Notice of Meeting:

I hereby give notice that an ordinary meeting of the Audit

and Risk Subcommittee will be held on:

Date: Monday

1 September 2025

Time: 11.30

am

Venue: Council

Chamber, Dunedin Public Art Gallery, The Octagon, Dunedin

Sandy Graham

Audit and Risk Subcommittee

PUBLIC AGENDA

|

Chairperson

|

Warren Allen

|

|

|

Deputy Chairperson

|

Janet Copeland

|

|

|

Members

|

Cr Christine Garey

|

Cr Cherry Lucas

|

|

|

Mayor Jules Radich

|

Cr Lee Vandervis

|

Senior Officer Carolyn

Allan, Chief Financial Officer

Governance Support Officer Wendy

Collard

Wendy Collard

Governance Support Officer

Telephone: 03 477 4000

Wendy.Collard@dcc.govt.nz

www.dunedin.govt.nz

Note: Reports

and recommendations contained in this agenda are not to be considered as

Council policy until adopted.

|

|

Audit and Risk Subcommittee

1 September 2025

|

ITEM TABLE OF CONTENTS PAGE

1 Apologies 4

2 Confirmation

of Agenda 4

3 Declaration

of Interest 5

4 Confirmation

of Minutes 10

4.1 Audit and Risk

Subcommittee meeting - 16 June 2025 10

Part

A Reports (Committee has power to decide these matters)

5 Health,

Safety and Wellbeing Monthly report for July 2025 21

6 Audit

and Risk Subcommittee Work Plan 2025 40

7 Audit

and Risk Subcommittee Updates Report - September 2025 44

8 DCC

Policy Update Report 50

9 Financial

Report - Period ended 30 June 2025 102

10 Financial

Strategy Compliance 136

11 Waipori

Fund - Quarter ending 30 June 2025 145

Resolution to Exclude the Public 150

|

|

Audit and Risk Subcommittee

1 September 2025

|

1 Apologies

At the close of the agenda no

apologies had been received.

2 Confirmation

of agenda

Note:

Any additions must be approved by resolution with an explanation as to why they

cannot be delayed until a future meeting.

|

|

Audit and Risk Subcommittee

1 September 2025

|

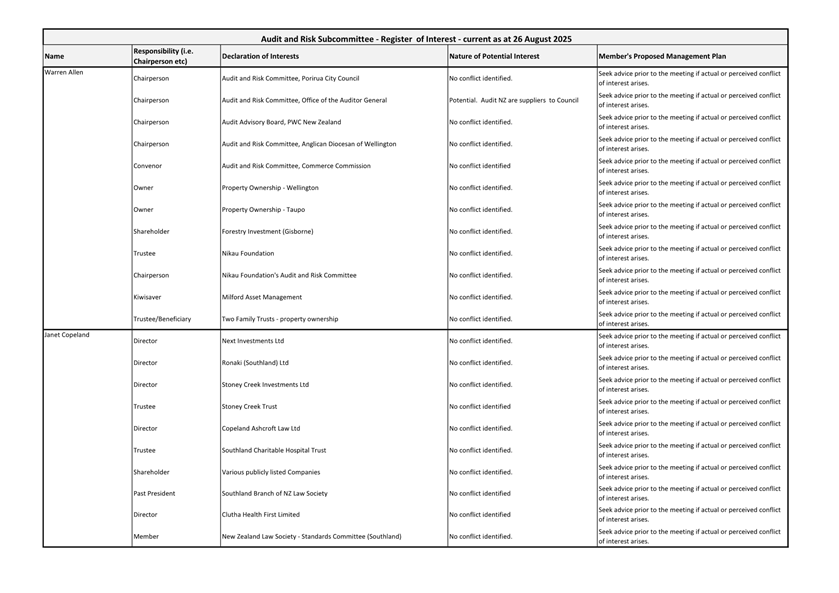

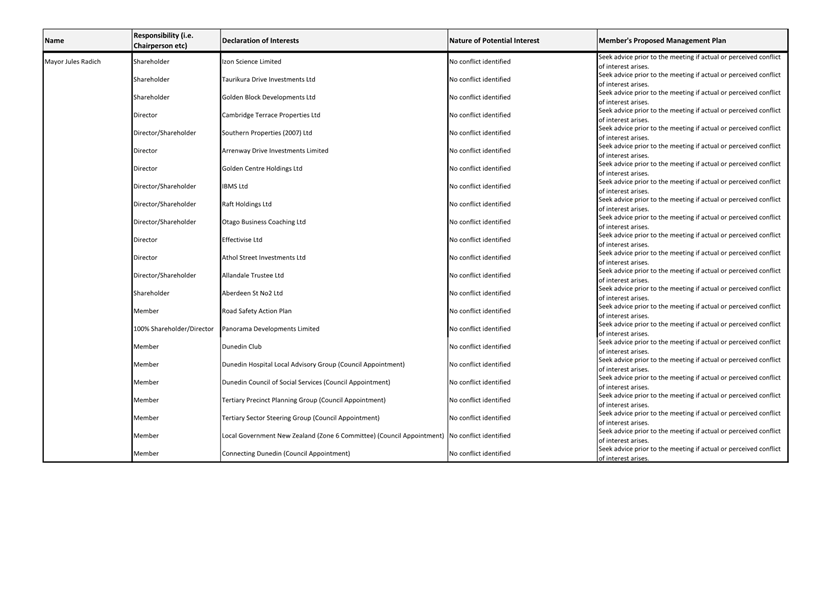

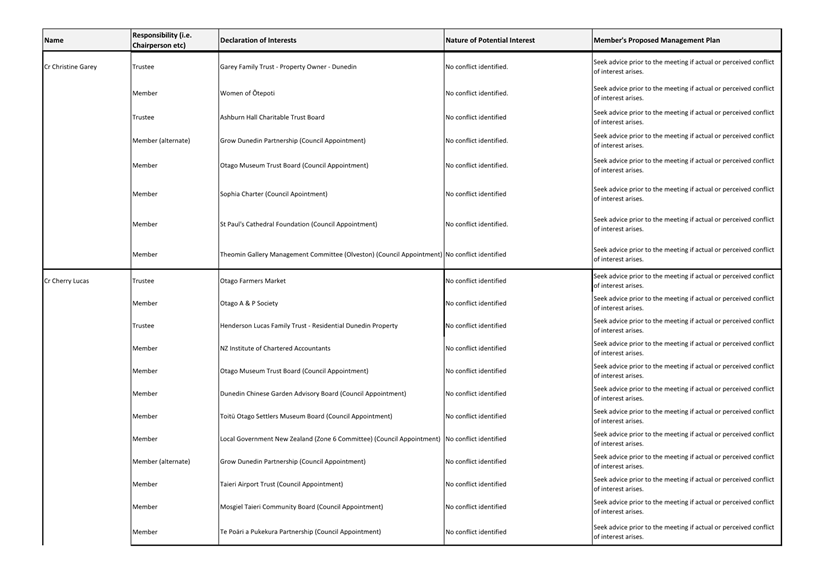

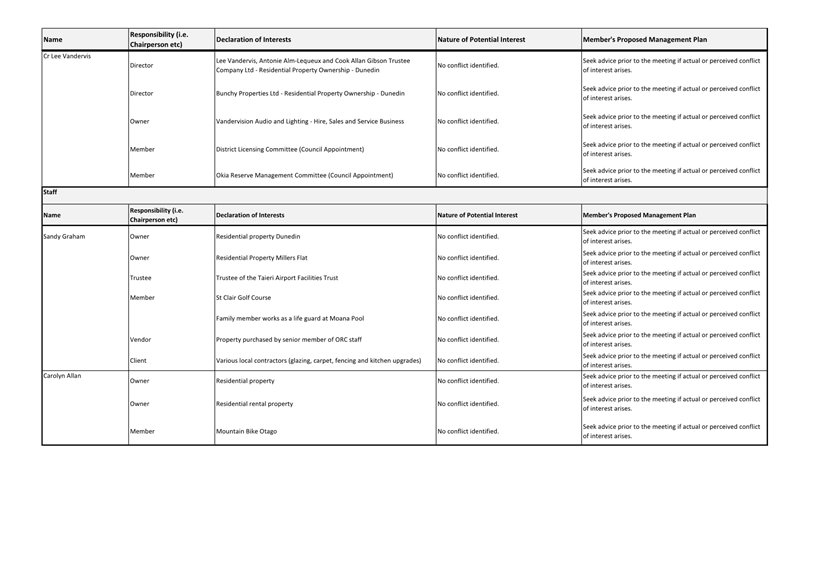

Declaration of Interest

EXECUTIVE SUMMARY

1. Members

are reminded of the need to stand aside from decision-making when a conflict

arises between their role as an elected or independent representative and any

private or other external interest they might have.

2. Elected

and Independent members are reminded to update their register

of interests as soon as practicable, including amending the register at this

meeting if necessary.

RECOMMENDATIONS

That the Subcommittee:

a) Notes/Amends if

necessary the Elected or Independent Members' Interest Register attached as

Attachment A; and

b) Confirms/Amends the

proposed management plan for Elected or Independent Members' Interests.

Attachments

|

|

Title

|

Page

|

|

⇩a

|

Register of Interest

|

6

|

|

|

Audit and Risk Subcommittee

1 September 2025

|

|

|

Audit and Risk Subcommittee

1 September 2025

|

Confirmation

of Minutes

Audit

and Risk Subcommittee meeting - 16 June 2025

RECOMMENDATIONS

That the Subcommittee:

a) Confirms the public

part of the minutes of the Audit and Risk Subcommittee meeting held on 16 June

2025 as a correct record.

Attachments

|

|

Title

|

Page

|

|

A⇩

|

Minutes of Audit and

Risk Subcommittee meeting held on 16 June 2025

|

11

|

|

|

Audit and Risk

Subcommittee

1 September 2025

|

Audit and Risk Subcommittee

MINUTES

Minutes of an ordinary

meeting of the Audit and Risk Subcommittee held in the Council Chamber, Dunedin

Public Art Gallery, The Octagon, Dunedin on Monday 16 June 2025, commencing at

11.30 am

PRESENT

|

Chairperson

|

Mr Warren Allen

|

|

|

Members

|

Cr Christine Garey

|

Cr Cherry Lucas

|

|

|

Cr Lee Vandervis

|

|

|

IN ATTENDANCE

|

Sandy Graham (Chief Executive

Officer), Rob West (General Manager Corporate Services), Hayden McAuliffe

(Financial Services Manager), Hayley Knight (Assurance Manager), Mandy Grieve

(Heath and Safety Advisor), Richard Davey (Treasurer, Dunedin City Holdings

Ltd), Serge Kolman (Procurement and Contracts Manager), Jackie Harrison

(Manager Governance), Cr Sophie Barker and Cr Carmen Houlahan

|

Governance Support Officer Wendy

Collard

.

|

1 Apologies

|

|

|

Moved (Warren Allen/Cr Cherry Lucas):

That the Subcommittee:

Accepts the apology from

Janet Copeland (for absence) and Mayor Radich (for lateness)

Motion

carried (AR/2025/014)

|

|

2 Confirmation

of agenda

|

|

|

Moved (Warren Allen/Cr Cherry Lucas):

That the Subcommittee:

Confirms the agenda

without addition or alteration

Motion

carried (AR/2025/015)

|

3 Declarations

of interest

Members were

reminded of the need to stand aside from decision-making when a conflict arose

between their role as an elected representative and any private or other

external interest they might have.

|

|

Moved (Warren Allen/Cr Cherry Lucas):

That the Subcommittee:

a) Notes the Elected or Independent Members' Interest Register; and

b) Confirms the proposed management plan for

Elected or Independent Members' Interests.

Motion

carried (AR/2025/016)

|

4 Confirmation

of Minutes

|

4.1 Audit

and Risk Subcommittee meeting - 10 March 2025

|

|

|

Moved (Warren Allen/Cr Cherry Lucas):

That the Subcommittee:

a) Confirms the public part of the minutes of the

Audit and Risk Subcommittee meeting held on 10 March 2025 as a correct

record.

Motion

carried (AR/2025/017)

|

Part

A Reports

|

5 Audit

and Risk Subcommittee Work Plan 2025

|

|

|

A report from Civic provided

the Audit and Risk Subcommittee Work Plan 2025 which has been aligned with

work programme scheduling and decision making.

The Chief Executive Officer

(Sandy Graham) and the Assurance Manager (Hayley Knight) spoke to the report

and responded to questions.

|

|

|

Moved (Warren Allen/Cr Cherry Lucas):

That the Committee:

a) Notes the Audit and Risk Subcommittee Work Plan for 2025

Motion

carried (AR/2025/018)

|

|

6 Audit

and Risk Subcommittee Updates Report - June 2025

|

|

|

A report from Civic provided

updates on the progress of various sundry matters that have been noted by the

Subcommittee.

The Chief Executive Officer

(Sandy Graham), the Financial Services Manager (Hayden McAuliffe) and the

Assurance Manager (Hayley Knight) spoke to the report and responded to

questions.

|

|

|

Moved (Warren Allen/Cr Cherry Lucas):

That the Committee:

a) Notes the Audit and Risk Subcommittee Updates Report

– June 2025

Motion

carried (AR/2025/019)

|

|

7 Financial

Report - Period ended 30 April 2025

|

|

|

A report

from Finance provided the financial results for the period ended 30 April

2025 and the financial position as at that date. It noted that the

report was presented to the Finance and Council Controlled Committee meeting

held on 11June 2025.

The Financial Services

Manager (Hayden McAuliffe) spoke to the report and responded to questions.

|

|

|

Moved (Warren Allen/Cr Cherry Lucas):

That the Subcommittee:

a) Notes the Financial Performance for the period ended 30

April 2025 and the Financial Position as at that date.

Motion

carried (AR/2025/020)

|

|

8 Waipori

Fund - Quarter Ending 31 March 2025

|

|

|

A report from Dunedin City

Treasury Limited provided information on the results of the Waipori Fund for

the quarter ended 31 March 2025. It noted that the report was presented

to the Finance and Council Controlled Committee meeting held on 11June 2025.

The Treasurer, Dunedin City Treasury Limited (Richard

Davey) spoke to the report and responded to questions.

|

|

|

Moved (Warren Allen/Cr Cherry Lucas):

That the Subcommittee:

a) Notes the report from Dunedin City Treasury Limited on the

Waipori Fund for the quarter ended 31 March 2025

Motion

carried (AR/2025/021)

|

|

9 Health,

Safety and Wellbeing monthly report for April 2025

|

|

|

A report from Health and

Safety provided the monthly Health, Safety and Wellbeing report for April

2025 for the Subcommittee’s information.

The General Manager Corporate (Robert West) and the Health

and Safety Advisor (Mandy Grieve) spoke to the report and responded to questions.

|

|

|

Moved (Warren Allen/Cr Christine Garey):

That the Subcommittee:

a) Notes the monthly Health, Safety and Wellbeing report for April

2025.

Motion

carried (AR/2025/022)

|

|

Resolution to Exclude the Public

|

|

Moved (Warren Allen/Cr Cherry Lucas):

That the Subcommittee:

Pursuant

to the provisions of the Local Government Official Information and Meetings

Act 1987, exclude the public from the following part of the proceedings of

this meeting namely:

|

General

subject of the matter to be considered

|

Reasons for

passing this resolution in relation to each matter

|

Ground(s) under

section 48(1) for the passing of this resolution

|

Reason for

Confidentiality

|

|

C1

Audit and Risk Subcommittee meeting - 10 March 2025 - Public Excluded

|

S7(2)(h)

The withholding of

the information is necessary to enable the local authority to carry out,

without prejudice or disadvantage, commercial activities.

S7(2)(b)(ii)

The withholding of

the information is necessary to protect information where the making

available of the information would be likely unreasonably to prejudice the

commercial position of the person who supplied or who is the subject of the

information.

S7(2)(b)(i)

The withholding of

the information is necessary to protect information where the making

available of the information would disclose a trade secret.

S7(2)(c)(i)

The withholding of

the information is necessary to protect information which is subject to an

obligation of confidence or which any person has been or could be compelled

to provide under the authority of any enactment, where the making available

of the information would be likely to prejudice the supply of similar

information or information from the same source and it is in the public

interest that such information should continue to be supplied.

S7(2)(a)

The withholding of

the information is necessary to protect the privacy of natural persons,

including that of a deceased person.

S7(2)(g)

The withholding of

the information is necessary to maintain legal professional privilege.

|

.

|

|

|

C2

Audit Arrangements for the year ending 30 June 2025

|

S7(2)(i)

The withholding of

the information is necessary to enable the local authority to carry on,

without prejudice or disadvantage, negotiations (including commercial and

industrial negotiations).

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C3

Long Term Plan Consultation Document Audit

|

S7(2)(i)

The withholding of

the information is necessary to enable the local authority to carry on,

without prejudice or disadvantage, negotiations (including commercial and

industrial negotiations).

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C4

DCC Risk 'Deep Dive' - Procurement and Contract Management

|

S7(2)(c)(i)

The withholding of

the information is necessary to protect information which is subject to an

obligation of confidence or which any person has been or could be compelled

to provide under the authority of any enactment, where the making available

of the information would be likely to prejudice the supply of similar

information or information from the same source and it is in the public

interest that such information should continue to be supplied.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C5

Improvement Opportunities

|

S7(2)(a)

The withholding of

the information is necessary to protect the privacy of natural persons,

including that of a deceased person.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C6

Internal Audit Workplan Update

|

S7(2)(b)(i)

The withholding of

the information is necessary to protect information where the making

available of the information would disclose a trade secret.

S7(2)(c)(i)

The withholding of

the information is necessary to protect information which is subject to an

obligation of confidence or which any person has been or could be compelled

to provide under the authority of any enactment, where the making available

of the information would be likely to prejudice the supply of similar

information or information from the same source and it is in the public

interest that such information should continue to be supplied.

S7(2)(h)

The withholding of

the information is necessary to enable the local authority to carry out,

without prejudice or disadvantage, commercial activities.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C7

DCC External Audit Actions Update - June 2025

|

S7(2)(c)(i)

The withholding of

the information is necessary to protect information which is subject to an

obligation of confidence or which any person has been or could be compelled

to provide under the authority of any enactment, where the making available

of the information would be likely to prejudice the supply of similar

information or information from the same source and it is in the public

interest that such information should continue to be supplied.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C8

Treasury Risk Management Compliance Report

|

S7(2)(h)

The withholding of

the information is necessary to enable the local authority to carry out,

without prejudice or disadvantage, commercial activities.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C9

Dunedin City Holdings Ltd - Update on Audit and Risk Activity

|

S7(2)(b)(ii)

The withholding of

the information is necessary to protect information where the making

available of the information would be likely unreasonably to prejudice the

commercial position of the person who supplied or who is the subject of the

information.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C10

Protected Disclosure Register - June 2025

|

S7(2)(a)

The withholding of

the information is necessary to protect the privacy of natural persons,

including that of a deceased person.

S7(2)(c)(i)

The withholding of

the information is necessary to protect information which is subject to an

obligation of confidence or which any person has been or could be compelled

to provide under the authority of any enactment, where the making available

of the information would be likely to prejudice the supply of similar

information or information from the same source and it is in the public

interest that such information should continue to be supplied.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C11

Investigation Register - June 2025

|

S7(2)(a)

The withholding of

the information is necessary to protect the privacy of natural persons,

including that of a deceased person.

S7(2)(c)(i)

The withholding of

the information is necessary to protect information which is subject to an

obligation of confidence or which any person has been or could be compelled

to provide under the authority of any enactment, where the making available

of the information would be likely to prejudice the supply of similar

information or information from the same source and it is in the public

interest that such information should continue to be supplied.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

This resolution is made in

reliance on Section 48(1)(a) of the Local Government Official Information and

Meetings Act 1987, and the particular interest or interests protected by

Section 6 or Section 7 of that Act, or Section 6 or Section 7 or Section 9 of

the Official Information Act 1982, as the case may require, which would be

prejudiced by the holding of the whole or the relevant part of the

proceedings of the meeting in public are as shown above after each item.

Motion

carried (AR/2025/023)

|

The meeting went into non-public at 12.36 pm and concluded

at 3.02 pm.

..............................................

CHAIRPERSON

|

|

Audit and Risk Subcommittee

1 September 2025

|

Part

A Reports

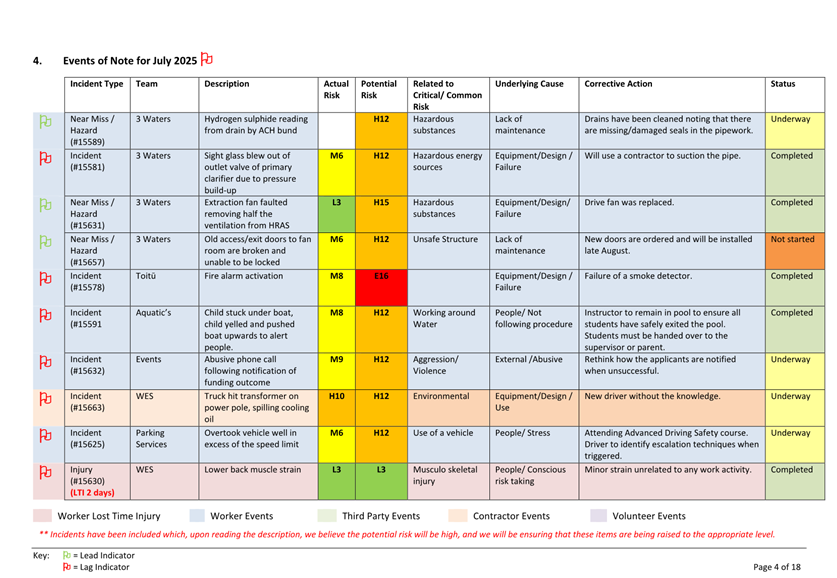

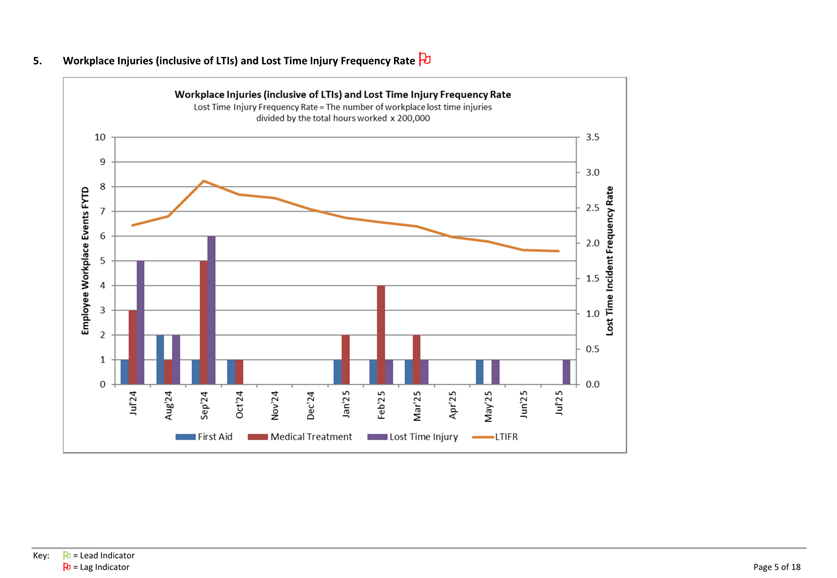

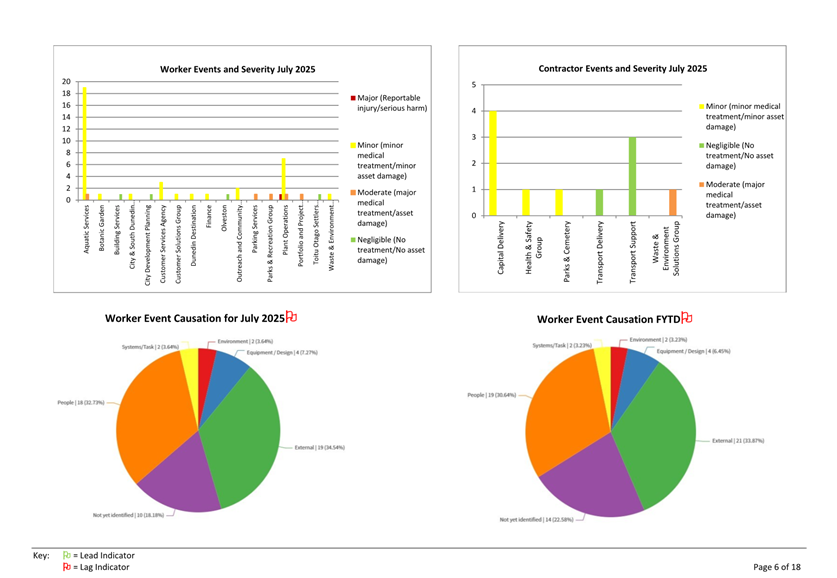

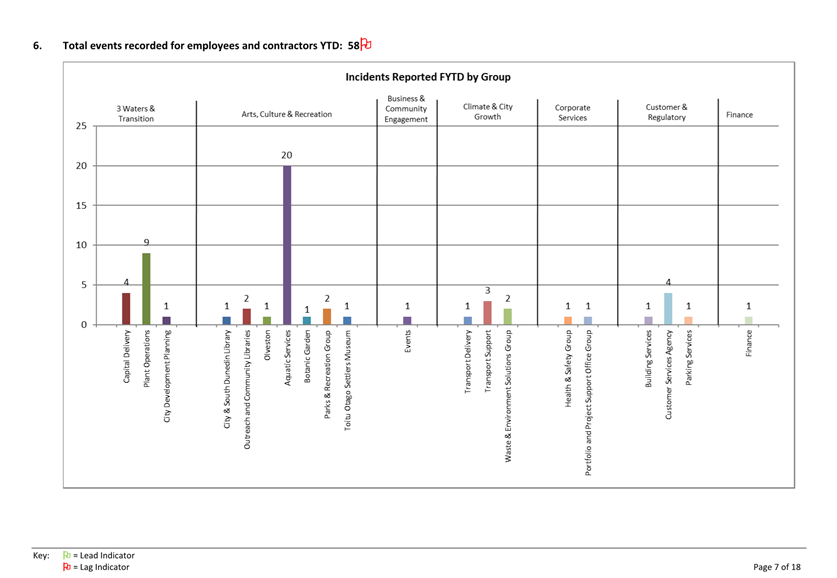

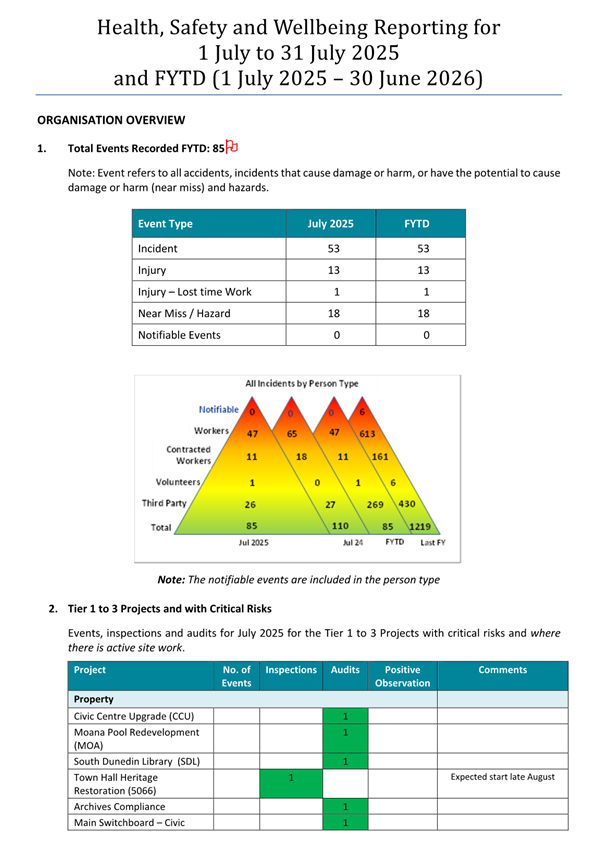

Health, Safety and Wellbeing Monthly report for July 2025

Department: Health and Safety

EXECUTIVE SUMMARY

1 The

monthly Health, Safety and Wellbeing report for July 2025 is attached for

consideration.

RECOMMENDATIONS

That the Subcommittee:

a) Notes the monthly

Health, Safety and Wellbeing report for July 2025.

Signatories

|

Author:

|

Jane Pearce - Health and Safety Manager

|

|

Authoriser:

|

David Ward - General Manager, 3 Waters and Transition

|

Attachments

|

|

Title

|

Page

|

|

⇩a

|

Health, Safety and Wellbeing

monthly report for July 2025

|

22

|

|

|

Audit and Risk Subcommittee

1 September 2025

|

|

|

Audit and Risk Subcommittee

1 September 2025

|

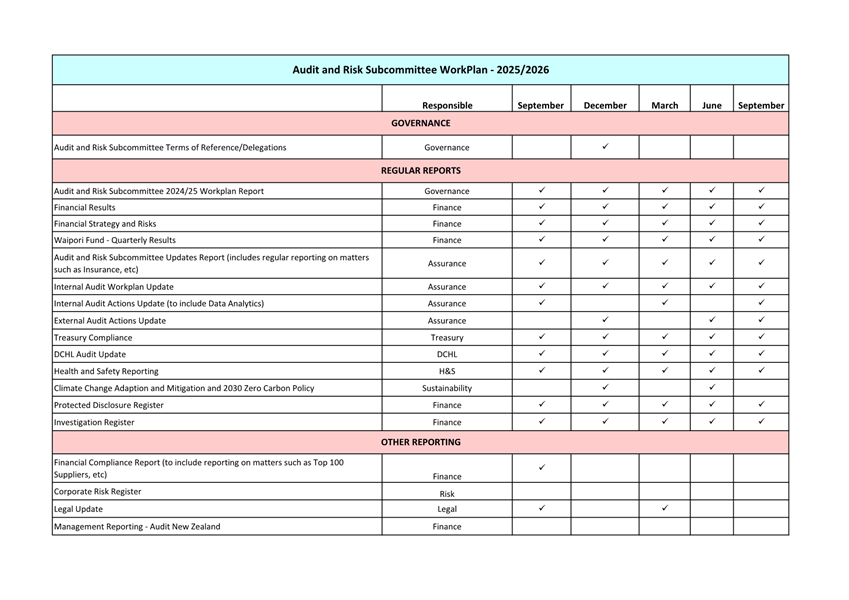

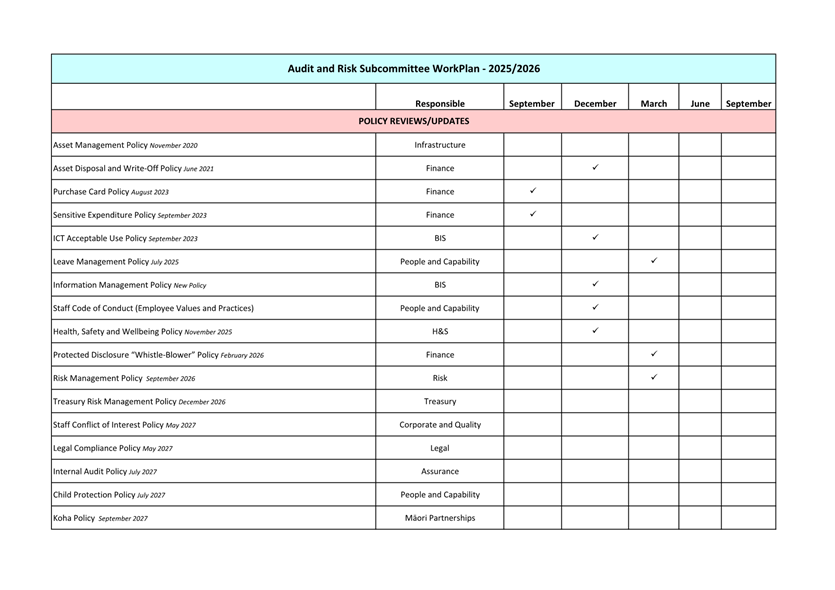

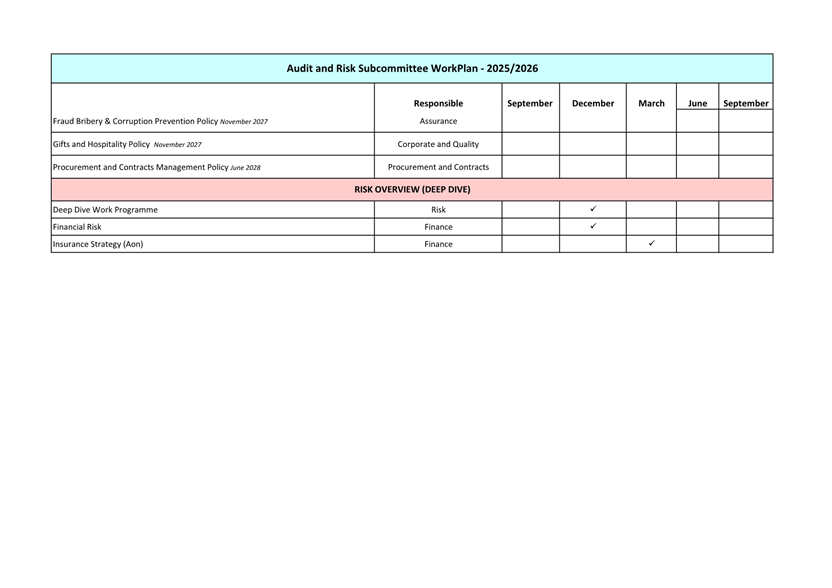

Audit and Risk Subcommittee Work Plan 2025

Department: Civic

EXECUTIVE SUMMARY

1 This

report provides a copy of the Audit and Risk Subcommittee Work Plan 2025 which

has been aligned with work programme scheduling and decision making.

2 Please

note that the items without ticks shown have not been scheduled for action. A

Deep Dive work programme will be developed after the Corporate Risk Register

has been reviewed. Deep dive topics will reflect high or emerging risks.

3 As

this is an administrative report only, the Summary of Consideration is not

required.

RECOMMENDATIONS

That the Subcommittee:

a) Notes the Audit and

Risk Subcommittee Work Plan for 2025.

Signatories

|

Author:

|

Wendy Collard - Governance Support Officer

|

|

Authoriser:

|

Carolyn Allan - Chief Financial Officer

|

Attachments

|

|

Title

|

Page

|

|

⇩a

|

Audit and Risk

Subcommittee Work Plan

|

41

|

|

|

Audit and Risk Subcommittee

1 September 2025

|

|

|

Audit and Risk Subcommittee

1 September 2025

|

Audit and Risk Subcommittee Updates Report - September 2025

Department: Finance

EXECUTIVE SUMMARY

1 This

report provides updates on the progress of various sundry matters that have

been noted by the Subcommittee.

RECOMMENDATIONS

That the Subcommittee:

a) Notes the Audit and

Risk Subcommittee Updates Report – September 2025

DISCUSSION

Insurance

2 The

main insurance renewal occurred on 30 June 2025 and incorporated the following

policies:

· Material

Damage Above Ground

· Business

Interruption Above Ground

· Material

Damage Below Ground Infrastructure

· Annual

Contract Works

· Fine

Arts

· Civil

Engineering – Taieri River Water Supply Viaduct Bridge

· Motor

Vehicle

· Liability

Policies – Internet, Crime, Directors, and Officers

· Travel

and Personal Accident

3 The

renewal process was completed on time with consistent terms and no changes to

loss limits or deductibles. Insured values were updated in line with current

above ground asset schedules and fleet assets. Cover under the annual contract

works policy was increased to reflect the larger capital programme in 2025/26.

Business interruption cover was updated based on recent modelling.

4 Overall,

a 7% reduction in premiums was achieved, reflecting improved market conditions,

saving approximately $400k on 2024/25 costs and approximately $500k against

budget.

5 The

remaining liability policies (general/public, statutory, professional indemnity

and employer) are due for renewal 1 November 2025. The renewal proposal

is currently being compiled in relation to these policies.

9-Year Plan

6 Audit

of the 9-year plan by Audit NZ started on 9th June and finished on

30th June 2025, resulting in an unqualified audit opinion.

7 Following

the audit process, Council adopted the plan on 30th June 2025.

8 Individual

letters were sent in response to submissions from each Community Board, and to

submitters with amenity or funding requests.

9 A

digital version of the 9-year plan was made available on the DCC website in the

week following its adoption. Two hard copies of the plan were sent to each DCC

service centre in early August.

2024/25 Annual Report

10 The interim

audit was completed in May. All audit requests have been submitted and

there are no outstanding requests.

11 Asset

valuations have been scheduled for three departments with the following

valuers:

· Transport

– Beca

· Property

(Investment Property portfolio only) – JLL

· Three

Waters - Beca

12 Audit New

Zealand will be engaging WSP as an auditors’ expert to assist with their

audit of the Three Waters valuation. There will continue to be a strong focus

between the Finance team and relevant departments to understand the rationale

for valuation adjustments.

13 The final

audit fieldwork will be commencing on the week of 15th September. The

Finance Team will have the financial statements for Core Council delivered to

Audit New Zealand on this date. The group consolidated financial

statements will be delivered by 7th October after the completion of the DCHL

audit.

14 Giving the

time required to complete audits of DCHL and the group companies, the 2024/25

Annual Report will not be ready for adoption by Council before the local

government elections on 11 October 2025.

15 Staff are

looking at presenting a draft, unaudited version of some sections of the

2024/25 Annual Report to the Council meeting on 23 September 2025, enabling the

current Council to review draft performance and results for the year ended 30

June 2025. The draft version would not include consolidated financial results.

16 Following

audit, the 2024/25 Annual Report will be adopted by Council at its inaugural

meeting of the new triennium on 31 October 2025.

17 The

Communications and Marketing Team have again been engaged to improve the

readability and presentation of the Annual Report document, building on work

done during the development of the 2023/24 Annual Report. Suggested work to

improve the presentation, accessibility and readability of the Annual Report

and Summary includes adding a performance snapshot, which summarises overall

performance of services and activities. Design elements will also be

considered such as layout, themes, images, and graphics, with a view to make

detailed reporting of service and activity performance more accessible to a

general reader. The proposed changes align with examples of accessible

and engaging Annual Reports and Summaries from the sector which have visual

elements to aid understanding and transparency of performance results.

2026/27 Annual Plan

18 Initial

work on the development of the 2026/27 Annual Plan has started. Staff will use

the development of the Plan as an opportunity to identify new or improved

revenue streams, and to review expenditure.

19 The

schedule for development of the 2026/27 Annual Plan includes sufficient time

for an amendment, including audit, should one be required to address a

significant or material change from Year 2 of the 9 Year Plan. Community

engagement is tentatively scheduled for March/April 2026.

20 The Annual

Plan 2026/27 will be adopted by Council by 30 June 2026.

Elections Update

21 Nominations

closed on 1st August with all areas requiring an election. We

received record number of candidates for Mayor and Councillors.

22 Candidate

Signs are now up, and full the campaigning has begun.

23 We are now

moving into voting period with special voting beginning on 9th

September, with an office opening in the plaza meeting room.

Local Water Done Well

24 The

Government is now in the final stage of their three-stage process implementing

its “Local Water Done Well” (LWDW) reform programme.

25 The third

stage of LWDW is in progress with the introduction of the Local Government

(Water Services) Bill (the December Bill) on 10 December 2024. The December

Bill provides the enduring settings for LWDW including the framework for

economic regulation as well as the more detailed powers and duties for service

delivery models. Council has made a submission on the Bill. The Bill which has

now been separated into two Bills is expected to be enacted in August 2025. The

Bills provide for:

a) Structural

arrangements for water service delivery including establishment, ownership, and

governance of water organisations.

b) Operational

matters such as arrangements for charging, bylaws, and management of stormwater

networks.

c) Planning,

reporting, and financial management.

d) A new

economic regulation and consumer protection regime.

e) Changes to

the water quality regulatory framework and the water services regulator.

f) Repeals

and amendments to other legislation resulting from the December Bill (separated

into a second Bill now).

26 Following

consultation on the Water Consultation Options, Council at its meeting on 26

May 2025 approved the in-house delivery option as the water services delivery

model and that this decision would be reflected in the 9-year plan 2025-34.

27 At the Council

meeting dated 12 August 2025 Council adopted the draft WSDP presented by staff

subject to minor edits. Staff submitted the WSDP to the Secretary for Local

Government on 25 August 2025.

28 Staff are

currently working through the contents of the December Bills to identify

further actions required.

Climate Mitigation and Adaptation

Report

29 As

requested by the ARS, Zero Carbon and South Dunedin Futures are developing a

regular update report on climate change mitigation and adaptation. This report

will cover the risks, controls, and planned improvement actions.

30 The aim

will be to have the first high level version of this report to ARS at the

December 2025 meeting and have this as a regular 6-monthly report.

OPTIONS

31 This is a

noting report so there are no options.

Signatories

|

Author:

|

Hayley Knight - Assurance Manager

|

|

Authoriser:

|

Carolyn Allan - Chief Financial Officer

|

Attachments

There are no attachments for

this report.

|

SUMMARY OF CONSIDERATIONS

|

|

Fit with purpose of Local Government

This report provides an update on various

audit and risk related matters.

|

|

Fit with strategic framework

|

|

Contributes

|

Detracts

|

Not applicable

|

|

Social Wellbeing Strategy

|

✔

|

☐

|

☐

|

|

Economic Development Strategy

|

✔

|

☐

|

☐

|

|

Environment Strategy

|

✔

|

☐

|

☐

|

|

Arts and Culture Strategy

|

✔

|

☐

|

☐

|

|

3 Waters Strategy

|

✔

|

☐

|

☐

|

|

Future Development Strategy

|

✔

|

☐

|

☐

|

|

Integrated Transport Strategy

|

✔

|

☐

|

☐

|

|

Parks and Recreation Strategy

|

✔

|

☐

|

☐

|

|

Other strategic projects/policies/plans

|

☐

|

☐

|

✔

|

This report provides an update on the progress made by

Council to deliver upon the activities identified by the Audit and Risk

Subcommittee, which is a regulatory function and considered good quality and

cost effective

|

|

Māori Impact Statement

There are no known impacts for mana whenua

|

|

Sustainability

There are no implications for sustainability

|

|

Zero carbon

There

are no implications for zero carbon

|

|

LTP/Annual Plan / Financial Strategy /Infrastructure

Strategy

There are no implications

|

|

Financial considerations

No financial implications have been identified

|

|

Significance

This report is rated low under the Council’s

Significance and Engagement Policy

|

|

Engagement – external

No external engagement has been undertaken

|

|

Engagement - internal

Activities noted herein include cross Council engagement

and collaboration

|

|

Risks: Legal / Health and Safety etc.

No risks have been identified

|

|

Conflict of Interest

There are no conflict of interest identified

|

|

Community Boards

There have been no implications for Community Boards

identified

|

|

|

Audit and Risk Subcommittee

1 September 2025

|

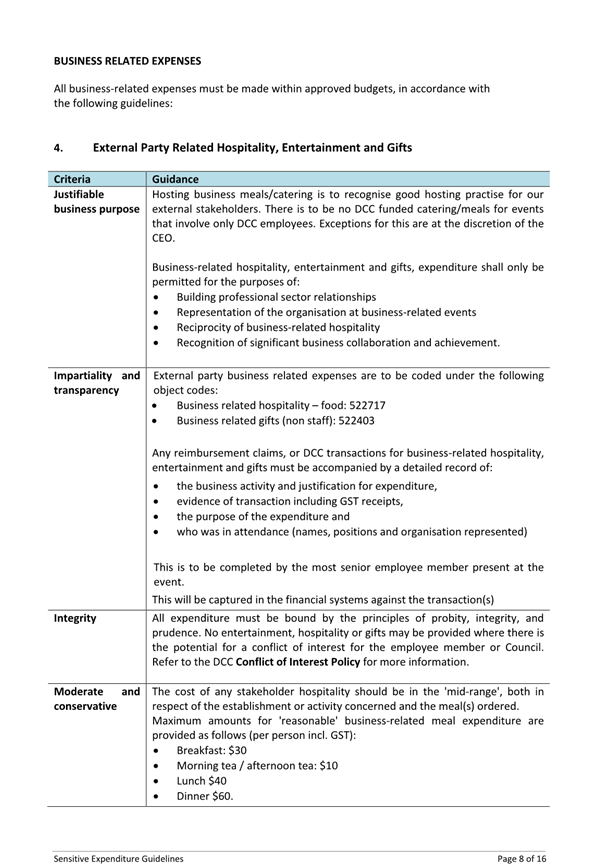

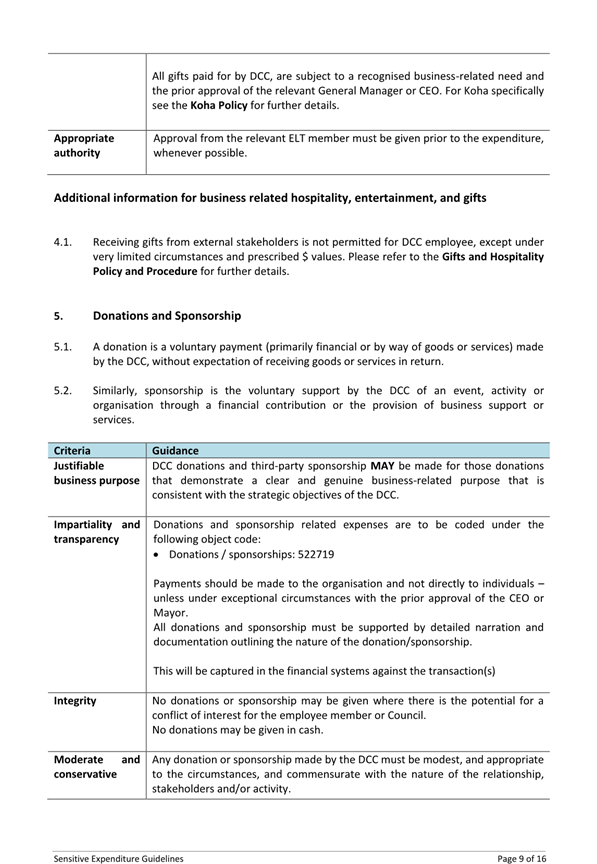

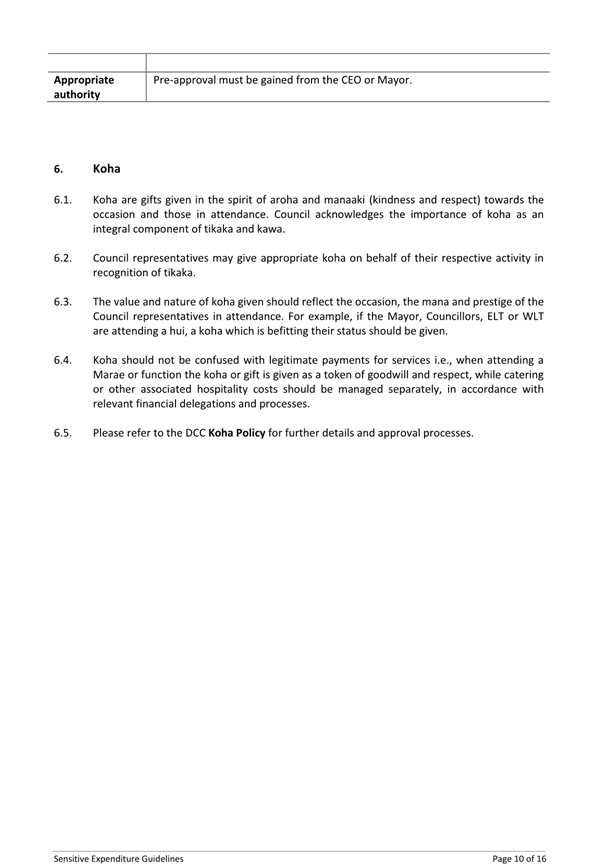

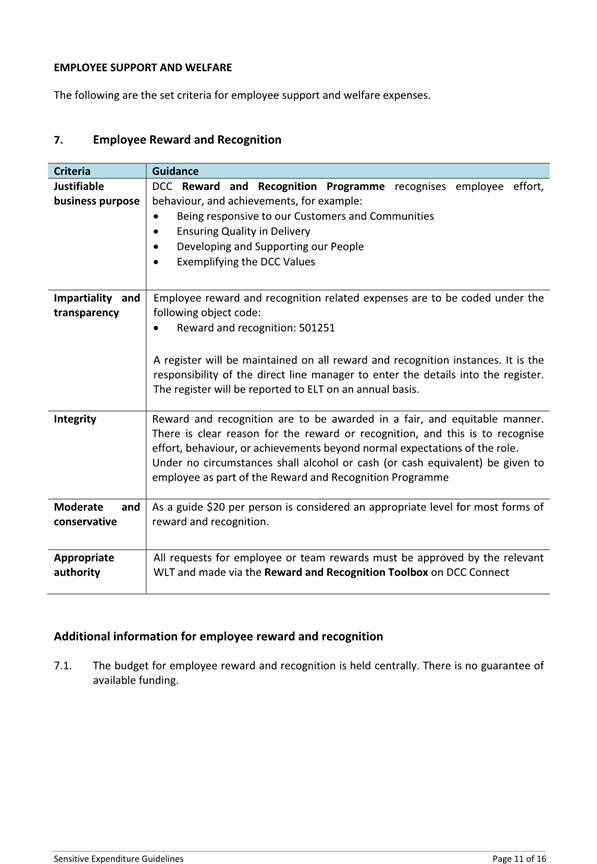

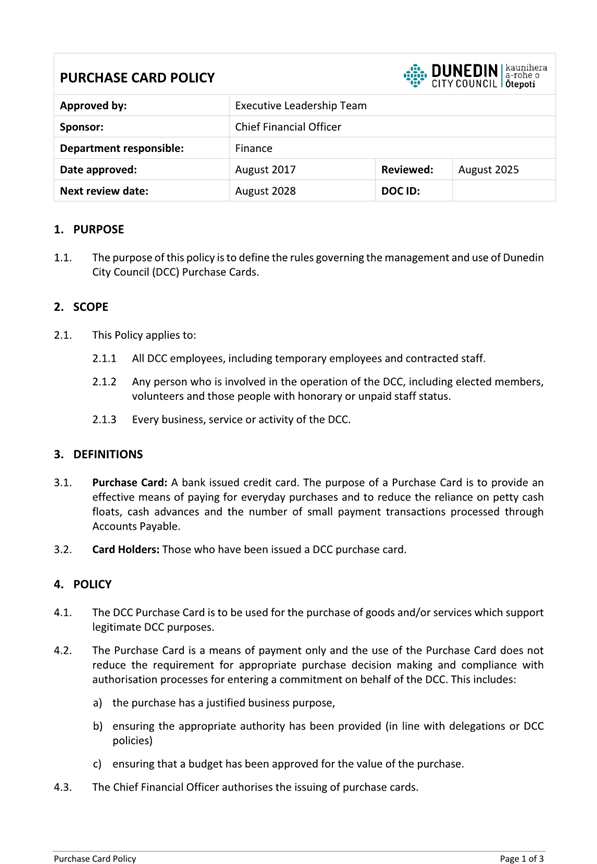

DCC Policy Update Report

Department: Finance

EXECUTIVE SUMMARY

1 This

report provides an update on DCC policies as identified in the Audit and Risk

Subcommittee (ARS) Workplan and ongoing audit and business improvement

activities.

RECOMMENDATIONS

That the Subcommittee:

a) Notes the Policy

Update Report – August 2025.

b) Provide feedback on

the Sensitive Expenditure Policy (Attachment A clean, Attachment B track

changes).

c) Notes the Sensitive

Expenditure Guidelines (Attachment C).

d) Provide feedback on

the Purchase Card Policy (Attachment D clean, Attachment E track changes).

e) Notes the Purchase

Card Procedures (Attachment F).

DISCUSSION

2 The

following policies are undergoing review:

a) Asset

Disposal and Write-Off Policy

b) ICT

Acceptable Use Policy

c) Information

Management Policy

d) Staff Code

of Conduct

e) Health,

Safety and Wellbeing Policy

3 After

the review process, updated copies of DCC policies will be provided to the

Subcommittee for either feedback or noting.

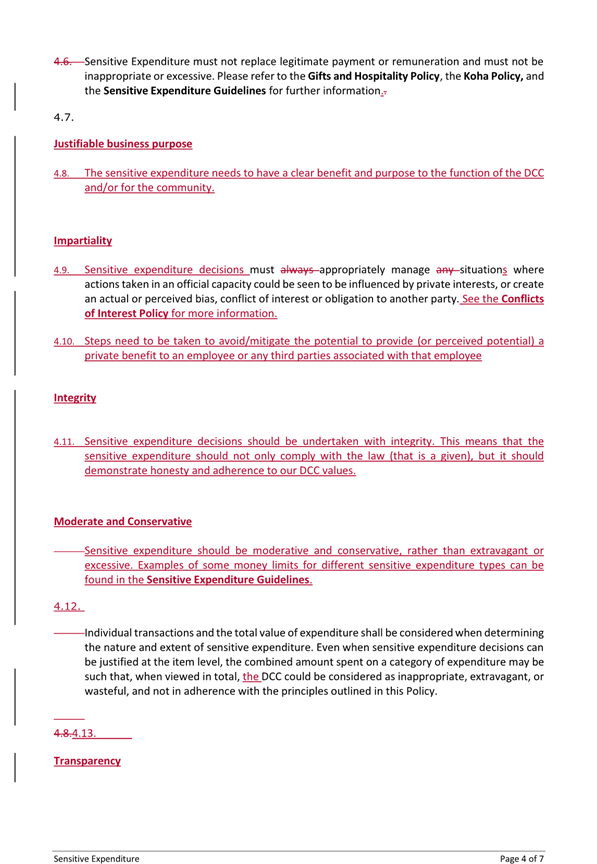

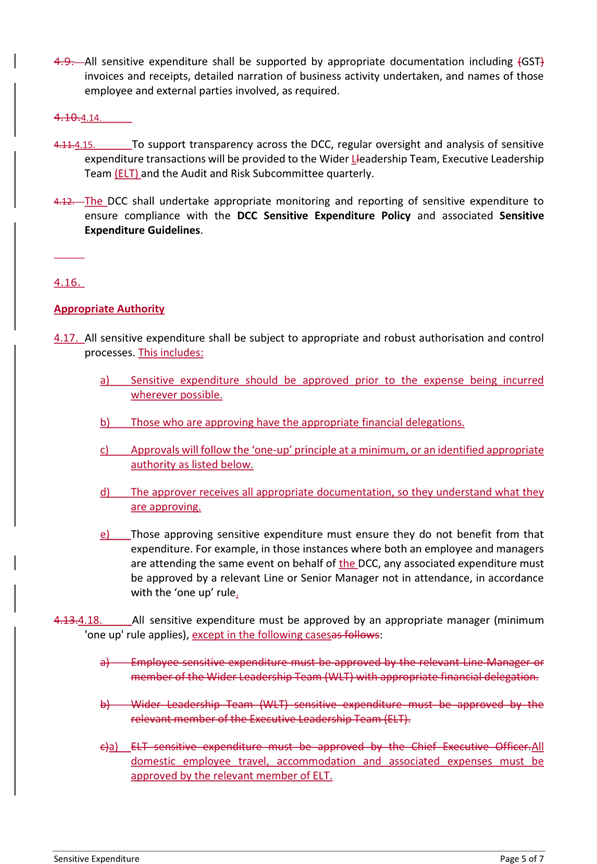

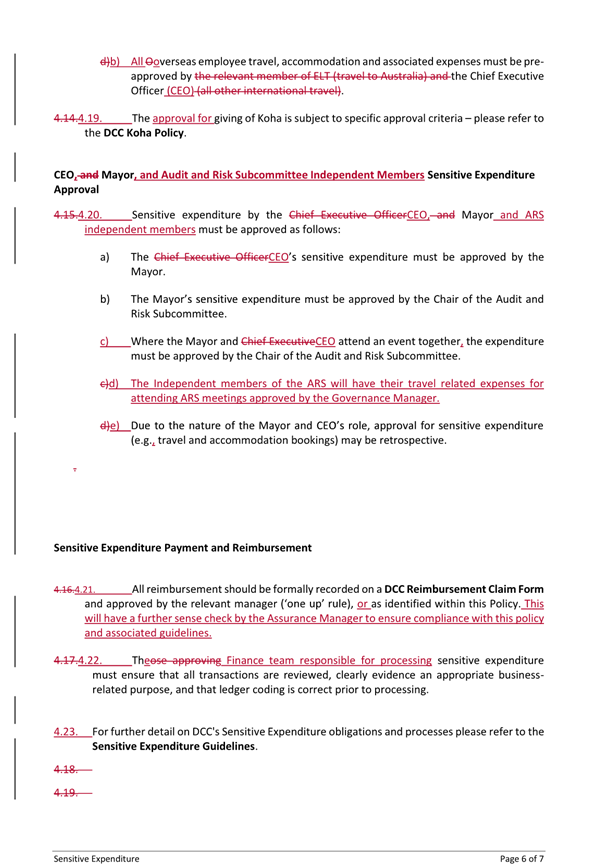

Sensitive Expenditure Policy

4 The

Office of the Auditor General (OAG) recommends that public sector have robust

policies and procedures for managing sensitive expenditure as a way of

promoting the public’s trust and confidence.

5 The

reviewed policy (Attachment A and B) has been provided for feedback, and the

guidelines (Attachment C) are presented to provide further context. Minor

changes have been made to the policy to provide further details in line with

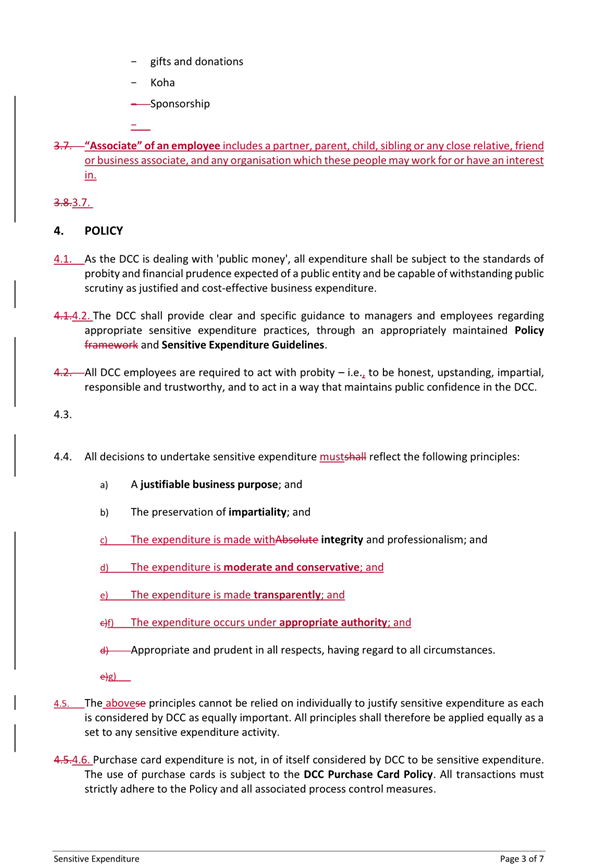

guidance from the OAG. These changes include:

a) Updated

the Responsible Officer to ‘Chief Financial Officer’

b) Changed the

scheduled review date period from 2 to 3 years – reviews can be conducted

at any stage as required to address substantial changes.

c) The

Policy has been updated to follow the new template.

d) Updating

the definition for employee to align with other policies.

e) Expanding

what is meant by each of the six-principles required for sensitive expenditure.

6 The

guidelines have used the six-principles approach to provide greater clarity on

what is appropriate sensitive expenditure at the DCC.

Purchase Card

Policy

7 A

review has been undertaken on the Purchase Card Policy (Attachment D and E) as

part of the regular scheduled review (review date scheduled for August 2023).

The review has been undertaken by the Assurance Manager, with representatives

from Finance and has incorporated recommendations from the recent Purchase

Cards Internal Audit completed by Crowe.

8 The

following updates have been made to the Purchase Card Policy:

a) Updated

the Responsible Officer to ‘Chief Financial Officer’

b) Changed the

scheduled review date period from 2 to 3 years – reviews can be conducted

at any stage as required to address substantial changes.

c) The

Policy has been updated to follow the new template.

d) Added

detail about Mayoral purchase card to follow current practice.

e) Added

details on the monthly limits which are applied to all DCC purchase cards.

f) Added

details on the requirement for a signed declaration for transactions without

receipts.

9 The

Purchase Card Procedures (Attachment F) have also been updated based upon Audit

recommendations - these are highlighted in the document.

NEXT STEPS

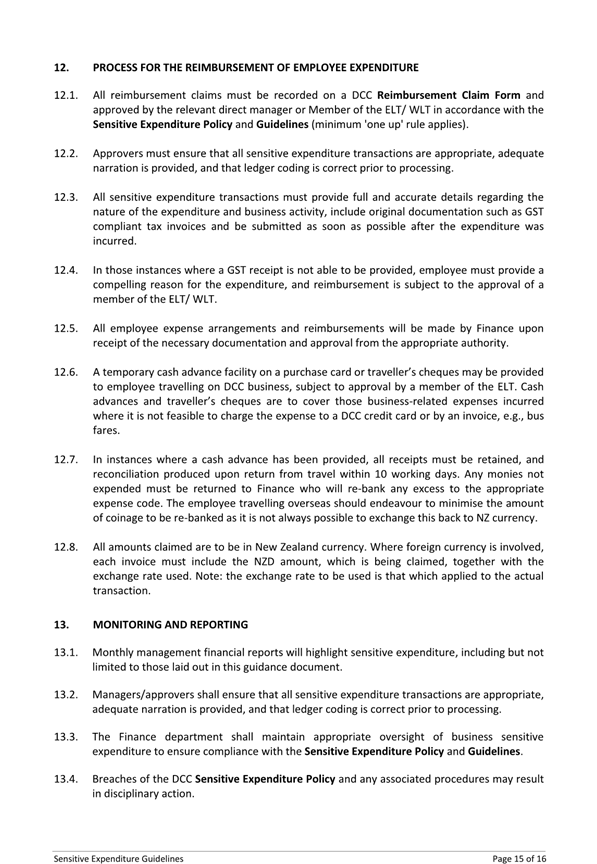

10 Feedback

provided by ARS on policies presented will be considered. If the changes are

major these will go back to the Executive Leadership Team for final review and

approval.

Signatories

|

Author:

|

Hayley Knight - Assurance Manager

|

|

Authoriser:

|

Carolyn Allan - Chief Financial Officer

|

Attachments

|

|

Title

|

Page

|

|

⇩a

|

Policy Sensitive

Expenditure August 2025 Clean

|

55

|

|

⇩b

|

Policy Sensitive

Expenditure August 2025 track changes

|

61

|

|

⇩c

|

Guidelines Sensitive

Expenditure August 2025

|

68

|

|

⇩d

|

Policy Purchase Card -

August 2025 clean

|

84

|

|

⇩e

|

Policy Purchase Card -

August 2025 track changes

|

87

|

|

⇩f

|

Purchase Card

Procedures August 2025

|

90

|

|

SUMMARY OF CONSIDERATIONS

|

|

Fit with purpose of Local Government

This report provides an update on Council

Policy documents as identified by the Audit and Risk Subcommittee Workplan,

which is a regulatory function considered good quality and cost effective.

|

|

Fit with strategic framework

|

|

Contributes

|

Detracts

|

Not applicable

|

|

Social Wellbeing Strategy

|

✔

|

☐

|

☐

|

|

Economic Development Strategy

|

✔

|

☐

|

☐

|

|

Environment Strategy

|

✔

|

☐

|

☐

|

|

Arts and Culture Strategy

|

✔

|

☐

|

☐

|

|

3 Waters Strategy

|

✔

|

☐

|

☐

|

|

Spatial Plan

|

✔

|

☐

|

☐

|

|

Integrated Transport Strategy

|

✔

|

☐

|

☐

|

|

Parks and Recreation Strategy

|

✔

|

☐

|

☐

|

|

Other strategic projects/policies/plans

|

☐

|

☐

|

✔

|

The Audit and Risk Subcommittee monitors and provides

assurance for the effective review and management of core Council Policies

– thereby supporting business controls and delivery, governance and the

realisation of strategic objectives.

|

|

Māori Impact Statement

There are no know impacts for mana whenua.

|

|

Sustainability

There are no implications for sustainability.

|

|

LTP/Annual Plan / Financial Strategy /Infrastructure

Strategy

There are no known implications.

|

|

Financial considerations

No financial implications have been identified.

|

|

Significance

This report is considered low in terms of the

Council’s Significance and Engagement Policy.

|

|

Engagement – external

The Serious Fraud Office was consulted on for the review

of the Fraud, Bribery and Corruption Prevention Policy.

Other local authorities were contacted to understand their

threshold for declaring gifts and hospitality offered as a part of the Gifts

and Hospitality Policy review process.

|

|

Engagement - internal

Activities noted herein include cross Council engagement

and collaboration on Policy review and development.

|

|

Risks: Legal / Health and Safety etc.

A failure to maintain effective and appropriate Policy

framework across core Council functions exposes the DCC to a range of operational

and strategic risks, including financial, business and service performance,

community, business and sector confidence, as well as potential fraud and

litigation.

|

|

Conflict of Interest

No conflicts of interest have been identified.

|

|

Community Boards

There are no known implications for the Community Boards.

|

|

|

Audit and Risk Subcommittee

1 September 2025

|

|

|

Audit and Risk Subcommittee

1 September 2025

|

|

|

Audit and Risk Subcommittee

1 September 2025

|

|

|

Audit and Risk Subcommittee

1 September 2025

|

|

|

Audit and Risk Subcommittee

1 September 2025

|

|

|

Audit and Risk Subcommittee

1 September 2025

|

|

|

Audit and Risk Subcommittee

1 September 2025

|

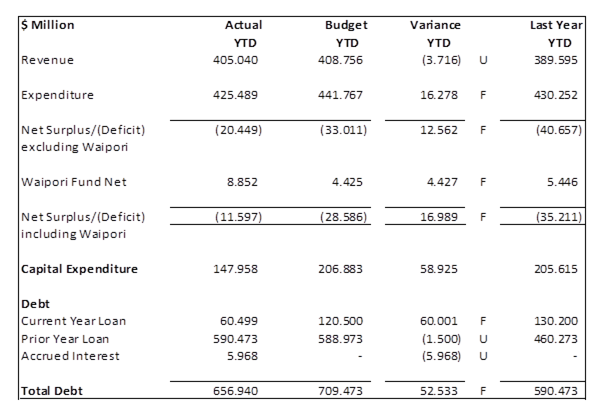

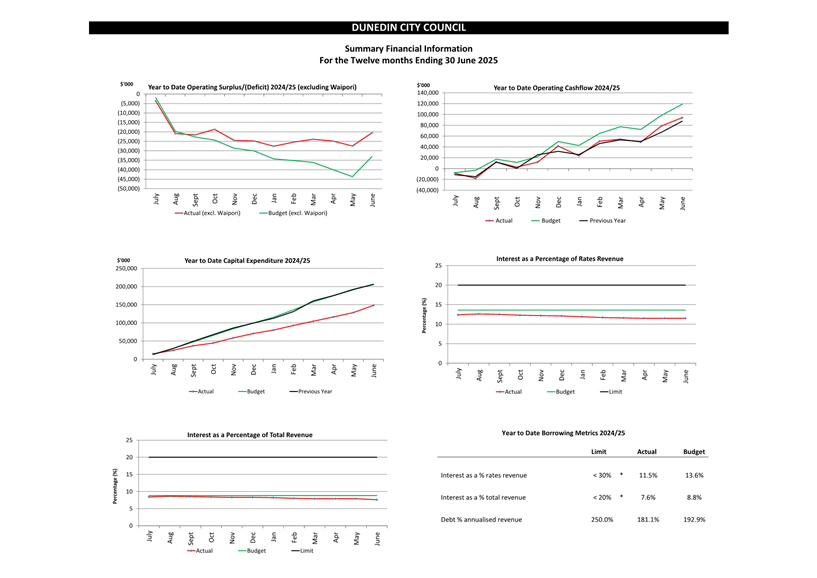

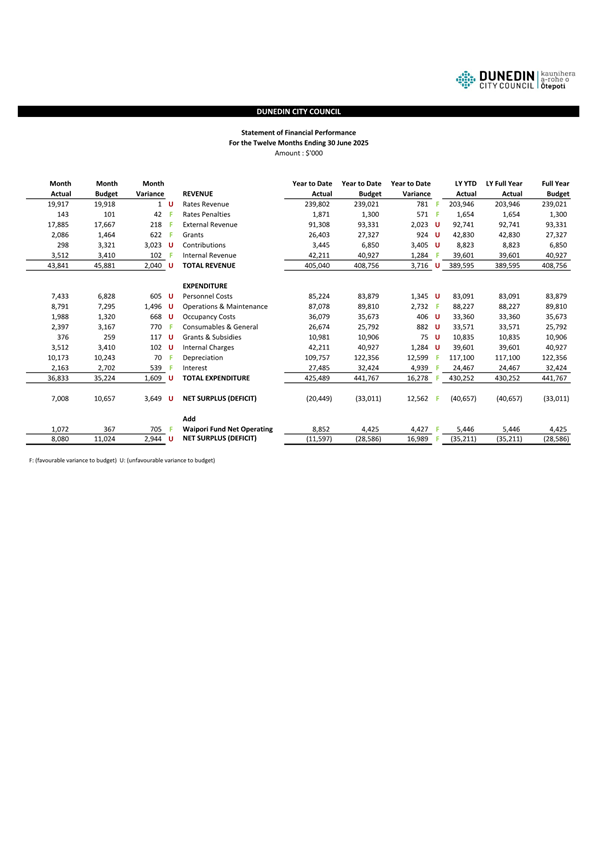

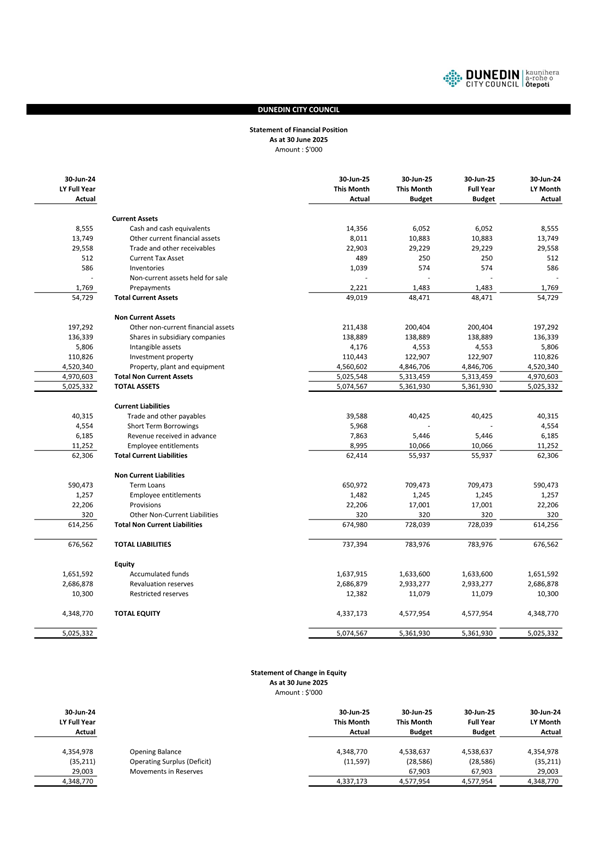

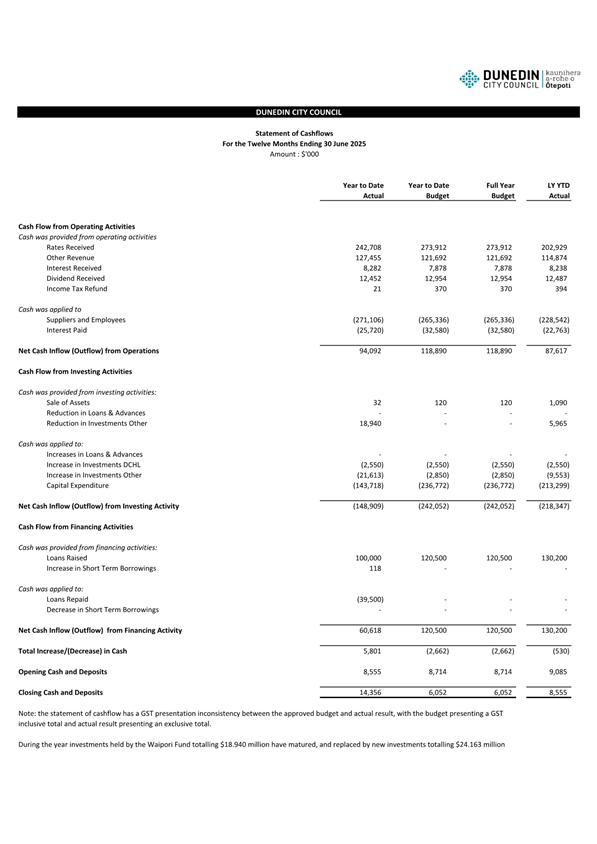

Financial Report - Period ended 30 June 2025

Department: Finance

EXECUTIVE SUMMARY

1 This

report provides the provisional financial results for the period ended 30 June

2025 and the financial position as at that date, noting the results presented

are subject to final adjustments and external audit. The report was

presented to the Council meeting held on Tuesday, 26 August 2025.

2 As

this is an administrative report only, there are no options or Summary of

Considerations.

Financial Overview

For the period ended 30 June 2025

RECOMMENDATIONS

That the Subcommittee:

a) Notes the Financial

Performance for the period ended 30 June 2025 and the Financial Position as at

that date.

b) Notes the 30 June 2025

result is subject to final adjustments and external audit, by Audit New Zealand.

BACKGROUND

3 This

report provides the financial statements for the period ended 30 June 2025. It includes reports on financial performance, financial

position, cashflows and capital expenditure. Summary information is

provided in the body of this report with detailed results attached. The

operating result is also shown by group, including analysis by revenue and

expenditure type.

DISCUSSION

4 This report includes a high-level summary of the financial

information to 30 June 2025. Please refer to Attachment I for the

detailed financial update, including a summary of Better Off Funding

expenditure for the quarter to 30 June 2025.

Statement of Financial Performance

5 Revenue

was $405.040 million for the period or $3.716 million less than budget.

6 Operating

revenue (external and internal combined) was unfavourable $739k, mainly due to

lower-than-expected revenue from the Parking Services, Transport, Aquatic

Services, Resource Consents and Building Services activities.

7 Grants

revenue was unfavourable $924 reflecting funding decisions by NZTA under the

National Land Transport Programme, and a reduction in the contractor

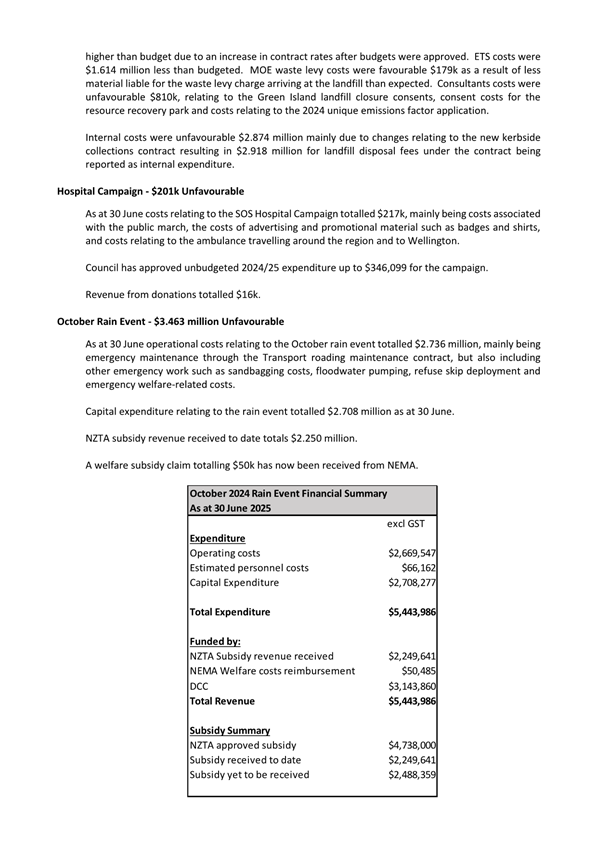

work programme in specific areas to offset cost over runs in some activities. NZTA subsidy revenue totalling $2.250 million relating to the

October rain event has been received, with a further $2.488 million approved

which will be claimed as costs are incurred.

8 Expenditure

was $425.489 million for the period, or $16.278 million less than budget.

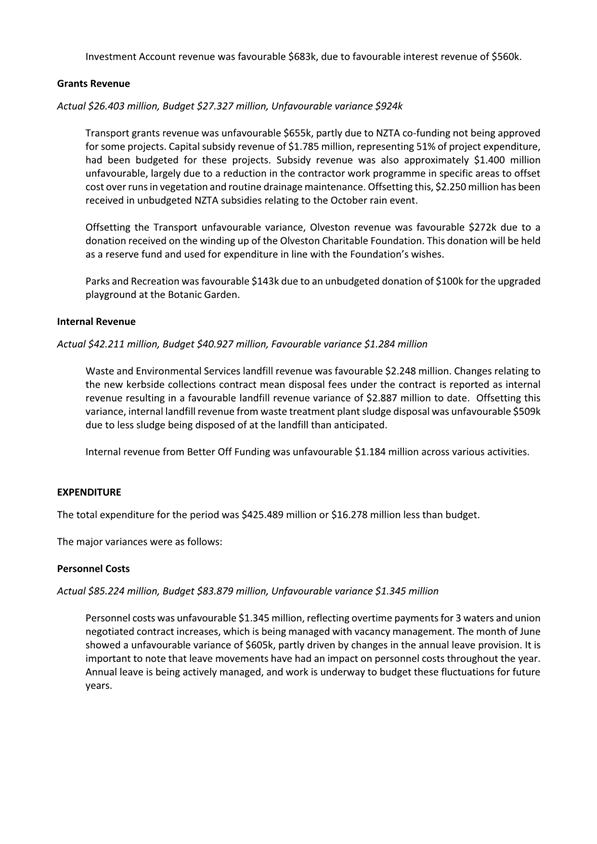

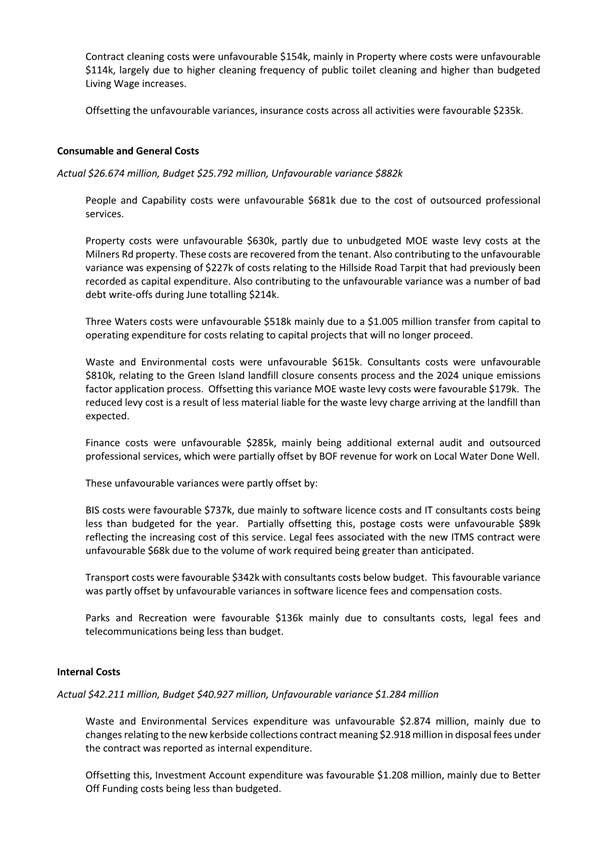

9 Personnel costs was unfavourable $1.345 million, reflecting overtime

payments for 3 waters and union negotiated contract increases, which is being

managed with vacancy management. The month of June showed an unfavourable

variance of $605k, mainly due to accrued leave adjustments.

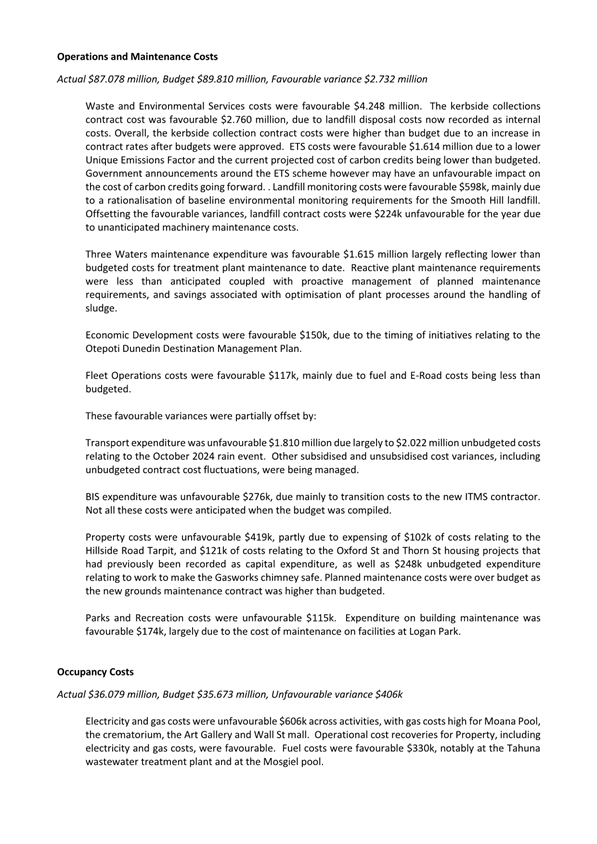

10 Operations

and maintenance expenditure was favourable $2.732 million; however, this

favourable variance was offset by an unfavourable $1.283 million variance in

internal costs, largely due largely to landfill disposal costs for kerbside

collections now recorded as internal costs. Unfavourable Transport maintenance

costs are more than offset by under expenditure in other activities, including

Three Waters and Waste and Environmental Services. Transport costs included

emergency works totalling $2.027 million associated with the October 2024 rain

event.

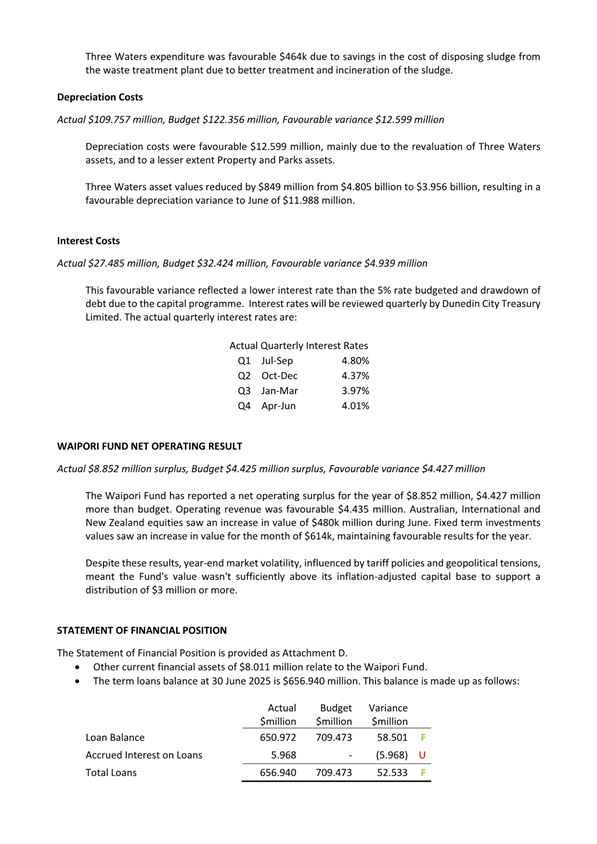

11 Depreciation

costs were favourable $12.599 million, mainly due to the revaluation of Three

Waters assets, and to a lesser extent Property and Parks assets.

12 Interest

costs were favourable $4.939 million, reflecting a lower interest rate than

budgeted and lower debt.

13 The

Waipori Fund has reported a net operating surplus for the year of $8.852

million, $4.427 million more than budget. Operating revenue was favourable

$4.435 million. Australian, International and New Zealand equities saw an

increase in value of $480k million during June. Fixed term investments values

saw an increase in value for the month of $614k, maintaining favourable results

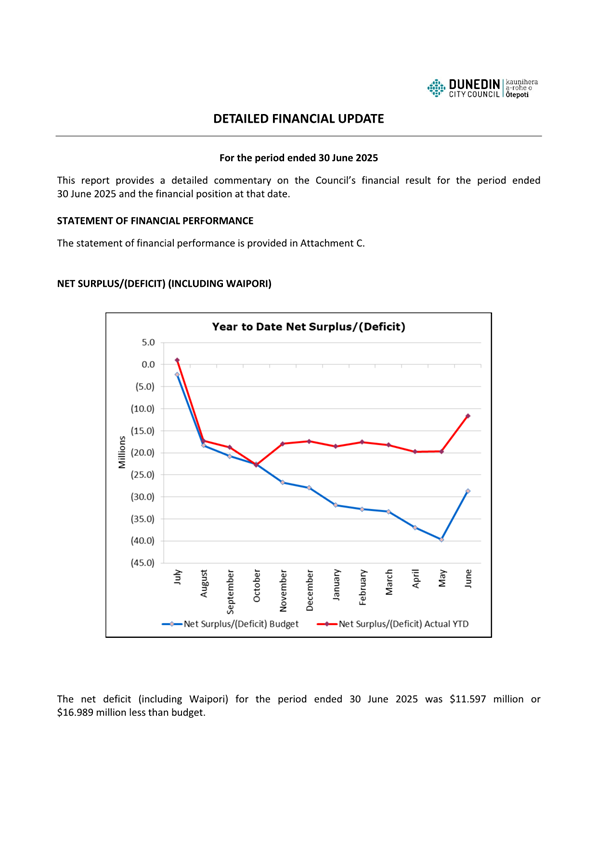

for the year. Despite these results, year-end market

volatility, influenced by tariff policies and geopolitical tensions, meant the

Fund's value wasn't sufficiently above its inflation-adjusted capital base to

support a distribution of $3 million or more.

Statement of Financial Position

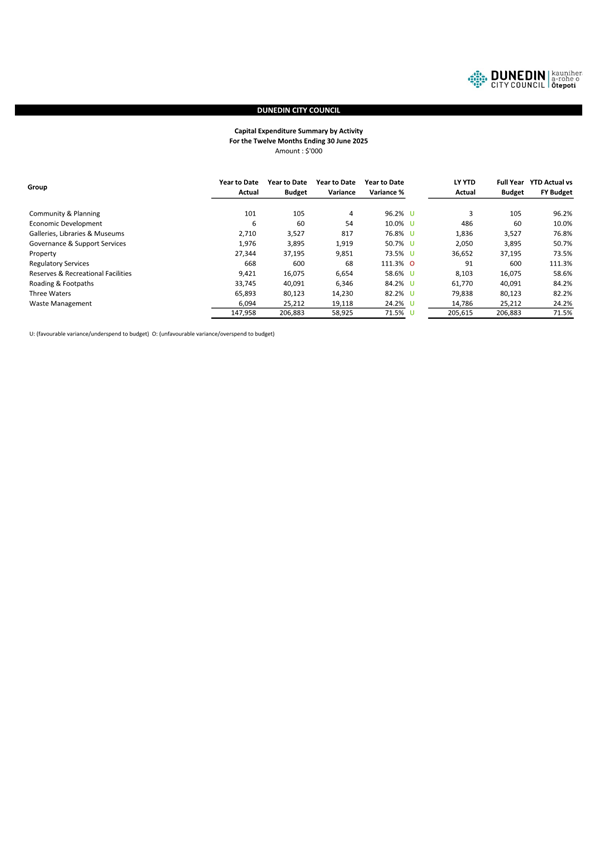

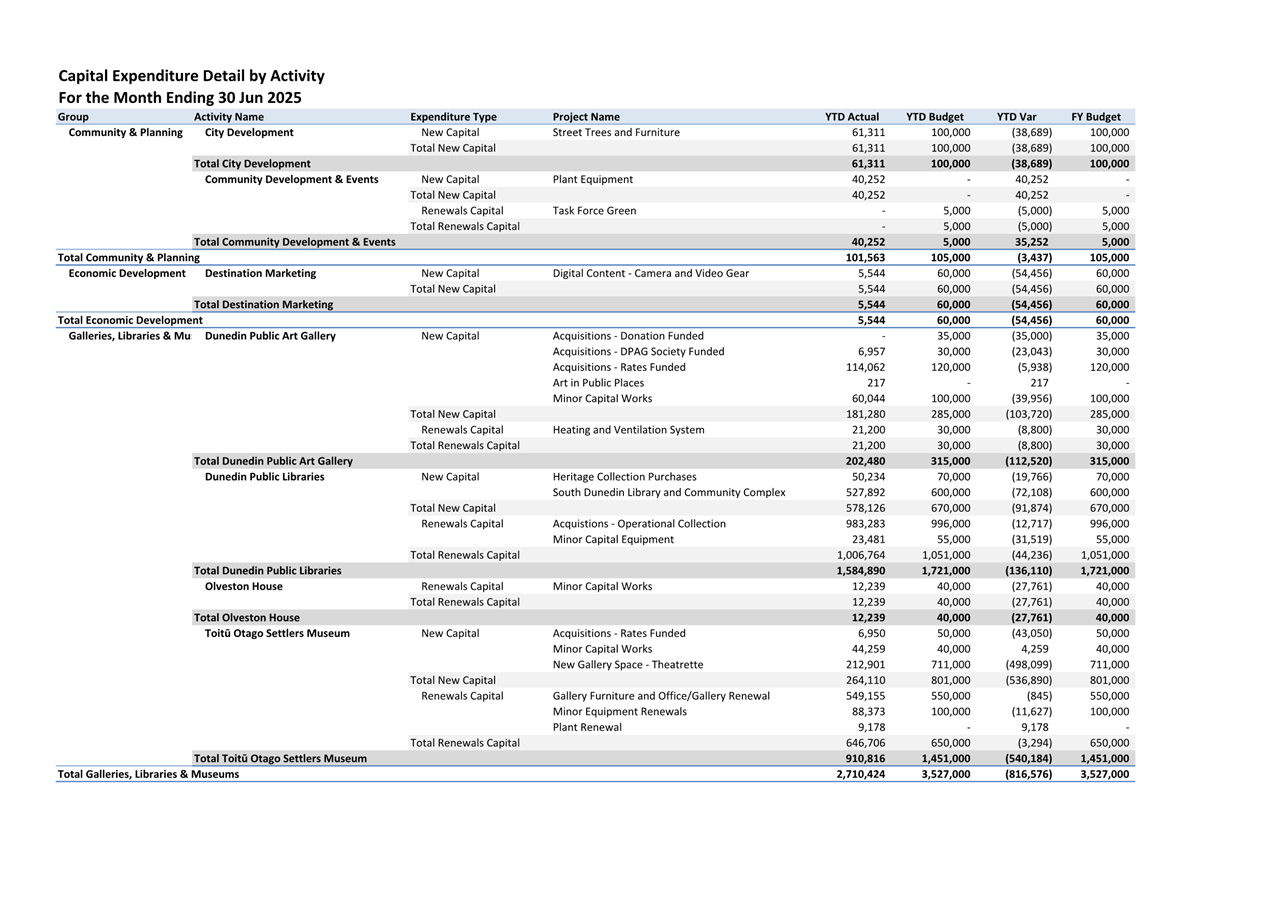

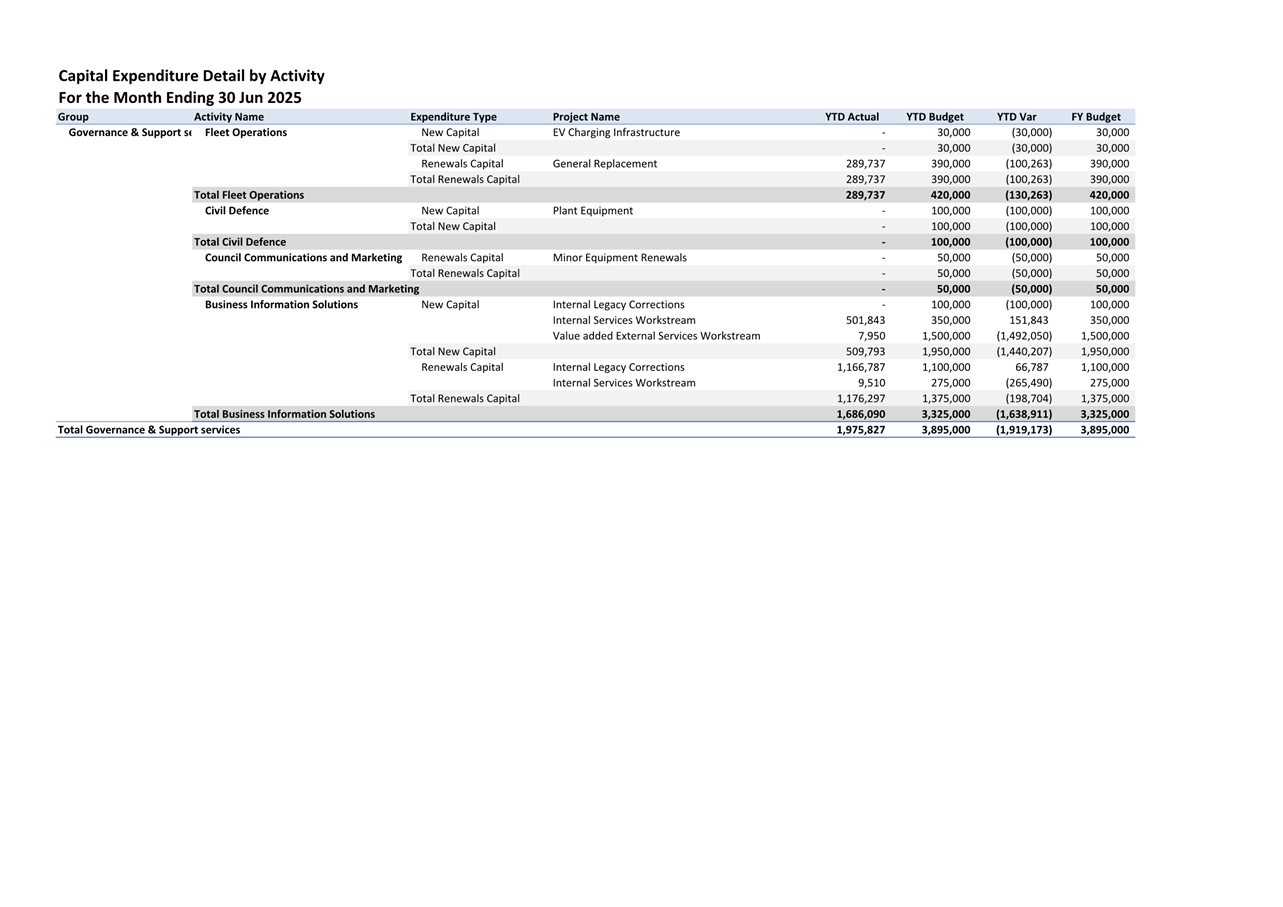

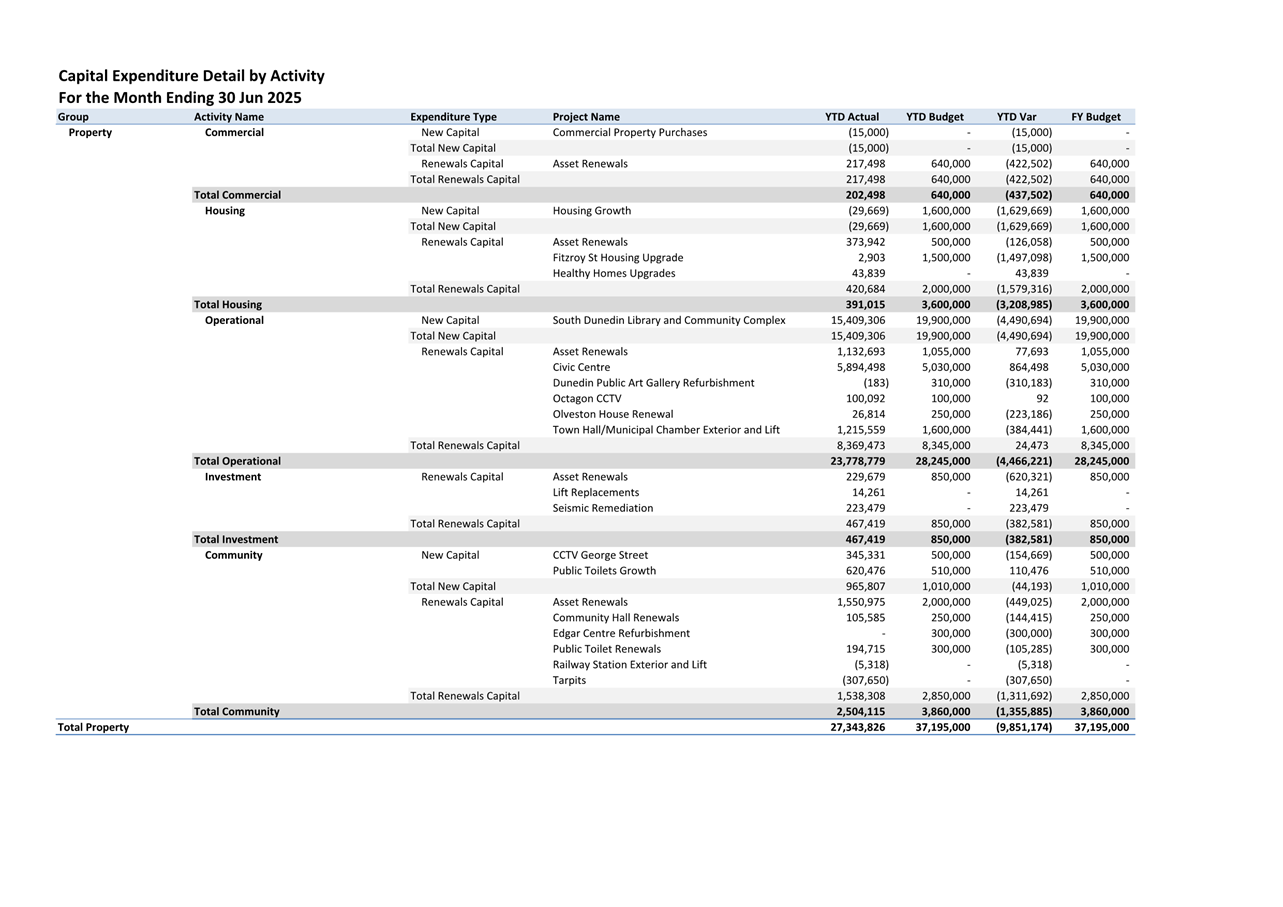

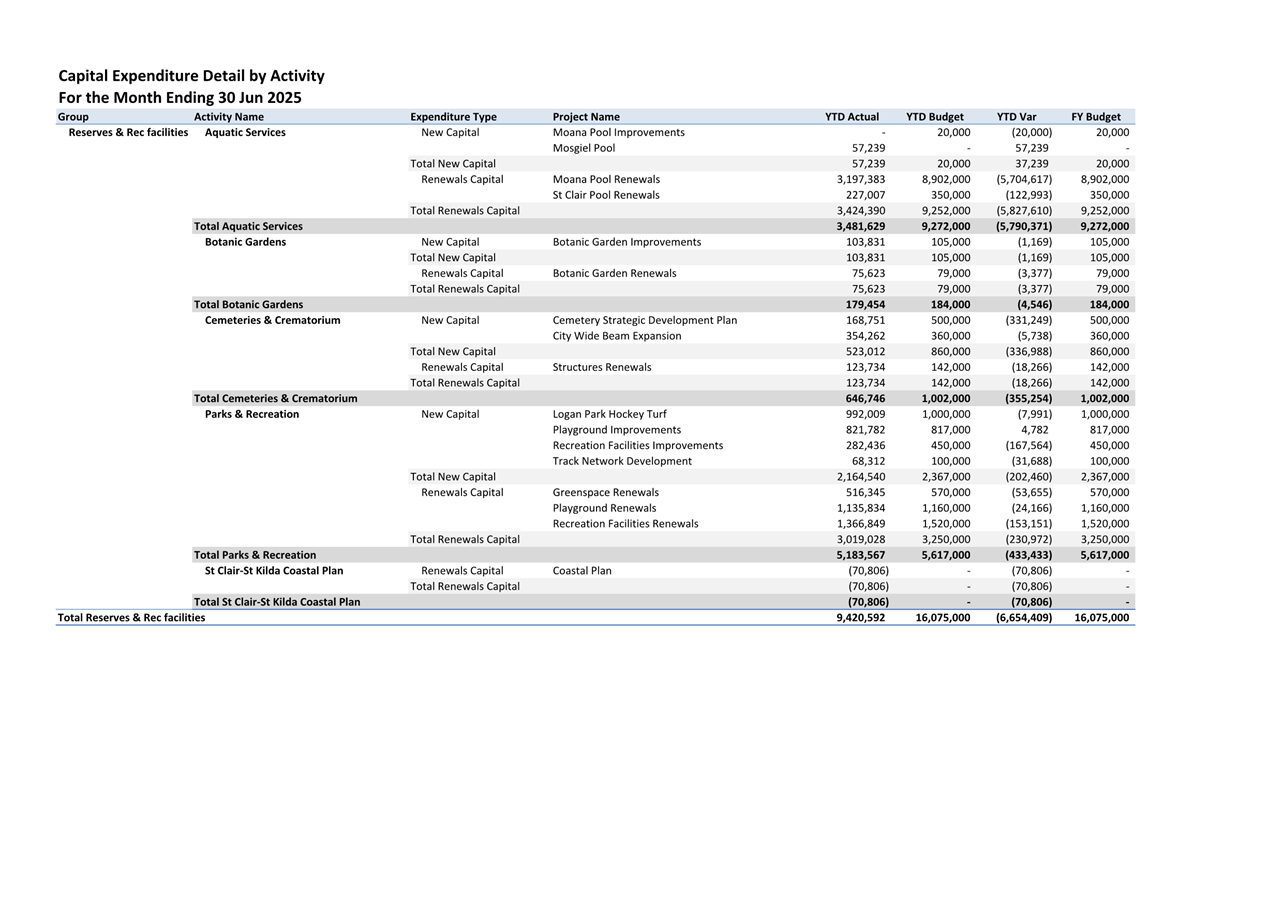

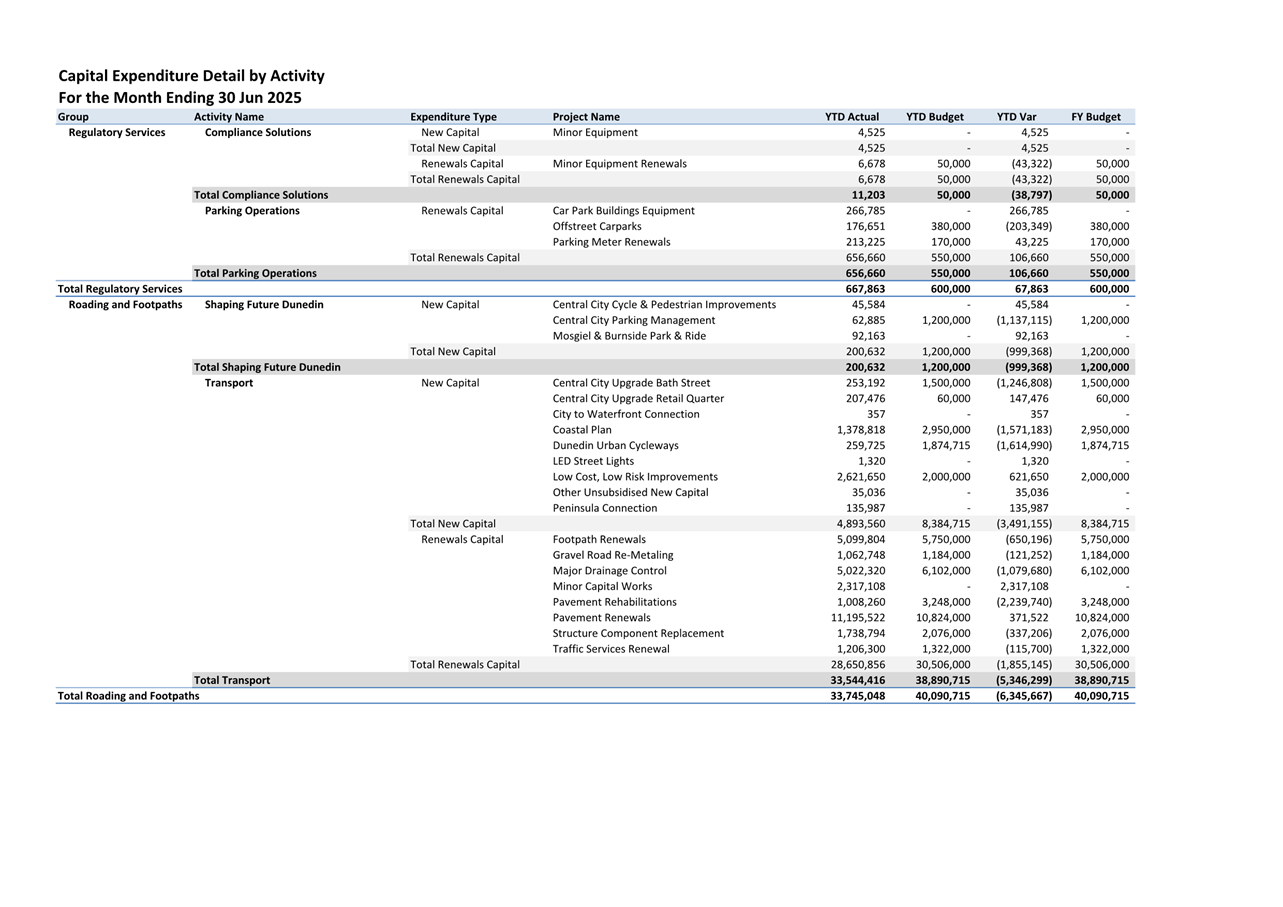

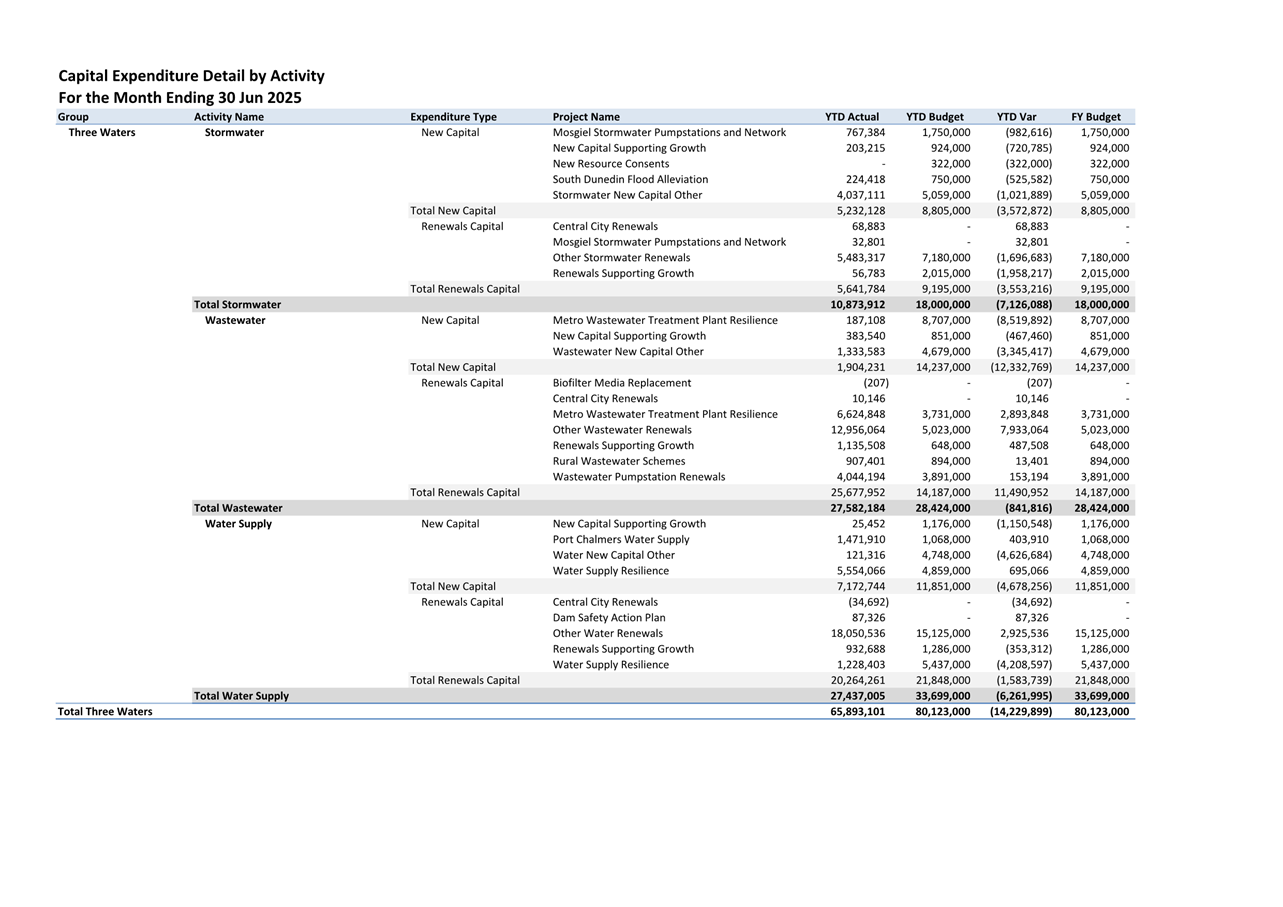

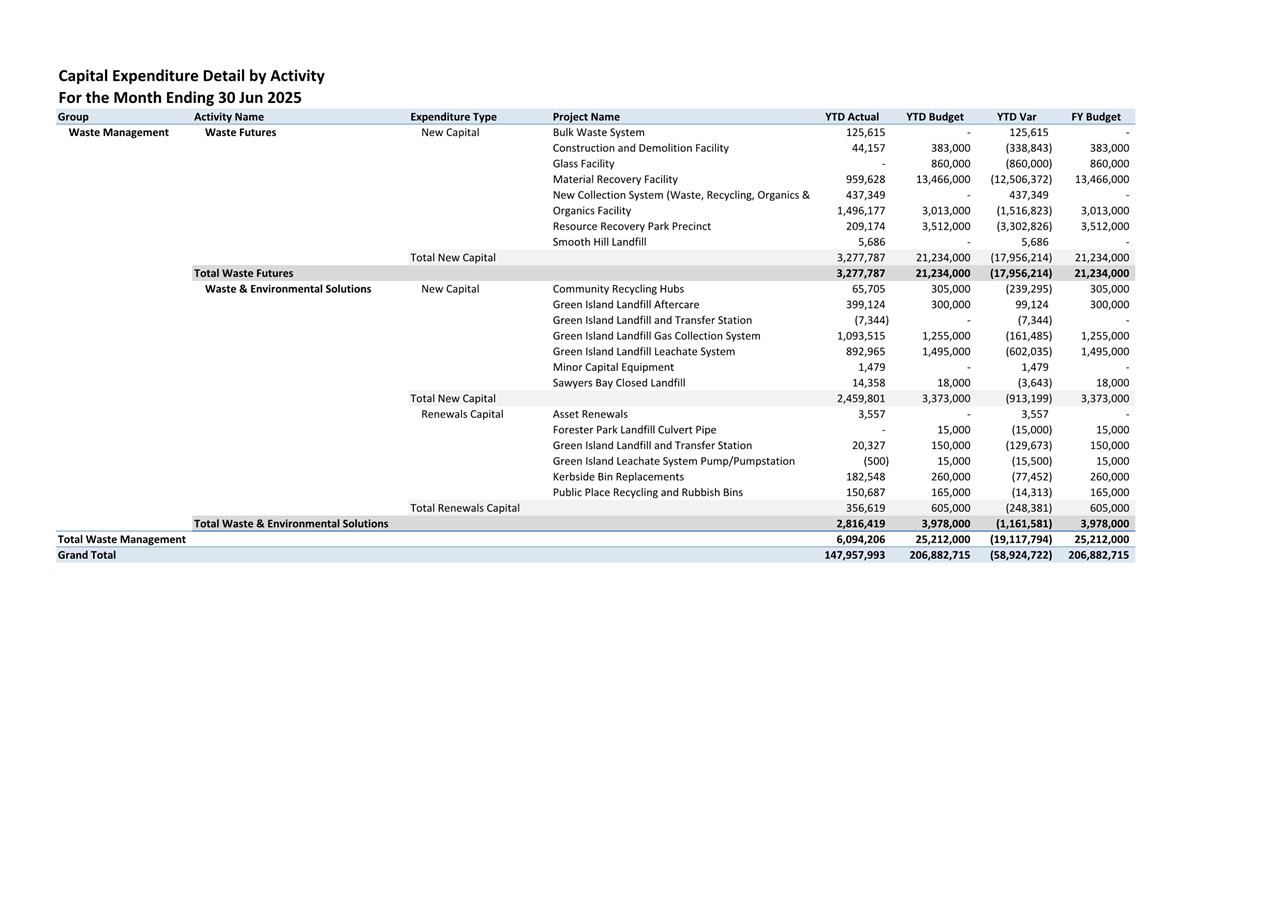

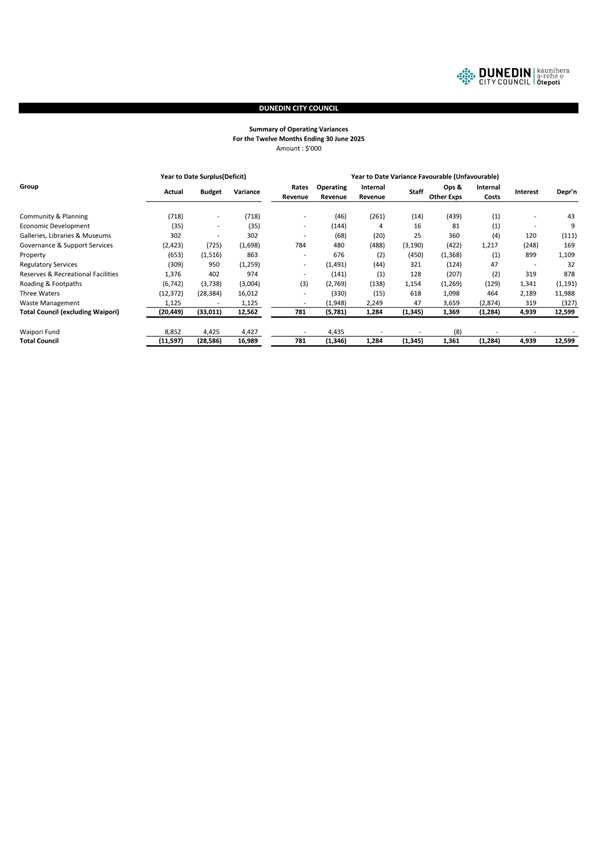

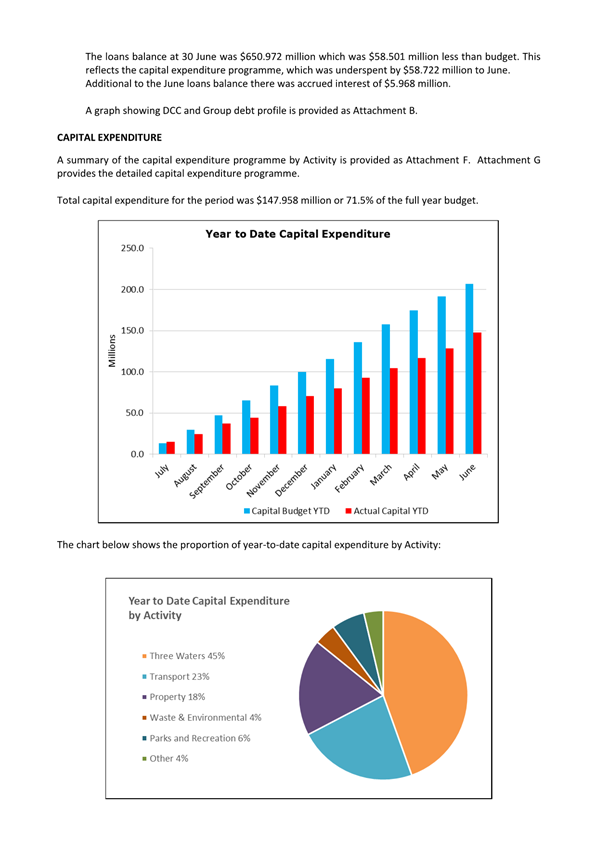

14 Capital

expenditure was $147.958 million or 71.5% of the full year budget. Capital

expenditure in most activities was generally within budget for the period.

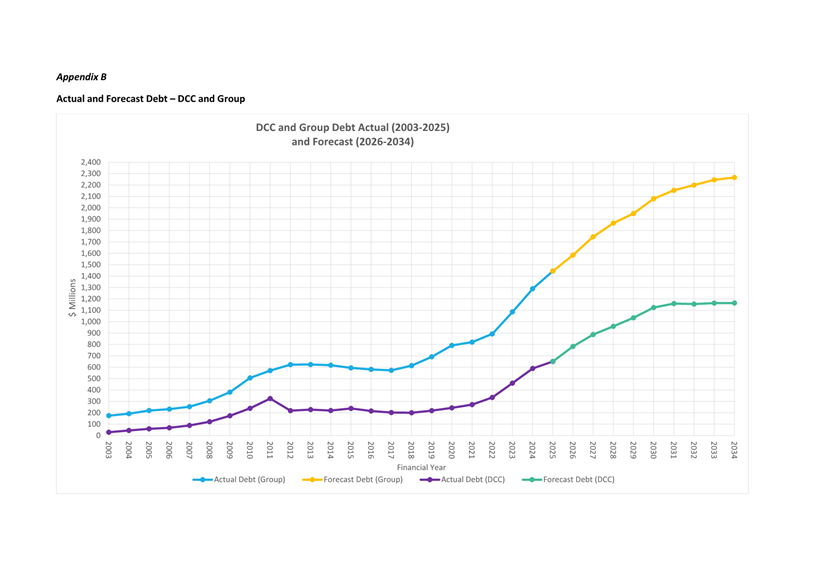

15 The loans

balance at 30 June was $650.972 million which was $58.501 million less than

budget. This a reflection of the capital expenditure programme, which was

underspent by $58.925 million to June. Additional to the June loans

balance there was accrued interest of $5.968 million.

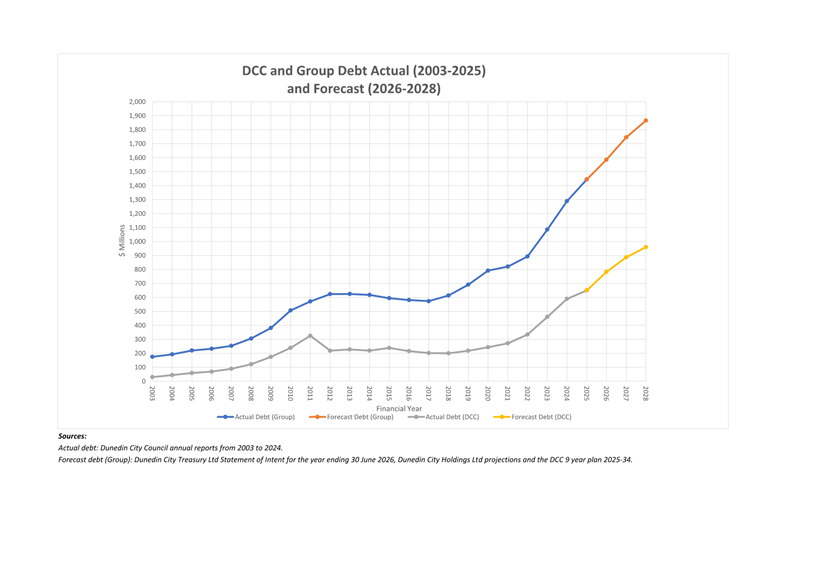

16 Attachment

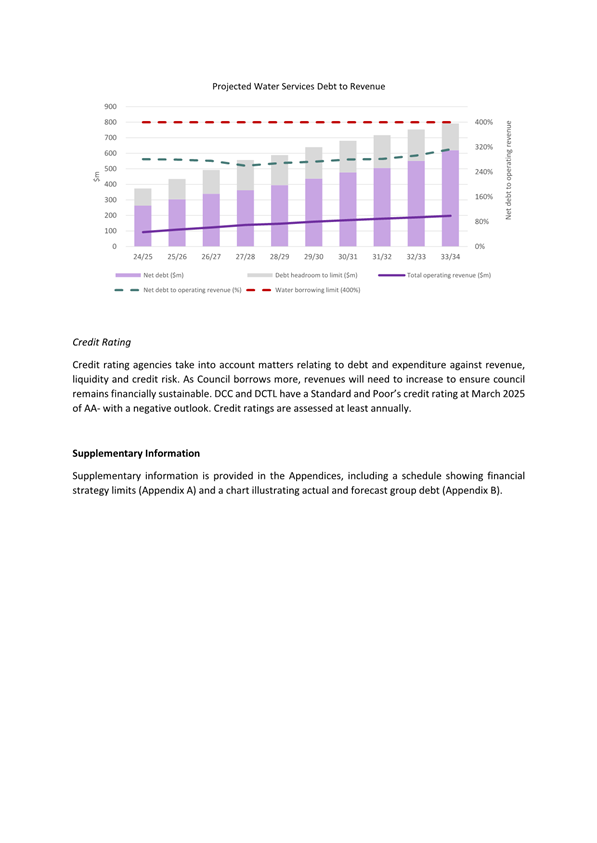

B includes a chart showing actual group and DCC debt for the years ending June 2004-2025.

It provides forecast information for the years ending June 2026 -2028

based on the current Statements of Intent (SOI), and the first two years of the

draft 9-year plan.

Final Adjustments and External Audit

17 Final

adjustments in addition to this report include:

· Completion of vested assets

· Revaluation of assets (Three Waters, Transport, Investment Property)

· Landfill aftercare provisions

· Depreciation

18 Audit

New Zealand is scheduled to start their audit in early September 2025, with an

expected signoff date of 31 October 2025.

OPTIONS

19 As this is

an administrative report only, there are no options provided.

NEXT STEPS

20 Financial

Result Reports continue be presented to future meetings of Council.

Signatories

|

Author:

|

Lawrie Warwood - Financial Analyst

|

|

Authoriser:

|

Carolyn Allan - Chief Financial Officer

|

Attachments

|

|

Title

|

Page

|

|

⇩a

|

Dashboard Summary

Financial Information

|

106

|

|

⇩b

|

Debt Graph

|

107

|

|

⇩c

|

Statement of Financial

Performance

|

108

|

|

⇩d

|

Statement of Financial

Position

|

109

|

|

⇩e

|

Statement of Cashflows

|

110

|

|

⇩f

|

Capital Expenditure

Summary

|

111

|

|

⇩g

|

Capital Expenditure

Detailed Programme

|

112

|

|

⇩h

|

Operating Variances

|

121

|

|

⇩i

|

Detailed Financial

Update

|

122

|

|

|

Audit and Risk Subcommittee

1 September 2025

|

|

|

Audit and Risk Subcommittee

1 September 2025

|

|

|

Audit and Risk Subcommittee

1 September 2025

|

|

|

Audit and Risk Subcommittee

1 September 2025

|

|

|

Audit and Risk Subcommittee

1 September 2025

|

|

|

Audit and Risk Subcommittee

1 September 2025

|

|

|

Audit and Risk Subcommittee

1 September 2025

|

|

|

Audit and Risk Subcommittee

1 September 2025

|

|

|

Audit and Risk Subcommittee

1 September 2025

|

|

|

Audit and Risk Subcommittee

1 September 2025

|

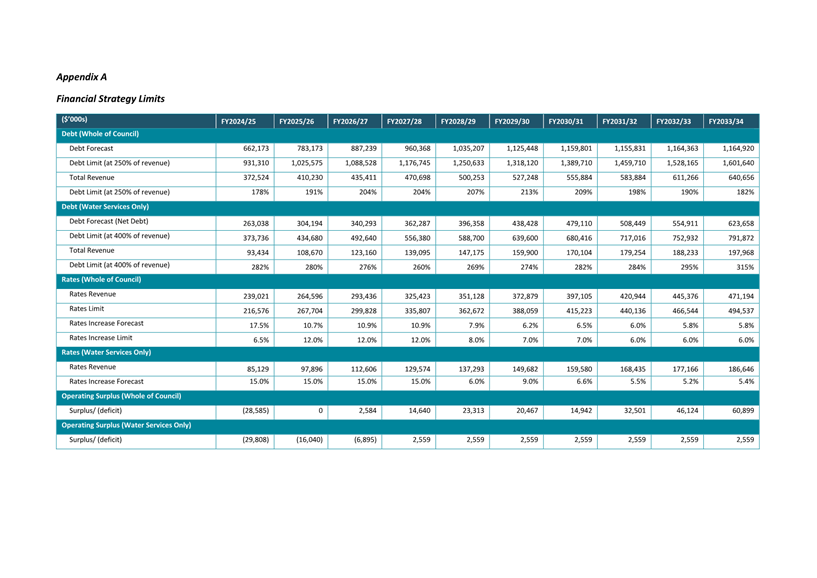

Financial Strategy Compliance

Department: Finance

EXECUTIVE SUMMARY

1 The

attached report provides a summary of rate and debt limits, including group

debt limits. The purpose of the report is to monitor compliance against

these limits.

2 As

this is an administrative report only, the Summary of Considerations is not

required.

RECOMMENDATIONS

That the Committee:

a) Notes the Financial

Strategy Compliance Report.

BACKGROUND

3 A

request was made by members of the Audit and Risk Subcommittee to provide a

report showing compliance with Financial Strategy limits and group debt limits.

The report provided in Attachment A summarises rates and debt limits as well as

forecast rates and debt levels for the period of the 9 year plan.

NEXT STEPS

4 Financial

Strategy Compliance Reports will be provided quarterly to the Audit and Risk

Subcommittee.

Signatories

|

Author:

|

Tony Nelmes - Project Accountant

|

|

Authoriser:

|

Carolyn Allan - Chief Financial Officer

|

Attachments

|

|

Title

|

Page

|

|

⇩a

|

Financial Strategy

Compliance

|

137

|

|

|

Audit and Risk Subcommittee

1 September 2025

|

|

|

Audit and Risk Subcommittee

1 September 2025

|

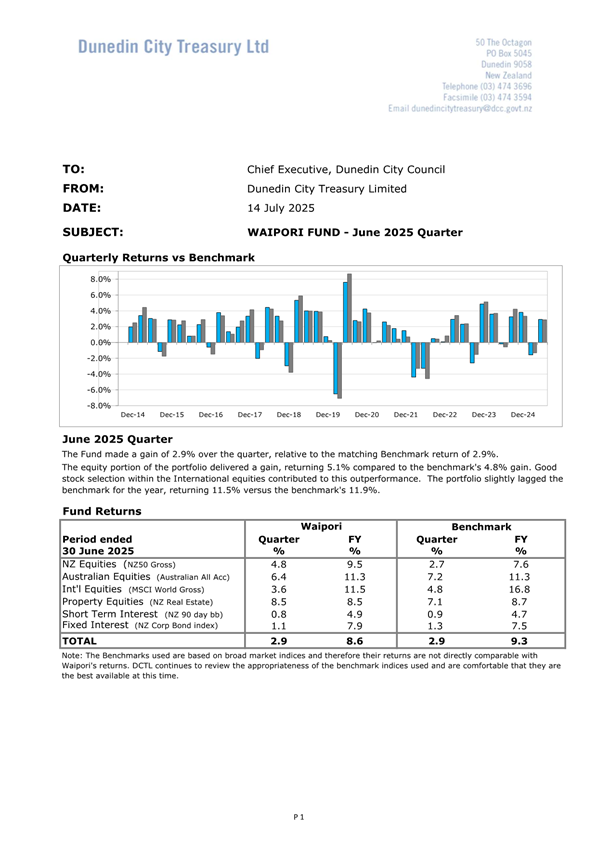

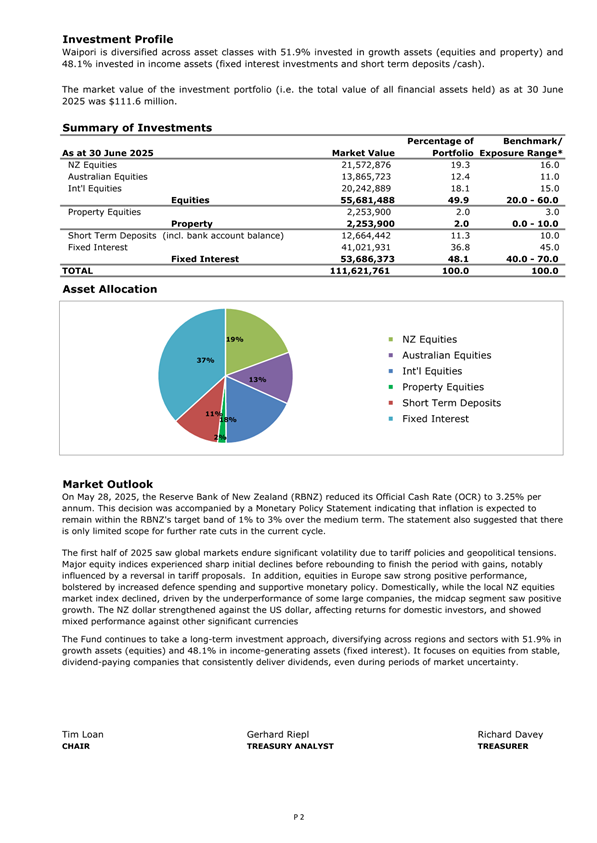

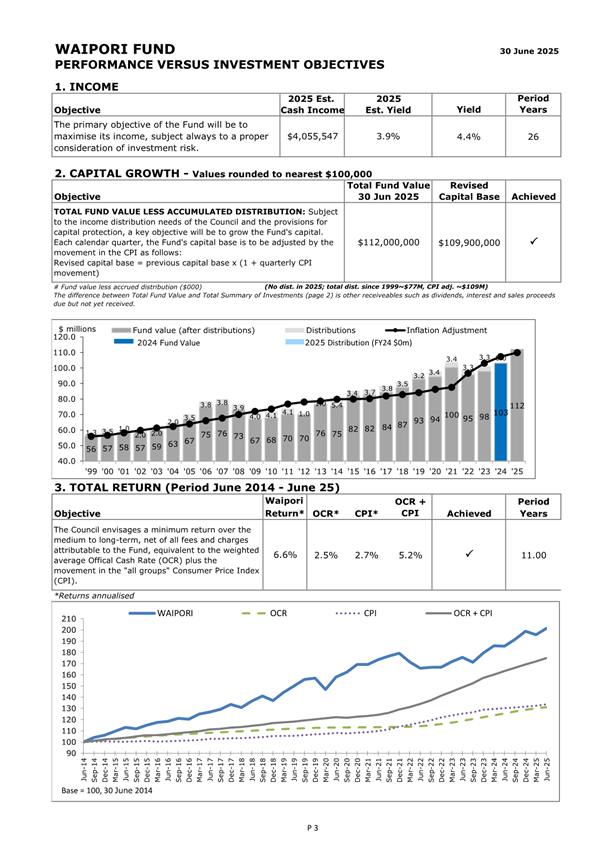

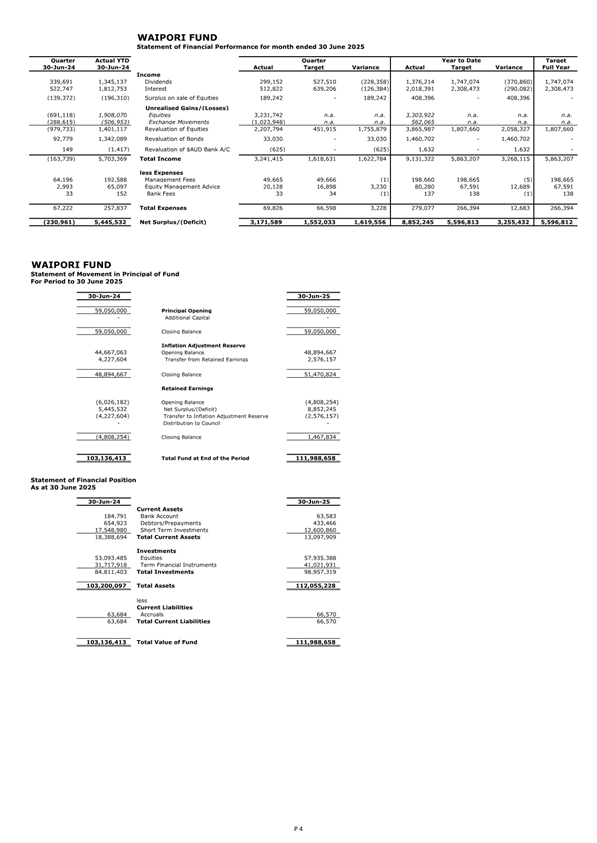

Waipori Fund - Quarter ending 30 June 2025

Department: Finance

EXECUTIVE SUMMARY

1 The

attached report from Dunedin City Treasury Limited provides information on the

results of the Waipori Fund for the quarter ended 30 June 2025. This

report was presented to the Council meeting held on 26 August 2025.

RECOMMENDATIONS

That the Subcommittee:

a) Notes the report from

Dunedin City Treasury Limited on the Waipori Fund for the quarter ended 30 June

2025.

DISCUSSION

2 The

Waipori Fund Statement of Investment Policy and Objectives (SIPO) requires

quarterly reporting on the performance and financial position of the fund.

3 Dunedin

City Treasury Limited has provided the Waipori Fund report for the June 2025

quarter. The report is provided as Attachment A.

4 The

fund value at 30 June 2025 of $112 million exceeds the inflation adjusted

capital base of $110 million. Despite this, year end market volatility meant

that the Fund’s value was not sufficiently above the inflation adjusted

capital base to support a distribution.

OPTIONS

5 As

this is a noting report, no options are provided.

NEXT STEPS

6 Quarterly

reporting on the performance and financial position of the fund will be

provided to future meetings of either the Financial and Council Controlled

Organisations Committee or Council.

Signatories

|

Authoriser:

|

Carolyn Allan - Chief Financial Officer

|

Attachments

|

|

Title

|

Page

|

|

⇩a

|

Waipori Fund- June 2025

Quarter

|

146

|

|

|

Audit and Risk Subcommittee

1 September 2025

|

|

|

Audit and Risk Subcommittee

1 September 2025

|

Resolution to Exclude the

Public

That the Audit and Risk

Subcommittee:

Pursuant to the provisions of the

Local Government Official Information and Meetings Act 1987, exclude the public

from the following part of the proceedings of this meeting namely:

|

General subject of the matter to be considered

|

Reasons

for passing this resolution in relation to each matter

|

Ground(s) under

section 48(1) for the passing of this resolution

|

Reason for

Confidentiality

|

|

C1

Confirmation of the Confidential Minutes of Audit and Risk Subcommittee

meeting - 16 June 2025 - Public Excluded

|

S7(2)(i)

The

withholding of the information is necessary to enable the local authority to

carry on, without prejudice or disadvantage, negotiations (including

commercial and industrial negotiations).

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to prejudice the supply

of similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of natural

persons, including that of a deceased person.

S7(2)(b)(i)

The

withholding of the information is necessary to protect information where the

making available of the information would disclose a trade secret.

S7(2)(h)

The

withholding of the information is necessary to enable the local authority to

carry out, without prejudice or disadvantage, commercial activities.

S7(2)(b)(ii)

The

withholding of the information is necessary to protect information where the

making available of the information would be likely unreasonably to prejudice

the commercial position of the person who supplied or who is the subject of

the information.

|

.

|

|

|

C2

Treasury Risk Management Compliance Report

|

S7(2)(h)

The

withholding of the information is necessary to enable the local authority to

carry out, without prejudice or disadvantage, commercial activities.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C3

DCC Employee Engagement and Wellbeing Survey 2025

|

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of natural

persons, including that of a deceased person.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C4

Audit NZ Report on the 9 year plan 2025-34

|

S7(2)(b)(ii)

The

withholding of the information is necessary to protect information where the

making available of the information would be likely unreasonably to prejudice

the commercial position of the person who supplied or who is the subject of

the information.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C5

Finance Assurance Report

|

S7(2)(h)

The

withholding of the information is necessary to enable the local authority to

carry out, without prejudice or disadvantage, commercial activities.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

The information in this

report is commercially sensitive..

|

|

C6

Internal Audit Workplan Update

|

S7(2)(b)(i)

The

withholding of the information is necessary to protect information where the making

available of the information would disclose a trade secret.

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to prejudice the supply

of similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

S7(2)(h)

The

withholding of the information is necessary to enable the local authority to

carry out, without prejudice or disadvantage, commercial activities.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C7

DCC Internal Audit Actions Update

|

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to prejudice the supply

of similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C8

Legal Matters

|

S7(2)(g)

The

withholding of the information is necessary to maintain legal professional

privilege.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C9

Protected Disclosure Register - August 2025

|

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of natural

persons, including that of a deceased person.

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to prejudice the supply

of similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C10

Investigation Register - August 2025

|

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of natural

persons, including that of a deceased person.

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to prejudice the supply

of similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

This resolution is made in

reliance on Section 48(1)(a) of the Local Government Official Information and

Meetings Act 1987, and the particular interest or interests protected by

Section 6 or Section 7 of that Act, or Section 6 or Section 7 or Section 9 of

the Official Information Act 1982, as the case may require, which would be

prejudiced by the holding of the whole or the relevant part of the proceedings

of the meeting in public are as shown above after each item.

That Rudie Tomlinson (Director,

Audit New Zealand) and Monique Kruger (Manager, Audit New Zealand) be permitted

to attend the meeting, after the public has been excluded, because of his

knowledge of Items C4. This knowledge, which would been of assistance in

relation to the matters discussed, was relevant because they would be reporting

on the item under consideration.