are adopted as the Council's land use codes

for the purpose of the rating method.

Separately Used or Inhabited Part of a

Rating Unit

f) Adopts the following

definition of a separately used or inhabited part of a rating unit:

"A

separately used or inhabited part of a rating unit includes any portion

inhabited or used by the owner/a person other than the owner, and who has the

right to use or inhabit that portion by virtue of a tenancy, lease, licence, or

other agreement.

This

definition includes separately used parts, whether or not actually occupied at

any particular time, which are provided by the owner for rental (or other form

of occupation) on an occasional or long term basis by someone other than the

owner.

For the

purpose of this definition, vacant land and vacant premises offered or intended

for use or habitation by a person other than the owner and usually used as such

are defined as 'used'.

For the

avoidance of doubt, a rating unit that has a single use or occupation is

treated as having one separately used or inhabited part."

Lump Sum Contributions

g) Approves that no lump

sum contributions will be sought for any targeted rate.

Rating by Instalments

h) Approves the following

schedule of rates to be collected by the Council, payable by four instalments.

The City is divided into four

areas based on Valuation Roll Numbers, as set out below:

|

Area 1

|

Area 2

|

Area 3

|

Area 3 continued

|

|

Valuation Roll

Numbers:

|

|

26700

|

26990

|

26500

|

27550

|

|

26710

|

27000

|

26520

|

27560

|

|

26760

|

27050

|

26530

|

27600

|

|

26770

|

27060

|

26541

|

27610

|

|

26850

|

27070

|

26550

|

27760

|

|

26860

|

27080

|

26580

|

27770

|

|

26950

|

27150

|

26590

|

27780

|

|

26960

|

27350

|

26620

|

27790

|

|

26970

|

27360

|

26640

|

27811

|

|

26980

|

27370

|

26651

|

27821

|

|

27160

|

27380

|

26750

|

27822

|

|

27170

|

27500

|

26780

|

27823

|

|

27180

|

27510

|

27250

|

27831

|

|

27190

|

27520

|

27260

|

27841

|

|

27200

|

27851

|

27270

|

27871

|

|

|

27861

|

27280

|

27911

|

|

|

27880

|

27450

|

27921

|

|

|

27890

|

27460

|

27931

|

|

|

27901

|

27470

|

27941

|

|

|

28000

|

|

|

|

|

28010

|

|

|

|

|

28020

|

|

|

Area 4 comprises ratepayers with multiple

assessments who pay on a schedule.

Due Dates for Payment of Rates

i) Approves the due dates

for all rates with the exception of water rates, which are charged based on

water meter consumption, will be payable in four instalments due on the dates

below:

|

|

Area 1

|

Area 2

|

Area 3

|

Area 4

|

|

Instalment 1

|

29/08/25

|

12/09/25

|

26/09/25

|

12/09/25

|

|

Instalment 2

|

21/11/25

|

05/12/25

|

19/12/25

|

05/12/25

|

|

Instalment 3

|

20/02/26

|

27/02/26

|

13/03/26

|

27/02/26

|

|

Instalment 4

|

15/05/26

|

22/05/26

|

05/06/26

|

22/05/26

|

Water meter invoices are sent separately from other

rates. Where water rates are charged based on metered consumption using a

meter other than a Smart Water Meter, invoices are sent on a quarterly or

monthly basis and the due date for payment shall be on the 20th of the month

following the date of the invoice as set out in the table below:

|

Date of

Invoice

|

Date for

Payment

|

|

July 2025

|

20 August 2025

|

|

August 2025

|

20 September 2025

|

|

September 2025

|

20 October 2025

|

|

October 2025

|

20 November 2025

|

|

November 2025

|

20 December 2025

|

|

December 2025

|

20 January 2026

|

|

January 2026

|

20 February 2026

|

|

February 2026

|

20 March 2026

|

|

March 2026

|

20 April 2026

|

|

April 2026

|

20 May 2026

|

|

May 2026

|

20 June 2026

|

|

June 2026

|

20 July 2026

|

Penalties

j) Resolves to charge the

following penalties on unpaid rates:

1 A

charge of 10% of the unpaid rates instalment will be added to the amount of any

instalment remaining unpaid the day after the instalment due date set out

above.

2 Where

a ratepayer has not paid the first instalment by the due date of that

instalment, and has paid the total rates and charges in respect of the rating

unit for the 2025/26 rating year by the due date of the second instalment, the

10% additional charge for the first instalment shall be remitted.

3 For

amounts levied in any previous financial year and which remain unpaid on

1 October 2025, 10% of that sum shall be charged, including additional

charges (if any).

4 For

amounts levied in any previous financial year and which remain unpaid on

1 April 2026, 10% of that sum shall be charged, including additional

charges (if any).

Assessing and Recovering Rates

k) Approves

that the Chief Executive Officer, Chief Financial Officer and Rates and Revenue

Team Leader be authorised to take all necessary steps to assess and recover the

above rates.

BACKGROUND

2. The rating method for the 2025/26 year formed part of the

supporting documentation made available during the community engagement period

of the 9 year plan 2025-34.

3. On 28

January 2025, the rating method 2025/26 was presented to Council with a

recommendation to combine the Tourism/Economic Development targeted rate into the

Commercial General Rate. Council resolved as follows:

Moved (Cr Bill Acklin/Cr Steve Walker):

That the

Council:

a) Approves an increase in the Community Services targeted rate for the 2025/26 year

of $4.00 to $121.00 including GST.

c) Combines

the Tourism/Economic Development targeted rate into the Commercial General

Rate.

d) Approves

the current rating method for the setting of all other rates for the 2025/26 year.

Motion carried (CNL/2025/001)

2

3

Please note that unless specified, all rating figures in this report are

GST inclusive.

DISCUSSION

4. The

rating method for the 2025/26 year incorporates the following changes:

· An increase in the Community Services targeted rate from $117.00 to

$121.00.

· The differentiated stadium: 10,000+ capacity rates have been

increased by the June 2024 Local Government Cost Index of 3.3%.

· The Tourism/Economic Development targeted rate is combined into the

Commercial General Rate.

Limit on

"Fixed" Charging

5. Section

21 of the Local Government (Rating) Act 2002 includes a limit on certain

rates. In any one year, the Council may not collect more than 30% of its

total rates revenue by way of:

· Any uniform

annual general charge.

· Any targeted

rate that is calculated as a fixed amount per rating unit or separately used or

inhabited part of a rating unit (and which is not used solely for water supply

or sewage disposal).

6. The

Council does not use a uniform annual general charge. The relevant

targeted rates for the 2025/26 year are the Kerbside Collection rate, the Community

Services rate and the Drainage fixed charge. These rates equate to 24% of

total rates revenue.

OPTIONS

7. The

option provided is to set rates in accordance with the Local Government Act

2002 and the Local Government (Rating) Act 2002 in order to provide rates

funding in the 2025/26 year in accordance with the 2025/26 budget.

NEXT STEPS

8. The

Council can now set and assess the rates described in its Funding Impact

Statement.

a)

Signatories

|

Author:

|

Hayden McAuliffe - Financial Services Manager

|

|

Authoriser:

|

Carolyn Allan - Chief Financial Officer

|

Attachments

|

|

Title

|

Page

|

|

⇩a

|

Land use codes

|

37

|

|

SUMMARY OF CONSIDERATIONS

|

|

Fit with purpose of Local Government

This decision enables democratic local

decision making and action by, and on behalf of communities and promotes the

social, economic, environmental and cultural well-being of communities in the

present and for the future.

|

|

Fit with strategic framework

|

|

Contributes

|

Detracts

|

Not applicable

|

|

Social Wellbeing Strategy

|

✔

|

☐

|

☐

|

|

Economic Development Strategy

|

✔

|

☐

|

☐

|

|

Environment Strategy

|

✔

|

☐

|

☐

|

|

Arts and Culture Strategy

|

✔

|

☐

|

☐

|

|

3 Waters Strategy

|

✔

|

☐

|

☐

|

|

Future Development Strategy

|

✔

|

☐

|

☐

|

|

Integrated Transport Strategy

|

✔

|

☐

|

☐

|

|

Parks and Recreation Strategy

|

✔

|

☐

|

☐

|

|

Other strategic projects/policies/plans

|

✔

|

☐

|

☐

|

This decision fits with the strategic framework because it

provides the necessary rates funding to implement the activities outlined in

the 9 year plan 2025-34.

|

|

Māori Impact Statement

As part of the DCC’s ongoing commitment to working

in partnership with mana whenua, consultation and engagement processes for

the 9 year plan ensured opportunities for Māori, both mana whenua and

mātāwaka, to contribute to the decision-making process.

|

|

Sustainability

There are no implications for sustainability.

|

|

Zero carbon

There

are no implications for emissions.

|

|

LTP/Annual Plan / Financial Strategy /Infrastructure

Strategy

The Council has adopted the 9 year plan 2025-34 and can

now set and assess the rates described in its Funding Impact Statement for

the 2025/26 year.

|

|

Financial considerations

The Council has adopted the 9 year plan 2025-34 and can

now set and assess the rates described in its Funding Impact Statement.

|

|

Significance

The decision sets the rates for the 2025/26 year as

outlined in the 9 year plan 2025-34.

|

|

Engagement – external

Community engagement was undertaken as part of the 9 year

plan 2025-34 process.

|

|

Engagement - internal

Internal engagement has occurred with staff in the

relevant departments.

|

|

Risks: Legal / Health and Safety etc.

Legal risks were considered, and appropriate advice

sought.

|

|

Conflict of Interest

There are no known conflicts of interest.

|

|

Community Boards

Community Boards may be interested in this report and were

involved in the 9 year plan 2025-34 engagement.

|