Notice of Meeting:

I hereby give notice that an ordinary meeting of the Audit,

Risk and Assurance Committee will be held on:

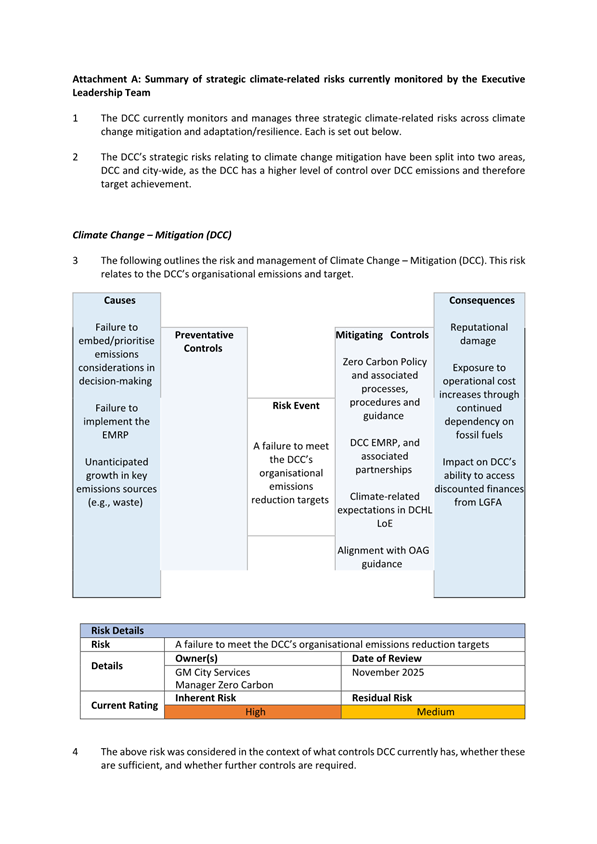

Date: Thursday

4 December 2025

Time: 11.30

am

Venue: Council

Chamber, Dunedin Public Art Gallery, The Octagon, Dunedin

Sandy Graham

Audit, Risk and Assurance Committee

PUBLIC AGENDA

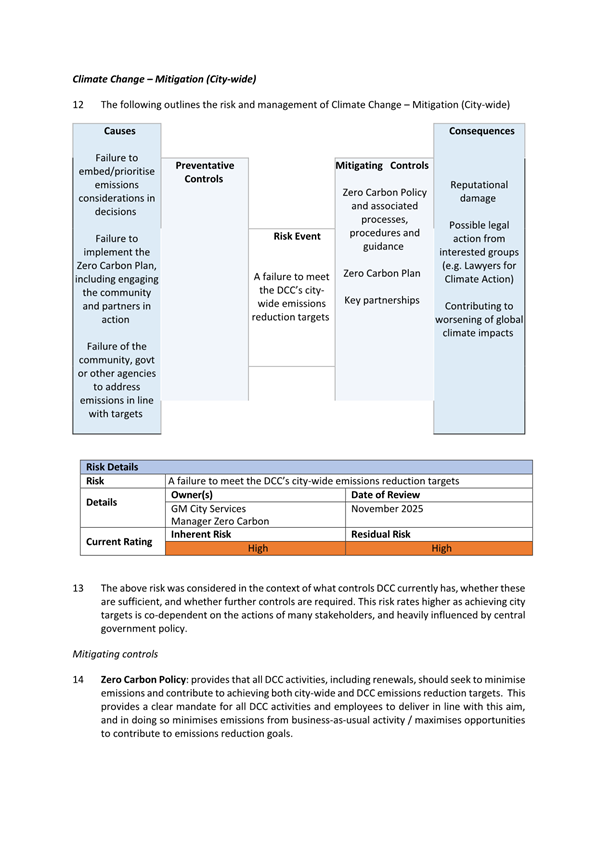

|

Chairperson

|

Warren Allen

|

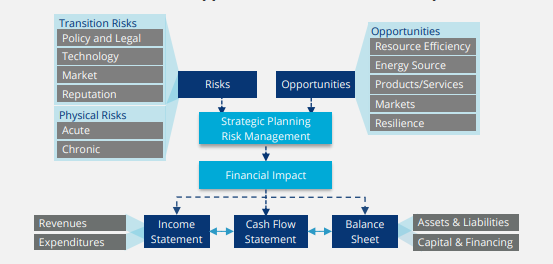

|

|

Deputy Chairperson

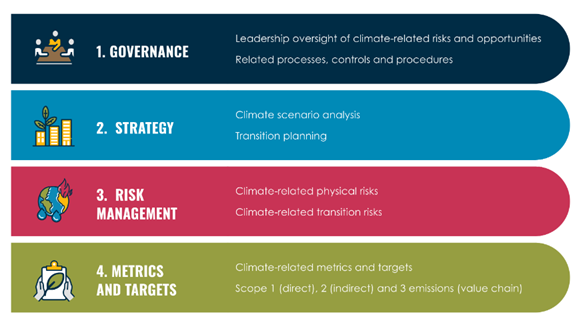

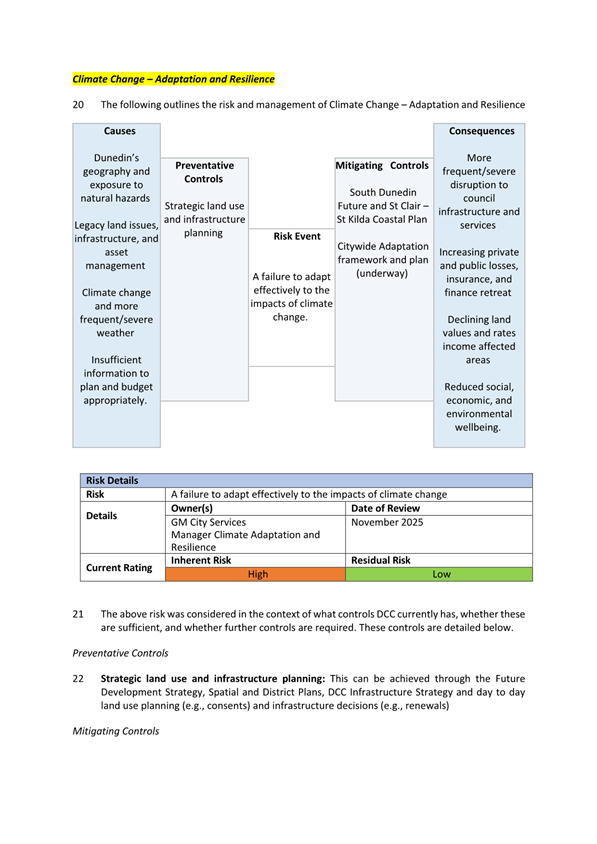

|

Janet Copeland

|

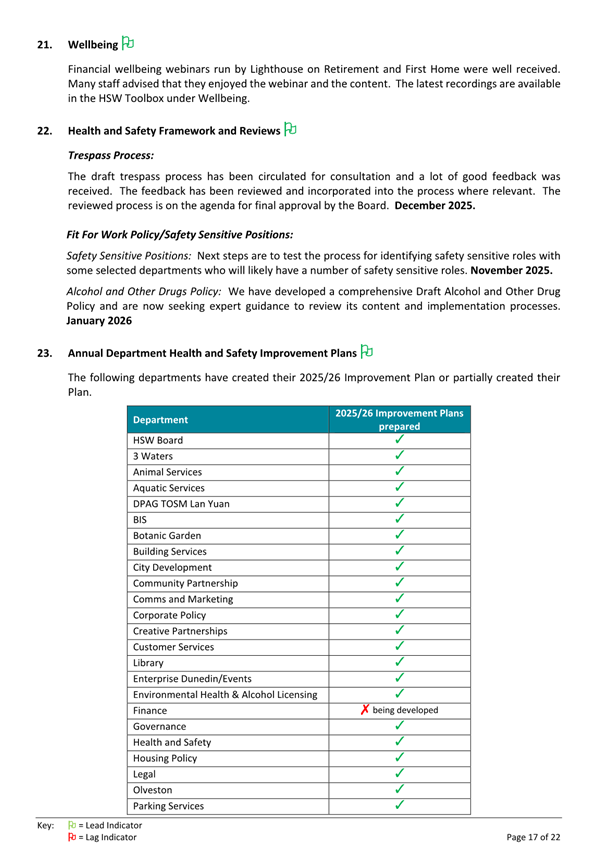

|

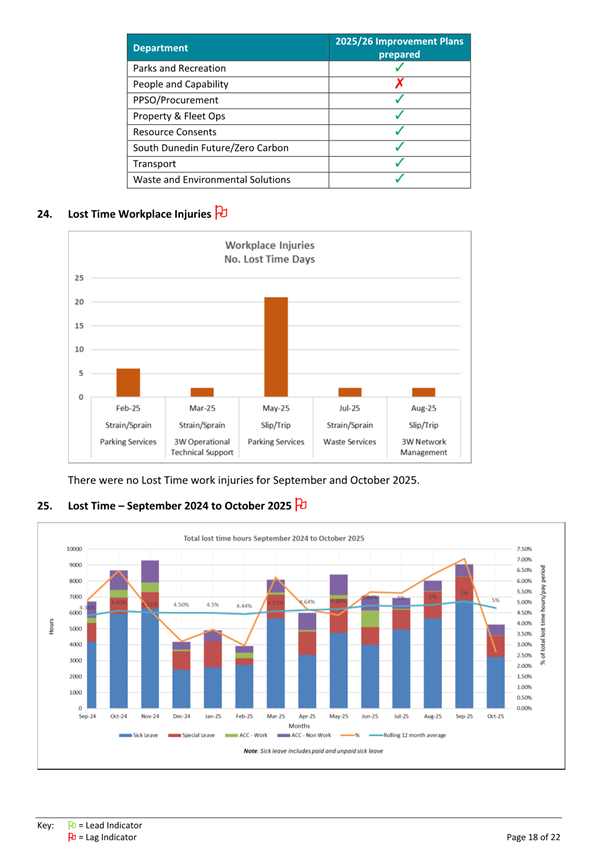

|

Members

|

Mayor Sophie Barker

|

Cr John Chambers

|

|

|

Cr Cherry Lucas

|

Cr Andrew Simms

|

|

|

Cr Lee Vandervis

|

|

Senior Officer Carolyn

Allan, Chief Financial Officer

Governance Support Officer Wendy

Collard

Wendy Collard

Governance Support Officer

Telephone: 03 477 4000

Wendy.Collard@dcc.govt.nz

www.dunedin.govt.nz

Note: Reports

and recommendations contained in this agenda are not to be considered as

Council policy until adopted.

|

|

Audit, Risk and Assurance

Committee

4 December 2025

|

ITEM TABLE OF CONTENTS PAGE

1 Apologies 4

2 Confirmation

of Agenda 4

3 Declaration

of Interest 5

Part

A Reports (Committee has power to decide these matters)

4 Delegations

for the Audit, Risk and Assurance Committee 11

5 Audit,

Risk and Assurance Committee Work Plan 2025-26 14

6 Audit,

Risk and Assurance Committee Updates Report - December 2025 17

7 Health,

Safety and Wellbeing Monthly report for September and October 2025 22

8 Waipori

Fund - Quarter ending 30 September 2025 45

9 Climate-related

risk management 50

10 Financial

Report - Period ended 30 September 2025 70

11 Financial

Strategy Compliance - November 2025 95

12 Elected

Member Gifts and Hospitality - Guidance 104

Resolution to Exclude the Public 160

|

|

Audit, Risk and Assurance

Committee

4 December 2025

|

1 Apologies

At the close of the agenda no

apologies had been received.

2 Confirmation

of agenda

Note:

Any additions must be approved by resolution with an explanation as to why they

cannot be delayed until a future meeting.

|

|

Audit, Risk and Assurance Committee

4 December 2025

|

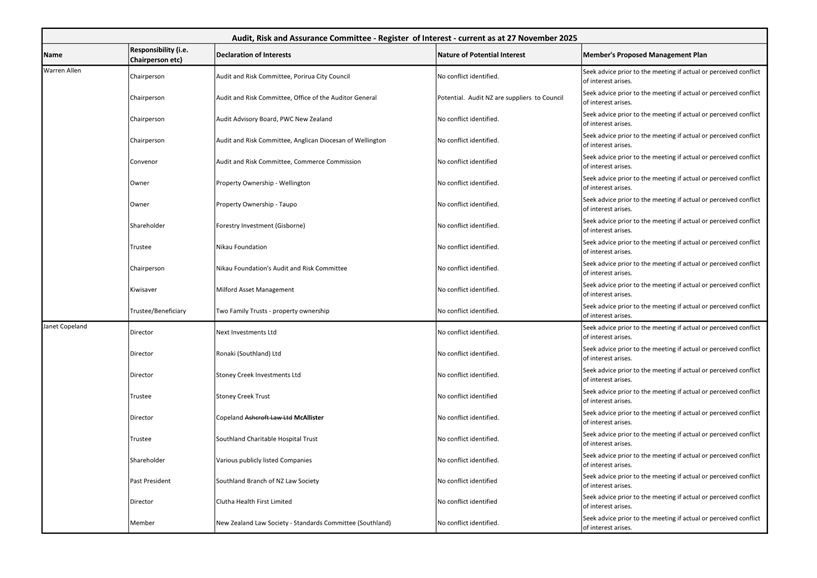

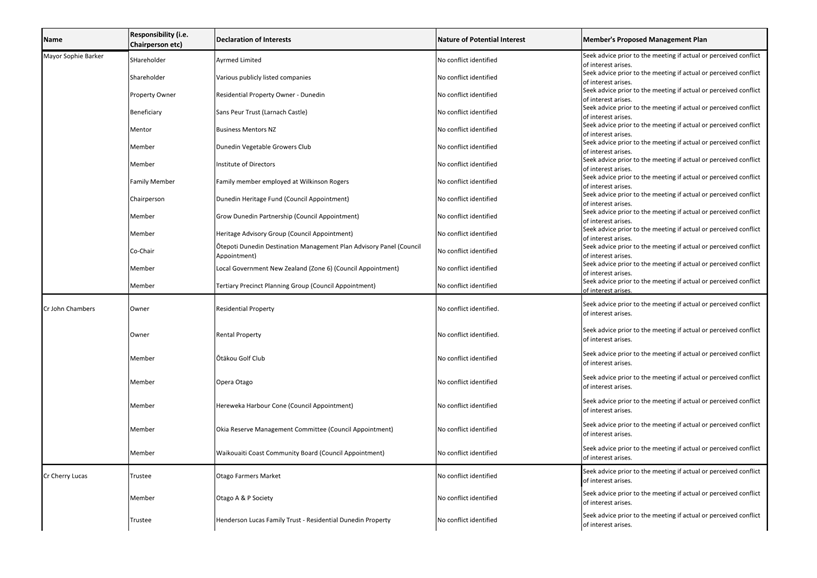

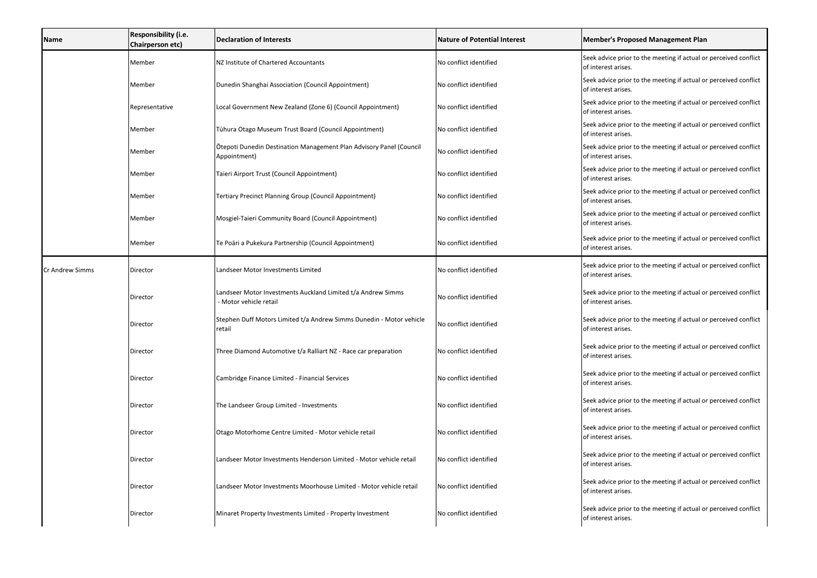

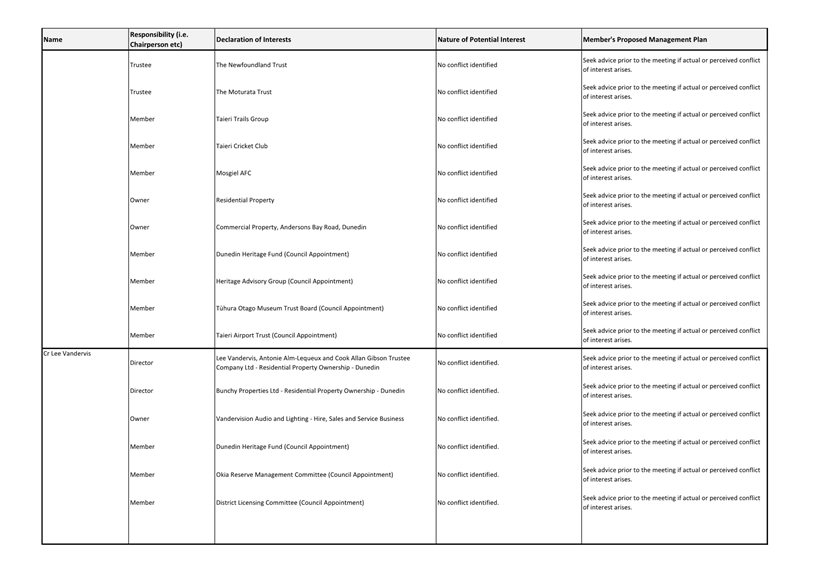

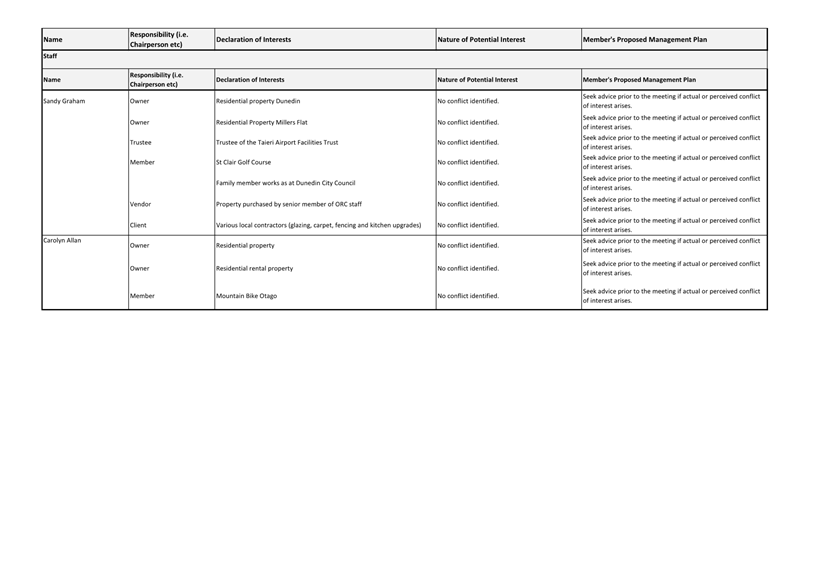

Declaration of Interest

EXECUTIVE SUMMARY

1. Members

are reminded of the need to stand aside from decision-making when a conflict

arises between their role as an independent or elected representative and any

private or other external interest they might have.

2. Elected

and Independent members are reminded to update their register

of interests as soon as practicable, including amending the register at this

meeting if necessary.

RECOMMENDATIONS

That the Committee:

a) Notes/Amends if

necessary the Elected or Independent Members' Interest Register attached as

Attachment A; and

b) Confirms/Amends the

proposed management plan for Elected or Independent Members' Interests.

Attachments

|

|

Title

|

Page

|

|

⇩a

|

Register of Interests

|

6

|

|

|

Audit, Risk and Assurance Committee

4 December 2025

|

|

|

Audit, Risk and Assurance Committee

4 December 2025

|

Part

A Reports

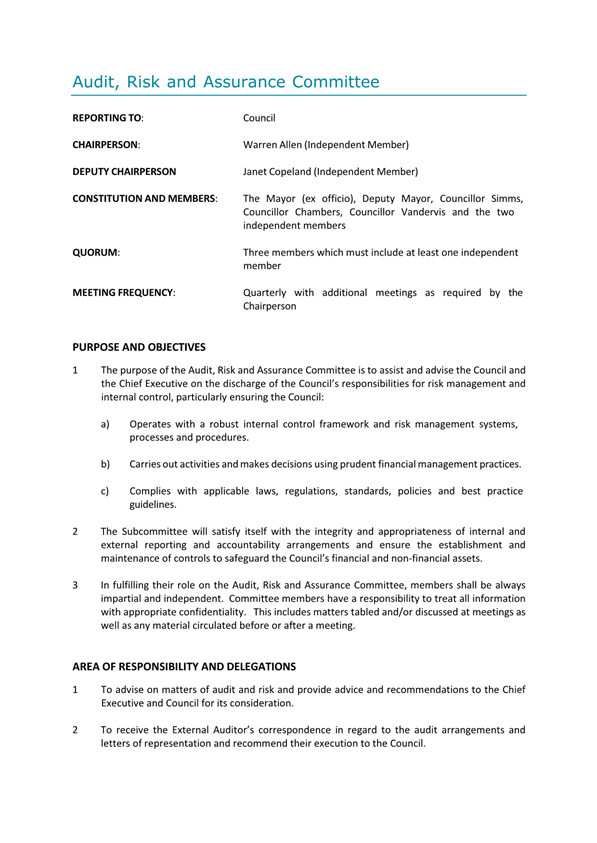

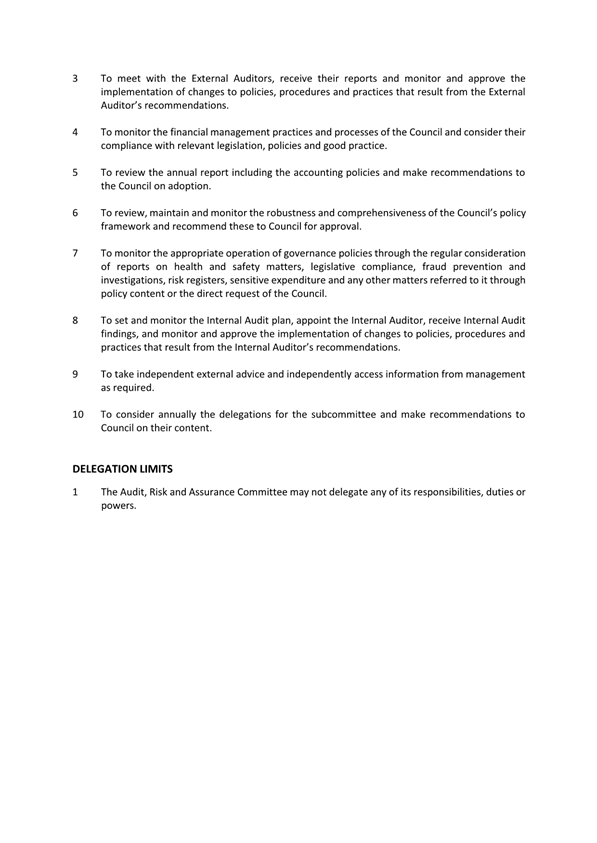

Delegations for the Audit, Risk and Assurance Committee

Department: Civic

EXECUTIVE SUMMARY

1 This

report provides a copy of the Audit, Risk and Assurance Committee’s

delegations for the Committee’s information (Attachment A)

2 The

Chairperson will also provide an overview of roles and responsibilities of an

Audit, Risk and Assurance Committee.

3 As

this is an administrative report, there is Summary of Considerations.

RECOMMENDATIONS

That the Committee:

a) Notes the delegations

and overview of the Audit, Risk and Assurance Committee.

Signatories

|

Author:

|

Wendy Collard - Governance Support Officer

|

|

Authoriser:

|

Jackie Harrison - Manager Governance

|

Attachments

|

|

Title

|

Page

|

|

⇩a

|

Audit, Risk and

Assurance Committee Delegations

|

12

|

|

|

Audit, Risk and Assurance Committee

4 December 2025

|

|

|

Audit, Risk and Assurance Committee

4 December 2025

|

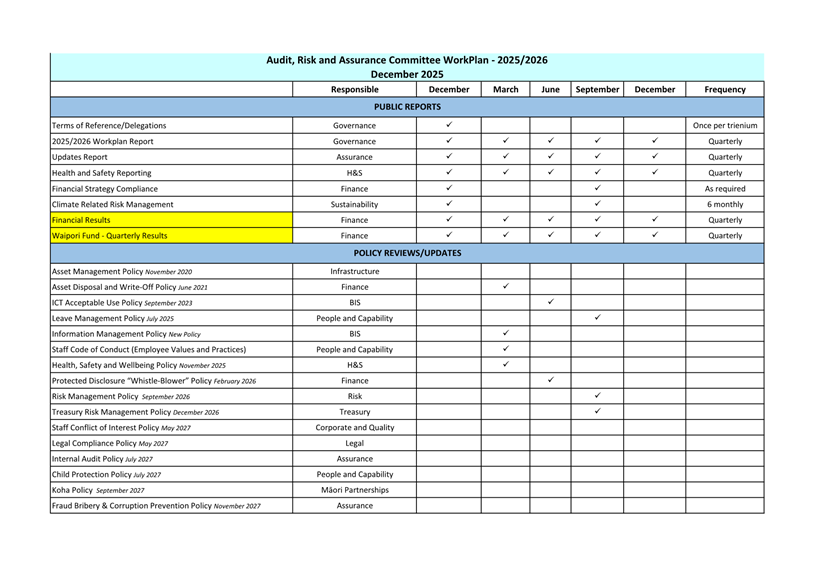

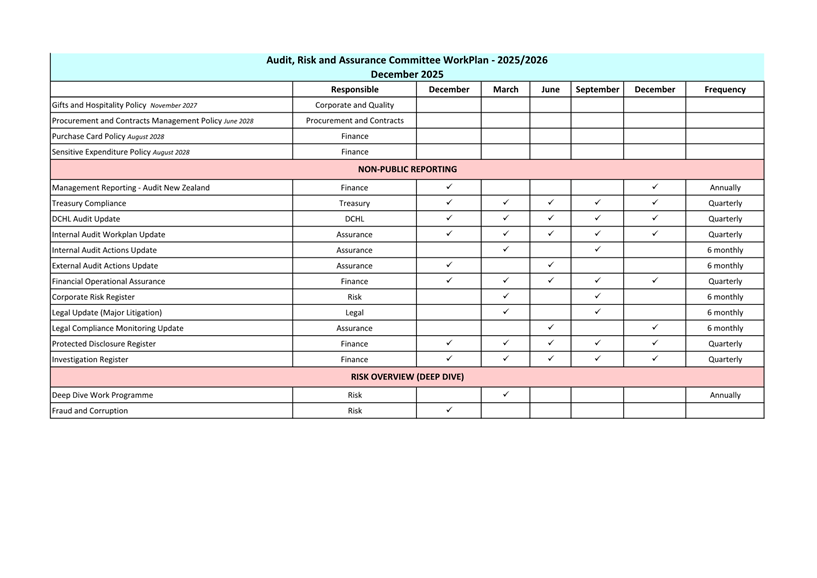

Audit, Risk and Assurance Committee Work Plan 2025-26

Department: Civic

EXECUTIVE SUMMARY

1 This

report provides a copy of the Audit, Risk and Assurance Committee Work Plan

2025-26 which has been aligned to work programme scheduling and decision

making.

2 Please

note that the items without ticks shown have not been scheduled for action. A

Deep Dive work programme will be developed and presented to the Committee in

2026. Deep dive topics will reflect high or emerging risks.

3 As

this is an administrative report only, the Summary of Consideration is not

required.

RECOMMENDATIONS

That the Committee:

a) Notes the Audit, Risk

and Assurance Committee Work Plan for 2025-26.

Signatories

|

Author:

|

Wendy Collard - Governance Support Officer

|

|

Authoriser:

|

Carolyn Allan - Chief Financial Officer

|

Attachments

|

|

Title

|

Page

|

|

⇩a

|

Audit, Risk and

Assurance Committee WorkPlan

|

15

|

|

|

Audit, Risk and Assurance Committee

4 December 2025

|

|

|

Audit, Risk and Assurance Committee

4 December 2025

|

Audit, Risk and Assurance Committee Updates Report -

December 2025

Department: Finance

EXECUTIVE SUMMARY

1 This

report provides updates on the progress of various sundry matters that have

been noted by the Committee.

RECOMMENDATIONS

That the Committee:

a) Notes the Audit, Risk

and Assurance Committee Updates Report – December 2025

DISCUSSION

Insurance

2 The

liability insurance programme has now been fully renewed with effect from 1

November 2025. The policies include general/public liability, statutory

liability, professional indemnity, and employer’s liability, with the

required capacity secured.

3 Full

cost insurance valuations are being undertaken at the DCC aquatic buildings and

University Oval assets (including plant).

4 Refresher

training is being scheduled with Project and Contract Managers on the contract

works insurance policy including key risks around hot works and hazardous

substance warranties.

2024/25

Annual Report

5 The

final audit fieldwork started in the week of 15 September 2025 and finished on

31 October 2025, resulting in an unqualified audit opinion.

6 Following

the audit process, the 2024/25 Annual Report was adopted by Council at its

inaugural meeting of the new triennium on 31 October 2025.

7 The

2024/25 Annual Report Summary has been prepared by staff and has been audited

by Audit NZ. An audit opinion was received in the week beginning 24 November

2025.

8 Following

this, the 2024/25 Annual Report and its Summary have been published on the DCC

website, within statutory deadlines.

9 Recommended

improvements to the development of future Annual Reports are as follows:

a) 3

Waters valuations are completed as at 31 March. Over the past four years, there

have been recurring issues with valuations, and completing them three months

earlier than usual provides a buffer to address any potential challenges.

b) More

detail is included on the performance of each Council-Controlled Organisation

(CCO). While the primary focus of the Annual Report is the performance of the

DCC, more supporting information on CCOs would provide helpful context to a

reader.

c) The

timeline for the development of the Annual Report is incrementally brought

forward each year, in consultation with Dunedin City Holdings Limited and Audit

NZ. This will ensure that the 2027/28 Annual Report can be adopted ahead of the

next local government elections.

2026/27 Annual Plan

10 Work on the

development of the 2026/27 Annual Plan continues. The development of the Plan

is being used as an opportunity to identify new or improved revenue streams,

and to review expenditure.

11 Budget

update reports for each activity are being prepared and will be considered by

Council in January 2026.

12 The

schedule for development of the 2026/27 Annual Plan includes sufficient time

for an amendment, including audit, should one be required to address a

significant or material change from Year 2 of the 9 Year Plan. Community engagement

is tentatively scheduled for March/April 2026.

13 The Annual

Plan 2026/27 will be adopted by Council by 30 June 2026.

Local Water Done Well

14 All

legislation making up the three stages of “Local Water Done Well”

have now been passed.

15 Council’s

Water Services Delivery Plan (WSDP) was accepted by the Secretary for Local

Government on 10 November 2025 and confirms acceptance of the in-house delivery

model. DIA accepted the plan without any changes being required and recommended

that the delivery of projects required to achieve regulatory compliance is

monitored.

16 Staff

are now in the process of implementing the WSDP. A programme governance

structure has been proposed with ELT representation and a cross departmental

group will be formed to meet regularly and coordinate implementation delivery.

This group will include representation from 3 Waters, finance and legal and

others as required. The DCC Project Management Framework (PMF) has been adopted

to manage this programme of work.

Policy Updates

17 The

following policies are undergoing review:

a) Information

Management Policy

b) Asset

Disposal and Write-Off Policy

c) ICT

Acceptable Use Policy

d) Staff Code

of Conduct

e) Health,

Safety and Wellbeing Policy

18 After

the review process, updated copies of DCC policies will be provided to the

Committee for either feedback or approval.

OPTIONS

19 This is a

noting report so there are no options.

Signatories

|

Author:

|

Hayley Knight - Assurance Manager

|

|

Authoriser:

|

Carolyn Allan - Chief Financial Officer

|

Attachments

There are no attachments for this report.

|

SUMMARY OF CONSIDERATIONS

|

|

Fit with purpose of Local Government

This report provides an update on various

audit, risk and assurance related matters.

|

|

Fit with strategic framework

|

|

Contributes

|

Detracts

|

Not applicable

|

|

Social Wellbeing Strategy

|

✔

|

☐

|

☐

|

|

Economic Development Strategy

|

✔

|

☐

|

☐

|

|

Environment Strategy

|

✔

|

☐

|

☐

|

|

Arts and Culture Strategy

|

✔

|

☐

|

☐

|

|

3 Waters Strategy

|

✔

|

☐

|

☐

|

|

Future Development Strategy

|

✔

|

☐

|

☐

|

|

Integrated Transport Strategy

|

✔

|

☐

|

☐

|

|

Parks and Recreation Strategy

|

✔

|

☐

|

☐

|

|

Other strategic projects/policies/plans

|

☐

|

☐

|

✔

|

This report provides an update on the progress made by

Council to deliver upon the activities identified by the Audit, Risk and

Assurance Committee, which is a regulatory function and considered good

quality and cost effective

|

|

Māori Impact Statement

There are no known impacts for mana whenua

|

|

Sustainability

There are no implications for sustainability

|

|

Zero carbon

There

are no implications for zero carbon

|

|

LTP/Annual Plan / Financial Strategy /Infrastructure

Strategy

There are no implications

|

|

Financial considerations

No financial implications have been identified

|

|

Significance

This report is rated low under the Council’s

Significance and Engagement Policy

|

|

Engagement – external

No external engagement has been undertaken

|

|

Engagement - internal

Activities noted herein include cross Council engagement

and collaboration

|

|

Risks: Legal / Health and Safety etc.

No risks have been identified

|

|

Conflict of Interest

There are no conflict of interest identified

|

|

Community Boards

There have been no implications for Community Boards

identified

|

|

|

Audit, Risk and Assurance Committee

4 December 2025

|

Health, Safety and Wellbeing Monthly report for September

and October 2025

Department: Health and Safety

EXECUTIVE SUMMARY

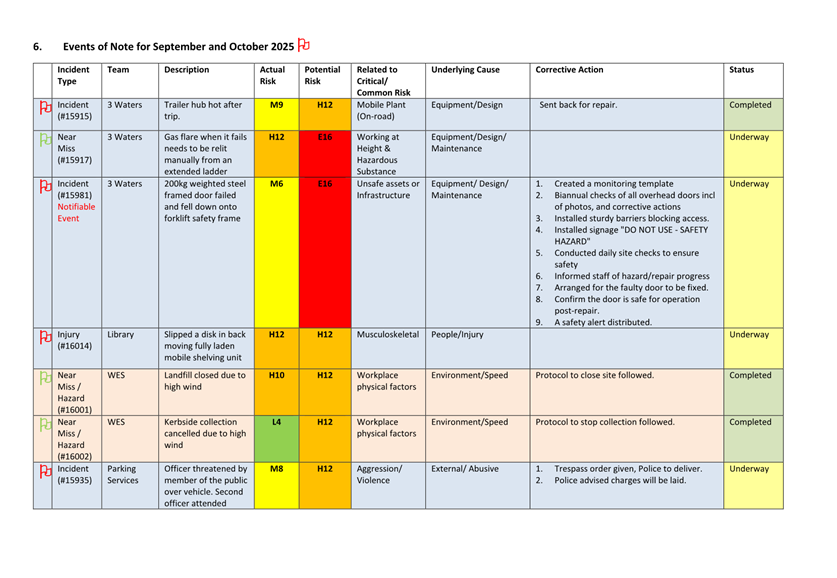

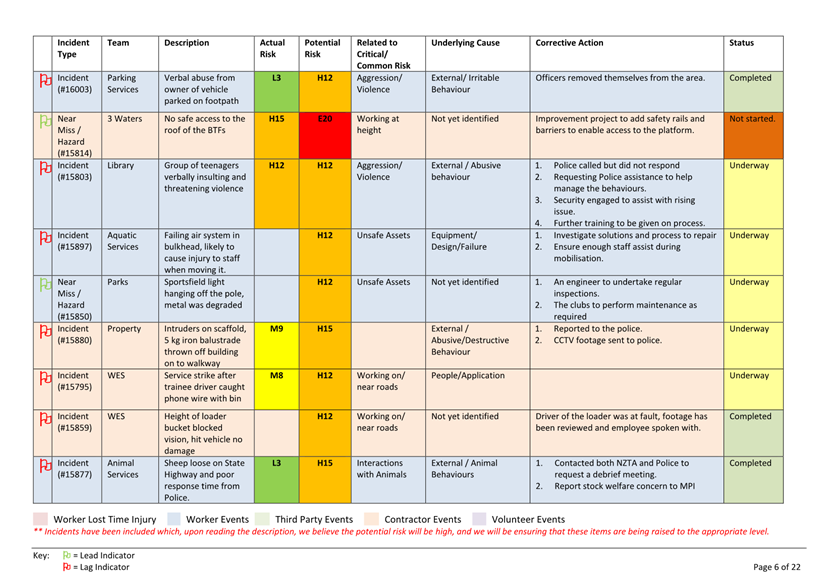

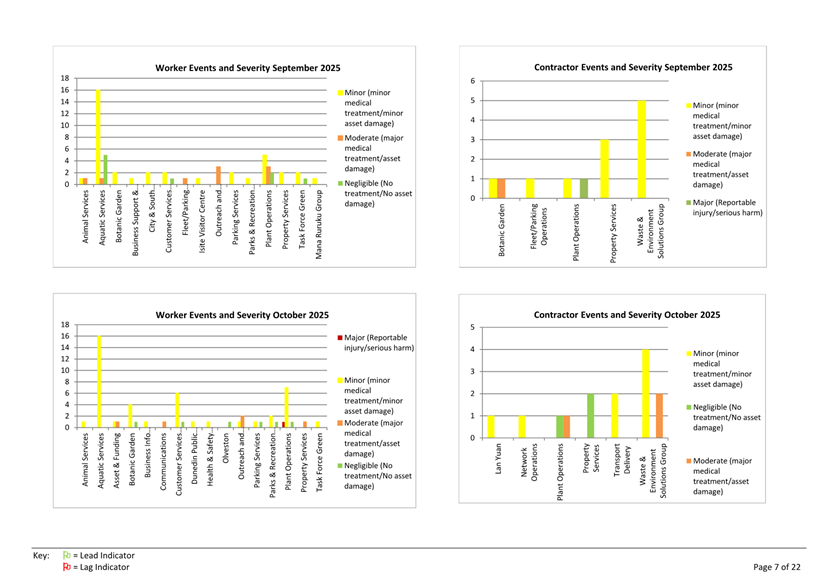

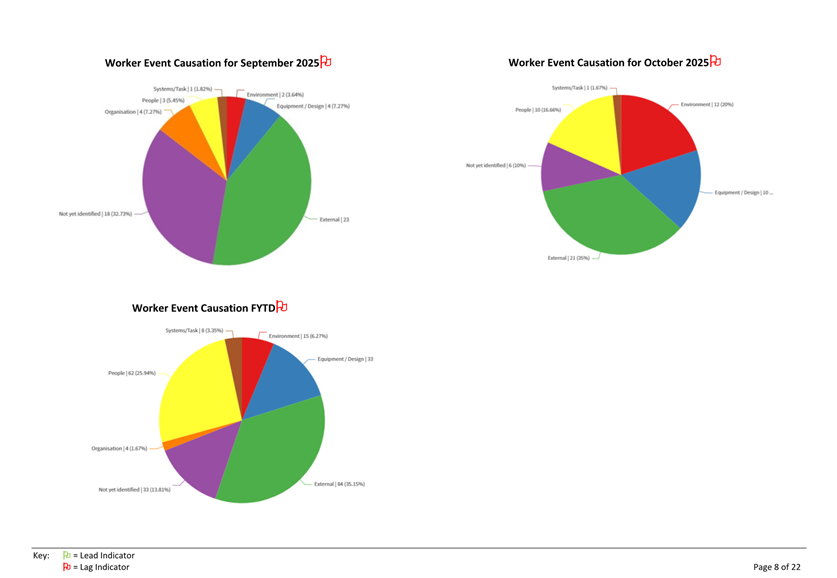

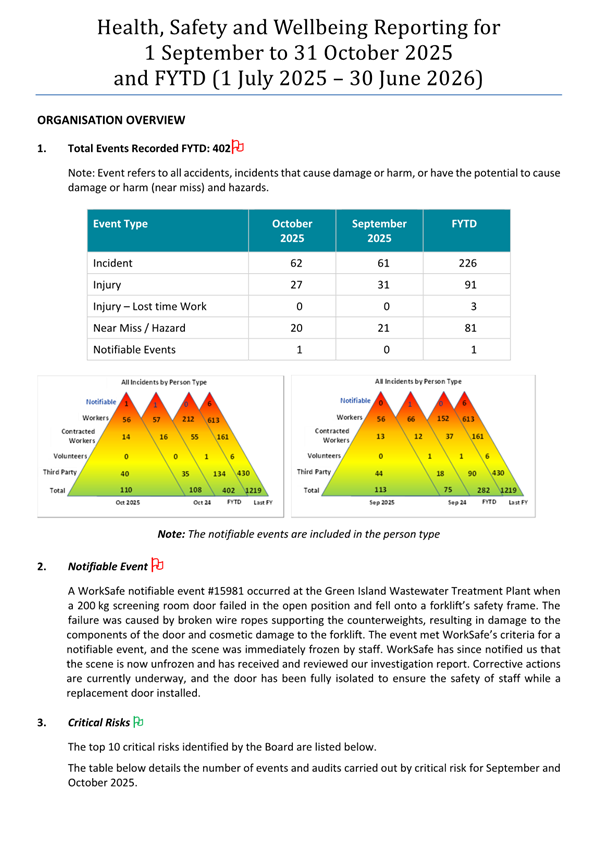

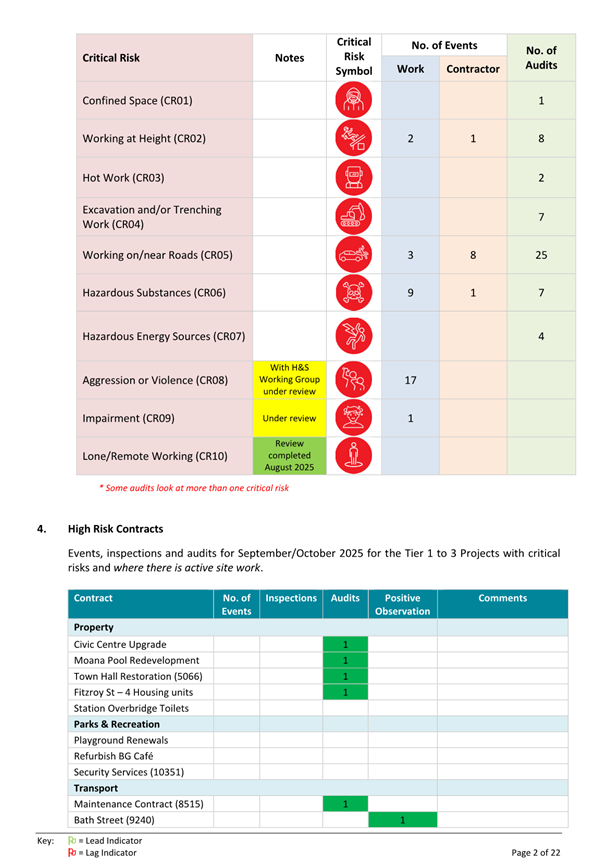

1 The

monthly Health, Safety and Wellbeing report for September and October 2025 is

attached for consideration.

RECOMMENDATIONS

That the Committee:

a) Notes the monthly

Health, Safety and Wellbeing report for September and October 2025.

Signatories

|

Author:

|

Jane Pearce - Health and Safety Manager

|

|

Authoriser:

|

Paul Henderson - General Manager Corporate and Regulatory

Services

|

Attachments

|

|

Title

|

Page

|

|

⇩a

|

Health, Safety and

Wellbeing monthly report for September and October 2025

|

23

|

|

|

Audit, Risk and Assurance Committee

4 December 2025

|

|

|

Audit, Risk and Assurance Committee

4 December 2025

|

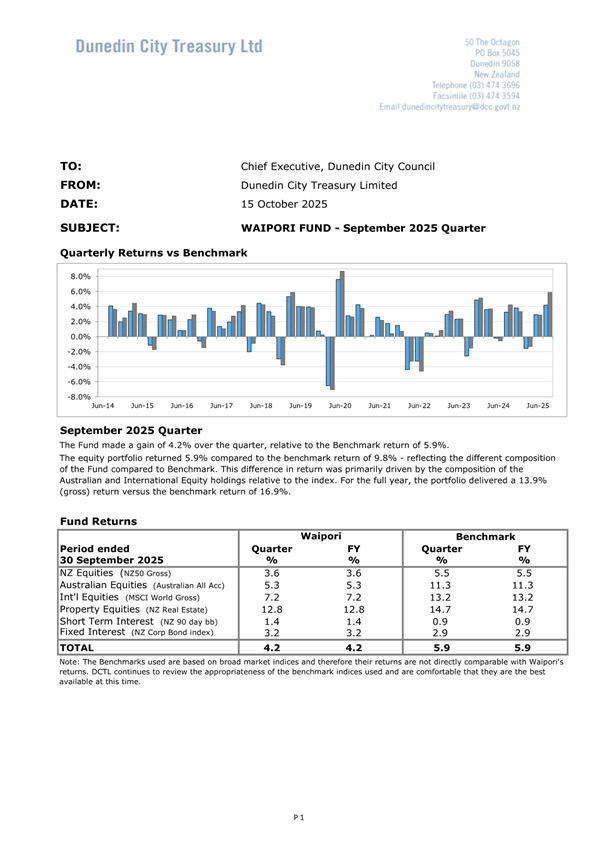

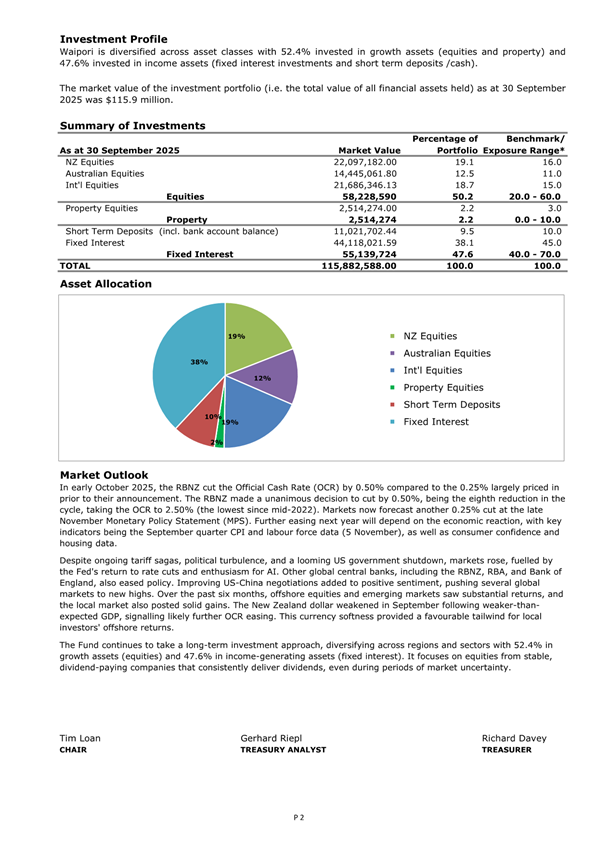

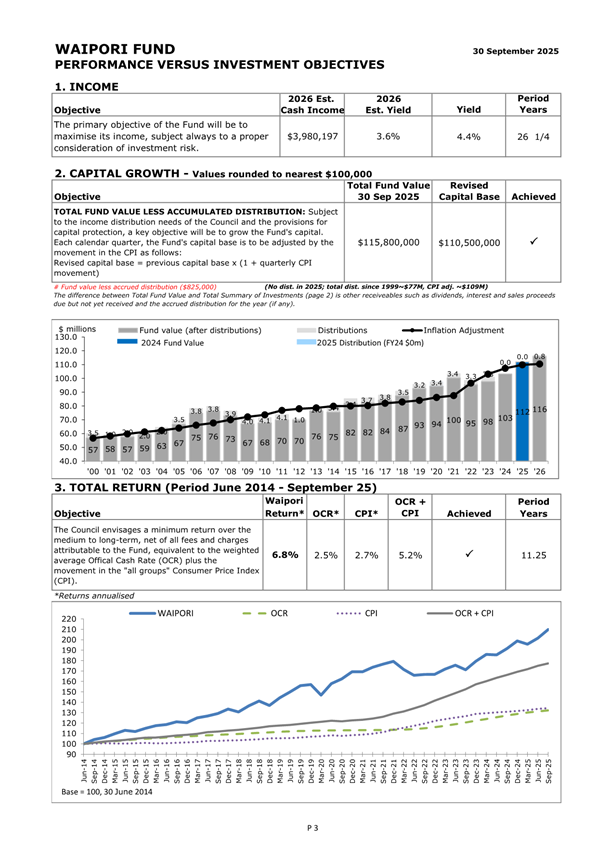

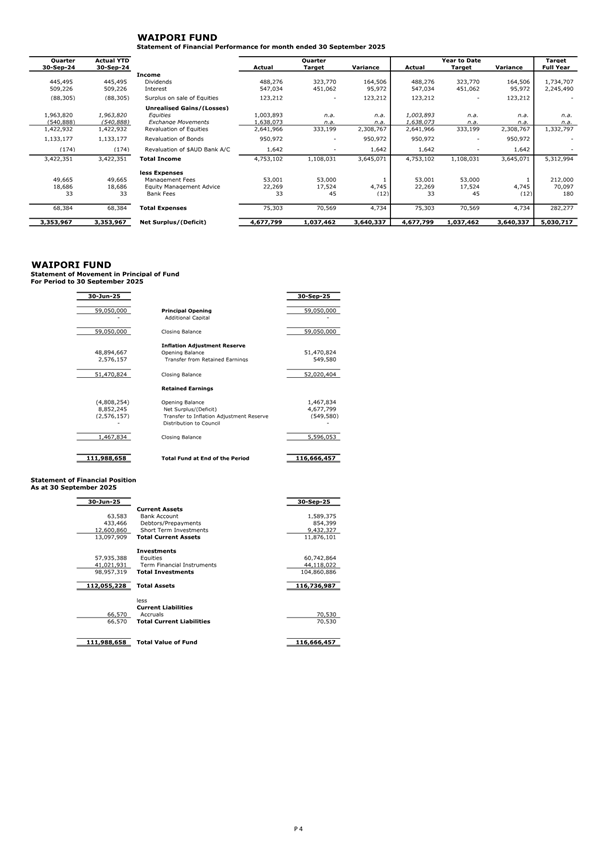

Waipori Fund - Quarter ending 30 September 2025

Department: Finance

EXECUTIVE SUMMARY

1 The

attached report from Dunedin City Treasury Limited provides information on the

results of the Waipori Fund for the quarter ended 30 September 2025. The report was presented to the Council meeting held on Tuesday, 11

November 2025.

RECOMMENDATIONS

That the Committee:

a) Notes the report from

Dunedin City Treasury Limited on the Waipori Fund for the quarter ended 30

September 2025.

DISCUSSION

2 The

Waipori Fund Statement of Investment Policy and Objectives (SIPO) requires

quarterly reporting on the performance and financial position of the fund.

3 Dunedin

City Treasury Limited has provided the Waipori Fund report for the September

2025 quarter. The report is provided as Attachment A.

OPTIONS

4 As

this is a noting report, no options are provided.

NEXT STEPS

5 Quarterly

reporting on the performance and financial position of the fund will be

provided to future Council meetings.

Signatories

|

Authoriser:

|

Carolyn Allan - Chief Financial Officer

|

Attachments

|

|

Title

|

Page

|

|

⇩a

|

Waipori Fund - Quarter

ending 30 September 2025

|

46

|

|

|

Audit, Risk and Assurance Committee

4 December 2025

|

|

|

Audit, Risk and Assurance Committee

4 December 2025

|

Climate-related risk management

Department: Zero Carbon, Climate and City Growth and Quality

and Improvement

EXECUTIVE SUMMARY

1 This

report provides information on the DCC’s current climate-related risk

management framework, and compares this with evolving best practice. It

discusses potential to strengthen the DCC’s approach.

2 The

DCC’s climate change response comprises mitigation and adaptation work

programmes (Zero Carbon and Climate Adaptation and Resilience). The DCC

currently monitors and manages three strategic climate-related risks.

3 Best

practice suggests that integration of climate change considerations across

governance, strategy, risk management, metrics/targets, and assurance is

required for an organisation to manage climate-related risk and opportunity

coherently and successfully.

4 The

DCC is giving effect to recent sector-specific guidance from the Office of the

Auditor General (OAG) on climate-related risk management and associated

organisational frameworks. However, an approach more closely aligned with the

New Zealand Climate Standards would afford ELT and Council deeper insights on

key areas of risk and opportunity, to support stronger climate-related

decision-making.

5 The

preferred option is for staff to investigate ways the DCC could align more

strongly with the NZ Climate Standards approach to climate-related risk

management. Staff would report their findings back to the Audit, Risk and

Assurance (ARAS) Subcommittee, no later than July 2026.

RECOMMENDATIONS

That the Subcommittee:

a) Notes the

climate-related risk management report

b) Approves staff

investigation of ways the DCC could align more strongly with the NZ Climate

Standards approach to climate-related risk management

BACKGROUND

Responding to climate change has two aspects:

mitigation and adaptation

6 Climate

Change is defined as a change of climate which is attributed directly or

indirectly to human activity that alters the composition of the global

atmosphere, and which is in addition to natural climate variability observed

over comparable time periods.

7 Climate

change mitigation is a human intervention to reduce emissions or enhance

the sinks of greenhouse gases.

8 Climate

change adaptation is the process of adjustment to actual or expected

climate and its effects, in order to moderate harm or exploit beneficial

opportunities.

The terms ‘resilience’ and ‘adaptation’ are often used

interchangeably in climate change discourse. While they are complementary

terms, there are subtle but important differences. Resilience describes the

capacity to anticipate and cope with shocks or adverse events, and to recover

from the associated impacts in a timely and efficient manner. In this sense,

adaptation is part of and contributes to resilience.

9 Most

economic sectors and industries are affected both by climate-related risks and

by the transition to a lower-carbon economy. There are also significant

opportunities for organisations focused on climate change mitigation and

adaptation.

10 While no

equivalent figures are available for Dunedin, a report by Deloitte estimates

that inadequate climate action could cost the New Zealand economy $4.4 billion

by 2050, with losses becoming exponentially worse after that. On the other

hand, decisive climate action could deliver $64 billion to New Zealand’s

economy by 2050.

11 The Office

of the Auditor General has recently updated its advice to councils with respect

to climate change. In doing so, it commented that:

“…in many ways,

councils are at the front line of a wider response to climate change. Councils

are largely responsible for civil defence, regional and district land use,

planning and major community infrastructure. They are also the owners of

significant assets, some of which are at risk because of climate change. They

also have a role in reducing greenhouse gas emissions.

Councils have obligations to

keep their communities and assets safe from the impacts of a changing climate.

They also have a responsibility to consult and keep their communities informed

about the scenarios they are planning for and the steps they are taking to

protect people and property.”

The DCC’s

climate change responses comprises two key work programmes

12 Across both

work programmes, the approach is designed to be practical, focused on outcomes,

and aligned with the city’s broader goals for economic and community

development. A low emissions, climate-resilient Ōtepoti Dunedin ultimately

means better local services and infrastructure, more efficient systems,

improved public health and wellbeing, as well as contributing to global climate

goals.

Climate change mitigation

13 The Zero

Carbon work programme supports emissions reduction at both the organisation

scale (DCC emissions) and the wider city scale (Dunedin emissions). It is led

by the Zero Carbon team but integrates with, and is co-dependent on, the work

of teams across the DCC. There is also an emphasis for the work programme on

collaboration with external partners.

Climate change adaptation

14 A citywide

climate adaptation and resilience framework is in development to guide

Council and communities as they make decisions about how to respond to natural

hazards and the anticipated impacts of climate change. This work commenced only

recently and is led by the newly formed Climate Adaptation and Resilience team.

The team and work programme have evolved out of the South Dunedin Future

programme – a joint initiative between the DCC and the Otago Regional

Council (in close association with other stakeholders) focused on producing a

long-term adaptation plan for the area by the end of 2026.

DISCUSSION

Best practice

climate-related risk management

15 Recent

years have seen rapid evolution of the guidance and tools available to steer

organisations’ climate-related risk management. Related to this, there is

an increasing focus on climate-related reporting and disclosures, and a growing

expectation from central government, private sector, and communities that local

government will align with the spirit and intent of these approaches.

International

guidance - Taskforce on Climate-related Financial Disclosures

16 In 2023,

the Task Force on Climate-related Financial Disclosures (TCFD, initiated by the

G20) set out recommendations for clear, comparable and consistent

climate-related disclosures. The aim was to:

a) promote

routine consideration of climate change in business and investment decisions

b) enable

entities to better demonstrate responsibility and foresight on climate

c) drive

smarter, more efficient allocation of capital, and

d) smooth the

transition to a low-carbon economy.

17 The

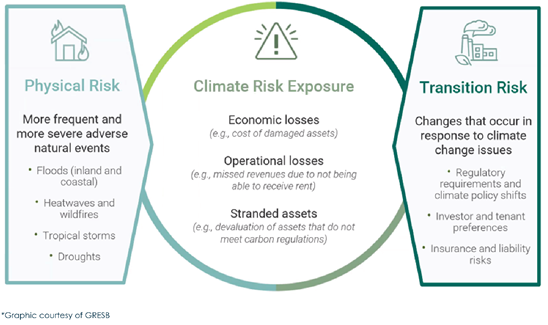

TCFD identified that an organisation’s climate risk exposure is a

function of both physical risks caused by the impacts of climate change,

and transition risks associated with changes that occur in response to

climate change issues:

18 The are

four core elements of TCFD’s recommended climate-related financial

disclosures, including risk management:

19 The TCFD

recommended greater emphasis on the impact of climate-related risks and

opportunities on an organisation’s future financial position (as

reflected in its income statement, cash flow statement, and balance sheet).

This is summarised by the figure below:

National guidance - Aotearoa New Zealand Climate

Standards

20 The New

Zealand government introduced a mandatory climate-related disclosures regime in

2023, applying to financial institutions, as well as managers of large investment

schemes and licensed/large listed issuers that meet certain thresholds. In

2025, thresholds for mandatory participation were revised upwards.

21 Under the

regime, climate reporting entities must report in line with the Aotearoa New

Zealand Climate Standards (NZ Climate Standards) issued by the External Reporting

Board (XRB). The NZ Climate Standards were developed largely in line with TCFD

recommendations (there are sections on governance, strategy, risk

management, metrics and targets), with an added emphasis on assurance

of emissions disclosed by an organisation under the standard. Key elements of

disclosure can be summarised as follows:

Source:

GRESB

22 The

standards can also be adopted voluntarily by organisations, to improve planning

and resilience. Examples of Dunedin organisations that have voluntarily aligned

with the standards include Silver Fern Farms and the University of Otago.

23 Within the

local government sector, strict adherence to the NZ Climate Standards appears

to be limited to entities that were caught by the 2023 legislation e.g.

Auckland Council (which report at a Group level), and Christchurch City

Holdings Ltd.

24 However,

local government is increasingly looking to TCFD and the NZ Climate Standards

to inform management approaches. This includes in management of council

controlled organisations (e.g. Nelson City Council/Tasman District Council have

set an expectation that their Infrastructure Holdings company provide

climate-related disclosure on an ongoing basis).

Sector-specific guidance - climate-related

OAG recommendations

25 In

late 2024 the Office of the Auditor General (OAG) released a report auditing

the performance of four councils’ climate work. The report included five

recommendations for councils, emphasising the need for clarity and transparency

with the public in climate-related objective setting and progress monitoring/reporting.

The recommendations echo best practice established by the TCFD framework, and

the NZ Climate Standard, by emphasising governance, strategy, metrics

and targets:

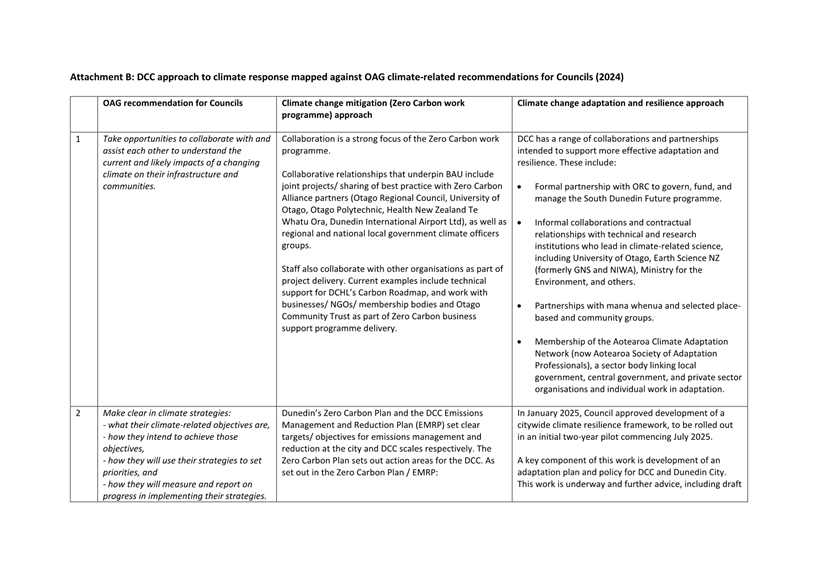

a) Take

opportunities to collaborate with and assist each other to understand the current

and likely impacts of a changing climate on their infrastructure and

communities.

b) Make clear

in climate strategies:

i) what

their climate-related objectives are,

ii) how

they intend to achieve those objectives,

iii) how they

will use their strategies to set priorities, and

iv) how they will

measure and report on progress in implementing their strategies.

c) Strengthen

the use of performance measures that reflect climate-related strategic

objectives and priorities.

d) Clearly set

out how climate-related activities will be governed and ensure that staff

understand what information the relevant governance body needs to govern

effectively.

e) Report

publicly on progress with their climate change strategies and work programmes,

to support accountability and so communities are well-informed, engaged, and

supportive.

26 Previous

OAG advice has also emphasised a role of Audit and Risk committees in

climate-related risk management.

The

DCC’s current approach to climate-related risk management and disclosure

27 The

DCC’s approach to climate-related risk management has evolved over time,

as the organisation’s general risk management framework and climate

change work programmes have matured.

28 From a

purely risk management perspective, ELT has included three climate-related

risks in its suite of strategic risks, considered as part of regular

monitoring:

a) Climate

Change (Mitigation – DCC): A failure to meet the DCC’s

organisational emissions reduction targets

b) Climate

Change (Mitigation – City-wide): A failure to meet the DCC’s

city-wide emissions reduction targets.

c) Adaptation

to Climate Change: A failure to respond effectively to the impacts of

climate change

29 The risks,

along with current ratings, mitigating controls and improvement plans are set

out in Attachment A.

30 However,

as discussed above, recent guidance at all scales places climate-related risk

management firmly in the context of wider organisational frameworks. Best

practice suggests that integration of climate change considerations across

governance, strategy, risk management, metrics/targets, and assurance is

required for an organisation to manage climate-related risk and opportunity

coherently and successfully.

31 The

DCC has to date closely followed and sought to align with evolving

climate-related OAG guidance. Council was most recently updated on alignment in

November 2024, when it noted the Zero Carbon work programme approach to align

with the OAG’s most recent recommendations (CNL/2024/221). At that

time, the city-wide climate change adaptation and resilience work programme had

not yet been developed or approved.

32 Attachment

B provides an updated view of how the OAG’s recommendations are being

given effect to. The approach is built out across the Zero Carbon work programme,

which has had a clear mandate to address climate change mitigation at both city

and DCC scales since its genesis in 2020. Work is underway to build a similar

framework for climate change adaptation and resilience at both city and DCC

scales, which is currently in design as part of an initial two-year pilot

through to June 2027. Further advice will be provided to ARAS and Council once

design works have progressed, likely in mid-2026.

33 When

compared with the NZ Climate Standards, the DCC is fully aligned with some

elements of the standards, including emissions-related metrics and annual

assurance of Scope 1, 2 and 3 emissions.

Further evolution of DCC’s climate-related risk

management

34 While the

DCC’s current approach aligns with OAG recommendations, the structured

approach set out in the NZ Climate Standards is a step up from current DCC

climate-related risk management practice. The approach prescribed by the

NZ Climate Standards involves scenario development and analysis,

risk/opportunity identification and impact assessment. It supports

organisations to develop a more granular understanding of both physical and

transition risks and mitigations, as well as climate-related opportunities.

35 Within the

local government sector, Auckland Council is most advanced with respect to

development of a formal NZ Climate Standards-aligned approach. It has developed

its framework at a group level, and currently manages 16 material

climate-related risks. Auckland Council anticipates its climate-related

scenarios will be reviewed on a three-yearly basis, with an annual review of

the group’s climate-related risks and ratings. Work is also underway on a

climate-related risk management framework that can be used by operational

teams.

36 While a

climate-related risk management and disclosures regime fully compliant with the

NZ Climate Standards would be a significant undertaking and beyond the current

capacity of the DCC’s Zero Carbon and Climate Adaptation and Resilience

teams to resource, greater alignment with the standards would afford ELT and

Council deeper insights on key areas of risk and opportunity, to support

stronger climate-related decision-making.

OPTIONS

37 Two options

have been identified.

Option One – Investigate ways to align DCC climate-related

risk management more closely with the NZ Climate Standards (Recommended Option)

38 Under this

option, the Zero Carbon and Climate Adaptation and Resilience teams investigate

ways the DCC could align more strongly with the NZ Climate Standards approach

to climate-related risk management. Staff would report their findings back to

the Audit, Risk and Assurance Subcommittee, no later than July 2026.

Advantages

· If

stronger alignment is ultimately realised, the approach is likely to afford

Council/ELT deeper insights on key areas of climate-related risk and

opportunity, supporting stronger climate-related decision-making.

· If

stronger alignment is ultimately realised, the approach would bring the

DCC’s approach more in line with best practice.

· Stronger

alignment would contribute to a range of direct and indirect benefits for

council and our communities, including in terms of avoided costs that would

otherwise be anticipated the impacts of climate change, and opportunities

associated with a planned and coordinated transition to a low carbon economy.

Disadvantages

· If

strongly alignment is ultimately realised, work associated with implementation

(including initial scenario development and analysis, risk/opportunity

identification and impact assessment) is likely to involve increased draw on

staff capacity. It is unknown at this point whether this could be absorbed

within existing team capacity.

Option Two – Continue with existing approach to

management of climate-related risk (Status Quo)

39 Under this

option, ELT’s current approach to climate-related risk management will

continue (currently monitoring three strategic risks).

40 The Zero

Carbon and Climate Adaptation and Resilience teams will continue to draw on OAG

advice to inform their evolving work programmes, and associated advice to

ELT/Council.

Advantages

· An

extension of business-as-usual that can be managed within existing resourcing.

Disadvantages

· DCC

climate-related risk management and associated decision-making will continue to

be less well aligned with best practice than what might be realised under

Option One.

· There

is a higher chance that climate-related risks and opportunities may remain

unaddressed/unrealised.

· DCC

and Dunedin city are likely to face costs associated with the impacts of

climate change that might otherwise be avoidable and forego opportunities associated

with a planned and coordinated transition to a low carbon economy.

NEXT STEPS

41 Should the

Committee endorse investigation of ways the DCC climate-related risk management

regime more strongly aligned with the NZ Climate Standards, the Zero Carbon and

Climate Adaptation and Resilience teams will work together to progress this,

reporting back to Audit, Risk and Assurance Subcommittee no later than July

2026.

Signatories

|

Author:

|

Jinty MacTavish - Manager - Zero Carbon

Jonathan Rowe - Programme Manager, South Dunedin Future

Tania Cribb - Risk Manager

|

|

Authoriser:

|

Scott MacLean - General Manager, City Services

|

Attachments

|

|

Title

|

Page

|

|

⇩a

|

Summary of strategic

climate-related risks currently monitored by DCC

|

61

|

|

⇩b

|

DCC climate risk

actions mapped against OAG recommendations

|

67

|

|

SUMMARY OF CONSIDERATIONS

|

|

Fit with purpose of Local Government

Strong climate-related risk management

promotes the social, economic and environmental well-being of communities in

the present and for the future.

|

|

Fit with strategic framework

|

|

Contributes

|

Detracts

|

Not applicable

|

|

Social Wellbeing Strategy

|

✔

|

☐

|

☐

|

|

Economic Development Strategy

|

✔

|

☐

|

☐

|

|

Environment Strategy

|

✔

|

☐

|

☐

|

|

Arts and Culture Strategy

|

☐

|

☐

|

✔

|

|

3 Waters Strategy

|

✔

|

☐

|

☐

|

|

Future Development Strategy

|

✔

|

☐

|

☐

|

|

Integrated Transport Strategy

|

✔

|

☐

|

☐

|

|

Parks and Recreation Strategy

|

✔

|

☐

|

☐

|

|

Other strategic projects/policies/plans

|

✔

|

☐

|

☐

|

Strong climate-related risk management supports

achievement of goals across most of the DCC’s strategies, as well as

the Zero Carbon Plan, Emissions Management and Reduction Plan, and Zero

Carbon Policy.

|

|

Māori Impact Statement

A critical

Treaty of Waitangi analysis was prepared previously as part of the Zero

Carbon work programme. This indicated that, in general, taking action to

reduce emissions is aligned with Treaty of Waitangi obligations because a

wide range of taonga are at risk from climate change. However, individual

projects will need to consider Te Taki Haruru and incorporate mana whenua and

mātāwaka inputs when delivered.

|

|

Sustainability

Climate change mitigation and adaptation efforts are

considered key to sustainability. ‘Climate Action’ is one of the

United Nation’s Sustainable Development Goals, reflecting the

centrality of action on climate change to the achievement of sustainable

development. Without significant cuts to emissions, climate change impacts

will further accelerate, with commensurate negative impacts on the social,

environmental, cultural and economic wellbeing of New Zealand communities.

Conversely, adaptation is essential to support community wellbeing to prepare

for impacts of climate change that are already locked in and actions to

reduce emissions generally have significant co-benefits in terms of community

wellbeing.

|

|

Zero carbon

A

strengthened climate-risk management regime is likely to support emissions reduction

at both DCC and city scale, by increasing Council and ELT oversight of

transition risks and opportunities.

|

|

LTP/Annual Plan / Financial Strategy /Infrastructure

Strategy

A strengthened climate-risk management regime would

support LTP / Annual Plan decision making.

|

|

Financial considerations

Staff can progress initial exploration of a strengthened

climate-risk management regime within existing budgets. It is unknown

at this point whether work associated with implementing a strengthened

climate risk management regime could be absorbed within existing team

capacity.

|

|

Significance

This decision is considered low significance in terms of

the Council’s Significance and Engagement Policy.

|

|

Engagement – external

There has been no external engagement.

|

|

Engagement - internal

Assurance Manager

|

|

Risks: Legal / Health and Safety etc.

This report sets out an option to deepen climate-related

risk management. Advantages and disadvantages are set out in the report.

|

|

Conflict of Interest

No conflict of interest has been identified.

|

|

Community Boards

No direct implications for Community Boards have been

identified.

|

|

|

Audit, Risk and Assurance Committee

4 December 2025

|

|

|

Audit, Risk and Assurance Committee

4 December 2025

|

|

|

Audit, Risk and Assurance Committee

4 December 2025

|

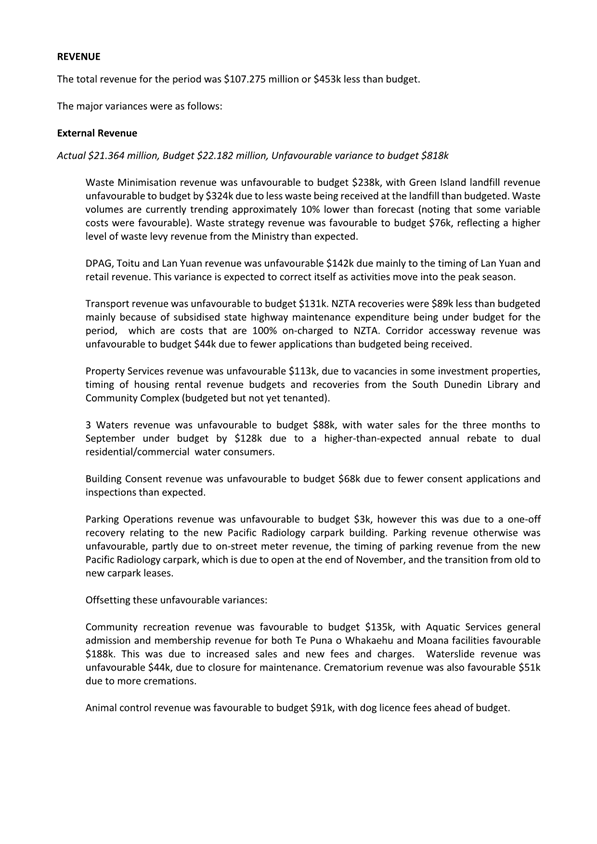

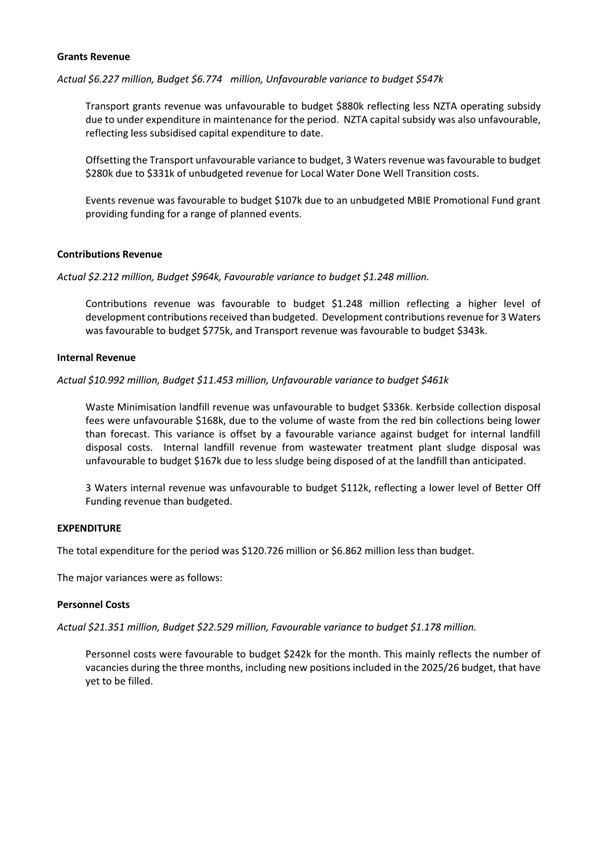

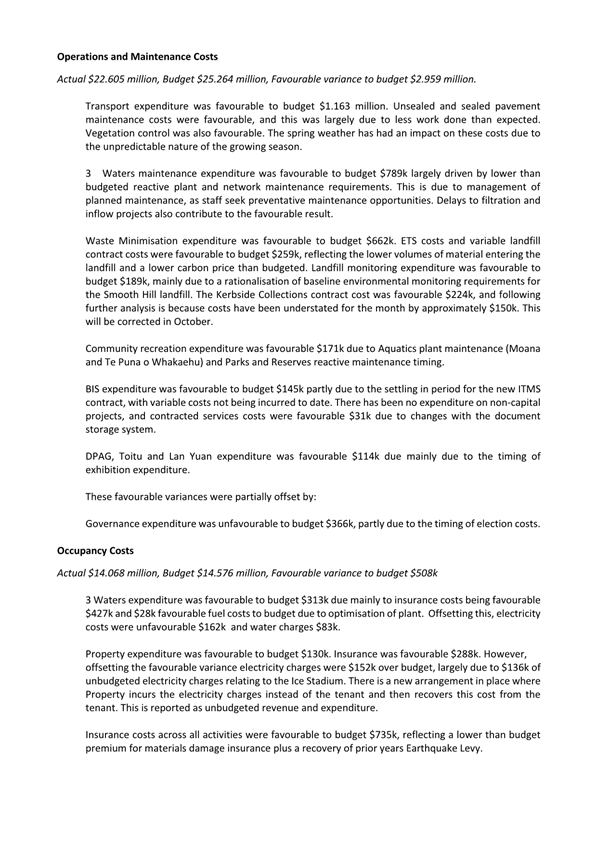

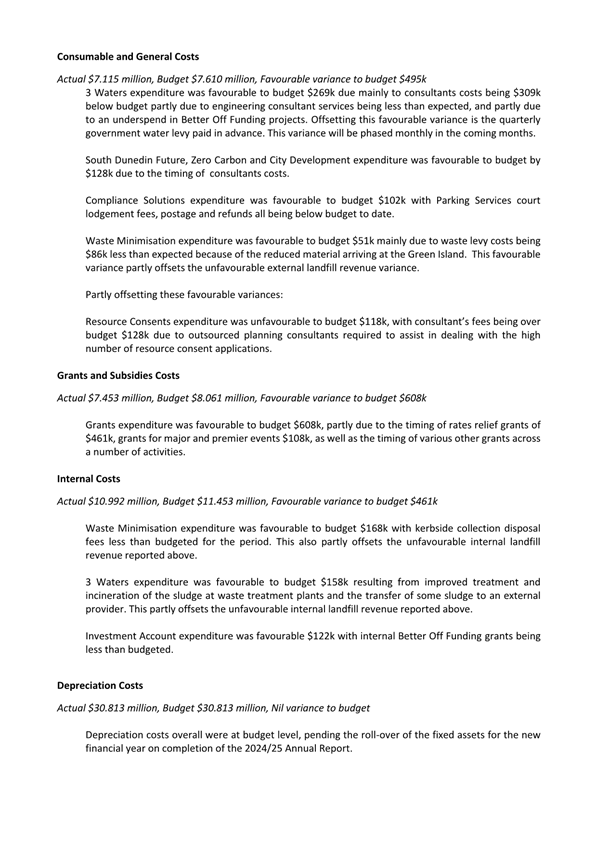

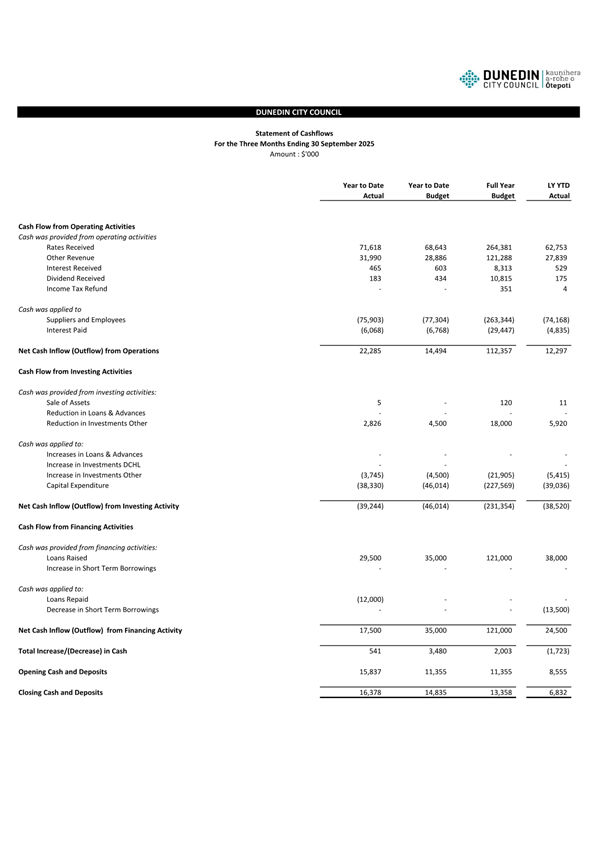

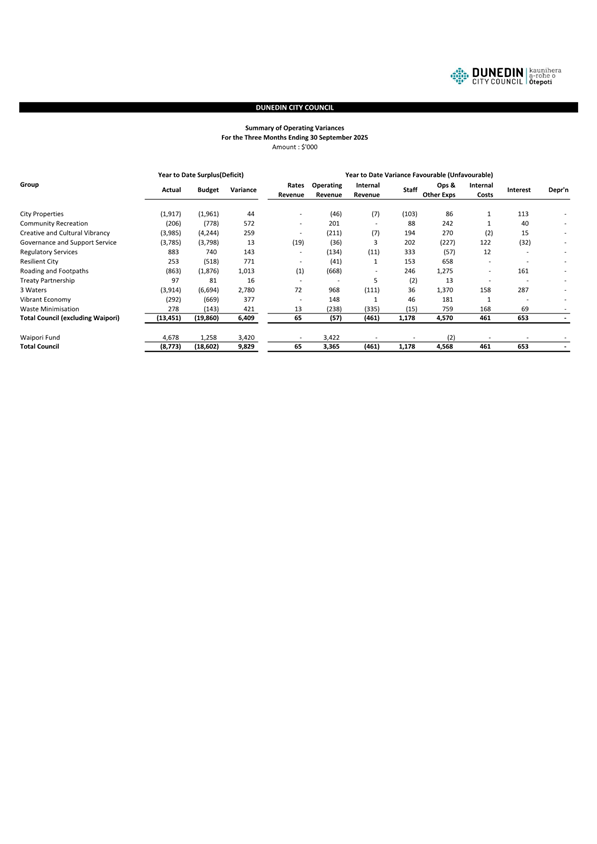

Financial Report - Period ended 30 September 2025

Department: Finance

EXECUTIVE SUMMARY

1 This

report provides the financial results for the period ended 30 September 2025

and the financial position as at that date. The report was presented to

the Council meeting held on Tuesday, 11 November 2025.

2

3 As

this is an administrative report only, there are no options or Summary of

Considerations.

RECOMMENDATIONS

That the Committee:

a) Notes the Financial

Performance for the period ended 30 September 2025 and the Financial Position

as at that date.

BACKGROUND

4 This

report attaches a financial update and financial statements for the period

ended 30 September 2025.

DISCUSSION

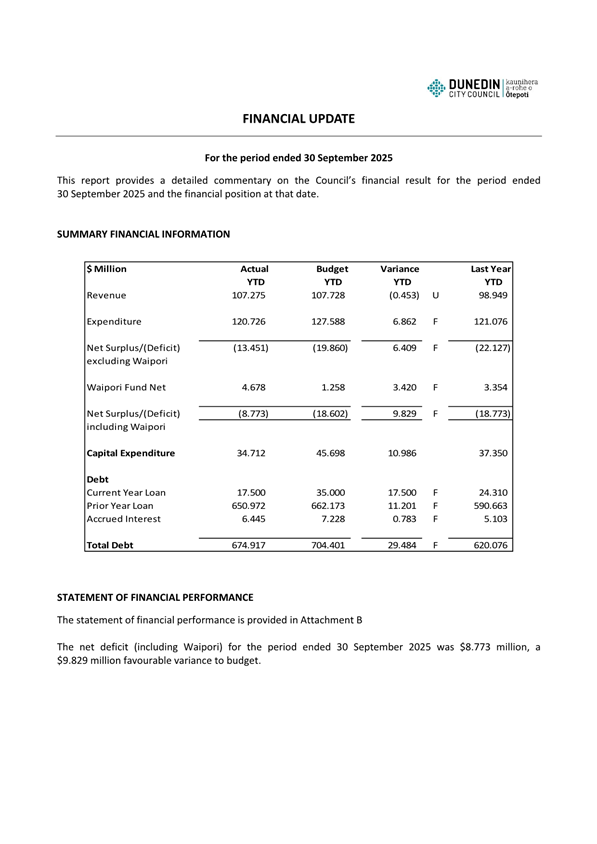

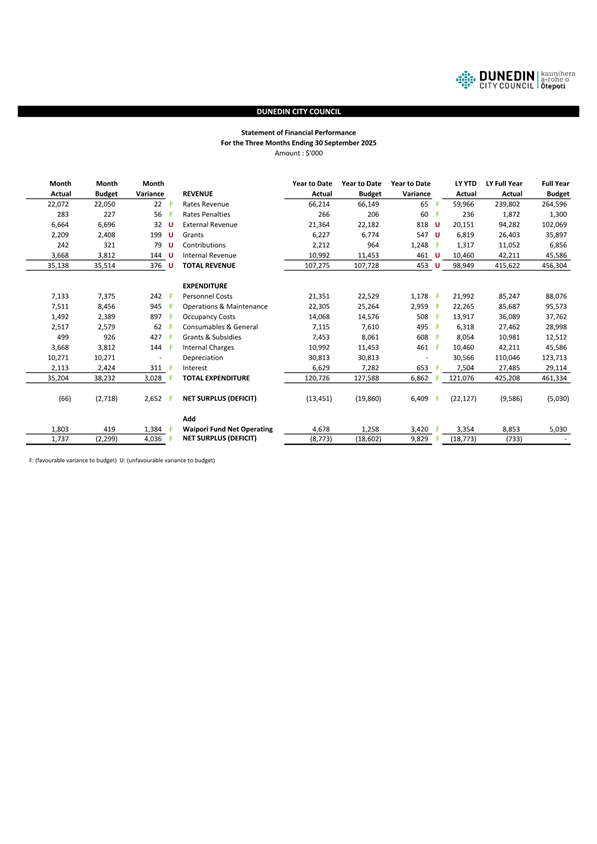

5 The

net deficit (including Waipori) for the period ended 30 September 2025 was $8.773

million, a $9.829 million favourable variance to budget. A detailed commentary is provided in Attachment A (Financial Update). In summary, the

following variances were recorded:

a) Revenue

was $107.275 million for the period or $453k unfavourable to budget.

b) Expenditure

was $120.726 million for the period, or $6.862 million favourable to budget.

c) The

Waipori Fund has reported a net operating surplus for the period of $4.678

million, $3.420 million favourable to budget.

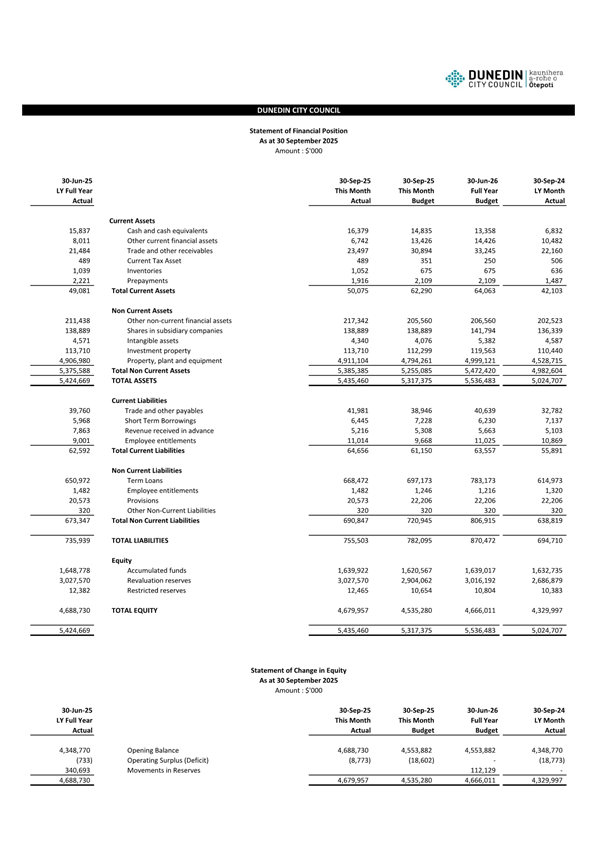

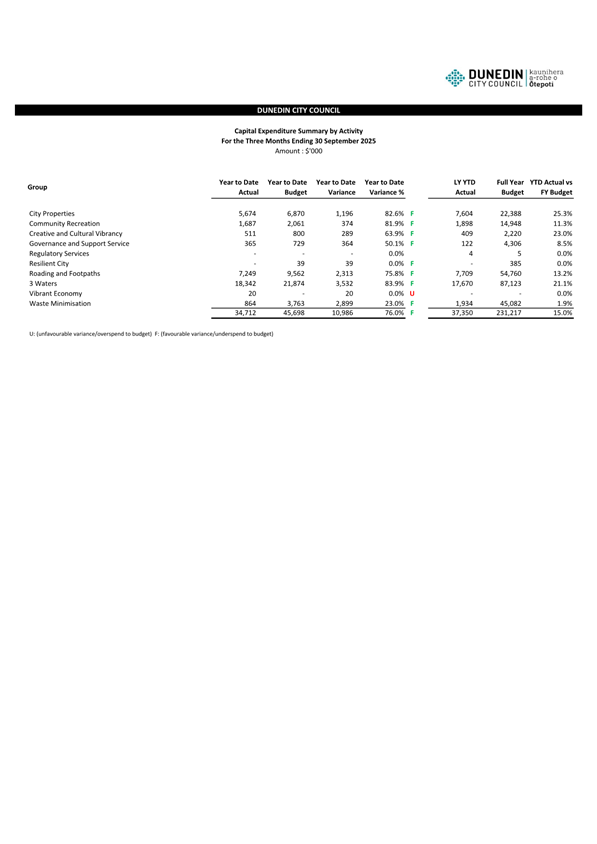

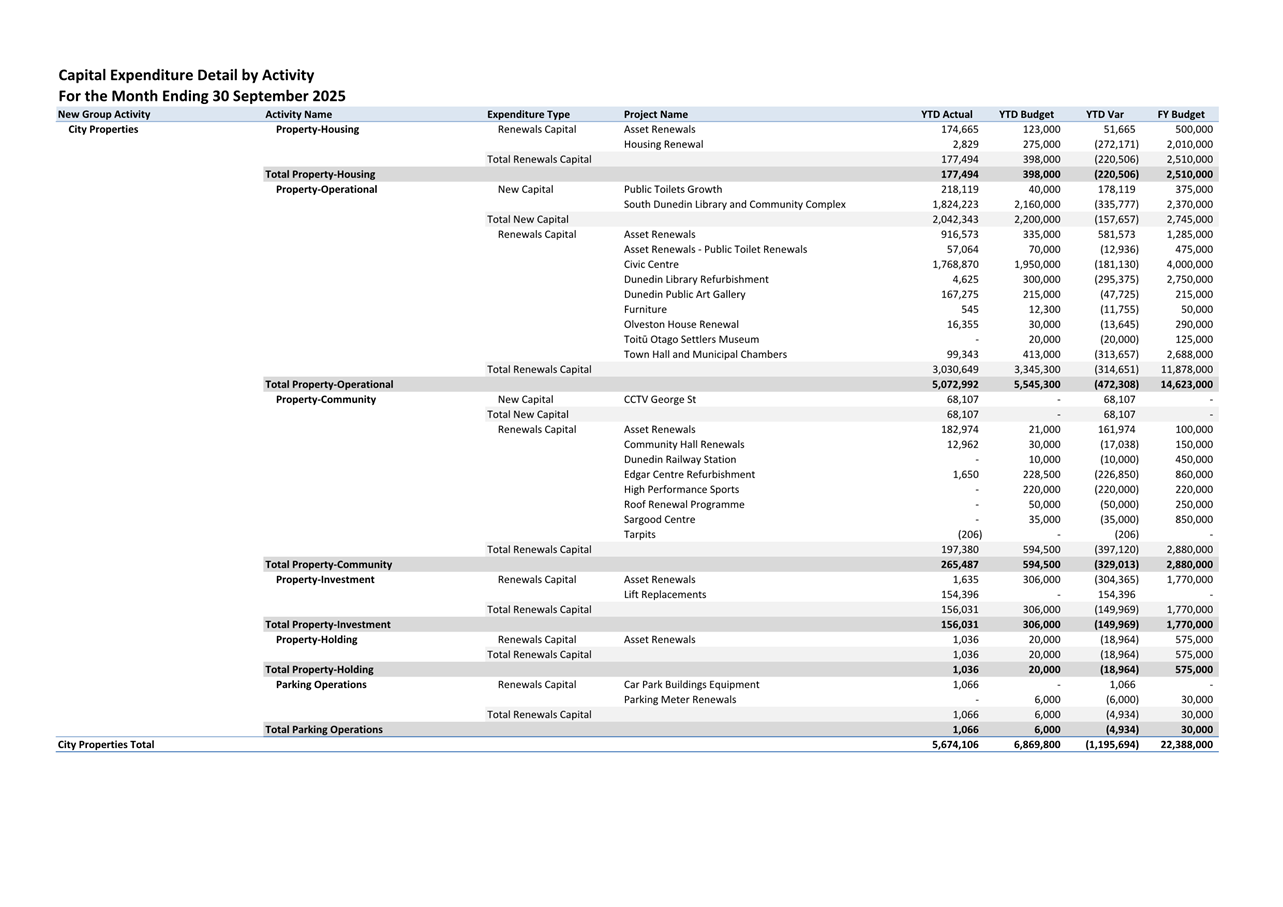

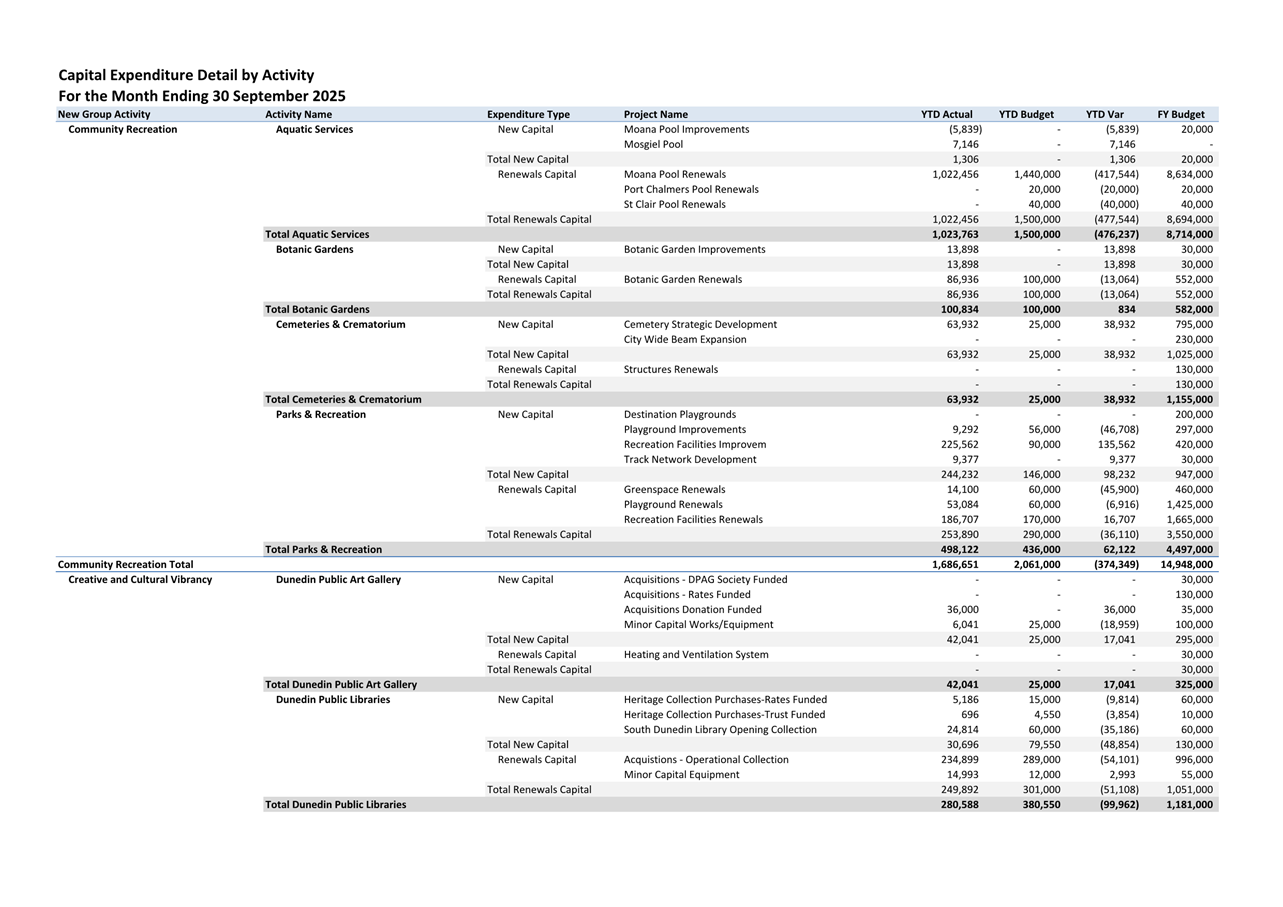

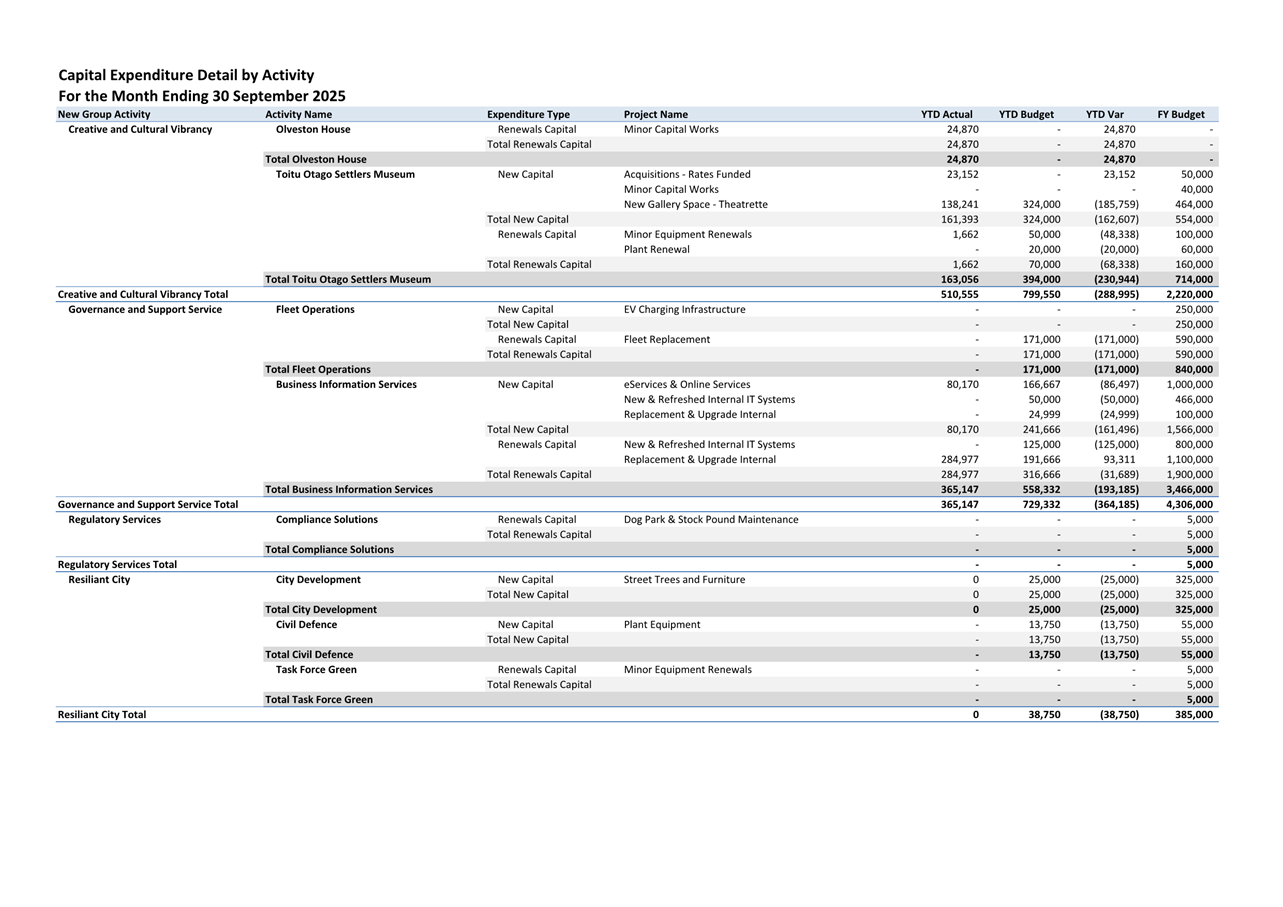

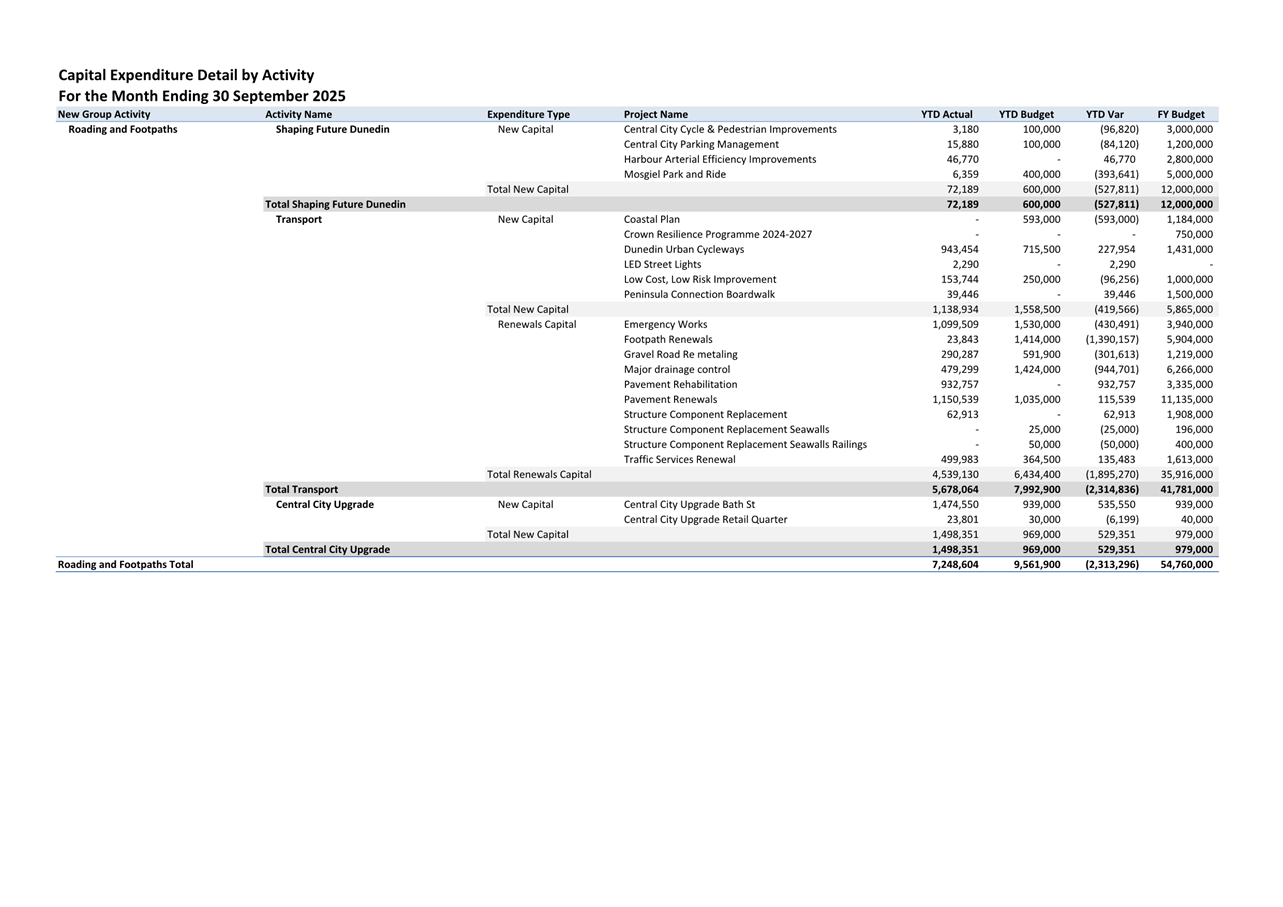

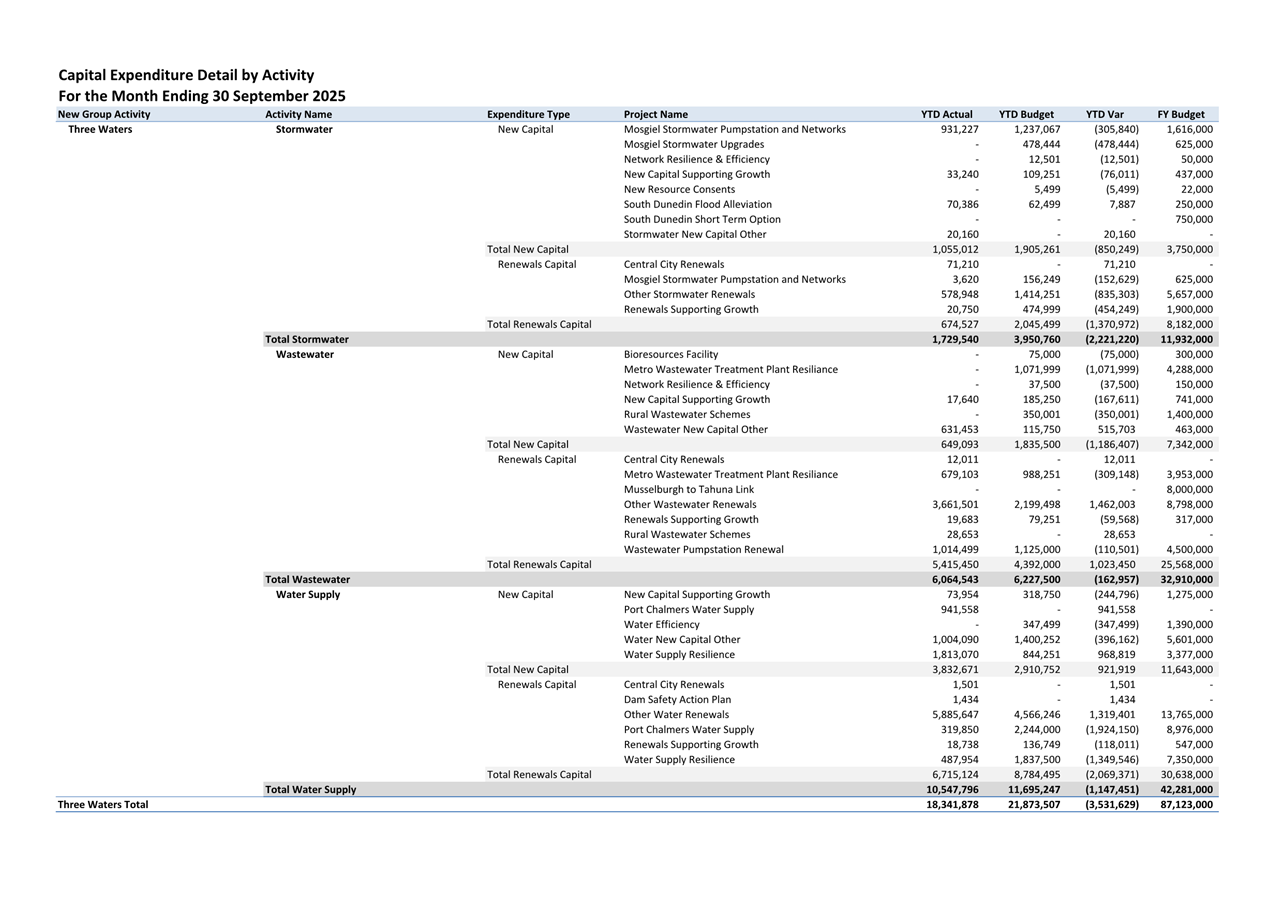

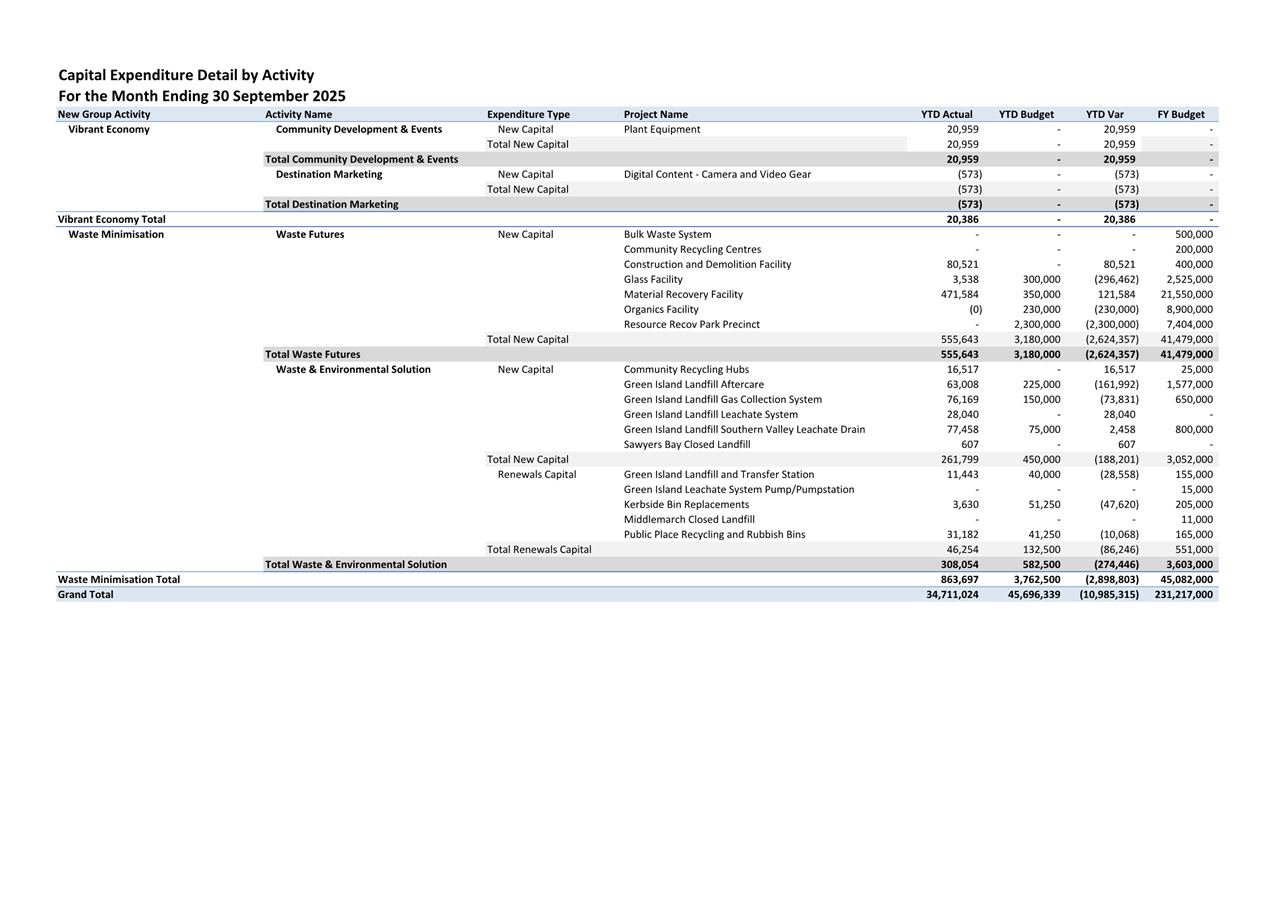

6 Capital

expenditure was $34.712 million for the period ended 30 September 2025 or 76.0%

of the year-to-date budget.

7 The

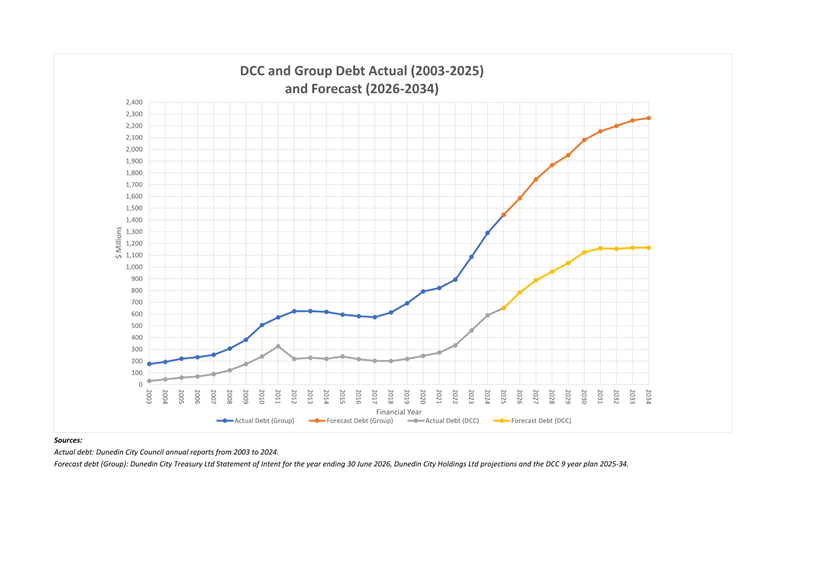

total loan balance at 30 September 2025 was $668.472 million which was $28.701

million less than budget.

OPTIONS

8 As

this is an administrative report only, there are no options provided.

NEXT STEPS

9 Month

end financial reports continue be presented to future Council meetings.

Signatories

|

Author:

|

Lawrie Warwood - Financial Analyst

|

|

Authoriser:

|

Hayden McAuliffe - Financial Services Manager

Carolyn Allan - Chief Financial Officer

|

Attachments

|

|

Title

|

Page

|

|

⇩a

|

Financial Update

|

72

|

|

⇩b

|

Statement of Financial

Performance

|

83

|

|

⇩c

|

Statement of Financial

Position

|

84

|

|

⇩d

|

Statement of Cashflows

|

85

|

|

⇩e

|

Capital Expenditure

Summary

|

86

|

|

⇩f

|

Capital Expenditure

Detailed

|

87

|

|

⇩g

|

Summary of Operating

Variances

|

93

|

|

⇩h

|

Debt Graph

|

94

|

|

|

Audit, Risk and Assurance Committee

4 December 2025

|

|

|

Audit, Risk and Assurance Committee

4 December 2025

|

|

|

Audit, Risk and Assurance Committee

4 December 2025

|

|

|

Audit, Risk and Assurance Committee

4 December 2025

|

|

|

Audit, Risk and Assurance Committee

4 December 2025

|

|

|

Audit, Risk and Assurance Committee

4 December 2025

|

|

|

Audit, Risk and Assurance Committee

4 December 2025

|

|

|

Audit, Risk and Assurance Committee

4 December 2025

|

|

|

Audit, Risk and Assurance Committee

4 December 2025

|

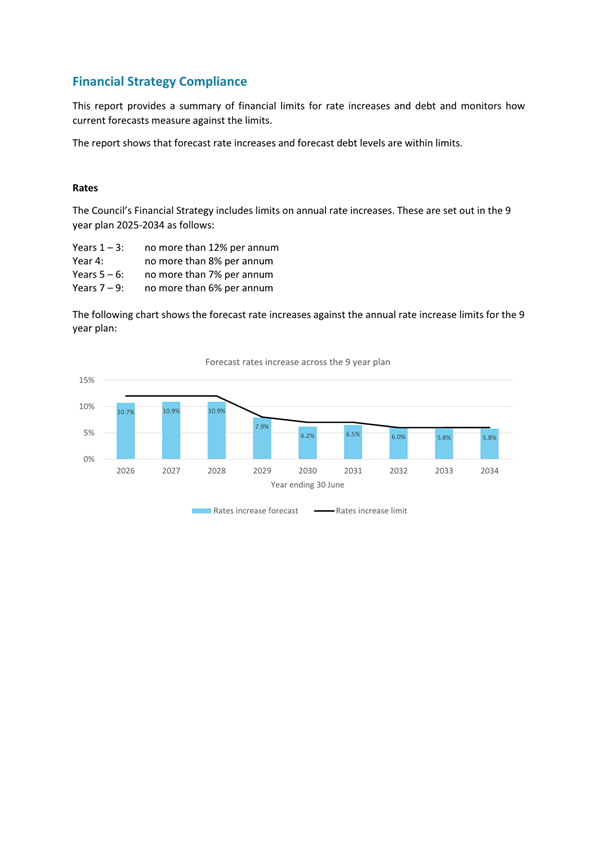

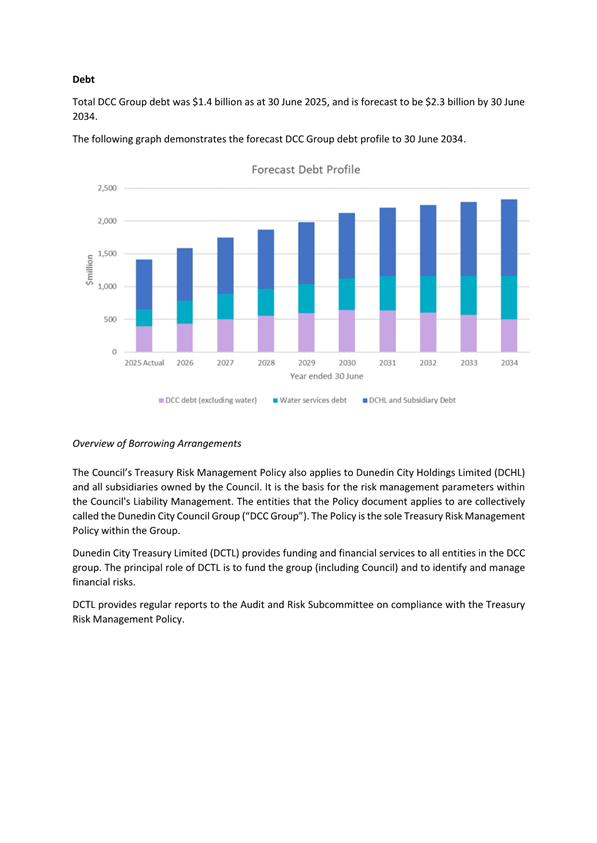

Financial Strategy Compliance - November 2025

Department: Finance

EXECUTIVE SUMMARY

1 The

attached report provides a summary of rate and debt limits, including group

debt limits. The purpose of the report is to monitor compliance against

these limits.

2 As

this is an administrative report only, the Summary of Considerations is not

required.

RECOMMENDATIONS

That the Committee:

a) Notes the Financial

Strategy Compliance – November 2025.

BACKGROUND

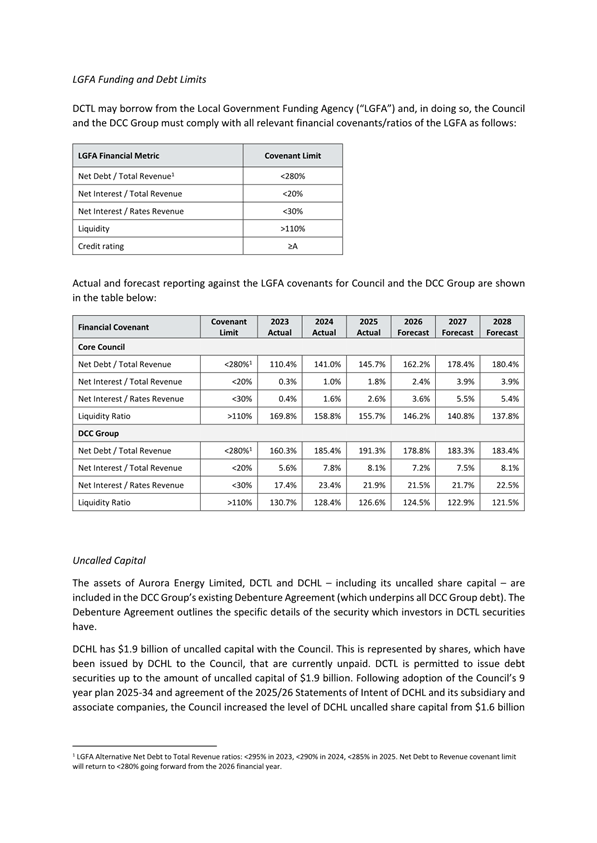

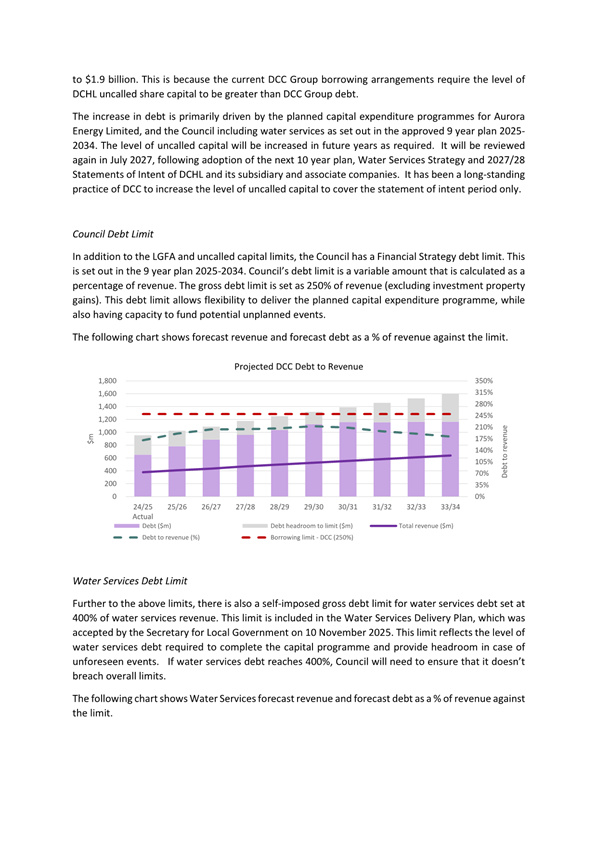

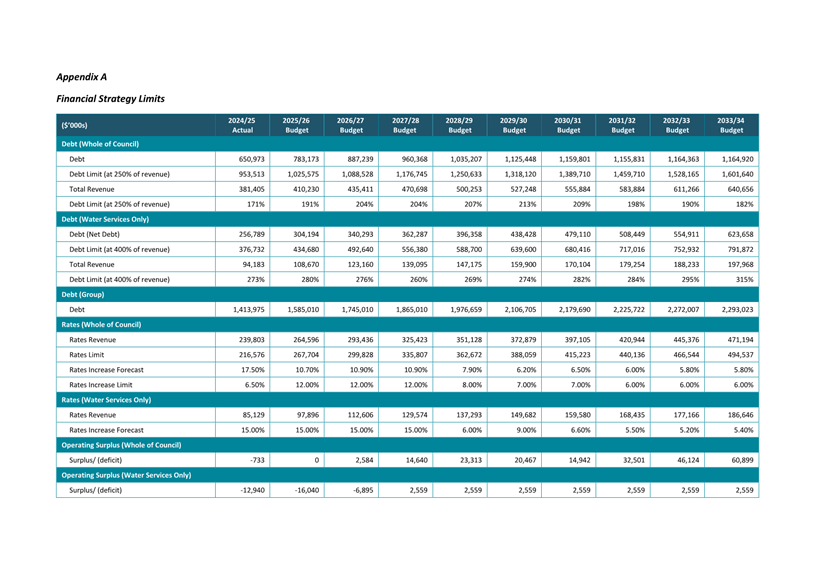

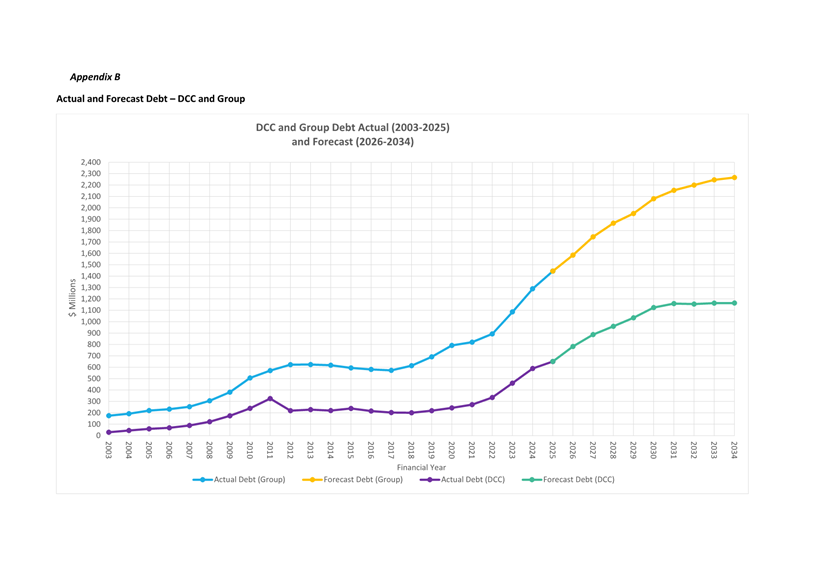

3 The

report provided in Attachment A shows compliance with Financial Strategy limits

and group debt limits. It summarises rates and debt limits as well as forecast

rates and debt levels for the period of the 9 year plan. Actual financial

information for the year ended 30 June 2025 is also now provided.

4 The

report uses financial forecasts from the 9 year plan, the Dunedin City Treasury

Limited Statement of Intent for the year ending 30 June 2026 and Dunedin City

Holdings Limited projections as at 30 June 2025.

NEXT STEPS

5 Financial

Strategy Compliance Reports will be provided quarterly to the Audit, Risk and

Assurance Committee.

Signatories

|

Author:

|

Tony Nelmes - Project Accountant

|

|

Authoriser:

|

Carolyn Allan - Chief Financial Officer

|

Attachments

|

|

Title

|

Page

|

|

⇩a

|

Financial Strategy

Compliance

|

96

|

|

|

Audit, Risk and Assurance Committee

4 December 2025

|

|

|

Audit, Risk and Assurance Committee

4 December 2025

|

Elected Member Gifts and Hospitality - Guidance

Department: Finance

EXECUTIVE SUMMARY

1 This

report provides an overview to the Audit, Risk and Assurance Committee (ARAC)

of the management of gifts and hospitality offered to elected members.

RECOMMENDATIONS

That the Committee:

a) Notes the Elected

Member Gifts and Hospitality – Guidance report.

BACKGROUND

2 The

offer of gifts and/or hospitality from third parties can constitute a personal

thank you or be appropriate for relationship management because of the nature

of the elected members role. However, gifts and/or hospitality offered by third

parties can create an actual, potential, or perceived conflict of interest.

3 By

managing conflicts of interest, the DCC ensures that all decision-making

processes and business activities cannot be justifiably challenged based on any

actual, potential, or perceived bias, or conflict of interest. Guidance has

been provided by the Office of the Auditor General on the management of

conflicts of interest and includes a scenario regarding gifts and hospitality

(attachment A).

4 At

a minimum the Local Government (Pecuniary Interests Register) Amendment Act

2022 requires elected members to declare gifts and hospitality valued at or

over $500.

5 The

Dunedin City Council has a limit for elected members of $50 for declaration as

per the code of conduct - https://www.dunedin.govt.nz/resources/documents/council/mayor-and-councillors/mayor/Code-of-Conduct-Oct-2019.pdf

6 The

$50 limit aligns with the DCC staff policy, and the table below captures the

limits for elected members from some of the other local authorities.

|

Local Authority

|

Limit for declaration

|

|

Ashburton District Council

|

$500

|

|

Christchurch City Council

|

$500

|

|

Queenstown Lakes District

Council

|

$500

|

|

Wellington City Council

|

$500

|

|

Hamilton City Council

|

$150

|

|

Auckland City Council

|

$100

|

|

Gisborne District Council

|

$100

|

|

Dunedin City

Council

|

$50

|

|

Hastings District Council

|

$50

|

|

Hutt City Council

|

$50

|

|

Invercargill City Council

|

$50

|

|

Kāpiti

Coast District Council

|

$50

|

|

Manawatū

District Council

|

$50

|

|

Napier City Council

|

$50

|

|

Tauranga City Council

|

$50

|

DISCUSSION

7 At

a recent fraud awareness and prevention training session for elected members,

questions were raised on what is acceptable or not regarding gifts and

hospitality. It was recognised that there needs to be further guidance and a

clear process for elected members on what to do when offered gifts and

hospitality as a part of their role for the DCC. The following sections aim to

provide that clarity.

8 Gifts

and hospitality are defined as follows:

a) Gifts

can be defined as any benefit provided as a good or service an elected members

receives in association with work at the DCC, from a third party. Gifts can

include, but are not limited to:

· Bottles

of wine

· Flowers

· Prizes

won in ‘business card draws’ at DCC-funded conferences

· Tickets

to an event

· Invitations

to attend an event which has a price tag, including corporate boxes or

corporate areas at any function.

b) Hospitality

is defined as a type of gift that involves food, drink, entertainment, or a

meal. It involves being hosted by a person or organisation at an occasion or

function without the freedom to choose when, where and which guests will also

attend. Hospitality includes, but is not limited to:

· Meals

(includes breakfast, lunch, dinner) paid for the third party with business

associates or networks for any purpose.

· Corporate

hospitality surrounding events.

· Corporate

functions that are catered.

9 Any

gifts or hospitality offered at or over the value of $50 needs to be declared,

regardless of if it was accepted or not.

10 An initial

gifts and hospitality register for elected members has been set-up with elected

members required to declare to the Councillor Support email Councillor.Support@dcc.govt.nz

An electronic form is under development.

11 The elected

members gift and hospitality register will be reviewed by ARAC every quarter.

Any identified gifts and hospitality valued at or over $500 will also be

included on the relevant members pecuniary interests register.

12 Like that

of the staff gifts and hospitality register, the elected members register will

capture:

a) Date

the gift/hospitality was offered.

b) Who the

gift/hospitality was offered to.

c) The

name of the third party (company or individual).

d) Description

of gift/hospitality.

e) Estimated

value.

f) Comments

on action (accepted, declined, offered to pay etc.)

g) Any

other relevant background (e.g. known DCC supplier, known grant recipient etc.)

13 If elected

members are unsure on what is appropriate to accept or not, they should seek

guidance from the CEO, or Chair of the Audit, Risk and Assurance Committee.

OPTIONS

14 There are

no options as this is an update report.

NEXT STEPS

15 Continue

development of an electronic form for the elected members gifts and hospitality

register.

16 Circulate

this guidance to elected members.

17 Report to

ARAC the elected members gifts and hospitality register alongside the staff

register.

Signatories

|

Author:

|

Hayley Knight - Assurance Manager

|

|

Authoriser:

|

Carolyn Allan - Chief Financial Officer

|

Attachments

|

|

Title

|

Page

|

|

⇩a

|

OAG Conflicts of

Interest Guidance

|

108

|

|

|

Audit, Risk and Assurance Committee

4 December 2025

|

|

|

Audit, Risk and Assurance

Committee

4 December 2025

|

Resolution to Exclude the

Public

That the Audit, Risk and

Assurance Committee:

Pursuant to the provisions of the

Local Government Official Information and Meetings Act 1987, exclude the public

from the following part of the proceedings of this meeting namely:

|

General subject of the matter to be considered

|

Reasons

for passing this resolution in relation to each matter

|

Ground(s) under

section 48(1) for the passing of this resolution

|

Reason for

Confidentiality

|

|

C1

Treasury Risk Management Compliance Report

|

S7(2)(h)

The

withholding of the information is necessary to enable the local authority to

carry out, without prejudice or disadvantage, commercial activities.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C2

Dunedin City Holdings Ltd - Update on Audit and Risk Activity

|

S7(2)(b)(ii)

The

withholding of the information is necessary to protect information where the

making available of the information would be likely unreasonably to prejudice

the commercial position of the person who supplied or who is the subject of

the information.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C3

Report to the Council on the Audit of Dunedin City Council for year end 30

June 2025

|

S7(2)(b)(ii)

The

withholding of the information is necessary to protect information where the

making available of the information would be likely unreasonably to prejudice

the commercial position of the person who supplied or who is the subject of

the information.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C4

Finance Operational Assurance Report

|

S7(2)(h)

The

withholding of the information is necessary to enable the local authority to

carry out, without prejudice or disadvantage, commercial activities.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

The information in this

report is commercially sensitive.

|

|

C5

Risk Deep Dive: Fraud and Corruption

|

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to prejudice the supply

of similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C6

DCC External Audit Actions Update - November 2025

|

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to prejudice the supply

of similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C7

Internal Audit Workplan Update

|

S7(2)(b)(i)

The

withholding of the information is necessary to protect information where the

making available of the information would disclose a trade secret.

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to prejudice the supply

of similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

S7(2)(h)

The

withholding of the information is necessary to enable the local authority to

carry out, without prejudice or disadvantage, commercial activities.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C8

Improvement Opportunities - Actions Update

|

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to prejudice the supply

of similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C9

Protected Disclosure Register - November 2025

|

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of natural

persons, including that of a deceased person.

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to prejudice the supply

of similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

|

C10

Investigation Register - November 2025

|

S7(2)(a)

The

withholding of the information is necessary to protect the privacy of natural

persons, including that of a deceased person.

S7(2)(c)(i)

The

withholding of the information is necessary to protect information which is

subject to an obligation of confidence or which any person has been or could

be compelled to provide under the authority of any enactment, where the

making available of the information would be likely to prejudice the supply

of similar information or information from the same source and it is in the

public interest that such information should continue to be supplied.

|

S48(1)(a)

The public conduct of

the part of the meeting would be likely to result in the disclosure of

information for which good reason for withholding exists under section 7.

|

|

This resolution is made in

reliance on Section 48(1)(a) of the Local Government Official Information and

Meetings Act 1987, and the particular interest or interests protected by

Section 6 or Section 7 of that Act, or Section 6 or Section 7 or Section 9 of

the Official Information Act 1982, as the case may require, which would be

prejudiced by the holding of the whole or the relevant part of the proceedings

of the meeting in public are as shown above after each item.